'Undervalued?' Northisle Copper & Gold Pushes PFS With Big Financing, Big Exploration & Bigger Ambition

Northisle: $5B NPV copper-gold project trading 0.3x NAV. $150M funded PFS, BC gov't priority, Wheaton backed. 40km district exploration upside. Q2 catalysts pending.

- Northisle Copper & Gold raised over $150 million over six months to advance its British Columbia copper-gold project through pre-feasibility study, following designation as a top provincial priority for critical minerals development

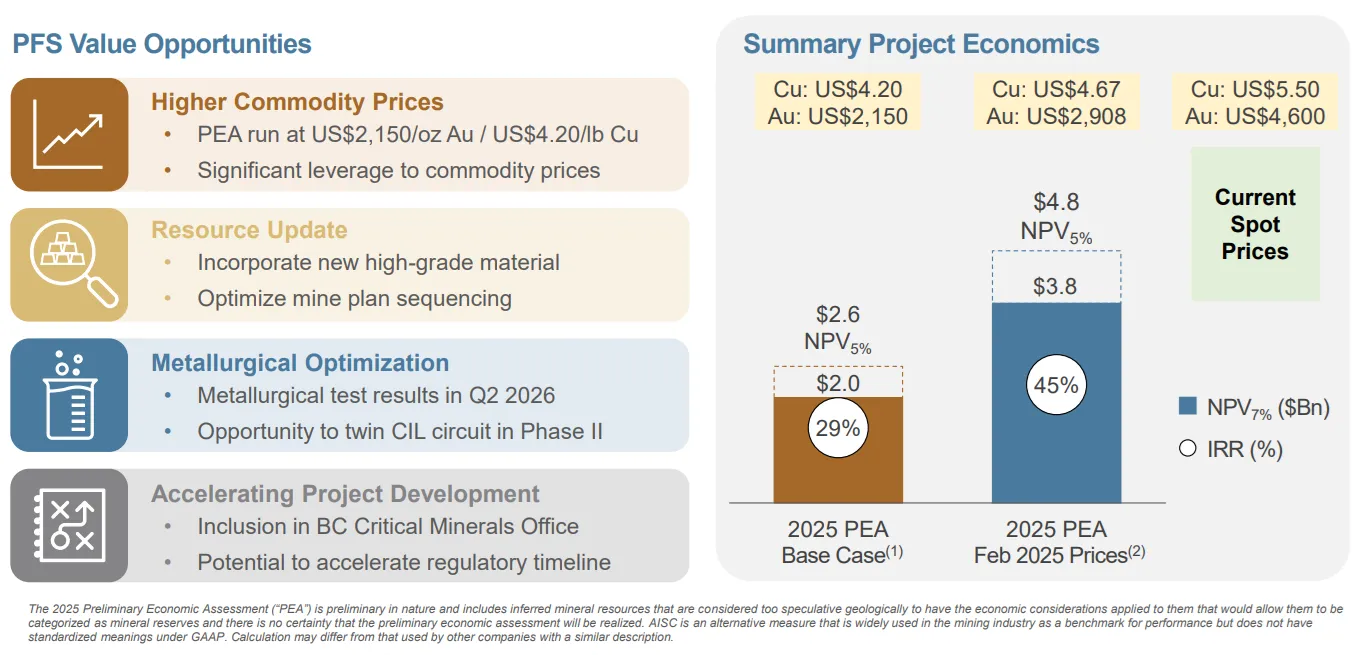

- Company currently trades at 0.3x analyst consensus NAV, well below the typical 0.4-0.7x range for pre-feasibility stage projects, with PEA showing $5 billion after-tax NPV that could expand significantly under current commodity price consensus ($3,400 gold vs. $2,150 used in PEA)

- The investment case combines systematic de-risking of the flagship project through feasibility work with a "free call option" on district-scale exploration across a 40km land package in a 50km porphyry district

- Three parallel workstreams aim to improve economics: incorporating the 1.2km West Goodspeed discovery (0.7-1% copper equivalent at surface), optimising metallurgical recoveries through potential CIL plant twinning (from 63% to potentially 80% gold recovery in Phase 2), and accelerating permitting timelines

- Management plans to fund development through diversified sources including streams/royalties with Wheaton Precious Metals (cornerstone investor), strategic off-takes with Exim Bank debt, government partnerships, and selective equity raises, targeting 3-5x returns on any dilution

Northisle Copper & Gold is advancing one of British Columbia's largest undeveloped copper-gold districts at a pivotal moment for critical minerals development in Canada. With over $150 million in recent financings and provincial government designation as a top-priority project, the company is executing a dual strategy: systematically de-risking its flagship deposit toward production while exploring a 40-kilometer district with world-class potential. This analysis examines the company's value proposition, growth opportunities, and path to development.

Provincial Priority Status Unlocks Capital

The British Columbia government's February designation of Northisle as a top priority within its Critical Minerals Office represents a fundamental shift in the project's development trajectory.

This government endorsement catalysed the company's ability to raise about $155 million in capital over six months, $39.5M closed financing in August last year and another $115M in January 2026 providing the resources to advance rapidly through pre-feasibility study. The market's willingness to provide substantial capital at this stage signals institutional confidence in both the project's technical merits and the company's execution capabilities.

The validation extends beyond government support. Wheaton Precious Metals, the world's largest precious metals streaming company and British Columbia's largest public company, has emerged as a cornerstone investor in Northisle's recent financing rounds. This strategic relationship positions the company to access favorable capital structures typically reserved for major mining operations.

Trading Below Pre-Feasibility Valuation Band

Northisle currently trades at approximately 0.3 times analyst consensus net asset value, positioning it within the typical range for preliminary economic assessment-stage projects (0.2-0.4x NAV) but below the 0.4-0.7x range associated with pre-feasibility study-stage assets. As the company advances through de-risking milestones, this multiple should expand toward the higher end of the pre-feasibility range and eventually approach 1.0x as the project nears final investment decision.

The company's February 2025 PEA demonstrated $5 billion in after-tax NPV using $2,900 gold and $4.60 copper prices to which at the time that were lower than long-term analyst consensus. Current pricings stands substantially higher than the PEA assumptions and suggesting significant upside to the published economics.

Three Pathways to Enhanced Economics

The Northisle project demonstrates robust economics with a 45% after-tax internal rate of return in the PEA scenario. The development plan encompasses two phases: an initial 40,000 tons-per-day concentrator operation followed by expansion to 80,000 tons per day, funded entirely by Phase 1 cash flows within the first 12-18 months of operation.

Three parallel initiatives aim to enhance project economics beyond PEA levels. First, the West Goodspeed discovery in a 1.2-kilometer zone shows 0.7-1% copper equivalent grades at surface will be incorporated into updated resource estimates by Q2 2026. This zone is nearly twice the length of the Red Dog deposit already included in the PEA and features zero strip ratio with high-grade mineralisation beginning at surface.

Second, metallurgical optimisation work focuses on recovery improvements. The current PEA assumes 80% gold recovery in Phase 1 but only 63% in Phase 2, as the initial design did not twin the CIL (carbon-in-leach) plant due to gold price assumptions of $2,150 per ounce. With current consensus at $3,400 per ounce, the company is studying the economics of twinning the CIL plant to maintain 80% gold recovery in Phase 2, which would significantly enhance revenue.

Third, the company is working with provincial and First Nations partners to accelerate permitting timelines, potentially contracting the typical four-year timeline and improving the project's net present value through earlier cash flow generation.

Interview with Sam Lee, CEO, Northisle Copper & Gold

District-Scale Exploration Opportunity

Beyond the flagship project, Northisle controls 40 kilometers of a 50-kilometer porphyry district that historically produced copper from BHP's Island Copper mine. CEO Sam Lee characterises this exploration potential as a "free call option" that doesn't factor into current valuations but offers transformational upside.

The company has inherited 70 years of exploration data from seven predecessor companies, including comprehensive magnetic and induced polarization surveys, surface sampling that would cost $40 million to replicate today, and stream sediment data. Current deposits - Northwest Expo, Red Dog, West Goodspeed, and Hushamu - were all discovered at depths less than 350 meters and show high-grade mineralisation at or near surface.

The exploration strategy focuses on identifying 1% copper equivalent mineralisation over 1,000 meters depth - the threshold for district-scale, world-class deposits. The company has allocated $2 million to complete surface sampling and data integration work in Q2 2026, after which it will design drill programs targeting deeper, potentially larger systems using advanced data-driven targeting methodologies.

Diversified Financing Approach

Management's approach to capital allocation emphasises return on dilution, with Lee and Chairman Dale Corman maintaining 12-13% ownership to ensure alignment with shareholders. Lee articulated the disciplined framework:

"Every time we dilute equity, we have to see a three to five x return on that dilution. Otherwise, it's not worth doing."

The planned capital structure incorporates multiple sources at different costs of capital. Precious metals streaming and royalties, potentially with Wheaton Precious Metals, could provide 0-4% cost of capital. Strategic off-take agreements with Asian buyers would bring sub-2% Exim Bank project finance debt. Government funding from federal, provincial, and First Nations sources provides both capital and stakeholder alignment. Finally, strategic partnerships and selective equity raises complete the financing mix.

Lee emphasised that the project could theoretically be funded entirely through less than 1% NSR royalty but noted this wouldn't represent optimal capital structure. The high-quality product - copper-molybdenum concentrate with low deleterious elements and 58% gold reporting to concentrate, plus gold doré bars - commands premium pricing and attracts strategic interest from off-takers facing concentrate shortages.

Premium Product Addressing Concentrate Shortage

Northisle's copper concentrate addresses critical supply constraints in global smelting capacity. Smelters currently operate at 40-50% capacity due to concentrate shortages, with Chinese buyers paying negative $100-per-ton treatment charges. The company's concentrate features low arsenic (<30 ppm), low selenium, and significant gold content, making it particularly attractive to non-Chinese smelters squeezed by Chinese competition.

The gold component provides exposure to safe-haven demand during geopolitical uncertainty, while copper and molybdenum address electrification and defense requirements. This product mix positions Northisle at the intersection of multiple structural demand drivers in the critical minerals sector.

The Investment Thesis for Northisle Copper & Gold

- Valuation Opportunity: Trading at 0.3x analyst consensus NAV versus 0.4-0.7x typical for PFS-stage projects, with systematic re-rating catalyst path through de-risking milestones toward 1.0x NAV at final investment decision

- Commodity Price Leverage: PEA economics based on $2,150 gold and $4.20 copper now superseded by analyst consensus of $3,400 gold and $4.70 copper, implying substantial NPV expansion without any operational improvements

- Near-Term Catalysts: Q2 2026 updated resource estimate incorporating West Goodspeed (1.2km strike length, 0.7-1% CuEq at surface), metallurgical optimisation results on CIL plant twinning (potential to increase Phase 2 gold recovery from 63% to 80%), and accelerated permitting timeline guidance

- Government and Strategic Validation: BC government Critical Minerals Office top-priority designation; Wheaton Precious Metals cornerstone investment signals institutional confidence and positions favorable streaming/royalty financing at 0-4% cost of capital

- Premium Product in Tight Market: High-quality copper concentrate (low deleterious elements, 58% gold reporting) and gold doré addressing structural concentrate shortages with smelters operating at 40-50% capacity; Chinese buyers paying negative treatment charges create premium pricing environment

- District-Scale Optionality: 40km of 50km porphyry district provides "free call option" on world-class discovery potential; 70 years of inherited exploration data ($40M+ replacement value), data-driven targeting approach led by PhD-level team, focused on 1% CuEq over 1,000m targets

- Capital Structure Optionality: Diversified financing strategy combining streams/royalties (0-4% cost), strategic off-takes with Exim debt (sub-2%), government partnerships, and disciplined equity (3-5x return hurdle on dilution); project theoretically fundable with <1% NSR royalty

- Two-Phase Development Model: Phase 1 (40ktpd) generates cash flow to self-fund Phase 2 expansion (80ktpd) within 12-18 months, reducing external capital requirements and demonstrating operational capability before scale-up

Macro Thematic Analysis

Northisle Copper & Gold exemplifies the convergence of electrification demand, defense requirements, and supply chain security driving critical minerals policy across Western economies. British Columbia's Critical Minerals Office designation reflects Canada's strategic imperative to develop domestic copper production as Chinese control of global concentrate supply tightens.

With smelters operating at 40-50% capacity and treatment charges turning negative, the market faces structural concentrate deficits precisely as energy transition and defense modernisation accelerate copper intensity. Northisle's high-quality concentrate (low deleterious elements, significant gold credits) addresses both the quantity and quality dimensions of this shortage. Gold's safe-haven role amid geopolitical tensions compounds the strategic value proposition, positioning Northisle's copper-gold-molybdenum product mix at the epicenter of Western critical minerals strategy.

TL;DR

Northisle Copper & Gold offers systematic re-rating potential from 0.3x to 0.7-1.0x NAV through PFS de-risking, enhanced by substantial commodity price leverage ($3,400 gold consensus vs. $2,150 PEA assumption), near-term resource expansion catalysts (West Goodspeed incorporation Q2 2026), and metallurgical optimisation (potential Phase 2 gold recovery improvement from 63% to 80%). The investment combines BC government-validated development pathway with $150M treasury, world-class operational team, and Wheaton Precious Metals strategic partnership, while providing "free call option" on district-scale exploration across 40km of prospective porphyry terrain - all producing premium concentrate into structurally tight markets.

FAQ's (AI Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed