Copper's $2T Investment Gap: Best Stocks for 2025

Copper faces structural supply deficits as demand surges 70% by 2050. US tariffs, AI infrastructure, and energy transition create compelling investment opportunities.

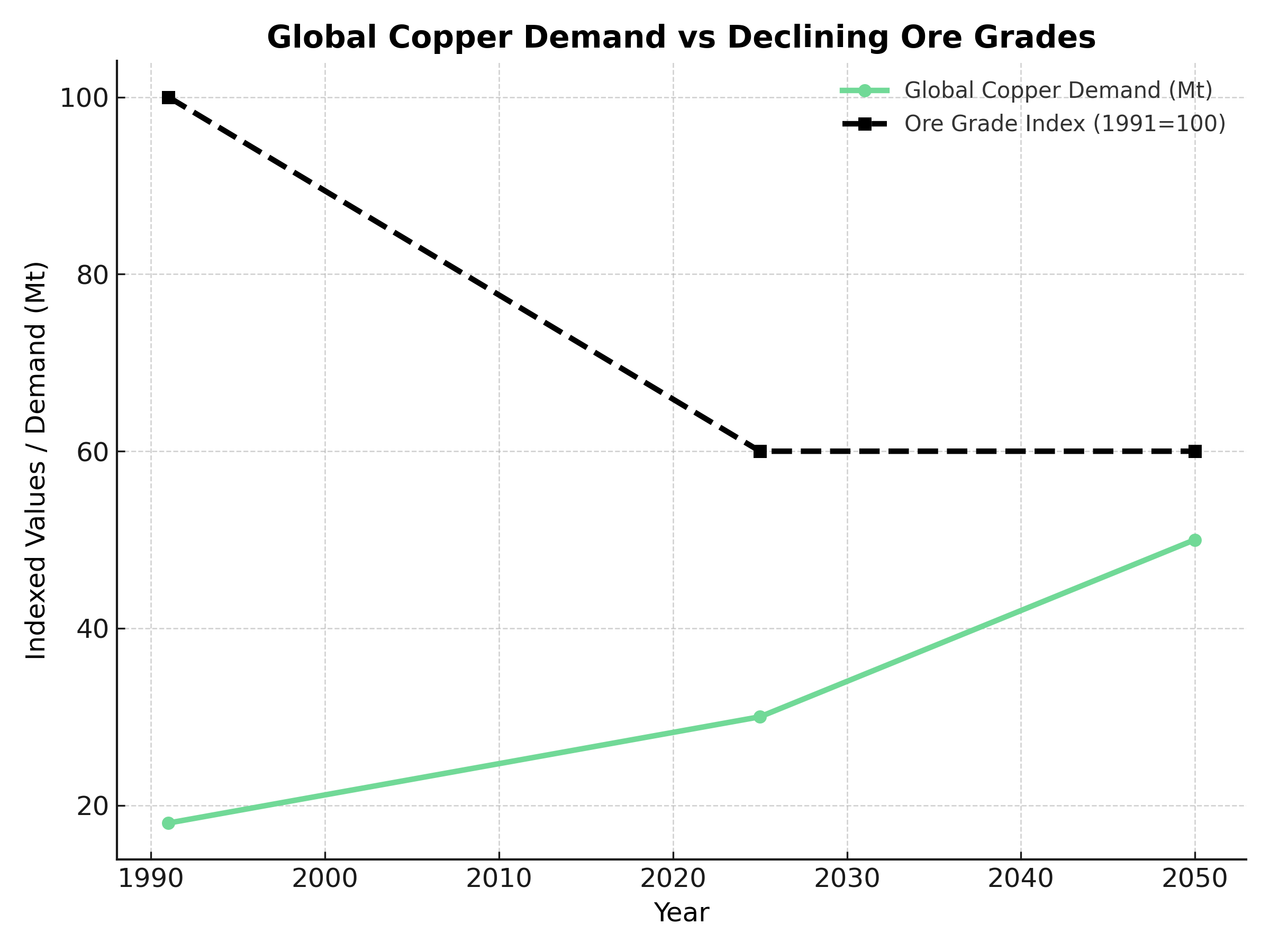

- Global copper demand is set to surge 70% to over 50 million tonnes by 2050, while supply faces structural constraints from declining ore grades (40% decline since 1991) and extended development timelines averaging 17 years from discovery to production.

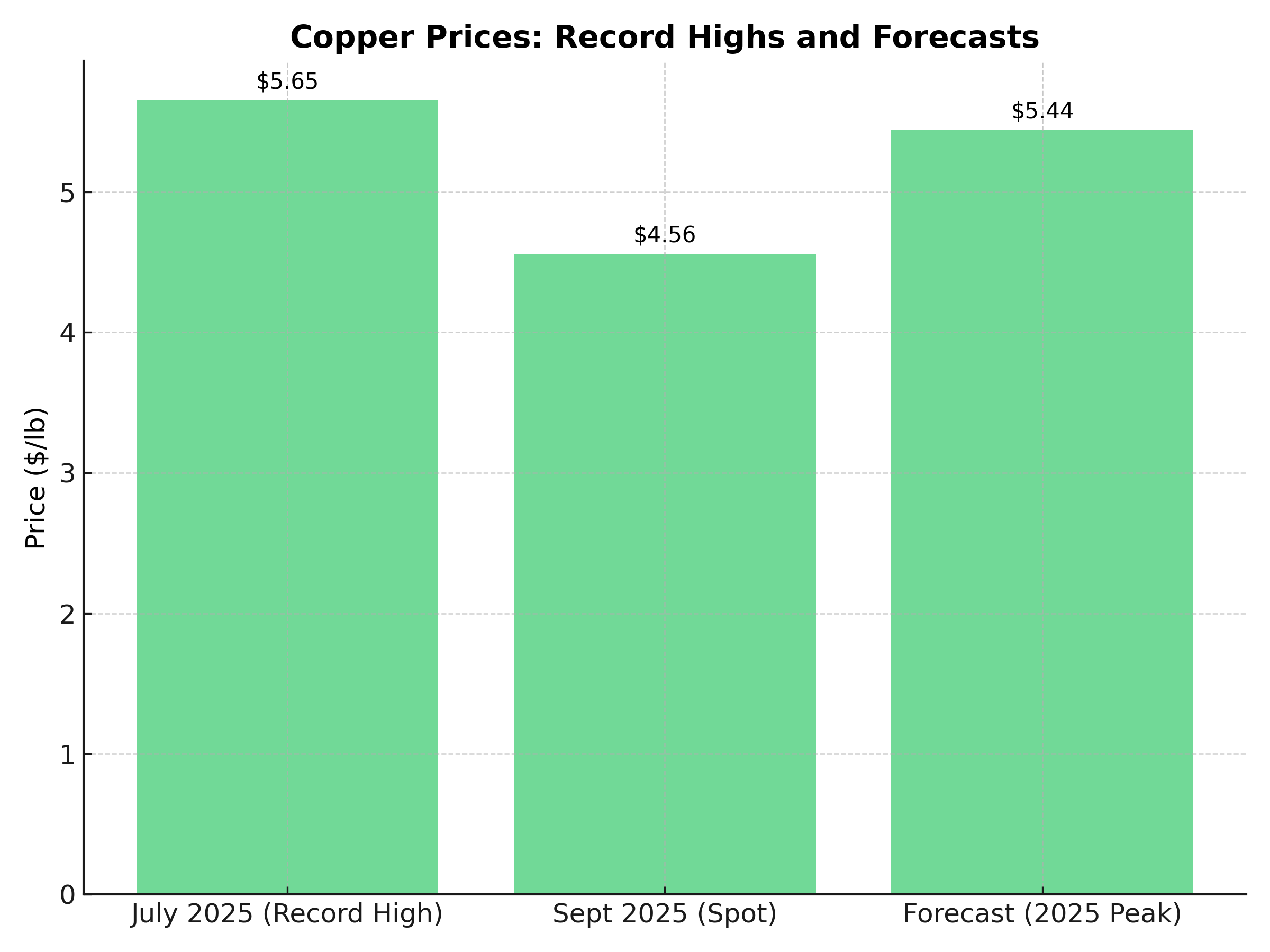

- Copper hit an all-time high of $5.65/lb in July 2025 amid tariff threats and supply concerns, with major trading houses predicting potential $12,000/tonne levels driven by structural deficits and AI/data center demand.

- US 50% copper tariffs implemented in July 2025 are reshaping global trade flows, creating inventory fragmentation and supporting North American exploration projects as strategic alternatives to Chinese supply dominance.

- AI data centers require massive copper infrastructure, with US capacity alone growing 50 GW by 2028. Electric vehicles use 4x more copper than conventional cars, while renewable energy infrastructure demands 3 tonnes per MW of wind capacity.

- Recent major financings including Marimaca's A$800M bookbuild and emerging discoveries at Gladiator (Yukon), Fitzroy (Chile), and India's anti-dumping measures signal institutional confidence in copper's strategic value.

Copper's Perfect Storm: Why Smart Money is Loading Up on These 5 Plays

Copper has emerged as the cornerstone mineral of the global energy transition, with BHP forecasting demand growth of approximately 70% to over 50 million tonnes annually by 2050. As the world electrifies transportation, builds renewable energy infrastructure, and expands AI-driven data centers, copper's unique properties superior electrical conductivity, thermal management, and durability make it irreplaceable across multiple growth sectors.

The copper market entered a supply deficit in 2025, with production failing to keep pace with accelerating demand from artificial intelligence data centers, emerging economies, and the energy transition. This fundamental shift creates compelling investment opportunities across the copper value chain, from established producers to exploration companies advancing district-scale discoveries.

Global Supply Challenges: The Foundation for Higher Prices

Since 1991, average copper ore grades have fallen by 40%, while only four significant copper discoveries were made between 2019-2023, totaling just 4.2 million tonnes of copper across all new finds. This resource depletion occurs precisely when global demand is accelerating, creating a structural imbalance that favors early-stage projects with high-grade potential.

The average timeline from discovery to production has extended to 17 years in 2023, making it increasingly unlikely that greenfield developments can respond quickly to strong demand signals. This extended development cycle creates substantial value for companies with advanced-stage projects approaching production decisions.

Capital Investment Requirements

BHP estimates that approximately $2.1 trillion in investment will be required to meet copper demand through 2050, with total expansion capex from 2025-2034 alone requiring around a quarter of a trillion dollars. These massive capital requirements favor well-funded companies with proven development capabilities and established partnerships.

Demand Acceleration: Multiple Growth Vectors Converging

In the United States alone, new data center capacity is expected to grow by approximately 50 gigawatts between 2023 and 2030 representing a tripling of current capacity from about 25 GW in 2024 to over 80 GW by 2030. Each gigawatt of data center capacity requires substantial copper infrastructure for power distribution, cooling systems, and connectivity networks.

The AI revolution is creating unprecedented demand for copper-intensive infrastructure. Data centers require robust electrical systems, advanced cooling networks, and high-performance connectivity all copper-dependent technologies that scale exponentially with processing power requirements.

Electric Vehicle & Renewable Energy Adoption

Electric vehicles use four times more copper than traditional cars, while a wind turbine requires 3 metric tons of copper for every megawatt of power produced. As governments worldwide implement net-zero targets and EV adoption accelerates, copper demand from these sectors will grow exponentially.

The energy transition represents the largest infrastructure buildout in human history. Power grids must be upgraded, charging networks deployed, and renewable generation capacity expanded all requiring substantial copper content. This creates multi-decade demand visibility for copper producers.

Geopolitical Dynamics: Reshaping Global Trade Flows

Following the July 8, 2025 announcement of 50% tariffs on copper imports, the Trump administration has identified copper as strategically important while noting that US smelting and refining capacity has declined as China has gained 50% global market share in refined copper.

This policy shift creates substantial opportunities for North American copper projects. Companies with US-based assets benefit from strategic importance, potential government support, and reduced trade risk. Projects like Highland Copper's fully-permitted Copperwood mine in Michigan exemplify this strategic positioning.

Trade Flow Disruption & Inventory Dynamics

The copper market has become fragmented due to US trade actions, with stocks moving into the US on speculation about tariffs, resulting in drastically lower inventories on the London Metal Exchange and Shanghai Futures Exchange. This inventory fragmentation supports price premiums and creates opportunities for regionally advantaged producers.

Company Case Studies: Marimaca Copper & Quality Projects Advancing Through Development

Marimaca Copper's recent A$800M bookbuild represents one of the largest copper financings of 2025, demonstrating institutional confidence in high-quality development projects. The company's flagship project in Chile's Antofagasta Region features 900kt of contained copper in measured and indicated categories, with simple heap leach processing offering 38% lower carbon intensity than conventional concentrators.

"What I'm pleased about is it confirms that we are in the bottom decile of capital intensity for copper projects, new development stage copper projects globally, according to the Wood Mac database. So we're sub $12,000 a tonne of copper equivalent production, which is a very nice place to be. All in sustaining costs right on the cusp of the first and second quartile, again, a very strong position to be in." — Hayden Locke, President & Chief Executive Officer, Marimaca Copper

The project's strategic advantages include proximity to established infrastructure, permitted seawater pipeline access, and district-scale exploration upside at Pampa Medina. As Chile maintains its position as the world's largest copper producer, projects like Marimaca provide exposure to stable jurisdiction mining with established regulatory frameworks.

Gladiator Metals: Yukon's Emerging Copper District

Gladiator Metals has reported significant copper-gold intercepts across its 35 km Whitehorse Copper Belt, including newly identified skarn and intrusive-related mineralization at Valerie and Little Chief, confirming the scale and diversity of the mineralization system.

"Gladiator's first drilling of new gravity targets at Little Chief and Valerie has intersected multiple zones of new mineralization with multiple copper (+/-magnetite) skarns flanking the margins of an intrusive body hosting significant mineralization that exhibits copper-porphyry signatures." — Jason Bontempo, CEO, Gladiator Metals

The Whitehorse Belt's infrastructure advantages include road access, grid hydro power, and proximity to skilled workforce combined with Tier-1 jurisdiction stability, positioning Gladiator as a leading North American exploration opportunity. Recent drilling results, including extensions at historically producing mines, demonstrate the belt's potential for significant resource expansion.

Fitzroy Minerals: Chilean Exploration Upside

Fitzroy Minerals' Buen Retiro project has delivered multiple wide, shallow copper intercepts including 119m @ 0.53% Cu from 49m and 32m @ 0.90% Cu from 2m, with strike length extended to approximately 985m and remaining open along strike.

"Drilling at Buen Retiro continues to demonstrate good copper grades and thicknesses below the gravels in the Southwest Area, which is great news. Our drilling takes the proven strike length of the system to almost 1 km long, and the wide and shallow mineralization we are finding will increase the dimensions of any potential future pit." — Merlin Marr-Johnson, Chief Executive Officer, Fitzroy Minerals

The project's shallow oxide mineralization provides potential for low-cost heap leach processing, while deeper sulphide zones offer longer-term value. Proximity to existing infrastructure in Chile's established Copiapó mining region reduces development risk and capital requirements.

Market Dynamics & Price Outlook

Copper traded at $4.56/lb on September 23, 2025, maintaining elevated levels despite short-term volatility.

Major trading houses predict copper could reach $12,000/tonne in 2025, representing approximately 20% upside from current levels.

Price forecasts reflect the fundamental supply-demand imbalance emerging in the copper market. While short-term volatility remains likely due to macroeconomic uncertainties, the structural deficit supports higher long-term pricing.

Supply Deficit Dynamics

Experts argue the market has moved into a structural deficit, with any price weakness potentially deterring investment and tightening the medium-term outlook. This apparent contradiction reflects the complexity of global copper flows and the impact of trade disruptions on regional supply-demand balances.

The regional nature of copper markets means global surplus figures can mask local tightness. US tariffs have created inventory fragmentation, with surpluses in some regions coinciding with deficits in others. This supports premium pricing for strategically located production.

Risk Considerations & Mitigation

Copper prices could slide toward $9,100/mt in Q3 2025 before stabilizing around $9,350/mt in Q4, citing concerns about front-loading dynamics and Chinese demand slowdown. This near-term weakness creates entry opportunities for long-term investors while highlighting the importance of position sizing and timing.

Operational & Environmental Challenges

Mining operations face increasing environmental scrutiny, permitting delays, and operational complexity. Companies with strong ESG credentials, community partnerships, and proven development track records offer superior risk-adjusted returns.

Geopolitical & Trade Risks

Trade tensions and resource nationalism present ongoing risks to global copper markets. Diversification across jurisdictions and exposure to strategic domestic projects provides portfolio resilience against geopolitical disruptions.

The Investment Thesis for Copper

- Allocate 40-50% to established producers for stability, 30-40% to advanced development projects, and 10-20% to quality exploration plays with discovery potential

- Focus on Tier-1 mining jurisdictions (Chile, Canada, Australia, US) that offer regulatory certainty, infrastructure access, and political stability

- North American projects benefit from trade tensions and strategic mineral policies, while Chilean assets provide scale and established operations

- Companies advancing automation, sustainable processing, and environmental stewardship will command premium valuations and improved access to capital

- Use market weakness to accumulate positions in quality assets, while maintaining flexibility to add exposure if structural deficits drive prices above $5.50/lb

- High-grade, shallow deposits offer superior economics and faster payback periods compared to large, low-grade resources requiring substantial capital investment

Key Takeaways & Investor Implications

The copper investment landscape in 2025 presents compelling opportunities driven by structural supply deficits, accelerating demand from energy transition and AI infrastructure, and supportive geopolitical dynamics favoring strategic domestic production. With global demand projected to reach 50 million tonnes by 2050 a 70% increase from current levels and limited new supply development, copper offers exposure to one of the most significant commodity imbalances of the coming decades.

Successful copper investing requires balancing exposure across development stages, prioritizing quality jurisdictions and management teams, and maintaining conviction through commodity cycles. Companies advancing high-grade projects in Tier-1 jurisdictions, particularly those with strategic geographic positioning and strong ESG credentials, offer the most attractive risk-adjusted return potential.

The convergence of supply constraints, demand acceleration, and supportive policy environments creates a multi-year opportunity for well-positioned copper investments. As global electrification accelerates and strategic mineral security becomes increasingly important, copper represents both a defensive infrastructure play and a growth opportunity aligned with transformative technological trends.

TL;DR

Copper markets face a structural transformation in 2025 as supply deficits intensify while demand accelerates from AI data centers and energy transition infrastructure. With global demand projected to surge 70% by 2050 and only four major discoveries made in the past five years, copper offers compelling long-term investment opportunities. US 50% tariffs create advantages for North American projects, while companies like Marimaca (A$800M financing), Gladiator (Yukon discoveries), and Highland Copper (fully-permitted US assets) represent quality opportunities across development stages. Successful copper investing requires balancing established producers for stability with exploration companies for growth potential, prioritizing Tier-1 jurisdictions and companies with strong ESG credentials and strategic geographic positioning.

Frequently Asked Questions (AI-Generated)

Based on current market analysis, top copper stocks include established producers like BHP Group, Freeport-McMoRan, and Southern Copper for stability, plus emerging opportunities like Marimaca Copper, Gladiator Metals, and Highland Copper for growth potential. Diversification across development stages is recommended.

The 50% US copper tariffs implemented in July 2025 create significant advantages for North American copper projects while disrupting global trade flows. This benefits companies like Highland Copper with fully-permitted US assets and creates regional price premiums supporting domestic production.

Copper demand acceleration stems from three key drivers: energy transition infrastructure (EVs use 4x more copper than conventional cars), AI/data center expansion (US capacity growing 50 GW by 2028), and global electrification programs requiring massive grid upgrades and renewable energy installations.

Primary risks include commodity price volatility (copper can decline 30-50% during downturns), geopolitical instability in major mining countries, environmental/permitting challenges, and operational execution risks. Diversification across jurisdictions and development stages helps mitigate these risks.

Key factors include management track record, project jurisdiction quality, resource grade and size, infrastructure proximity, permitting status, and funding capability. Focus on companies with tier-1 jurisdictions, high-grade deposits, and experienced development teams with proven execution ability.

Note: These FAQs are AI-generated based on current market analysis and investment considerations.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed