Copper Price Collapse Exposes Structural Fragility in Supply Chains & Investment Flows

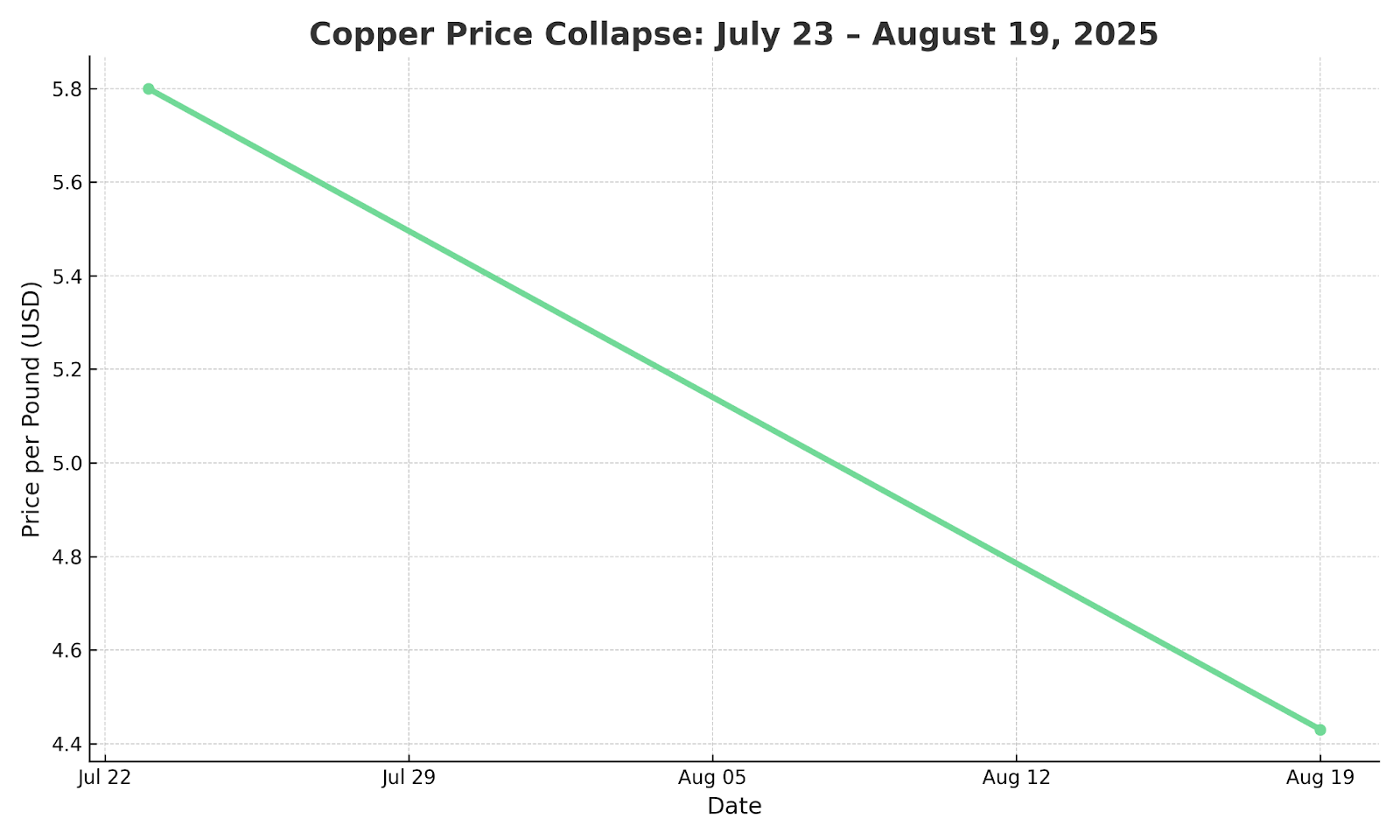

- Copper fell approximately 20% from $5.80 per pound on July 23 to $4.43 per pound on August 19 after the United States tariff exemption, triggering volatility and trade route reversals across global markets.

- United States inventories surged past 600,000 tonnes, creating short-term oversupply risks despite a structurally bullish long-term demand outlook driven by electrification and infrastructure development.

- Arbitrage unwinding collapsed the COMEX–London Metal Exchange premium, recalibrating global trade flows and ending the speculative surge of Asia-to-United States shipments.

- Chinese demand for softness in housing, solar, and white goods contrasts sharply with United States reshoring strategies and capacity expansion initiatives across North America.

- Investors are urged to focus on low-cost, politically stable copper developers like Gladiator Metals, Marimaca Copper, and Fitzroy Minerals that align with electrification and Environmental, Social & Governance demand requirements.

Copper's 20% Price Collapse: A Wake Up Call?

The copper market's steep correction following the United States tariff exemption represents more than a simple policy adjustment, it exposes the fragility of speculative positioning and the interconnectedness of global supply chains. Copper's role as a bellwether for global growth and electrification trends makes this volatility particularly significant for institutional investors monitoring macro economic indicators.

The 20% decline from July peaks reflects a market that had become overextended on short-term policy speculation rather than fundamental demand-supply dynamics. This correction serves as a critical reminder that commodity markets remain vulnerable to policy shifts, inventory movements, and sentiment-driven positioning that can quickly unwind established trading patterns.

Strategic Implications for Investors

Market volatility of this magnitude highlights the importance of distinguishing between tactical disruptions and structural trends. While the immediate price action creates uncertainty, it also presents opportunities for disciplined investors to evaluate positioning strategies based on long-term fundamentals rather than short-term speculation.

The investor angle centers on recognizing that price dislocations create both risk through oversupply concerns and opportunity through tactical positioning for those with conviction in copper's role in the global energy transition. Strategic investors must navigate this volatility while maintaining focus on projects and companies positioned to benefit from structural demand themes.

Inventories & Supply Chain Realignment

United States visible and off-market inventories exceeding 600,000 tonnes represent sufficient copper to meet months of domestic consumption, creating immediate pressure on pricing dynamics. This inventory buildup reflects the rapid reversal of trade flows that had developed during the period of tariff-driven arbitrage opportunities between Asian and North American markets.

The impact of cargo rerouting following policy clarification demonstrates how quickly global commodity flows can shift in response to regulatory changes. Ships that had been diverted to United States ports during the premium period were redirected to alternative destinations, creating temporary oversupply in specific regional markets while potentially tightening availability elsewhere.

This inventory surge illustrates the short-term price drag that can result from policy-driven supply chain disruptions, even when underlying demand fundamentals remain supportive. The copper market's response demonstrates how speculative positioning can amplify the effects of policy changes, creating volatility that extends beyond the direct impact of regulatory adjustments.

Arbitrage Collapse & Trade Flows

The collapse of the COMEX–London Metal Exchange premium from 28% to near zero represents one of the most dramatic arbitrage unwinding events in recent copper market history. This premium collapse eliminated the financial incentive for Asia-to-United States shipments that had driven significant cargo movements during the height of the tariff-driven premium period.

Global copper flows were redirected as the arbitrage opportunity disappeared, with Asian copper supplies finding alternative destinations in regional markets. This redirection created ripple effects across multiple markets, affecting local pricing dynamics and availability patterns in ways that continue to influence regional copper markets.

The volatility in regional spreads creates tactical arbitrage opportunities for sophisticated traders and investors capable of navigating the complex logistics and financial arrangements required to capitalize on these dislocations. However, the speed of this premium collapse also demonstrates the risks inherent in arbitrage strategies based on policy-driven market distortions.

Hayden Locke, Marimaca Copper's Chief Executive Officer, President & Director, observes how inventory dynamics influence strategic decision-making:

"We have the opportunity to build a mine that becomes very cash generative in today's copper price environment"

China's Weakness vs. United States Reshoring

Chinese copper demand faces headwinds across multiple sectors, with housing completions declining, regulatory pressure affecting solar installations, and reduced demand for air conditioning and white goods reflecting broader economic softness. This demand weakness in China, historically the world's largest copper consumer, creates near-term pressure on global consumption patterns.

Conversely, United States reshoring initiatives and smelting capacity expansion projects represent a structural shift in North American copper demand. The development of a Pan-American copper corridor aligns with strategic resource security objectives and creates new demand centers that may prove more stable than export-dependent consumption patterns.

This demand divergence between Asian weakness and America's strength reflects broader geopolitical and economic realignments that extend beyond cyclical factors. The shift toward regional supply chains and strategic resource security considerations suggests these divergent trends may persist longer than traditional cyclical patterns would indicate.

Implications for Project Developers

United States policy frameworks increasingly support secure, ESG-compliant supply chains, creating preferences for copper projects in politically stable jurisdictions with established regulatory frameworks. Projects in Chile and Canada benefit from this policy alignment, as they offer jurisdictional stability and established mining frameworks that align with strategic resource security objectives.

The emphasis on low-carbon supply chains creates additional advantages for projects capable of demonstrating reduced environmental impact through renewable energy usage, efficient processing technologies, and comprehensive ESG compliance programs. These factors are increasingly important in securing offtake agreements and financing arrangements with institutional investors.

Project developers in the Americas benefit from proximity to growing North American demand centers and alignment with reshoring initiatives that prioritize regional supply chain security. This geographic advantage becomes more valuable as supply chain resilience gains importance relative to pure cost optimization in sourcing decisions.

Market Volatility & Tactical Positioning

Copper futures markets have entered a consolidation phase following the initial collapse, with trading ranges reflecting uncertainty about near-term supply-demand balance and the sustainability of current inventory levels. Market participants are monitoring key technical levels and fundamental indicators to assess whether current pricing represents a temporary correction or the beginning of a more sustained adjustment.

Price forecasts suggest continued softness through the third quarter, with consensus estimates around $9,100 per metric tonne, followed by potential recovery to $9,350 per metric tonne in the fourth quarter as seasonal demand patterns and inventory normalization support price stabilization. These forecasts reflect expectations for gradual inventory absorption and stabilization of trade flows.

Technical Analysis & Investment Strategies

Technical analysis identifies the 200-day exponential moving average as a critical support level, with breaks below this level potentially triggering additional selling pressure from algorithmic trading systems and momentum-based strategies. Conversely, successful defense of this technical level could provide foundation for price stabilization and potential recovery.

Tactical strategies for institutional investors include buy-on-dips approaches for long-term positions, adaptive hedging programs that adjust to changing volatility levels, and monitoring of the gold-to-copper ratio as an indicator of risk sentiment and inflation expectations. These strategies require sophisticated risk management capabilities and clear investment mandates that can accommodate short-term volatility.

Jason Bontempo, Chief Executive Officer of Gladiator Metals, emphasizes the importance of long-term perspective during market volatility:

"We are targeting over 100 million tons at above 1% copper not including any credits"

Yukon's High-Grade Belt Amid United States Supply Realignment

The Whitehorse Copper Project represents significant potential within Canada's established mining framework, with historical production data supporting resource estimates exceeding 100 million tonnes. The project's location in Yukon provides access to established infrastructure while maintaining jurisdictional stability that aligns with North American supply security objectives.

Near-term catalysts include delivery of a maiden resource estimate scheduled for the first quarter of 2026, supported by a comprehensive 30,000-meter drilling program designed to define the scale and grade continuity across the 35-kilometer copper belt.

The project's strategic fit within North American supply chains reflects both high-grade oxide and sulfide mineralization optionality, providing flexibility in development scenarios and processing approaches. The combination of established infrastructure access and proximity to skilled labor markets in Whitehorse creates favorable development economics compared to more remote Canadian projects.

Bontempo highlights the project's accessibility advantages:

"We're working along the western margin of the city. We have excellent highway and road access and trail access. Excellent draw on labor resource and being so close to the city, we can pretty much work all year round so our dollars go a fair way"

Low-Carbon Development for Global Offtake

Marimaca Copper's 900,000-tonne measured and indicated resource represents a substantial oxide-focused development opportunity with low capital expenditure requirements relative to conventional copper projects. The project's definitive feasibility study nearing completion provides clarity on development parameters and economic returns under current market conditions.

The company's strong institutional and strategic shareholder base, including Mitsubishi Corporation and Assore International Holdings through warrant positions, demonstrates sophisticated investor confidence in the project's development potential. These strategic relationships provide potential pathways for offtake arrangements and development financing.

Unique positioning in the green copper market segment aligns with growing Environmental, Social & Governance-driven demand from United States and European buyers seeking low-carbon intensity copper sources. This positioning becomes increasingly valuable as supply chain decarbonization requirements drive procurement decisions beyond pure price considerations.

Marimaca Copper's Chief Executive Officer, President & Director Hayden Locke, emphasizes the project's financial viability:

"It's a very financeable project. It's not going to blow up our share structure. We have the opportunity to build a mine that becomes very cash generative in today's copper price environment"

Leveraging Oxide Optionality & Critical By-Products

The Buen Retiro oxide system combined with Caballos copper-molybdenum-rhenium potential creates diversified commodity exposure that provides natural hedging against single-commodity price volatility. Planned drilling programs totaling 12,000 meters for 2025 target expansion of known mineralization and exploration of additional targets within the project area.

Strategic leverage to copper, gold, molybdenum, and rhenium creates multiple value drivers that can respond to different market conditions and industrial demand patterns. This diversification becomes particularly valuable during periods of copper price volatility, as by-product credits can maintain project economics through commodity cycle fluctuations.

Location in Chile and Argentina provides access to established mining infrastructure and regulatory frameworks while maintaining exposure to politically stable mining jurisdictions. ESG compliance capabilities align with institutional investor requirements and facilitate access to development financing from major international lenders.

Gilberto Schubert, technical leadership at Fitzroy Minerals, describes the project's mineral complexity:

"The molybdenum grade represents almost doubling the copper grade, and together with the molybdenum we have rhenium which is a very important element. Chile is the second largest rhenium producer in the world"

Capital Formation & Risk Management in Mining

Macroeconomic volatility creates significant financing challenges for junior mining companies, particularly those in development and exploration phases that require sustained capital access for drilling programs and feasibility studies. Treasury strength becomes critical during volatile periods, with companies maintaining sufficient cash reserves better positioned to continue operations without dilutive financing during unfavorable market conditions.

Current treasury positions across the sector vary significantly, with Gladiator Metals maintaining C$15 million, Marimaca Copper holding US$14.9 million, and Fitzroy Minerals carrying C$5 million in available funds. These treasury levels provide varying degrees of operational flexibility and runway for continued development activities during market downturns.

ESG Compliance & Risk Mitigation Strategies

Environmental, Social & Governance compliance, established permitting frameworks, and jurisdictional stability serve as critical risk mitigators for institutional investors evaluating mining investments. These factors become increasingly important during volatile periods when risk premium demands increase across all investment categories.

Hedging strategies for companies in the developer stage require careful balance between price protection and maintaining upside exposure to commodity price recovery. Sophisticated hedging programs may include collar strategies, forward sales arrangements, and streaming agreements that provide price protection while preserving participation in potential price appreciation.

The Investment Thesis for Copper

- Short-term oversupply risks and market volatility require tactical discipline from institutional investors, with careful attention to entry timing and position sizing during periods of elevated price uncertainty.

- Medium-term United States reshoring initiatives and low-carbon mandates provide structural support for copper demand, particularly from projects capable of demonstrating ESG compliance and supply chain security advantages.

- Long-term electrification trends, renewable energy infrastructure build-out, and Environmental, Social & Governance-driven demand requirements anchor copper's fundamental bullish case despite short-term market disruptions.

- Company alignment with these themes varies significantly across the sector. Gladiator Metals offers high-grade, scalable assets with near-infrastructure advantages in a tier-one Canadian jurisdiction. Marimaca Copper provides low-capital expenditure, low-carbon oxide development in established Chilean mining regions. Fitzroy Minerals delivers oxide optionality combined with strategic by-product leverage across multiple commodity exposures.

- Risk-adjusted growth potential through exploration programs and merger and acquisition optionality provides additional value drivers for companies with strong management teams and strategic asset positions.

- Operational strategies adapted for inflationary and policy-driven cost environments become increasingly important as global supply chains adjust to new regulatory and economic realities.

- Asset portfolios demonstrating resilience to commodity price volatility and foreign exchange risk provide stability during uncertain market conditions while maintaining exposure to structural demand growth themes.

Volatility as a Strategic Signal

Copper's 20% correction underscores the market's short-term fragility while simultaneously highlighting long-term opportunity for strategically positioned investors and companies. The speed and magnitude of this price movement demonstrate how quickly sentiment-driven positioning can unwind, but also reveal the underlying strength of structural demand themes that persist beyond cyclical disruptions.

Investors should focus on jurisdictional safety, Environmental, Social & Governance compliance, and near-term operational catalysts when evaluating copper investments during volatile periods. Companies with strong treasury positions, established permitting progress, and alignment with electrification and supply security themes are best positioned to navigate current uncertainty while capturing long-term value creation opportunities.

Tactical volatility in today's market creates the foundation for strategic re-rating tomorrow, particularly for projects that demonstrate clear alignment with global electrification trends and supply chain realignment initiatives that prioritize security and sustainability alongside economic returns.

Analyst's Notes

Subscribe to Our Channel

Stay Informed