China's Copper Refining Capacity Expansion Shifts Global Pricing Power, Repricing Low-Cost Developers Over Capital-Intensive Projects

China’s copper dominance reshapes pricing power, favoring low-cost developers as supply risks and rising costs challenge capital-intensive projects.

- China's refining self-sufficiency reduces the London Metal Exchange's responsiveness to Western supply disruptions, requiring investors to model copper prices against Chinese industrial policy and inventory cycles rather than marginal Western supply alone.

- The copper market is simultaneously in short-term surplus through Shanghai Futures Exchange inventory builds and long-term structural deficit tied to grid electrification, creating discrete entry windows for quality assets during macro-driven dislocations.

- Sulfuric acid supply constraints linked to Middle East shipping disruptions and Chinese export controls raise the marginal cost of solvent extraction and electrowinning production, which accounts for roughly 17% of global refined copper supply.

- Developers with permitted projects, completed definitive feasibility studies, and all-in sustaining cost visibility are attracting institutional capital ahead of explorers lacking defined economics.

- Capital discipline, measured in treasury strength and non-dilutive financing capacity, has become a primary screening criterion for institutional allocators across the junior and mid-tier copper space.

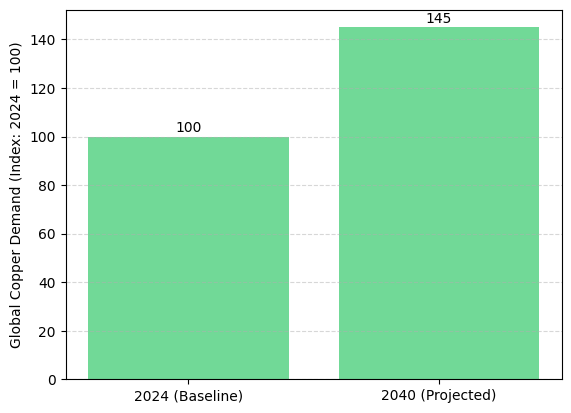

Shanghai Futures Exchange inventories rose sharply through 2025 while Chinese refined copper imports declined, pointing to a near-term surplus dynamic. At the same time, the International Energy Agency's Critical Minerals Outlook 2024 projects copper demand growth of 40% to 50% by 2040 under its Announced Pledges scenario, driven by grid infrastructure renewal, electric vehicle deployment, and data center electrification.

China's refining capacity expansion has changed who sets the marginal price of refined copper, and the shift is flowing through to how equity investors value producers, developers, and explorers. Copper price signals are becoming less responsive to Western supply disruptions and more responsive to Chinese inventory cycles, US dollar against Chinese yuan currency moves, and industrial policy decisions. The result is a bifurcated capital market, with institutional flows concentrating on assets carrying defined economics and near-term production visibility while discount rates widen against long-dated, capital-intensive projects.

The Shift in Global Copper Price

Copper pricing has historically been set at the London Metal Exchange, with the marginal tonne of Western mine supply clearing against Chinese refined copper imports. China's domestic smelting and refining capacity has expanded faster than its mine supply growth, and the country transitioned to a net exporter of refined copper during 2025. Shanghai Futures Exchange inventory builds through the year signaled that domestic supply was outpacing immediate demand, reducing import urgency and weakening the transmission mechanism between Western supply disruptions and global price.

Copper price discovery is now occurring across two reference points, the London Metal Exchange and the Shanghai Futures Exchange, with the latter increasingly driving directional moves. Western supply disruptions still matter, but their price impact is dampened when Chinese inventories are elevated and domestic refining runs above import parity. Currency dynamics amplify this effect, because a stronger US dollar raises the yuan cost of imported concentrate and compresses refined copper affordability in emerging markets.

Copper now behaves more like a macro-sensitive asset than a pure supply-demand commodity. Portfolio construction in copper mining must account for US Federal Reserve interest rate cycles, dollar-yuan volatility, and Chinese industrial policy alongside traditional grade-and-tonnage fundamentals.

Geopolitics & Supply Chain Fragility Raise the Cost Curve

Sulfuric acid is now a material variable in the cost curve, and its availability is increasingly constrained by geopolitics. Sulfuric acid is essential for solvent extraction and electrowinning production, which accounts for approximately 17% of global refined copper supply and is concentrated in Chile, Peru, and the Democratic Republic of the Congo. Shipping disruptions through the Strait of Hormuz, combined with export restrictions imposed by China and Turkey during 2024 and 2025, tightened the global sulfuric acid market and raised landed costs for Chilean and Congolese operators.

The broader supply-side pressure facing Chile, the world's largest copper-producing country at roughly 5.3 million tonnes in 2023 according to the US Geological Survey, reinforces this dynamic. Declining head grades, rising energy input costs, and permitting delays have raised sustaining capital requirements for legacy operations.

Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, frames the structural cost pressure:

“Production growth within Chile is difficult; it is struggling to maintain output. Vast amounts of capital are being deployed just to sustain production. As a result, metal prices have to materially re-rate.”

Margin compression is most acute for high-cost producers dependent on imported chemical inputs and legacy infrastructure, while low-cost oxide operators with secure acid supply and competitive energy contracts retain pricing power.

Short-Term Surplus & Long-Term Deficit

In the near term, Chinese property sector weakness, moderated electric vehicle subsidy support, and Shanghai Futures Exchange inventory builds are producing surplus conditions. Refined copper has traded in a defined range through 2025, and physical delivery premiums have softened from 2023 highs.

Over the longer horizon, the International Energy Agency projects copper demand growth of 40% to 50% by 2040 under its Announced Pledges scenario, driven by transmission capacity expansion, electric vehicle fleet rollout, and data center electrification. Mine supply growth is unlikely to match this demand profile. Global reserve grades are declining, new discoveries are smaller and deeper, and permitting timelines in Tier-1 jurisdictions routinely exceed a decade.

Short-term traders face a range-bound market sensitive to Chinese macro data and US dollar moves. Long-term allocators are targeting entry during macro-driven dislocations, with a preference for assets that can reach production before the structural deficit tightens in the late 2020s.

How Developers Are Positioning for Capital Discipline

Marimaca Copper is advancing the Marimaca Oxide Deposit in Chile's Antofagasta Region. The project's definitive feasibility study, completed in 2025, delivered industry-competitive capital intensity and all-in sustaining cost metrics, and environmental approvals have been secured ahead of a targeted 2026 construction start. The oxide-first strategy uses heap leach and solvent extraction and electrowinning processing to reduce upfront capital expenditure and shorten the path to cash flow, with a sulphide expansion preserved as an internally funded growth option.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, places the project within the broader asset economics:

“Confirmed what we already knew: industry-leading capital costs, very competitive operating costs, and industry-leading returns on invested capital.”

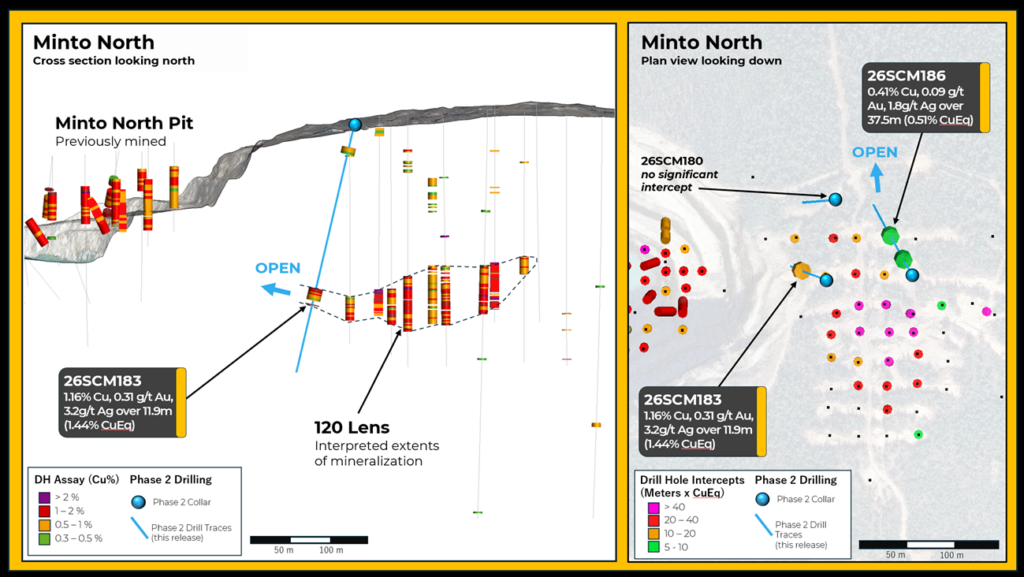

Cobra Resources is advancing the Manna Hill Copper Project in South Australia's Nakra Arc, an analogous setting to Cadia Valley. The project delivered intercepts of 48 meters grading 2.2% copper and 0.76 grams per tonne gold from 11 meters depth. Shallow ore bodies reduce mining costs and upfront capital requirements, positioning the project toward the lower end of cost curves. The adjacent Netley Hill Prospect hosts a 3-kilometer-long geophysical anomaly with shallow copper-molybdenum mineralization from surface, including 350 meters of continuous mineralization downhole, providing district-scale exploration potential.

Explorers & Optionality on Discovery Leverage

Advanced exploration companies provide leverage to resource growth and discovery in a structurally tightening supply backdrop. The risk-reward profile is distinct from developers, with valuations driven by drill results, resource expansion, and metallurgical outcomes rather than defined project economics. The investor base skews toward specialist funds and sophisticated retail allocators comfortable with pre-economic assets.

Abitibi Metals, advancing the B26 polymetallic deposit in Quebec, illustrates the model. Resource growth has been delivered at low discovery cost, and the system remains open along strike and at depth.

Jon Deluce, Chief Executive Officer of Abitibi Metals Corp, quantifies the scale potential and capital efficiency:

“We’re up over 125% in terms of tonnage growth. This could very well be a 30-50 million tonne deposit, achieved at a discovery cost of 2.5 cents per pound of copper equivalent.”

Producers evaluating acquisition pipelines are favoring copper-gold deposits, particularly volcanogenic massive sulphide systems, because multi-commodity revenue streams provide a natural hedge against single-commodity price volatility.

Capital Allocation in a Bifurcated Market

Developers with permitted projects, completed definitive feasibility studies, and defined all-in sustaining cost profiles are attracting institutional capital. Explorers without defined economics are funded primarily by specialist funds and retail investors, with valuations driven by drill result momentum and broader risk sentiment.

Three factors are decisive in institutional screening. First, cost curve position, where assets in the lower half of the global all-in sustaining cost curve carry downside price protection. Second, capital expenditure intensity, where lower capex per annual tonne of copper production supports return on invested capital metrics in a higher-rate environment. Third, jurisdiction, where the Fraser Institute Policy Perception Index and permitting transparency now factor directly into discount rate assumptions.

Elevated US policy rates and the higher cost of project debt have reduced investor tolerance for long-dated, capital-intensive developments. The preference for near-term cash flow visibility is a mathematical consequence of discount rate compression across long-duration mining assets.

The Investment Thesis for Copper

- Exposure to electrification-driven structural demand growth, with the International Energy Agency projecting 40% to 50% copper demand expansion by 2040

- Asymmetric entry opportunities created by short-term Chinese surplus dynamics against long-term supply deficits

- Cost curve support from rising sulfuric acid prices across solvent extraction and electrowinning production representing 17% of global supply

- Premium valuations for low-cost oxide developers with permitted projects, completed definitive feasibility studies, and near-term production timelines

- Leveraged upside through advanced explorers delivering resource growth at low discovery cost in established mining jurisdictions

- Self-funded growth optionality through early-stage developer-explorers using near-term oxide cash flow to underwrite larger sulphide exploration

- Capital discipline measured in treasury strength and non-dilutive financing capacity as a primary institutional screening criterion

- Jurisdictional resilience in established copper-producing countries with defined permitting frameworks and integrated infrastructure

China's refining capacity expansion has shifted pricing power eastward, geopolitical constraints on chemical inputs have raised the cost curve, and the simultaneous presence of short-term surplus and long-term deficit has created a bifurcated capital market. Institutional capital is concentrating on producers and developers with defined economics, while explorers must now compete on capital efficiency and jurisdictional positioning.

The next phase of the copper cycle will not be driven by scarcity alone. It will be shaped by which operators can deliver supply efficiently in a constrained, volatile, and increasingly policy-driven market. For investors, the assessment framework must now combine macro drivers, including Chinese policy, geopolitics, and interest rates, with asset-level fundamentals, including grade, all-in sustaining cost, and production timeline.

TL;DR

China's refining capacity expansion and 2025 inventory builds have weakened the London Metal Exchange's sensitivity to Western copper supply disruptions, shifting pricing power toward Chinese industrial policy and currency dynamics. Combined with sulfuric acid supply constraints raising the global cost curve, the result is a bifurcated capital market that rewards low-cost developers with permitted projects and defined economics while pressuring capital-intensive, long-dated assets. Advanced explorers and early-stage developer-explorers retain discovery leverage but must demonstrate capital efficiency and jurisdictional quality to attract institutional flows.

FAQs (AI-generated)

China has rapidly expanded its domestic refining capacity, reducing its reliance on imported refined copper and weakening the traditional pricing mechanism dominated by the London Metal Exchange. As a result, copper prices are increasingly influenced by Chinese inventory levels, industrial policy decisions, and yuan dynamics rather than purely Western mine supply disruptions. This shift means investors must now incorporate macro variables like Chinese demand cycles and currency movements into valuation models, rather than relying solely on traditional supply-demand fundamentals.

Both, depending on the timeframe. In the short term, rising inventories on the Shanghai Futures Exchange and weaker Chinese imports point to surplus conditions, which have kept prices range-bound. However, long-term fundamentals remain tight, with global copper demand projected to grow 40-50% by 2040 due to electrification, grid expansion, and data center growth. This creates a cyclical disconnect where short-term weakness may offer entry points into a structurally bullish long-term market.

Geopolitics is increasingly shaping the copper cost curve, particularly through constraints on sulfuric acid, a critical input for solvent extraction and electrowinning (SX-EW) production. Shipping disruptions and export restrictions have tightened supply, raising input costs for producers in key regions like Chile and the DRC. These pressures disproportionately impact higher-cost operators, while low-cost producers with secure supply chains retain stronger margins and pricing resilience.

In a higher interest rate environment, investors are prioritizing projects with near-term cash flow visibility and defined economics. Developers with completed feasibility studies, permitting progress, and clear all-in sustaining cost (AISC) profiles offer lower execution risk and more predictable returns. In contrast, explorers, while offering higher upside, carry greater uncertainty around resource size, metallurgy, and financing, making them more sensitive to market sentiment and capital availability.

Investors should focus on three key factors: cost position (preferably in the lower half of the global cost curve), capital intensity (lower capex per tonne improves returns), and jurisdictional stability (clear permitting and infrastructure access). Additionally, capital discipline, such as strong balance sheets and non-dilutive funding strategies, has become a critical differentiator. In today’s market, success depends on aligning macro awareness with asset-level fundamentals, particularly timing projects to come online before the expected supply deficit intensifies.

Analyst's Notes

Subscribe to Our Channel

Stay Informed