Electric Royalties (ELEC) - Focused on Entire Suite of Battery Metals

Electric Royalties Inc. is a royalty company set to take advantage of the demand for a wide range of commodities

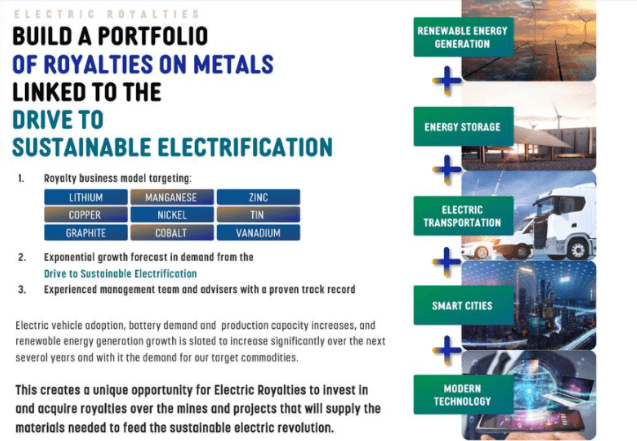

Electric Royalties is a royalty company set to take advantage of the demand for a wide range of commodities (lithium, vanadium, manganese, tin, graphite, cobalt, nickel & copper) that will benefit from the drive to electrification in cars, rechargeable batteries, large scale energy storage, renewable energy generation and other applications.

We recently had the opportunity to speak with Brendan Yurik, CEO and Director at Electric Royalties, an emerging company with a sharp focus on supplying the commodities that power many electric applications in the ongoing green revolution.

Company Overview

Electric Royalties is a relatively new, Vancouver, B.C.-based mining royalty company and one that intends to focus on the entire suite of battery metals, including lithium, zinc, manganese, vanadium, cobalt, tin, copper, nickel, and graphite, which are needed for battery storage. Electric vehicles, battery production capacity, and renewable energy generation are expected to increase significantly over the next several years, and with it the demand for these strategic commodities. Based on that premise, Electric is building a portfolio of royalties that will benefit from the global move toward electrification. It claims it currently has a dozen royalties in the portfolio.

IPO During COVID

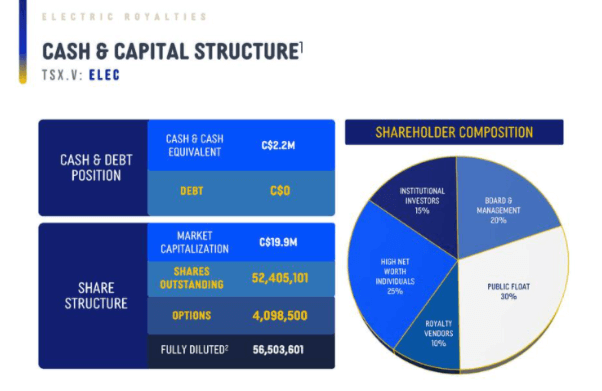

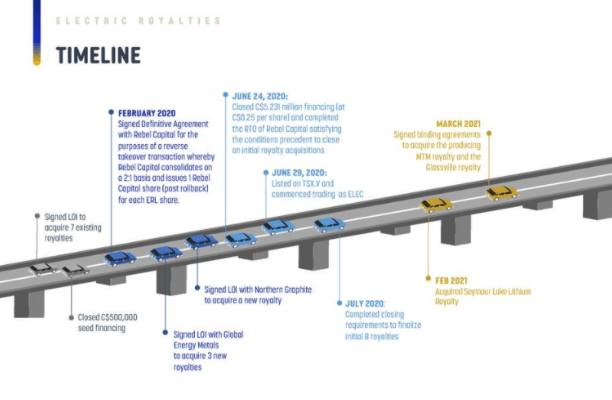

Electric Royalties were first listed on the TSXV on June 29, 2020. At that time, COVID-19 was running rampant. Despite that, the IPO was oversubscribed and the company closed out all the royalties that they had signed up prior to going public. The company was able to raise $5.2M during the IPO phase.

The timing of all this activity was difficult, relative to the pandemic-related stresses. Nonetheless, Yurik was pleased that they were able to get it all done.

Prior to the IPO, the business operated as a capital pool company named Rebel Capital, which was founded in 2016.

Management Team Composition

In addition to CEO Yurik, the management team also includes several company advisors, including Greg Bowes, Rod Cooper, Darcy Marud, Nicolas Schlumberger, and Richard Williams.

Brendon Yurik believes that his entire career trajectory makes him perfect for Electric Royalties: “My entire history and background, my career has been focused on alternative financing, project financing, royalty obviously being a form of alternative financing for the mining sector”. He began his career with Endeavour Financial in London. He has worked with several groups near Vancouver, including the King & Bay West Management Group and the Hunter Dickinson Group. Additionally, he has been advising junior mining companies on his own, helping them structure deals to build their portfolios.

The company advisors bring mining experience to Electric Royalties. Rod Cooper is CEO of Northern Graphite. Yaris tells us that his 10-years of graphite experience will help Electric Royalties navigate some of those pitfalls in the graphite ecosystem. Richard Williams is CEO at Cornish Metals. He brings advice and expertise on tin. Darcy Merud is the former senior VP for exploration at Yamana. Rod Cooper, was the former senior VP for technical services at Kinross. Nicolas Nicholas Schlumberger is probably best known for his oil experience because of his family’s legacy business. He also has tremendous knowledge of private equity and brings that to the team at Electric Royalties.

Electric’s Metals Portfolio

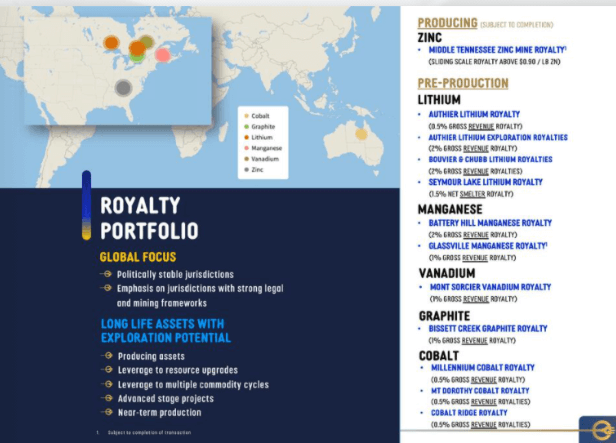

Yurik says Electric Royalties has built up its portfolio to 12 royalties, if he includes the Middle Tennessee Zinc Mine, which is currently cash flowing. However, the deal is not closed, but they want to close it in the next 3 months, subject to their ability to raise the capital to pay for it.

Middle Tennessee Zinc Mine is owned and operated by Trafigura. As highlighted by Yurik: “It has produced intermittently for over 50-years. They’ve been at it for a pretty long time, and have already produced over 2.7Bn lbs. of zinc to date. If you go through that operating history, you see pretty consistent recoveries. The deposit has been pretty consistent, and it produces a really clean concentrate. Right now, since production restarted in the middle of 2017, it’s already paid out royalty revenues close to $5M (to the current royalty holder)”.

Other non-cash-flowing royalty assets in the portfolio include:

- Battery Hill, Canada – Manganese

- Bisset Creek, Canada – Graphite

- Bouvier and Chubb, Canada – Lithium

- Mont Sorcier, Canada – Vanadium

- Authier, Canada – Lithium

- Dorothy and Cobalt Ridge, Australia – Cobalt

- Millenium, Australia –Cobalt

- Glassville, Canada – Manganese

- Seymour Lake, Canada – Lithium

Although not immediate cash producers, some of these are in advanced stages of development. For example, the Authier project, operated by Sayona Mining, is “ready to go” at the feasibility stage, according to Yurik. The Seymour Lake project is in a similar and “Looks pretty identical to where Authier was just a few years ago”, said Yurik. The manganese property at Battery Hill looks capable of bringing in $6M pa over the next 35 to 40 years, according to the CEO.

Electric’s Early-Stage Finances

Given much of the early-stage financial picture revolves around the only cash-flowing asset in this discussion, we asked Yurik about the timing of the financial contribution from the Middle Tennessee project to their portfolio. Yurik provided this: “At today’s Zinc price, so they can ramp this up effectively and get over some of the Covid blaze from last year, we’re looking at about $2.5M a year in Royalty revenue. Based on our calculations, they’ve got about 15-years of outlines, so estimate a 15-year mine life to date. Really, we see a lot of expansion potential beyond that. It’s the kind of thing that has been producing intermittently for over 50-years”.

Yurik confirmed that Electric believes that the $2.5M royalty they may receive from Middle Tennessee is sustainable year in and year out over the foreseeable future. He has received a bit of pushback because of the rather long payback time on this investment, but he countered that with: “You’ve got to look at this as a much longer-term play. If someone comes to you and says, ‘Hey, I could give you $10M today, you’re going to pay me back $1M every year for the next 35-years’ - that’s how you have to think about it”.

When pressed on the acquisition price for Middle Tennessee, Yurik offered the following: “The acquisition price is $13M and 14.5M shares of Electric Royalties. We’ve had a little bit of feedback, people say that’s expensive when they look at maybe the payback period being a little bit longer than you see in some other investments, but you’ve got to remember, this costs us nothing to hold after this. We have no costs going out the door. All the exploration upside after that payback happens, it’s just cash flow coming in and that cash flow could be coming in for another 10 to 15-years beyond that”.

The company hasn’t raised any capital since the initial 2.5M, but promises to do some in the near future to be able to acquire Middle Tennessee. They are looking at a number of different financial options going forward. Some of this includes bring in co-investors, debt financing, convertible debt, and more. According to Yurik: We’re having some discussions with bankers and such right now. We’re hoping to formalise a financing plan in the next few weeks” in order to move forward. It concerned us that the CEO was including this deal in his description of teh current state of affairs given the not so insignificant task of raising the capital and concluding a potentially over priced transaction.

Financial Barriers

We asked Yurik about any financial barriers the Electric Royalties may face in the near future. He responded that he believes that “there’s quite a bit of money out there right now”, although he admits that “the market could change in a minute”.

He continued: “If you look at the multiples of where base metal royalty groups are trading, we don’t really have any better comps because we’re the only battery metals focused group, but those have gone up considerably over the last 6-months to the point where you’re almost seeing a parody with gold royalty companies, which is interesting. If you look at it from that kind of metric and if we can hit that $2.5M annualised cash flow number, the transaction could be valued at $40M - $45M in our company today”. Again one could argue that this is over stating given Middle Tennessee is far from complete and merely an aspiration at this point, albeit one under and need binding MOU.

Above all, he said, he wants to do what is right for the shareholders.

A Look at the Competition

We also asked Yurik about is perspective on the competition. He’s quite aware that there have been quite a number of new entrants into the royalty space. He answered his own concern with this: ”I would say that the difference with us is focus. Commodities focus. All the big established players are primarily gold and silver, precious metals. Most of the new entrants have made that their focus as well. That’s a lot of competition across a couple of commodities. That impacts pricing, your ability to build a portfolio, and grow that portfolio”.

We shared with him that we are aware of a handful of people that are interested in starting battery-metal-themed Royalty companies. He replied that the move to electricity is “Going to be a shift you haven’t seen before in human history, where you have so many new sets of demands basically legislated by government, funded by government, for the drive for clean energy across so many different metals all at once”. So he recognises that increased competition is in the cards. He further offered that Elemental Royalties can stay ahead of the game: “The key thing for us right now is to focus on keeping diversification across all these different metals so you’re not too heavily in one. There’s a risk to each commodity out there; you never want to be all-in on one commodity”.

Finally, Yurik shared that Elemental has been receiving quite a bit of in-bound deal flow. He indicated that pricing and deal flow is better than in the gold royalty space because at the moment there is a lot less competition with battery-specialty commodities. And for those that are coming into the space, he says that he’s “2-years ahead of them”.

To find out more, go to Electric Royalties' Website.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.webp)

Stay Informed