Electric Royalties Positions for Revenue Growth Across 43 Royalties

Electric Royalties holds 43 clean energy metals royalties valued at under CAD $20M, with multiple assets targeting production in 2–5 years and strategic M&A under active consideration.

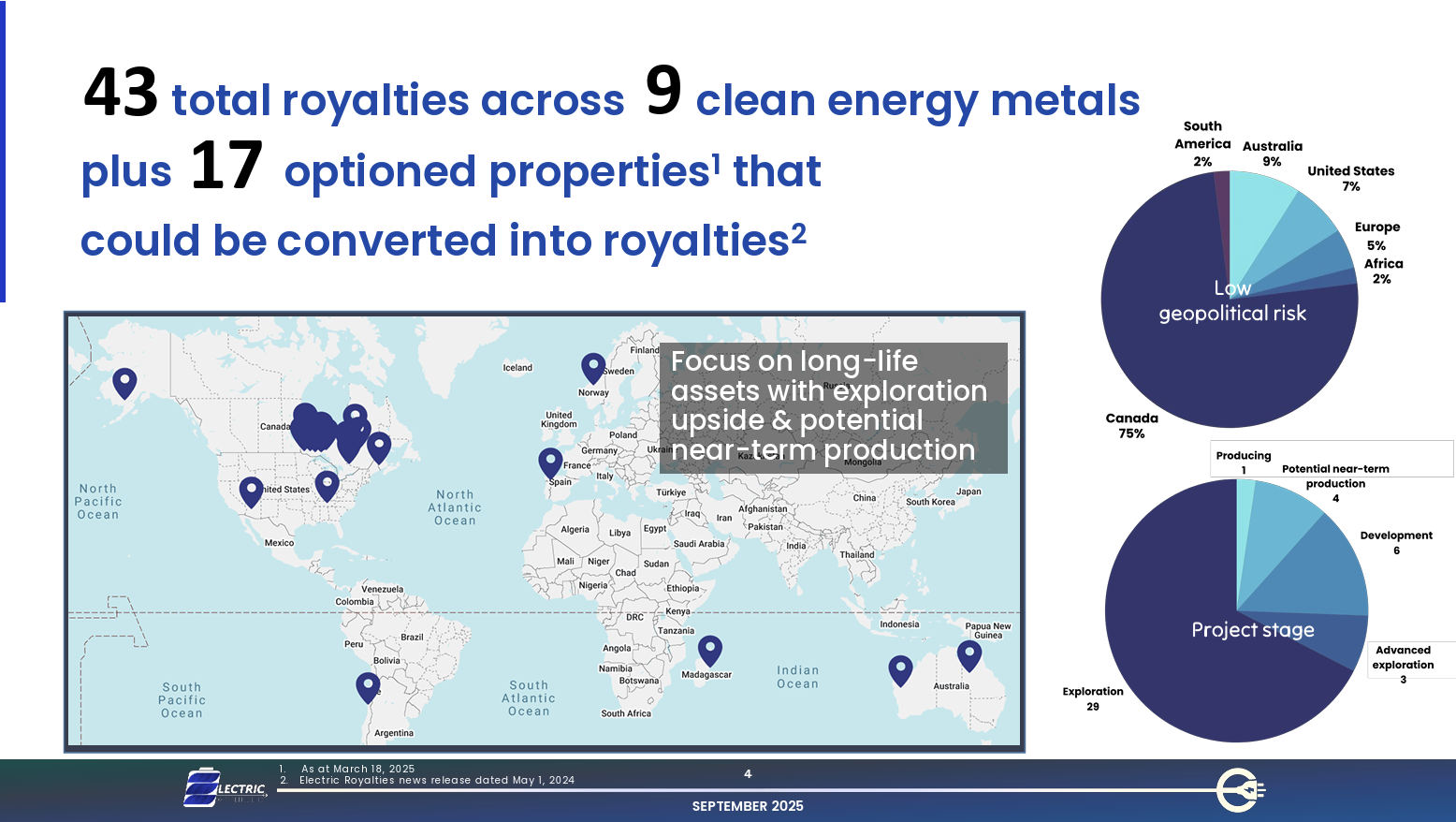

- Electric Royalties has assembled a portfolio of 43 clean energy metals royalties spanning copper, zinc, tin, graphite, manganese, lithium, and nickel. Currently valued at less than C$20 million, $ELEC represents a significant discount to comparable royalty companies that trade well above $200 million with far fewer assets.

- The company's producing royalty at the Punitaqui copper-gold mine in Chile is expected to generate over $500,000 this year with potential of up to $1 million demonstrating a lean cost structure that limits dilution risk during the portfolio's development phase.

- A concentrated pipeline of near-term production catalysts including Mont Sorcier (iron-vanadium, Quebec), Bissett Creek (graphite, Ontario), the Zonia copper project (Arizona), and Seymour Lake (lithium, Ontario) are each targeting production milestones within two to five years.

- Several of the company's most material assets are backed by sovereign capital commitments, including a $500 million UK Export and Import Bank financing for Mont Sorcier and Canadian government funding for both Bissett Creek and Seymour Lake, reducing execution risk and accelerating development timelines.

- CEO Brendan Yurik confirmed that strategic M&A is under active consideration, noting that combining royalty portfolios offers a low-risk path to revenue diversification and operational leverage, while the company's tightly held share structure ensures management retains control over the process.

While most players in the royalty and streaming space have anchored their portfolios around gold and silver, Electric Royalties has staked a different claim: one built on the metals underpinning the global energy transition. With 43 royalties across copper, zinc, tin, graphite, manganese, lithium, and nickel, the company is positioning itself as a differentiated vehicle for investors seeking exposure to clean energy metals through a royalty structure. At PDAC 2026, CEO Brendan Yurik sat down to provide an update on the portfolio, the company's path to cash flow, and why management believes the current valuation represents a significant disconnect from long-term fundamental value.

Royalties Across the Clean Energy Metals Complex

Electric Royalties has assembled a portfolio deliberately weighted toward the metals required to build out the clean energy infrastructure of the coming decades. The portfolio's commoditybreakdown is broadly distributed at: 15% copper, 15% lithium, 15% manganese, 15% graphite, and a further 15% split across tin, nickel, and zinc. This diversification across commodity types reflects both the breadth of the energy transition supply chain and management's view that multiple metals will face structural supply deficits over the medium term.

The company currently has one producing royalty: the Punitaqui copper-gold mine in Chile, majority-owned by the Yorktown Group which manages approximately $3.2 billion in assets. The royalty is expected to generate over $500,000 in revenue this year, with a near-term target of approximately $1 million annually. Given that Electric Royalties operates with a corporate G&A of roughly $1 million per year, the company is approaching operational self-sufficiency from a single asset, a lean cost profile that underpins management's confidence in the portfolio's leverage potential.

The Near-Term Catalyst Funnel

Beyond Punitaqui, the company has identified a concentrated pipeline of royalties that management believes could enter production within the next two to five years, each representing a step-change in revenue relative to the current base.

- Bissett Creek is a graphite project operated by Northern Graphite, which has secured Canadian government funding. Northern Graphite is targeting Bissett Creek as its flagship asset, with a production profile that has since been scaled to approximately four times the level at which Electric Royalties initially acquired its royalty. The project reportedly holds 70 years of resources at its prior production rate.

- The Zonia copper project, now the sole focus of Edge Copper, recently doubled its resource to one billion pounds of copper. A 50,000-foot drill programme is currently underway, a feasibility study is expected within the coming years, and construction timelines of approximately 18 months have been outlined and an initial capital expenditure of $100 million.

- Mont Sorcier, an iron-vanadium project in Quebec, is perhaps the most advanced near-term catalyst. A feasibility study is expected in Q2 2026, and the project has already secured approximately $500 million in financing from the UK Export and Import Bank with Glencore named as a project partner. Yurik estimates that Mont Sorcier could add $1 to $1.5 million annually in royalty revenues to Electric Royalties upon entering production, with a projected mine life exceeding 40 years.

- Seymour Lake, a lithium project, has received an extension of a letter of intent for $100 million in Canadian government funding and is targeting production within a two- to three-year window.

Collectively, Yurik notes that each of these royalties entering production would represent an eight-times or greater increase over current revenue levels, with several potentially materialising in the same window.

The Funding Gap: Where Electric Royalties Operates

A key element of the Electric Royalties investment case lies in its operating niche. The company targets royalty acquisitions in a segment of the market that larger capital pools are structurally unable or unwilling to address. As Yurik explained:

"When you look at deals under $15 million which is the vast majority of opportunities out there, there's almost no capital for those. And so, there's definitely still opportunity out there for us."

Most dedicated clean energy metals private equity funds have concentrated capital into a small number of large transactions and none of them routinely engage with deals below the $15 million threshold. This leaves a broad universe of royalty acquisition opportunities accessible to Electric Royalties at terms that would be unavailable to a better-capitalised competitor. The Punitaqui royalty is an example of this approach: acquired at a price that reflected its sub-scale profile at the time, it is now generating meaningful cash flow backed by a multi-billion-dollar private equity operator.

Interview with Brendan Yurik, CEO of Electric Royalties Ltd.

Governments as Capital Partners

The backdrop for Electric Royalties' portfolio is one of accelerating government intervention in critical minerals supply chains. Yurik pointed specifically to the $500 million UK Export and Import Bank commitment to Mont Sorcier, the Canadian government funding behind both Bissett Creek and Seymour Lake, and the emergence of a $5 billion co-investment programme between Orion Resource Partners and the US government as evidence that sovereign capital is beginning to flow toward projects in which Electric Royalties holds royalties.

On the domestic sourcing imperative, Yurik noted that the company's asset base has been deliberately geographically concentrated in jurisdictions aligned with this trend. The Sleitat tin deposit in the United States, the only economically viable domestic tin resource in the country, has received no attributed value in current market pricing, but Yurik believes it could attract government-backed activity given that the US has not produced domestic tin since 1986.

Strategic M&A and Capital Structure

Electric Royalties is actively exploring strategic M&A as a parallel path to portfolio growth. With over 50% of shares held by the Yurik and Gleason families, the company cannot be subject to hostile acquisition but management is open to combining portfolios with other royalty companies to achieve diversification and cost efficiencies without incremental operational risk. Yurik drew a parallel to the acquisition of Lithium Royalty Corp by Altius Minerals for over $500 million, noting the consolidation dynamic that is beginning to emerge in the clean energy metals royalty space.

Regarding capital access, Yurik acknowledged that while gold and silver companies are experiencing relatively easy financing conditions, the critical metals space remains comparatively underserved. Nevertheless, he noted growing engagement from private equity groups that have spent the past three years developing the technical expertise to evaluate clean energy metals royalty deals, and expressed confidence in the company's ability to fund a near-term acquisition:

"I do think we're actually going to be able to access that capital and we do have a number of good deals. I will say if we're going to add something rather than do M&A, it'll be a very impactful royalty. It'll be cash flowing.

Any new capital deployment, Yurik emphasised, would be directed toward a cash-flowing royalty consistent with the company's broader objective of compressing the gap between corporate costs and revenues ahead of the portfolio's multi-year production inflection.

Valuation Context

Electric Royalties is currently valued at less than C$20 million. Yurik noted that comparable royalty companies with one or two royalties have achieved market capitalisations in excess of $200 million, and that mid-tier royalty platforms are trading well above $1 billion. Against that peer context, the company's 43-royalty portfolio with multiple assets at advanced development stages and meaningful government-backed operators represents a material valuation gap to sector norms. The ratio of current valuation to the sector's mid-tier benchmark implies a 50-times rerating potential in absolute terms, a comparison management cites not as a price target but as an illustration of where the current entry point sits relative to the royalty sector's precedent transactions and trading multiples.

The Investment Thesis for Electric Royalties

- Electric Royalties is one of very few publicly listed royalty companies focused exclusively on clean energy metals. Most royalty platforms remain anchored to precious metals, leaving significant white space in the critical minerals royalty market.

- At under CAD $20 million market capitalisation, Electric Royalties trades at a fraction of comparable royalty companies. Investors are acquiring 43 royalties at a per-royalty cost that appears structurally anomalous relative to sector pricing.

- Portfolio-scale production inflection within a defined window with multiple royalties: Mont Sorcier, Bisichi Creek, Arizona copper, Seymour Lake, are targeting production milestones within two to five years. Each asset entering production has the potential to add multiples of current annual revenue. The convergence of several in the same window creates a non-linear revenue profile.

- With corporate costs of approximately $1 million annually and a single producing royalty nearly covering that base, the company has limited dilution risk relative to earlier-stage peers. Management has significant personal capital invested and strong incentive alignment.

- Several of the company's most material royalties such as Mont Sorcier, Bisichi Creek, Seymour Lake are backed by government funding commitments or are partnered with institutional-grade operators. This reduces the execution risk associated with development timelines.

- Strategic portfolio consolidation with another royalty company could compress the discount to NAV rapidly, without requiring any individual asset to enter production. The Lithium Royalty Corp/Altius precedent illustrates the valuation uplifts achievable through this route.

The Critical Minerals Royalty Opportunity

The global energy transition has generated broad consensus around the need for substantially more copper, lithium, graphite, manganese, and tin but the capital markets infrastructure to finance the development of these assets remains conspicuously underdeveloped relative to the scale of the challenge. While gold and silver royalty companies benefit from a mature, well-capitalised ecosystem of royalty and streaming vehicles, the critical minerals equivalent is only beginning to take shape.

Major private equity funds dedicated to clean energy metals have emerged over the past several years, but they have concentrated capital into large-scale transactions and lack the mandate or flexibility to engage with smaller royalty acquisitions. This leaves the majority of royalty opportunities across the critical minerals development pipeline effectively uncapitalised, creating a durable competitive advantage for platforms willing to operate in this space.

Sovereign capital is beginning to fill part of this void. Governments in Canada, the United States, the United Kingdom, and Australia have each initiated programmes that place public capital alongside private development of strategic mineral assets.

As Yurik observed, "The US government probably the biggest player for us. Governments around the world are definitely starting to play a much bigger role in the space and they're partnering up with private equity."

The $500 million UK Export and Import Bank commitment to Mont Sorcier and the Canadian government's funding of Bissett Creek and Seymour Lake are early instances of a trend likely to accelerate as domestic supply chain security moves up the policy agenda.

Royalty companies are insulated from capital expenditure overruns, operating cost inflation, and the execution risks that have historically challenged direct project developers in the critical minerals space. For investors, a royalty platform with well-positioned assets across the critical minerals supply chain may represent one of the more asymmetric risk-reward setups available in the broader resources sector.

TL;DR

Electric Royalties enters 2026 at a pivotal juncture. The company has spent several years assembling a 43-royalty portfolio in clean energy metals at a cost structure and entry pricing that larger capital pools could not replicate. One producing asset is approaching the point of covering corporate costs, while a cluster of advanced-stage royalties backed by government capital, institutional-grade operators, and in some cases completed feasibility work are approaching production decisions. The market has not yet priced this progression, leaving the company valued at a significant discount to the royalty sector by almost any comparative metric. Whether the value realisation comes through organic portfolio maturation, a strategic M&A transaction, or both, management has constructed a platform with meaningful upside and a cost base that limits the downside during the waiting period.

Frequently Asked Questions (FAQs) AI-Generated

Analyst's Notes

Subscribe to Our Channel

Stay Informed