Electric Royalties (ELEC) - Revenue Guidance for 2022

Interview with Brendan Yurik, CEO of Electric Royalties Ltd.

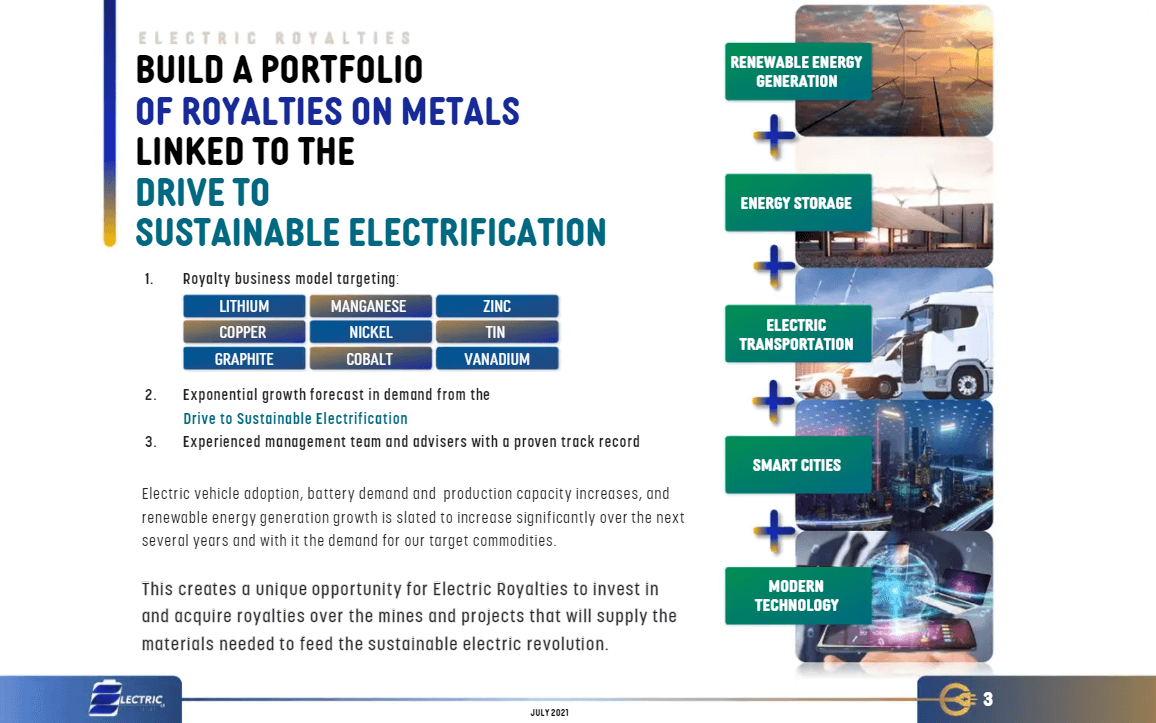

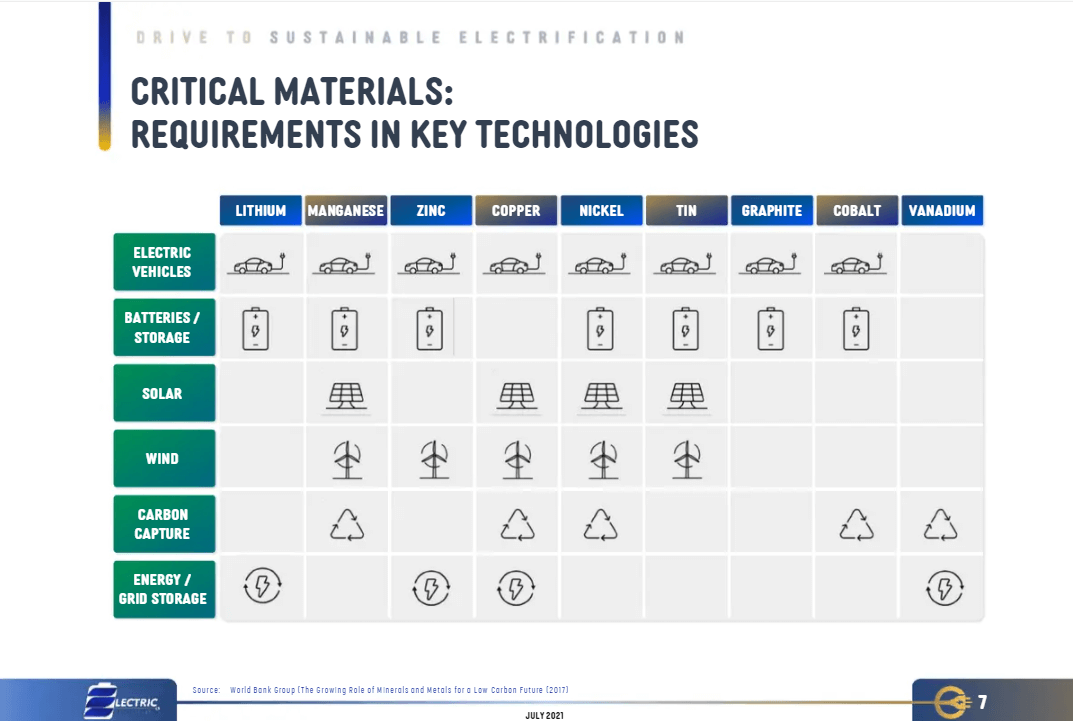

Electric Royalties Inc is a royalty company set to take advantage of the demand for a wide range of commodities including lithium, vanadium, manganese, tin, graphite, cobalt, nickel & copper. These commodities will benefit from the drive to electrification and be used in cars, rechargeable batteries, large scale energy storage, renewable energy generation and other applications.

We caught up with Brendan Yurik, CEO of Electric Royalties for an update on recent deals, current revenue and plans for the company going forward.

Company Overview

Electric Royalties focuses on the entire suite of metals required for the transition to clean energy. The company is only of the only royalty groups to do so. As society moves towards a decarbonised future, the rebuilding the of global infrastructure will require an exhaustive amount of these metals.

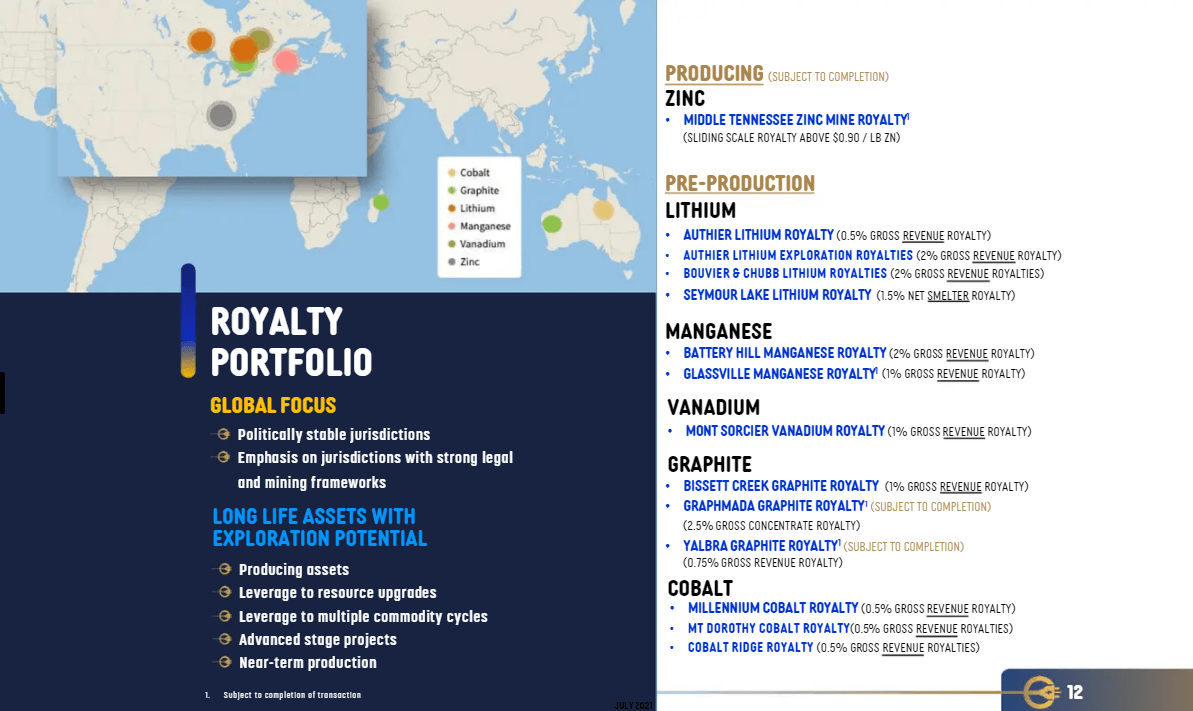

Electric Royalties has a growing portfolio of 17 Royalties, with cash flow from their recently closed MTM acquisition in the US. The company is looking to offer investors exposure to the underlying commodities that are required as we build out this clean energy future.

Good Deals, Current Revenue, & Finding Out More

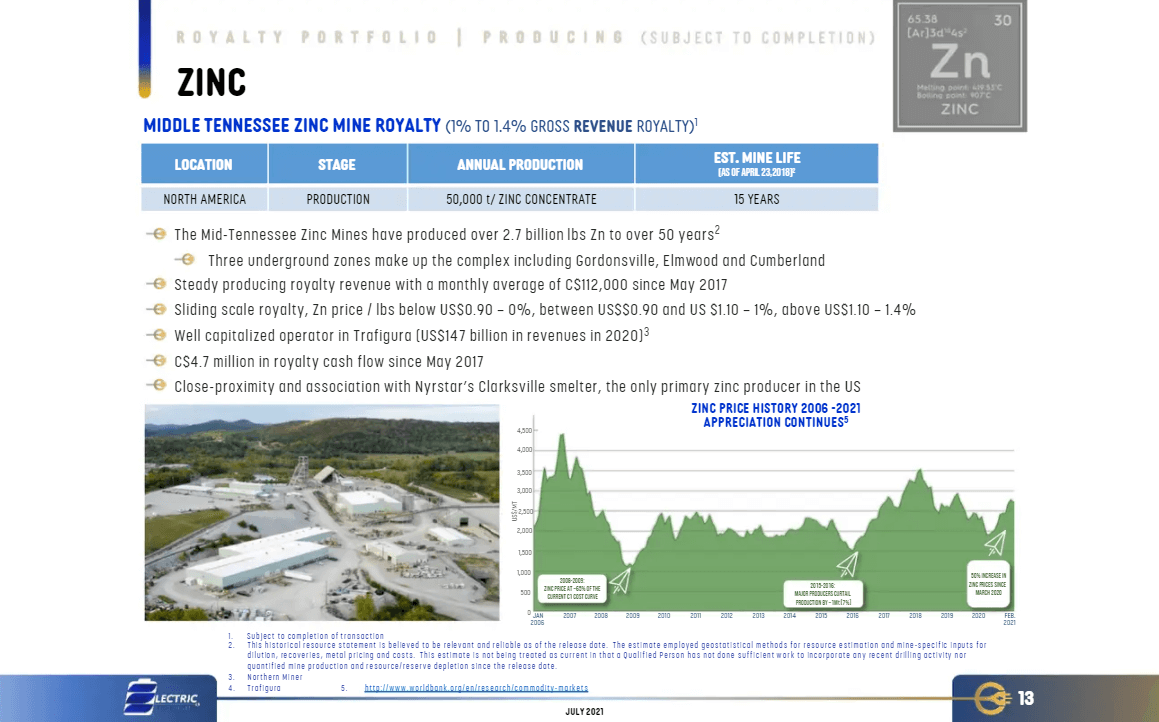

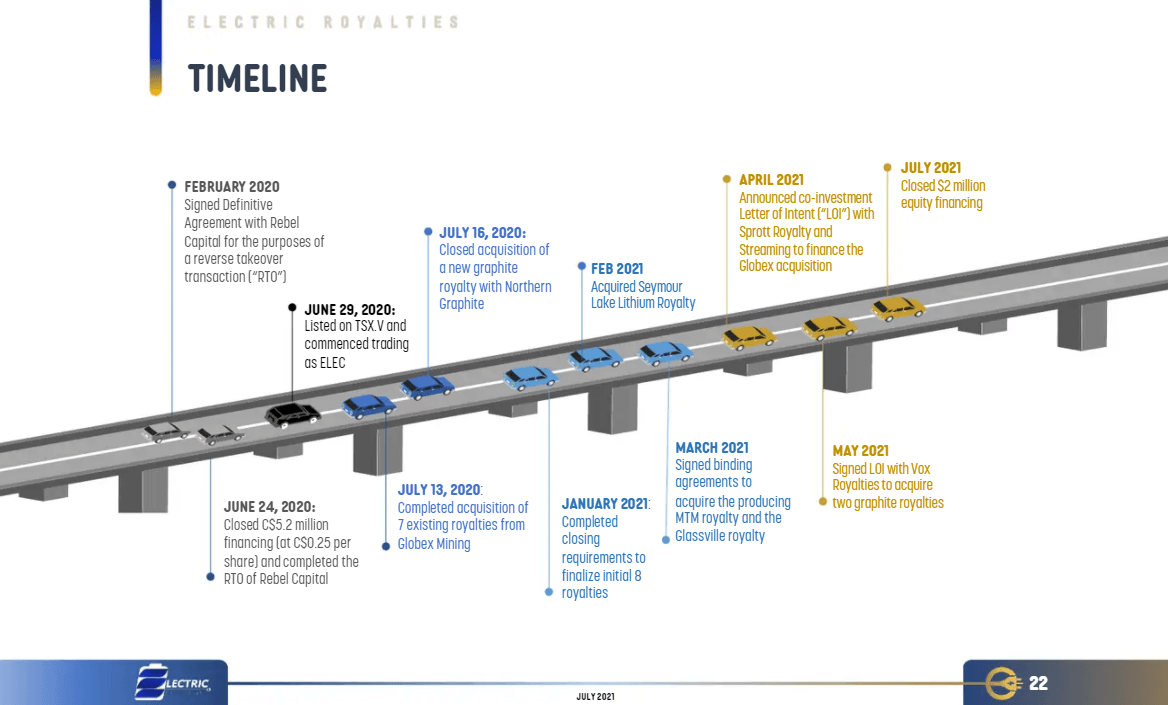

Electric Royalties has closed the Sprott deal on better terms than the company initially signed up to months ago. Sprott came in for $13.5M cash, and co-invested alongside Electric Royalties. As part of the Globex acquisition, Electric Royalties now has its first cash flow and royalty on the Middle Tennessee Zinc Mine in the US, operated by Trafigura which has been producing for over 50-years, with the expectation it will be producing for decades to come.

Electric Royalties has also recently closed on its VOX acquisition which includes two graphite royalties in the portfolio, one of which is on care and maintenance: the Graphmada mine in Madagascar which could be back in production as early as Q2 of next year. Electric Royalties hopes that this will be the first of many deals with VOX and will see how that partnership progresses as they move forward.

With the Middle Tennessee royalty, Electric Royalties currently has 25% but they have an option to increase their ownership to 50% which would double the revenue from this royalty. In the first year, they are expecting about $500,000 from this royalty but hope to double it, boosting revenue up to about $1M a year. The Graphmada asset is expected to come back online next year which should be about $500,000 a year in revenue for Electric Royalties.

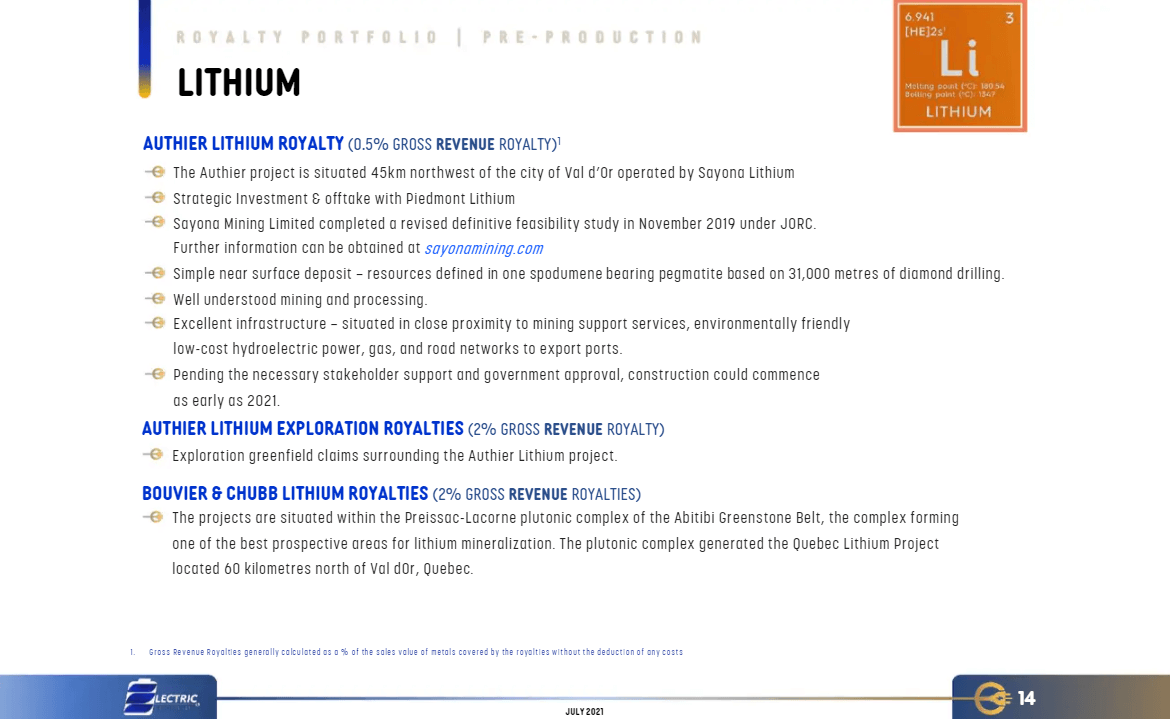

From their own portfolio, Sayona Mining, is moving quickly and they have just finalised and closed their acquisition of the Canadian Lithium mine, which is right next door to the Authier Lithium royalty project. The plan is to blend the ore from the Authier project to ramp up production at the mine which will be formalised and should be in production within the next 2-years.

Trafigura has just taken over the Middle Tennessee mine and historically, Trafigura has looked to maximise operations on project acquisition. The concentrate at the Middle Tennessee mine is among the highest grade and cleanest globally which is a good concentrate to blend other ores with. Electric Royalties expects that this operation will grow as Trafigura starts ramping up production so things might look differently after the first year in production when they need to make the decision to double the ownership to 50%.

Timeframe for the second quarter, management teams, & future deals

Graphite in Madagascar is very high quality and as with a lot of these commodities, it really comes down to the quality. Bass Metals is the operator of the Graphmada graphite project, and they are one of two ASX listed companies who are actually capable of producing Graphite. Graphite is a small market and Electric Royalties is keen to partner these companies at this stage and ultimately fund these groups into mid-tiers of their commodities.

The Graphmada asset is the flagship asset for Bass Metals and they will be pushing hard on it over the next 3-6 months to get into production and could possibly double or triple production with minimal Capex as resources are there.

The VOX royalty involved $2M worth of shares with no cash component to it and the Sprott deal involved $9M worth of shares with the only cash element as the down payment when they signed the deal.

The 3rd project, the Lithium project is in Quebec which involved only $1M shares. This project is situated right next to all the hydropower required for mine production and is perfectly located from an infrastructure point of view and the Quebec Government is very supportive of development. Lithium Royalty Corp also did a royalty financing on this asset about a month earlier than Electric Royalties and paid about $6.5M cash on their funding of about $3M of the equity. In terms of the spin out of the asset, they're raising $18M to advance this asset forward. Electric Royalties believes there is more exploration upside to come and expects that it's going to be fast tracked over the next 2-years.

Technical Commodities, Contributions, & Representative Certainty

There is always a risk in mining but this lithium royalty covers the drilling and the current resources. It has boundaries on both sides and all the drilling is pretty shallow and the grades are very good. They've got an exploration target there and could probably put together a resource today. Electric Royalties expects this project will come together very quickly and it is perfectly located around clean hydropower and good road access.

The plan for Electric Royalties is diversification and they aim to get 10 of these assets to spread their risk. They have spent about 2-years looking at assets in this space and feel pretty confident that this lithium project is special.

Stocks, Short Term Revenue, Private Transactions & Deal Decisions

At the moment, Electric Royalties has about a $25M market cap. The share price has moved sideways since we last spoke in June. The company hasn’t got access to much cash and issues shares at various prices instead where they have selected their partners carefully, people buying into the bigger picture of Electric Royalties going forward.

Electric Royalties thinks there is a tremendous amount of opportunity in this sector and by focusing on the clean energy, metal space, they have differentiated themselves from 95% of the royalty groups out there. They look at it as a broader opportunity and their strategy is to stay diversified across each of these commodities. By staying diversified with all these commodities that have exponential growth forecasts across the board, their plan is to tie themselves to this clean energy revolution and offer investors exposure to the underlying building blocks of that. It is more about the overall transition to clean energy, rather than any one commodity.

Electric Royalties has only been public for about a year and already has a portfolio of 17 royalties. Three of these royalties will produce cash flow in the near term, since they've released announcements, have already been in production or have been in care and maintenance. The company also has a number of assets at feasibility stage in the portfolio and some that are 4 or 5-years out which are exciting prospects too. They are expecting two of them alone within their Vanadium royalty and their Manganese royalty to be looking at about $7.5M a year in cash flow and those have big mine lives in addition.

Electric Royalties needs to ensure that they find the right deals as revenue is really important for them as they become established. They have proved that they can syndicate a deal. Sprott is a very supportive partner and Electric Royalties is keen to do other deals with them. They are keen to get another big cash flowing royalty before they go back to market and to pick up some of the deals that they had in the pipeline that are very value accretive.

To find out more, go to the Electric Royalties Website

Analyst's Notes

Subscribe to Our Channel

.jpg)

.webp)

Stay Informed