Summit Royalties: How a New Precious Metals Royalty Company Amassed 47 Assets in Four Months

Summit Royalties: New precious metals royalty co. 47 assets, cash flow positive, trading 0.75x NAV at $85M cap. Targets $200-300M through accretive M&A.

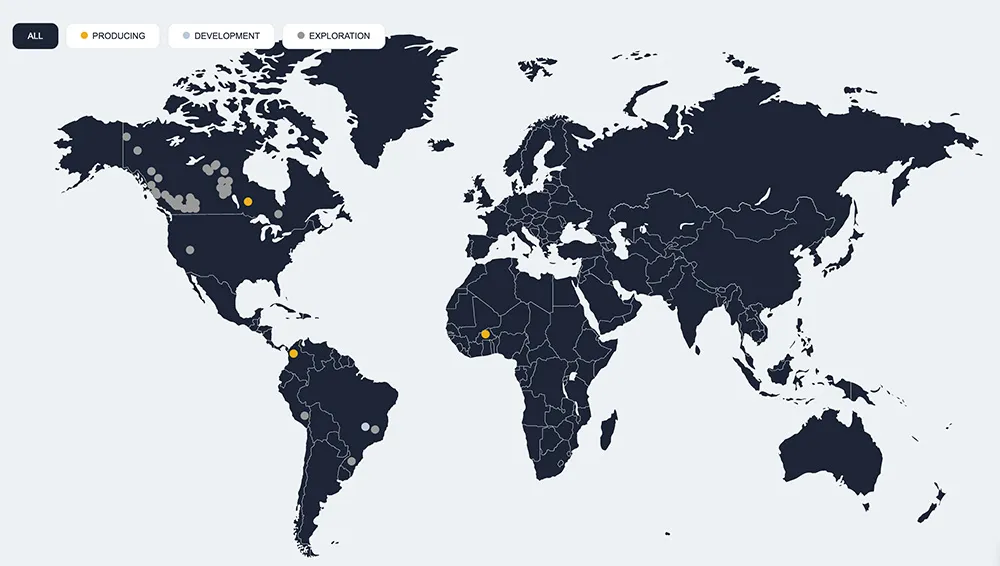

- Summit Royalties built a 47-asset portfolio in just four months through three major transactions, raising approximately $23M USD while becoming cash flow positive and never issuing warrants.

- The company has three producing assets generating revenue: Madsen (1% NSR yielding ~500 oz gold annually), Orezone (50% silver stream producing 37.5k oz), and Zancudo (ramping up in Q3 2026).

- With only two full-time employees, the team has completed $2 billion in royalty deals over the past decade, with management and directors owning 15% of the company.

- Trading at 0.75-0.8x NAV with an ~$85M USD market cap, Summit represents significant value compared to peers, having appreciated from $0.90 to $1.60 per share in under four months.

- The company targets scaling to $10M+ annual revenue and $200-300M market cap through accretive acquisitions, with a strong deal pipeline and access to institutional capital from prominent mining investors.

The precious metals royalty sector has experienced significant consolidation in recent years, creating a valuation gap for companies under $1 billion in market capitalisation. Summit Royalties has emerged as a new entrant targeting this opportunity, building a diversified portfolio of 47 assets in approximately four months while achieving cash flow positivity. The company's rapid development, experienced management team, and disciplined capital allocation strategy position it as a potential consolidation platform in the royalty space.

Building a Portfolio at "Furious Pace"

Summit Royalties executed three major transactions between May and September 2025 to assemble its initial asset base. The company acquired a portfolio from IAMGold for $17.5 million ($10 million cash and $7.5 million in stock, making IAMGold the largest shareholder). This was followed by a reverse takeover (RTO) with Eagle Royalties, which brought the majority of the company's royalty count, 3,000 retail shareholders, $3 million in cash, and the valuable Banyan royalty. During the RTO process, Summit also acquired the Madsen Royalty from Sprott Natural Resource Investment Partners, purchasing the asset from West Red Lake in Ontario.

In total, Summit raised approximately $23 million USD during this period while maintaining a disciplined capital structure. Notably, the company has never issued warrants, preserving shareholder value and avoiding dilutive financing structures common among junior resource companies. The equity has appreciated from $0.90 to $1.60 per share in less than four months of trading, reflecting market recognition of the portfolio quality and management execution.

Current Revenue-Generating Assets

Summit currently has three operating assets producing cash flow. The Madsen mine is a high-grade gold operation in Ontario guiding for approximately 50,000 ounces of production in 2025. Summit holds a 1% net smelter return (NSR) royalty, which translates to approximately 500 ounces of attributable gold production annually.

The Orezone asset represents a 50% silver stream at no ongoing cost to Summit. The mine is expanding from 120,000 to 250,000 ounces of gold production by the end of 2026, with Summit receiving a minimum of 37,500 ounces of silver annually. While Orezone does not break out silver production publicly, Summit receives monthly silver revenue from this stream.

The third producing asset is Zancudo, a smaller operation currently conducting direct shipping ore activities. The mine is installing a mill in Q3 2026, which will increase production capacity and royalty payments in 2027. CEO Drew Clark noted,

"One observation from all three of those assets is that they're all expanding right now. They're all being drilled and we love the fact that we're cash flow positive today with just that base, but they're all growing."

Near-Term Production Catalysts

Beyond current production, Summit has identified clear near-term growth from development projects. The Pitangui deposit, a satellite to Jaguar Mining's Turmalina mill in Brazil, begins construction in 2026 with production scheduled for 2027. This represents defined, committed production rather than speculative long-dated development, providing visibility for revenue growth.

The Banyan royalty offers significant exploration upside. Summit holds a 2% NSR on the Airstrip deposit where the high-grade discovery was made, and a 1% NSR on the western extension of the Powerline zone. Approximately 50% of Banyan's drilling in 2025 focused on Summit's 2% ground. While Banyan does not yet have a preliminary economic assessment, the company has raised $55 million Canadian and increased its market capitalisation from $70 million to over $540 million Canadian, driven largely by drilling results on Summit's royalty ground.

Interview with Drew Clark, CEO, Summit Royalties

The Team Behind the Execution

Summit operates with only two full-time employees: CEO Drew Clark and VP Connor Pugliese, who previously worked at Triple Flag. Between them, the team has completed approximately $2 billion worth of royalty transactions over the past decade. Clark previously worked at Metalla Royalty, where he executed 27 of the company's 32 deals. Connor's experience at Triple Flag includes executing half a billion dollars in streaming transactions and acquiring Mavericks Royalty.

The board includes individuals who have each built billion-dollar companies, providing strategic oversight and network access. Management and directors collectively own 15% of Summit, aligning incentives with shareholders. Clark emphasised the importance of accretive growth:

"The number one thing that you have to tell everyone is we are going to grow on an accretive per share basis. That's the end. Every time I transact, my company is worth more."

Sourcing Off-Market Opportunities

Summit faces competition from established royalty companies with larger balance sheets and lower costs of capital. However, the company believes its structure and valuation create opportunities. Trading at 0.75-0.8x net asset value (NAV) while peers trade at higher multiples, Summit can offer sellers attractive equity participation in a discounted vehicle with significant re-rating potential.

The company sources deals through bilateral negotiations rather than competitive auctions. In the case of IAMGold, Summit offered a creative structure that allowed IAMGold to own less than 20% for accounting purposes while participating in equity upside by pricing the transaction at 0.6x NAV. With the Madsen royalty, Summit learned of Sprott's intention to sell before a formal process began and preempted the auction by negotiating directly.

Summit has already bid over $200 million on assets it did not ultimately acquire, demonstrating both ambition and discipline. The company believes its current valuation and tight capital structure make it attractive to larger companies looking to monetise non-core royalty portfolios.

The Path to Multiple Expansion

Summit currently trades at approximately $85 million USD market capitalisation and 0.75-0.8x NAV. Management believes that scaling the business will compress the valuation discount and reduce the cost of capital. The company targets reaching $10 million in annual revenue and $150 million USD market cap, at which point institutional investor restrictions would begin to ease.

The company sees a clear path to $200-300 million market capitalisation through several portfolio transactions or potentially acquiring another royalty company. At this scale, Summit would become relevant to a broader universe of institutional investors and could pursue NASDAQ listing for additional liquidity.

Building Toward Critical Mass

Summit's growth strategy focuses on portfolio acquisitions and potential royalty company consolidation. The company believes there is a gap in the market for royalty companies under $1 billion market capitalisation, particularly as recent M&A activity has consolidated the sector. Summit has been approached by larger companies looking to monetise royalty portfolios, suggesting deal flow may come to the company rather than requiring aggressive competition in auctions.

The company maintains flexibility in deal structuring, using combinations of cash, equity, and creative terms to align with sellers' objectives. While Summit focuses primarily on precious metals (gold and silver), management does not exclude copper exposure if attractive opportunities arise, though the company will not pursue battery metals like lithium, manganese, or uranium.

Clark sees two potential outcomes for investors, both positive. Either Summit successfully scales to become a dividend-paying, exchange-listed royalty company with improving multiples as assets advance, or the company becomes an M&A target for a larger royalty company seeking accretive consolidation.

Conclusion

The precious metals royalty sector has experienced significant consolidation, creating a valuation gap and opportunity for new entrants. Summit Royalties emerges at an inflection point where established royalty companies trade at premium multiples while the sector continues expanding (from $3 billion to $150 billion in market capitalisation over 20 years). Gold prices near all-time highs and institutional demand for precious metals exposure support royalty company valuations.

Additionally, larger producers increasingly seek to monetise non-core royalty portfolios for balance sheet optimisation, creating deal flow for consolidators like Summit. The company's focus on accretive transactions below 1.0x NAV while peers trade above 1.2x NAV positions Summit to benefit from multiple expansion as it scales. With institutional funds increasingly restricting investments to companies above critical size thresholds, Summit's rapid growth strategy targets crossing these barriers to unlock broader investor access and valuation re-rating.

TL;DR: Executive Summary

Summit Royalties has built a 47-asset precious metals royalty portfolio in four months, achieving cash flow positivity while trading at 0.75-0.8x NAV with an $85M market cap - a significant discount to peers. The experienced management team (having completed $2B in deals) owns 15% and targets scaling to $10M revenue and $200-300M market cap through accretive acquisitions. With three producing assets expanding, near-term production catalysts, and access to institutional capital, Summit offers investors leveraged exposure to either independent growth with multiple re-rating or value-creating M&A consolidation.

FAQ's (AI Generated)

The company has only been public for four months and lacks the scale and analyst coverage of peers. As Summit crosses revenue and market cap thresholds that unlock institutional investor access, the valuation discount should compress toward peer multiples.

Summit sources deals bilaterally before competitive processes begin, offering creative structures and equity participation in a discounted vehicle with significant re-rating potential. The team's $2B transaction track record provides access to off-market opportunities.

Primary risks include: execution risk on accretive acquisitions, operational underperformance at underlying mining assets, difficulty accessing capital at favorable terms, and gold/silver price volatility impacting royalty values and acquisition multiples.

The company prioritises accretive portfolio acquisitions that expand scale and revenue while maintaining NAV multiples below 1.0x. Management targets transactions that improve per-share metrics and move the company toward $10M revenue and $150M market cap thresholds.

Summit achieved cash flow positivity from inception with three producing assets, maintains a warrant-free capital structure, has experienced management with proven deal execution, and focuses exclusively on precious metals rather than battery metals, maintaining clear strategic focus.

Analyst's Notes

Subscribe to Our Channel

Stay Informed