Copper Supply Shortage Through 2027 Fuels Advanced Developers

Copper's Critical Role in Electrification: Strategic shortage creates compelling investment opportunities as demand doubles by 2040 while advanced developers achieve breakthrough grades

- Copper treatment charges collapsing to negative territory signals acute copper concentrate shortage through 2027, while copper demand could double by 2040 driven by electrification and renewable energy infrastructure requiring 4x more copper per electric vehicle

- Multiple copper developers demonstrate strong project economics with recent Australian takeovers valued at $185-380 million, providing empirical valuation benchmarks for advanced development assets with comparable NPV and IRR metrics.

- European and North American copper projects benefit from critical raw materials policies and reduced geopolitical risk are positioning for domestic production as strategically valuable amid global supply constraints.

- Copper projects around the world that can navigate permitting challenges, demonstrate technical innovation, and leverage existing infrastructure will likely capture disproportionate value as supply-demand imbalances intensify over the coming decade.

The global copper market stands at a critical inflection point where unprecedented demand growth driven by electrification meets severe supply constraints, creating compelling investment opportunities across the development spectrum. From fully permitted US projects to breakthrough discoveries in Chile, copper developers are positioning themselves to capitalize on a supply-demand imbalance that industry experts project will intensify over the coming decades.

Market Fundamentals Signal Supply Crisis

The copper market faces structural challenges that extend well beyond typical cyclical patterns. Treatment charges, which represent fees paid by miners to smelters for processing copper concentrate, have collapsed to negative territory, reflecting an acute shortage of copper concentrate expected to persist through 2027. This unprecedented market condition indicates that smelters are effectively paying miners for access to raw materials, a clear signal of supply constraints.

The International Energy Agency projects copper demand could double by 2040 under net-zero scenarios, driven primarily by the electrification megatrend. Electric vehicles require four times more copper than conventional vehicles, while renewable energy infrastructure demands substantial copper-intensive transmission and distribution networks. These demand drivers create a strategic opportunity for copper developers, particularly those with advanced projects capable of reaching production within reasonable timeframes.

Barry O'Shea, CEO of Highland Copper, emphasizes the timing advantage:

"What the US needs now is projects that can be built and not ones that are sitting at first drill hole."

This construction-ready status differentiates advanced developers from earlier-stage exploration companies and positions them to benefit from both private investment and potential government funding initiatives.

Domestic Production Gains Strategic Value

The shift toward domestic copper production reflects growing recognition of supply chain security as a national priority. Highland Copper's Copperwood project in Michigan's Upper Peninsula exemplifies this trend, holding all seven required state permits and operating on private land, avoiding lengthy federal NEPA processes that can delay projects for years.

O'Shea describes recent meetings in Washington that revealed the depth of federal interest:

"I was taken aback at just how up-to-date they were, how well-versed they were in copper, both talking to members of natural resources committee as well as armed services committee, the importance both from an energy and a defense perspective."

The company has secured unprecedented government support, including a proposed $50 million state grant that has progressed through Michigan's appropriation process, along with 22 formal resolutions of support from local authorities. This multilevel endorsement reflects copper's strategic importance for national security, renewable energy infrastructure, and economic development in traditional industrial regions.

Barry O'Shea, CEO of Highland Copper

Strong Returns on Copper's Economics

Advanced copper projects are delivering compelling economics that have attracted significant acquisition activity. Highland Copper's feasibility study shows $170 million NPV with 18% IRR at $4 per pound copper, but the project's leverage to higher prices creates substantial upside potential. O'Shea highlights this sensitivity:

"If you increase copper price from $4 to $5, an 25% increase in copper price, it's actually a 300% net increase in net asset value. So from $170 million to about $510 million."

Recent takeover activity in the Australian copper sector provides empirical valuation benchmarks. Rex Minerals was acquired for A$393 million, New World Resources faces competing bids over $230 million, and Xanadu Mines accepted a $160 million offer. These transactions occurred during strengthening copper prices and demonstrate institutional recognition of scarcity value in advanced development assets.

Chris Stevens, CEO of Coda Minerals, notes the strategic timing:

"There is now empirical evidence that companies that are able to do that with credible solid projects with comparable NPVs, comparable IRRs, comparable CapEx's are being valued over $200 million. That gives me a lot of pep in my step to be quite frank."

Chris Stevens, CEO of Coda Minerals

Operational Development & Discovery Potential Drives Growth

- Metallurgical innovations are transforming project economics across the sector. Coda Minerals achieved a breakthrough in recovery rates, improving from 55% to 95%+ through ammonium chloride whole ore leaching. Stevens characterizes this advancement as transformational, as the improved recovery translates directly to enhanced revenue generation over the mine's life while potentially enabling smaller-scale startup operations that reduce initial capital requirements. The simplified processing route provides operational flexibility and earlier cash flow generation, addressing one of the project's historical challenges.

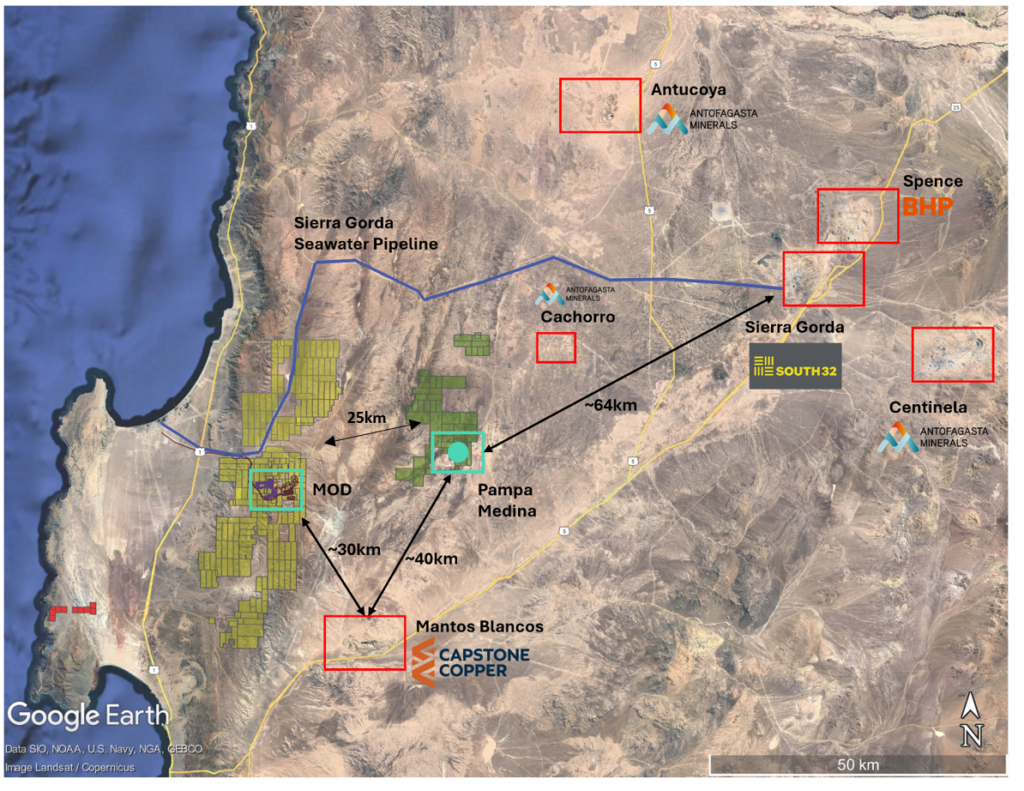

- Exceptional drilling results continue to emerge from systematic exploration programs. Marimaca Copper's discovery at Pampa Medina delivered 6 meters of 12.0% copper within 26 meters of 4.1% copper, representing ultra high-grade bornite-chalcopyrite mineralization in a rare sediment-hosted manto system.

The absence of dilutive byproducts enhances the economic potential of the discovery. President and CEO Hayden Locke emphasized the purity of the mineralization:

"The highest grade one is 6 meters at 12% and that's all copper. There's no byproducts. There's no gold. There's no silver included in that."

Referring to VP Exploration Sergio Rivera, with four decades of Chilean experience, Locke added how crucial this is in geological context:

"Sergio says he's never seen a deposit like this other than in very small areas in Chile. So his view is that it's much more analogous to the Kupfershiefer in Poland and Germany and then the African sedimentary copper basin."

This comparison is significant, as these systems represent some of the world's most prolific copper-producing regions.

Hayden Locke, CEO of Marimaca Copper

- Strategic positioning near existing infrastructure creates competitive advantages for development projects. Coda Minerals' Elizabeth Creek project benefits from proximity to BHP's established haulage road with contractual usage rights, while being located just one hour from Roxby Downs, BHP's major operational center. This infrastructure density is unusual for Australian mining projects, which typically require significant capital investment for basic access and services.

Similarly, Pan Global Resources' Escacena Project benefits from exceptional connectivity, situated 30 minutes from Seville with direct access to highways, rail networks, and export ports. The project's proximity to three existing processing plants and the Atlantic Copper smelter creates multiple development pathways and potential cost efficiencies.

Tim Moody, CEO of Pan Global Resources

Cash Flow Generation

Existing production operations demonstrate the cash generation potential of copper assets while funding exploration and development activities:

Central Asia Metals' Kounrad operation in Kazakhstan delivered 6,218 tonnes of copper production in H1 2025, maintaining consistent output through dump-leach operations. In the news release, CEO Gavin Ferrar commented on operational reliability:

"Kounrad delivered another quarter of safe and reliable copper production in Q2 2025, with H1 2025 output in line with our guidance for the year. At Sasa, the transition to new methods for mining and tailings disposal continued [...] We expect head grades to improve as the proportion of mining by the new methods continues to increase during H2 2025, but we believe it is prudent to revise Sasa's FY2025 production guidance at this stage."

As of June 2025, Central Asia Metals has $49.5 million cash in bank, including $6.6 million drawn under group overdraft facilities. The company maintains strong financial positioning with $42.9 million net cash, supporting ongoing development activities across its portfolio.

ATEX Resources continues to expand its Valeriano project in Chile, with recent drilling intersecting 104 meters of 1.06% copper equivalent within 568 meters of 0.86% copper equivalent. In the company update, President and CEO Ben Pullinger noted the system's scale:

"These latest results continue to demonstrate the scale and continuity of the high-grade porphyry corridor at Valeriano, while further extending mineralization to the north [...] As we reflect on a very successful Phase V campaign and look ahead to an updated Mineral Resource announcement and Phase VI commencement later this year, Valeriano is quickly emerging as one of the most significant undeveloped copper-gold projects in the Americas."

The Valeriano copper-gold project maintains an enterprise value of $630 million. ATEX Resources' net cash flow at C$45 million and a market capitalization of C$630 million demonstrates continued confidence from shareholders in the company as the Phase VI on the Valeriano project drilling is anticipated to commence in September which aims to further define the geometry and scale of the B2B Zone and other high-grade breccia targets.

The Investment Thesis for Copper

- Strategic Resource Positioning: Invest in fully permitted, construction-ready projects like Highland Copper's Copperwood that can capitalize on immediate supply shortages without regulatory delays or extended development timelines

- Geographic Diversification: Target projects in stable jurisdictions with supportive government policies, particularly North American and European assets that benefit from critical raw materials initiatives and reduced geopolitical risk

- Technical Innovation Exposure: Focus on companies achieving metallurgical breakthroughs that significantly improve project economics, such as Coda Minerals' 95%+ recovery rates that transform operational cash flows

- Discovery Leverage: Seek exposure to rare geological systems like Marimaca's sediment-hosted deposits that offer potential for world-class resource definition and district-scale consolidation opportunities

- Infrastructure Advantage: Prioritize projects with established infrastructure access that reduces development risk and capital requirements compared to greenfield developments in remote locations

- Production Cash Flow: Balance development exposure with producing assets that generate immediate cash flow to fund exploration and reduce dilution risk during development phases

- Market Timing Alignment: Target companies with 2-4 year production timelines that align with projected copper supply shortages and sustained price support from electrification demand

- Acquisition Potential: Consider advanced development assets with economics comparable to recent takeover targets, providing potential exit strategies through strategic acquisition by major producers

The copper investment opportunity reflects a convergence of structural demand growth, supply constraints, and technological innovation that creates compelling value propositions across the development spectrum. Companies with advanced projects, strategic positioning, and proven execution capabilities are positioned to deliver significant returns as the global economy transitions toward electrification and renewable energy infrastructure.

The sector's transformation from cyclical commodity exposure to strategic resource investment reflects copper's essential role in the energy transition. Projects that can navigate permitting challenges, demonstrate technical innovation, and leverage existing infrastructure will likely capture disproportionate value as supply-demand imbalances intensify over the coming decade.

Analyst's Notes

Subscribe to Our Channel

Stay Informed