Danakali (DNK) - Funding Niche High Margin Potash

Interview with Seamus Cornelius, Exec. Chairman of Danakali Ltd.

We recently had a chance to speak with Seamus Cornelius, Executive Chairman at Danakali Ltd. He spoke about the company’s giant Colluli Potash Project in Eritrea. He tells us that Colluli will be the dominant sulphate of potash (SOP) project anywhere in the world within two-years time.

Company Overview

Headquartered in Perth, Western Australia, Danakali is a resource company in the process of developing a world-class potash mine in Eritrea, East Africa. This resource is expected to be a pivotal project, not only for African agriculture but global potash needs as well.

Shares of the company trade on the Australian and London Stock Exchanges. The company also trades on the OTC marketplace.

Leadership Team

In addition to the Executive Chairman, leadership consists of Neil Gregson, Non-Executive Director; Samaila Zubairu, Non-Executive Director; Taiwo Adeniji, Non-Executive Director; John Daniel Fitzgerald, Non-Executive Director; Zhang Jung, Non-Executive Director; Melissa Chapman, Joint Company Secretary; and Catherine Grant-Edwards, Joint Company Secretary.

The Colluli Project

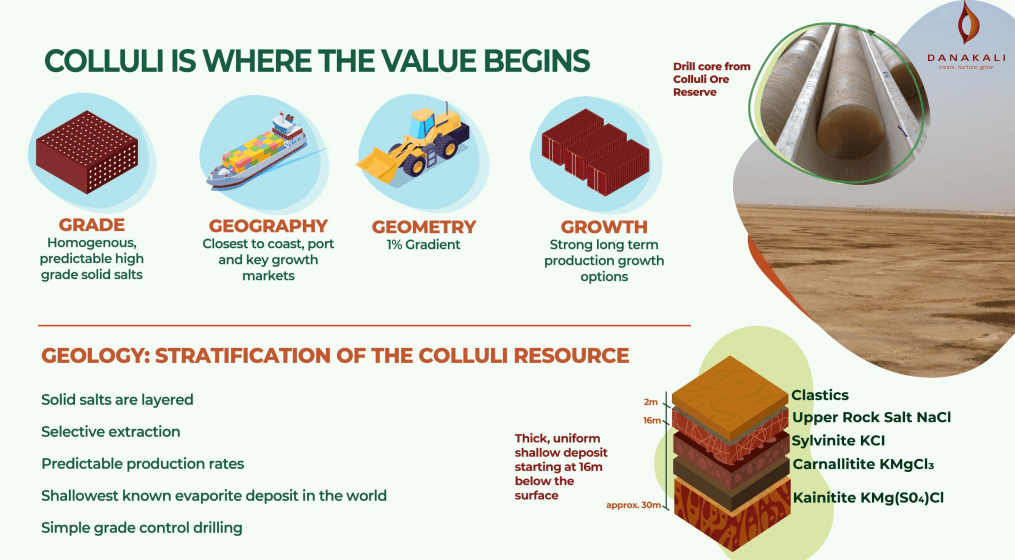

The Colluli Project contains a world-class resource consisting of three evaporative potassium-bearing salts: sylvite, carnallite and kainite. These minerals are suitable for high-yield production of sulphate of potash (SOP), which is a high-quality potash fertilizer that fetches a price premium over the more common potassium chloride or muriate of potash (MOP).

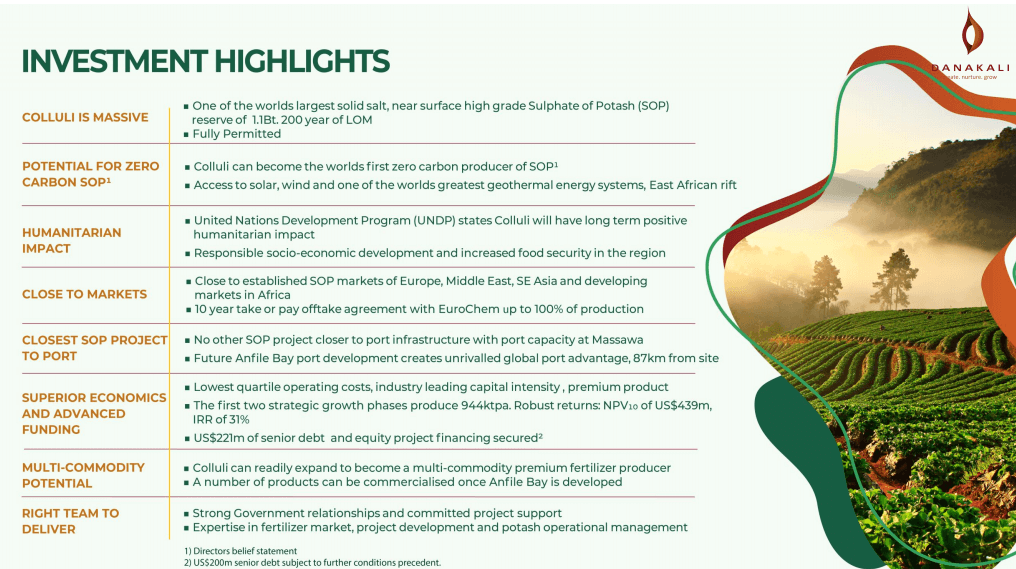

Colluli has enormous reserves of 1.1 Bt of potash ore. This reserve is broken down as follows:

· 303 Mt Measured Mineral Resource at 10.98% K2O,

· 951 Mt Indicated Mineral Resource at 10.89% K2O, and

· 35 Mt Inferred Mineral Resource at 10.28% K2O.

The minerals are near the surface and conducive to inexpensive solid-salt mining. All other places throughout the world with primary production of potassium sulphate from kainite commences with low-potassium brines that require substantial solar evaporation to generate a commercial product. Solid extraction at Colluli provides for immediate generation of the commercial potash. The Colluli mine will have a 200-year lifespan.

Colluli will be developed as a single open-cut pit, with a progressive working face that provides access to each of the evaporite ore layers simultaneously. The minerals will be mined using conventional mechanized equipment.

The mine is fully permitted as a 50% joint venture with ENAMCO, the Eritrean National Mining Company. Development of the mine was begun in 2020. Production is expected to begin in 2022. Colluli is located 75 km from the Red Sea, making it the closest-known SOP deposit to oceanic transport. Colluli is 230 km form Massawa, Eritrea’s main export port.

Eritrea: Is There A Business Risk?

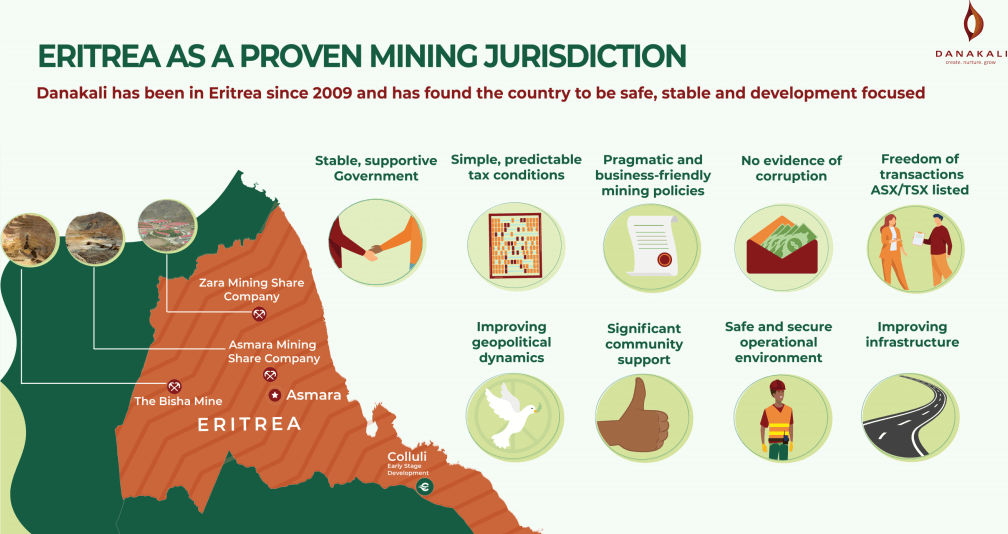

Eritrea is a proven mining district. The problem that Danakali has had is that it’s not a well-known jurisdiction. Simply because it’s not a well-known district doesn’t make it any more or less inherently risky.

The way that Cornelius looks at country risk is to look at what has happened in that particular country: What mining projects have been in that country and how have they fared?

For foreign mining investors and businesses, there has been nothing but success in Eritrea. Examples include the Beisha mine, the Zara mine and the Asmara project, all of which are highly successful operations. In addition, there are dozens of exploration projects, all of them foreign invested.

In Eritrea, the tax system is predictable and stable, and money can be moved easily out of the country. So, yes, Eritrea is a great place to have a mining operation.

Enamco: The Government Partner

Danakali’s partner at Colluli is Enamco, the Eritrea National Mining Corporation. People may not appreciate that the people who run Enamco are tremendously experienced mining company executives. Enamco only does exploration and mining, and they are the designated partner in every foreign mining investment project in Eritrea. They've been functioning in that capacity over the last 23 years, through the entire mining cycle, multiple times over.

Cornelius said that it is very easy to deal with the government departments in Eritrea, but it is easier when one talks to Enamco and says: How should one go about this project? And then they help tremendously.

Is Colluli On The Slow Track?

Cornelius admitted that it has taken a long time to get traction at Colluli. They initially had trouble getting debt financing for the project. In 2019 they did obtain USD $200 M senior debt funding. Half of that came from Afreximbank and the remainder from the Africa Finance Corporation.

Before Danakali could borrow money from either of those institutions for their Colluli project, the country of Eritrea needed to be a member country of those two institutions, which it was not. Getting those memberships took a bit of time. Furthermore, up until now, no foreign company had ever successfully debt-financed a mining project in Eritrea. Danakali is breaking new ground all the time and that's why it took a lot longer. Then, of course, there was the pandemic that slowed things up as well.

They haven’t been idle, though. They have been further testing the process of making SOP, which will be the first primary product from Colluli. Now, they basically understand everything down to the finest detail of how one actually makes SOP economically and efficiently. That enabled them to design the plant that they will construct at Colluli so that it is precisely suitable for the evaporative-salt ore that occurs at the deposit.

A Deeper Dive Into The Potash Market

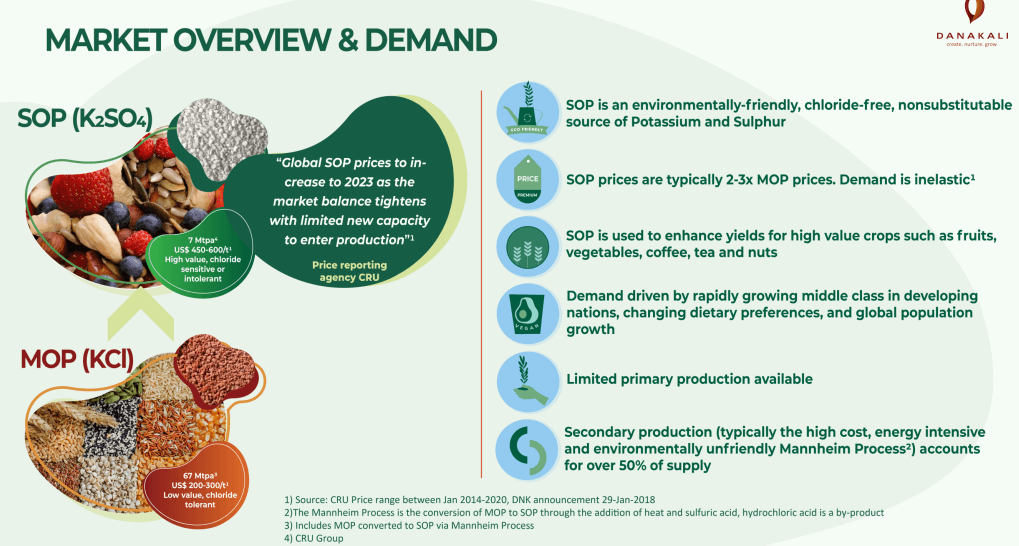

As mentioned, the potash market consists largely of two products, SOP and MOP. SOP is a better quality product but constitutes only about 10 percent of the global market. The overall market, then, is dominated by MOP with a global production of about 70 Mt per year. SOP comes in at about 7 Mt each year.

SOP has a particularly high-value use: It is used for citrus, nut, tea, coffee, potato, and berry agriculture. MOP does not work with these crops.

MOP production is dominated by Canada, Russia, and Ukraine-Belarus, who essentially function as a cartel. SOP is fundamentally different: It comes from a whole spectrum of small producers. About half of those producers actually make their SOP artificially. What that means is they take MOP, then add sulfuric acid to it, cook it up, and they produce SOP. Clearly there are insufficient sources of natural SOP. That alone makes Colluli special and globally important. Furthermore, because the process to produce MOP is so different from SOP, the cartel will have relatively little influence over it.

The actual method of producing SOP artificially is quite expensive. The few low-cost producers are in North America and China. That's why there's always roughly a USD $200-$250/t premium for SOP over MOP.

Danakali believes that because they will have the largest and lowest-cost SOP mine in the world, all of those margins become the company’s because few, if any, of the other producers can ever hope to compete with them. There is nothing that competing companies can do about Colluli, said Cornelius.

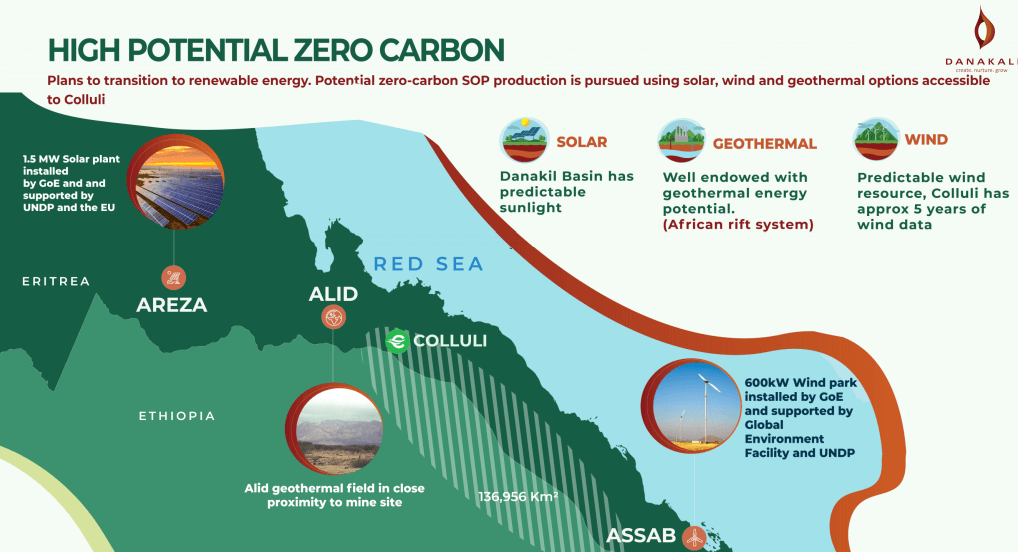

The Benefit of Using Seawater in SOP Processing at Colluli

Danakali intends to use regular seawater as part of the processing workflow at the plant that they will build. Earlier, they intended to use desalinated seawater from the Red Sea during processing, which would have been quite costly.

Most people know seawater is salty. But, in fact, the amount of salt in seawater is irrelevant compared to the massive amounts of salt that you are putting into the ore processing workflow. The water in the ground at Colluli is hundreds of times saltier than seawater. Given that the primary function of the plant is to remove the salt that the company doesn't want and leave Danakali with SOP, which is what is valuable. Thus, adding a tiny bit of seawater is nothing. That epiphany was a giant breakthrough because it changed the whole way that they looked at the seaside infrastructure. There was going to be a significant desalination plant and now it's not going to be needed anymore.

Not only is this a major cost savings for Danakali, but the adverse environmental footprint is greatly reduced as well. The fish, coral and other biota are winners too.

More on the Business Model

Cornelius estimates that the all-inclusive, freight-on-board (FOB) costs at the Massawa port is USD $258 per t. The product today in Europe is selling at about $600 per t., and that is one of the primary markets. The producers that compete with Danakali in Europe are factory-based producers in Manheim, Germany. The cheapest that they can produce it at is about $400/t, but some of them are at $500/t. Clearly, Danakali has a massive margin advantage relative to these competitors.

They intend to develop the deposit in phases or modules. So, the company has module 1, module 2, and it's not going to stop at module 2.

A major part of Danakali’s business model is to undercut all of these synthetic SOP producers. The company looked at the SOP market and broke it into segments: the East African time zone, the American time zone, and the Chinese time zone. There is a slight difference in the price in each of these three.

In the East African time zone all the producers are high-cost, expensive producers, and Danakali’s tons can go into that market very easily without disrupting the price. That's why they intend to initially produce 472,000t. Look at the size of the Colluli asset: If they decided to stay at that production scale, they'd be doing it for 400-years. So clearly, the initial objective is to get production up and running, keep the CAPEX low, and then expand as quickly as we can.

The medium-term objective is to take a major market share from all of those Manheim producers; that will bring production up to 2Mt. Then, the company will start looking to India, Saudi Arabia, and South America to open up additional market objectives.

Indeed, there may be more products down the line than SOP, attractive as it is. For example, rock salt gypsum can come out of Colluli at a profit with very little extra CAPEX, and even very little additional OPEX.

Can Danakali’s Competitors Fight Back?

Cornelius is not sure that his competition will be able to muster an adequate response to his company’s business plans. One of the challenges is that these competitors use a massive amount of hydrochloric acid in the processing of their SOP. Hydrochloric acid has to be disposed of and the only real place that European processors can dispose of it is in the steel industry. And everybody knows that the Chinese, Koreans, and Japanese have been eating away at the European steel industry for a long time. Thus, the environmental cost of dealing with that hydrochloric acid and the regulations around producing this type of SOP in Europe are not favorable for them. Additionally, they will have difficulty overcoming costs. Their cost of production is fixed by the cost of MOP, acid, and power.

Danakali has natural markets in Africa and India. They are serious under-utilizers of SOP, in large part because they can't afford it and they can't get it. Colluli will solve that problem for these parts of the world, regardless of what effect Danakali’s output will have on the European SOP producers.

Indeed, for Danakali’s SOP, the growth markets of the future are in Africa and India. SOP is used not so much on grain crops, but for food types that are cultivated and sold in developed markets. As Africa and India continue to develop, the market for SOP will only increase, said Cornelius.

Will Danakali Set Up Its Own Distribution Network?

Cornelius indicated that Danakali does not intend to set up its own distribution network. Instead, they have a ten-year agreement in place with Eurochem, a leading fertilizer producer and trader. Danakali delivers the SOP to the Red Sea port at Massawa. Euorchem takes it from there through its own and other networks.

Eurochem gets it to the customers and they get a fee for doing that based on the net-back revenue to Danakali. Here are the details of the arrangement: Eurochem has to take 87 percent (about 400,000 t) of Danakali’s module 1 product, and at Danakali’s election, can take up to 100 percent. Danakali can elect to sell the remaining 13% to the local market or wherever they choose. Going forward, there is additional optionality that can be built into the contract terms as well.

Interestingly, Eurochem would love to have some of Danakali’s SOP for their own purposes other than reselling. They actually buy their SOP from some of their direct competitors, and they don't want to continue doing that indefinitely. So, not all of the product going to Eurochem from Colluli will be going out to third parties. Some of it will be replacing SOP from their current suppliers.

Forward Financial Plan

Right now, Danakali sits at an AUD $160M market capitalization. The critical thing needed now is to raise the balance of the funding that the company requires to get Colluli into production. Cornelius indicated that the company is talking very actively and at an advanced level with their lenders about getting further senior debt.

Then there's the equity component. They have a dual-track process going on and the continuous disclosure rules are such that nothing much more can be spoken about at this time. But they are at a very advanced point in the process where they will likely be able to go to their shareholders with a deal. That's the next step in the financing process.

As far as being a potential takeover target, Cornelius doesn’t think that there is too much incentive for that. Potential suitors would want to see Colluli developed further, and then perhaps things could happen. Right now, Danakali is in the middle ground, said Cornelius. What is important for the company and what drives the value is getting the balance of the funding. That's where all the company’s energy is going.

Closing Thoughts

The bottom line is this: Danakali wants to get the giant-sized Colluli deposit into SOP production and then start to exploit the full suite of minerals that Colluli is endowed with. That will produce at least 10 to 20 years of solid growth.

To find out more, go to the Danakali Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed