From $3,600 to $3,760: Gold's Record Run Reinforces Institutional Demand

Gold surges to record $3,760/oz on Fed easing and geopolitical risks. Institutional flows hit 3-year highs. Mining stocks with strong balance sheets poised to benefit.

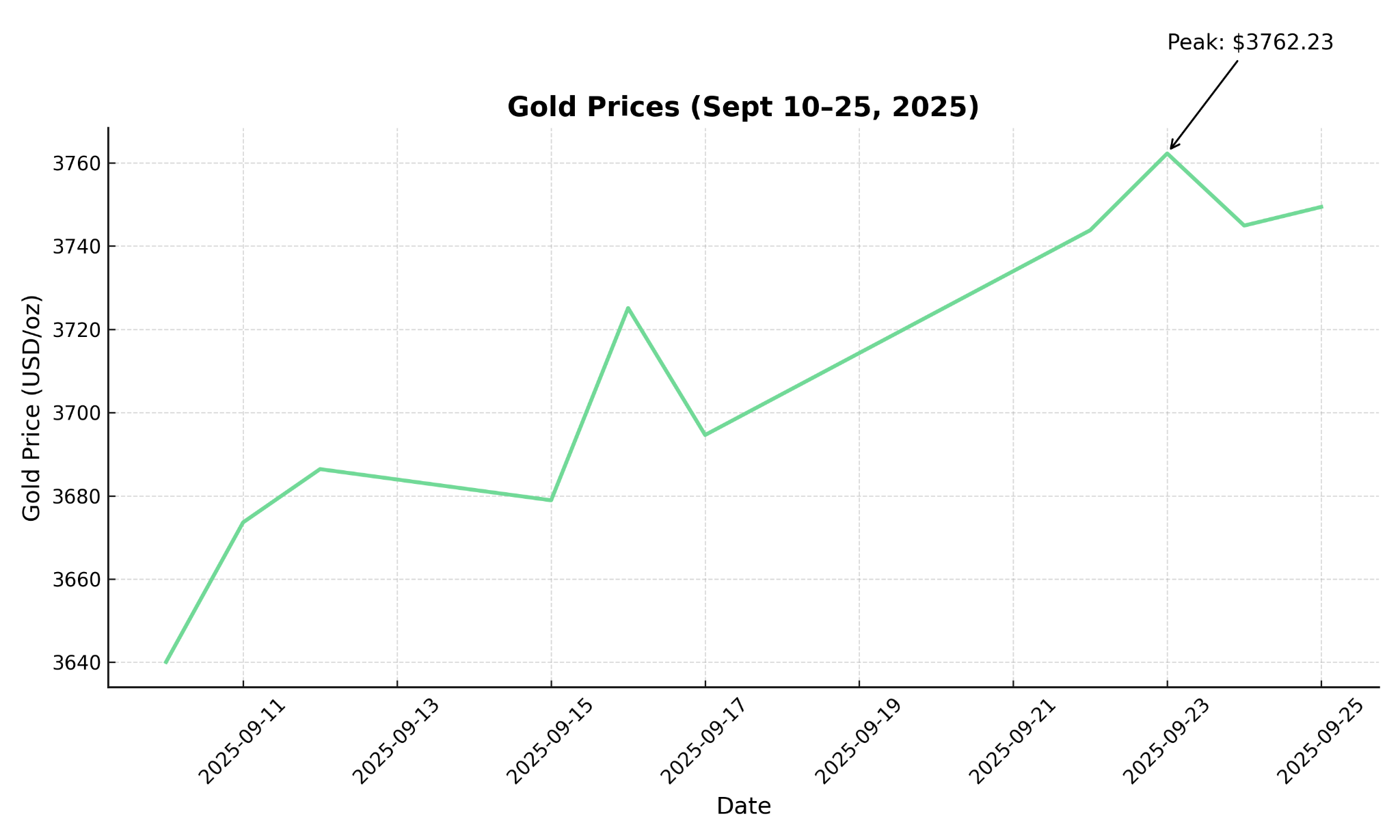

- Gold advanced from $3,600/oz to a record $3,760/oz in recent weeks, supported by Fed easing, weak US labor data, and heightened geopolitical risk.

- The Relative Strength Index (RSI) hit historic overbought levels, signaling possible short-term consolidation but confirming strong secular momentum.

- Institutional flows surged with ETF holdings reaching a three-year high, and central banks extended record purchasing streaks, reinforcing structural demand.

- Producers and developers with strong balance sheets and low All-In Sustaining Costs (AISC)—such as Integra Resources, Perseus Mining, Serabi Gold, West Red Lake Gold Mines, and i-80 Gold—are positioned to capture outsized leverage.

- Long-term investment implications include structural de-dollarization, geopolitical fragmentation, and cost-curve pressure ensuring sustained demand for gold and increased capital rotation into mining equities.

Macroeconomic Drivers of Gold's Record Run

The Federal Reserve's recent 25 basis point cut has fundamentally altered gold's risk-reward equation, reducing the opportunity cost of holding the non-yielding asset while markets price in additional easing through 2025. This dovish stance reflects a delicate balancing act between persistent inflationary pressures and weakening labor market dynamics, with unemployment claims rising and job creation decelerating across key sectors.

The U.S. dollar's trajectory remains central to gold's performance, with recent strength proving temporary against medium-term structural headwinds. As real yields compress and the Fed signals continued accommodation, dollar-denominated assets face devaluation pressure that historically benefits precious metals. This dynamic particularly favors U.S.-based developers like i-80 Gold, which operates in Nevada's established mining jurisdiction, and U.S. Gold Corp, whose Wyoming copper-gold project benefits from domestic policy support for critical minerals as Vice President of External Affairs & Sustainability of Integra Resources Mark Stockton highlights the commodity’s jurisdictional advantages:

"In the US, we're in a very fortunate time where everyone from state, federal, and down to the county governments are all really singing the same tune as it comes to securing domestic sources of minerals."

Lower financing costs enable capital-intensive mining projects to achieve improved project economics, while jurisdictional stability provides additional value for North American assets. U.S. Gold Corp's fully permitted Cheyenne project exemplifies this advantage, positioned within 20 miles of major infrastructure while benefiting from both copper and gold's critical mineral classifications under current administration priorities.

Geopolitical Instability & the Safe-Haven Bid

Multiple geopolitical flashpoints have created a sustained safe-haven premium that differentiates 2025's gold rally from previous cycles. Russia-Ukraine conflict escalation, NATO posturing in Eastern Europe, and Middle East volatility have combined with Fed accommodation to create optimal conditions for precious metals appreciation.

Unlike historical rallies driven by single crisis events, current geopolitical risks exhibit layered complexity with no clear resolution timeline. This persistence supports higher base-case gold prices while creating asymmetric upside potential during crisis escalations. For mining companies, this environment rewards geographical diversification strategies that mitigate single-jurisdiction exposure.

Institutional & Structural Demand Trends

Institutional capital allocation to gold has reached inflection point levels, with Exchange-Traded Fund (ETF) holdings hitting three-year peaks as portfolio managers reassess traditional 60/40 allocations. This institutional migration reflects fundamental shifts in monetary policy expectations and long-term portfolio construction, moving beyond tactical safe-haven positioning toward strategic allocation decisions.

Central bank gold purchases continue at record pace, driven by de-dollarization initiatives and foreign exchange reserve diversification mandates. These structural buyers operate with multi-decade investment horizons, creating persistent underlying demand that supports higher long-term price floors regardless of short-term market volatility.

The institutional appetite for scalable gold assets has particularly benefited development-stage companies with district-scale potential. New Found Gold's Queensway project in Newfoundland exemplifies this trend, attracting institutional interest through systematic exploration programs that continue expanding the resource footprint. The company's recent board appointments, including former Newfoundland and Labrador Premier Andrew Furey, signal strategic positioning for institutional engagement, as Chief Executive Officer Keith Boyle highlights:

"We're really strengthening our board, really making a statement that we're here to stay… The political world and all those connections really do help a business and that oversight making sure that we advance in the right way."

This institutional flow extends beyond exploration assets to near-production developers, where visibility into cash flow generation attracts growth-oriented capital. West Red Lake Gold Mines' successful Madsen mine restart demonstrates this dynamic, with systematic technical validation attracting institutional investors seeking exposure to new gold production in established mining districts.

Technical Momentum & Investor Psychology

Gold's advance from $3,600 to $3,760 reflects disciplined buying rather than speculative excess, with price action characterized by higher lows and measured consolidations rather than parabolic moves. The Relative Strength Index (RSI) reaching historically overbought levels signals potential near-term consolidation, but underlying momentum remains intact as fundamental drivers continue strengthening.

The psychological shift from crisis-driven to confidence-driven buying represents a structural change in investor behavior. Rather than panic purchases during market dislocations, current institutional flows reflect calculated portfolio repositioning based on macroeconomic analysis and long-term structural trends. This foundation provides greater sustainability for higher gold prices compared to speculative bubbles.

For development-stage mining companies, this technical strength translates into improved valuation multiples and enhanced financing conditions. Integra Resources' DeLamar project demonstrates how conservative feasibility assumptions create operational leverage when gold prices exceed base-case scenarios, providing investors with asymmetric upside exposure to continued bullish momentum.

How Producers, Developers & Explorers Are Positioned

Balance sheet strength has emerged as the primary differentiator among mining companies during periods of elevated gold prices and market volatility. Companies with substantial liquidity can maintain development schedules, pursue strategic acquisitions, and return capital to shareholders while competitors face financing constraints.

Perseus Mining highlights this financial discipline, reporting zero debt alongside consistent dividend payments. Chief Executive Officer & Managing Director Jeff Quartermaine detailed the company's recent performance:

"Our revenue was a touch over $1.25 billion US, up 22%. The profit after tax was $421.7 million USD, up 16%. Operating cash flow was $536.7 million, up 25%... We have zero debt at the present time."

This financial strength enables Perseus to advance its Nyanzaga project in Tanzania toward January 2027 production while maintaining operational stability across existing assets. The company's target of 500,000-600,000 ounces annually from Nyanzaga will establish it among larger-scale producers with correspondingly lower cost structures.

Project Milestones & Operational Visibility

Development catalysts create discrete revaluation opportunities as companies demonstrate execution capability and approach cash flow generation. The transition from resource definition to production provides measurable value creation milestones that institutional investors can evaluate and price accordingly.

West Red Lake Gold Mines' Madsen restart exemplifies this progression, with successful bulk sampling and test mining providing technical validation ahead of commercial production declaration. Vice President of Communications Gwen Preston emphasized the company's methodical approach:

"The fact that we could reconcile our expected and actual results through a test mining and bulk sample program was the final check mark that we needed technically to put the mine back into production."

Cabral Gold's two-stage development strategy at Cuiú Cuiú provides another model for measured progression, with oxide starter project economics supporting subsequent primary resource development. Vice President Project Development John Sestan outlined the integrated approach:

"The starter project has a very strong Internal Rate of Return (IRR) of 77%, a 10-month payback, and is expected to generate after-tax cash flows averaging over $20 million annually during its initial six-year mine life, all at $2,500 an ounce."

Exploration Outlook & Resource Development

Systematic exploration programs continue adding optionality value, particularly for companies with district-scale land positions in established mining camps. Resource growth provides tangible value creation independent of gold price movements while maintaining leverage to commodity price appreciation through expanded production profiles.

Serabi Gold's brownfield programs target resource expansion from current levels toward 1.5 million ounces by end-2026, supporting eventual 100,000-ounce annual production rates. Chief Executive Officer Michael Hodgson emphasized the self-funded growth strategy:

"We're doing exploration as much as we can, we got six rigs turning and that's a lot of meters that we're drilling every week, every day, but we can fund all of that through cash flow."

New Found Gold's systematic exploration at Queensway continues defining district-scale potential through high-grade intersections across multiple zones. The company's evolution from pure exploration toward development reflects resource confidence and operational capability building that attracts institutional capital seeking scalable asset exposure.

Risk Management & ESG Considerations

Operational risk management has evolved beyond traditional mining hazards to encompass regulatory approval timelines, community engagement effectiveness, and environmental compliance standards. Companies demonstrating proactive stakeholder management achieve superior permitting outcomes while reducing development timeline uncertainty.

U.S. Gold Corp's fully permitted status at CK Gold exemplifies effective regulatory navigation, achieving mine permits on state land with established infrastructure access. This regulatory advantage reduces execution risk while providing development flexibility in a supportive jurisdictional environment.

i-80 Gold's autoclave hub-and-spoke strategy demonstrates operational efficiency through existing infrastructure utilization while achieving superior metallurgical recovery rates. This approach reduces both capital intensity and environmental impact while maximizing resource extraction from multiple deposit types across the Northern Nevada land position.

Investor Implications & Risk Outlook

The primary risks to gold's continued appreciation center on Federal Reserve policy surprises, geopolitical de-escalation, and technical corrections following extended price advances. A hawkish Fed pivot could strengthen the dollar and raise real yields, reducing gold's relative attractiveness. Similarly, resolution of major geopolitical conflicts could eliminate risk premiums while reducing safe-haven demand.

However, these risks appear manageable given structural demand drivers and institutional allocation trends. Central bank purchasing programs operate independently of short-term sentiment while ETF flows reflect strategic positioning rather than tactical trades. Lower cost of capital benefits mining companies through improved project economics and enhanced financing availability.

Companies with scalable projects and strong balance sheets provide asymmetric upside exposure to continued gold strength while maintaining downside protection through conservative development assumptions. Integra Resources and i-80 Gold exemplify this positioning, with feasibility studies and restart timelines aligned with 2025-2026 macroeconomic catalysts.

The Investment Thesis for Gold

- Fed easing cycles combined with structural dollar weakness support higher long-term gold prices beyond current levels.

- Central bank buying programs and ETF inflows reinforce demand sustainability while reducing available supply for private investors.

- Geopolitical instability adds persistent risk premiums that enhance safe-haven appeal during market volatility.

- Producers with low All-In Sustaining Costs like Perseus Mining and Serabi Gold deliver expanding margins at higher gold prices while maintaining operational flexibility.

- Developers approaching production including Integra Resources, West Red Lake Gold Mines, and U.S. Gold Corp gained valuation leverage through production ramp-up and cash flow generation.

- Explorers with scalable assets such as New Found Gold and Cabral Gold provide discovery upside aligned with institutional flows seeking large-scale asset exposure.

- Companies demonstrating strong balance sheets and disciplined capital allocation benefit from improved financing conditions while maintaining strategic flexibility.

- Geographic diversification across stable jurisdictions reduces operational risk while providing exposure to global gold price appreciation.

- Development timelines aligned with macroeconomic catalysts create discrete revaluation opportunities as projects progress toward production.

Gold's Strategic Pivot: Navigating the New Investment Landscape

Federal Reserve accommodation combined with persistent geopolitical instability has driven gold to record highs while establishing sustainable demand foundations. Structural factors including central bank diversification, institutional portfolio allocation, and currency debasement concerns reinforce long-term positioning beyond traditional safe-haven dynamics.

Institutional flows and liquidity expansion into mining equities create favorable conditions for well-capitalized companies across the development spectrum. Investors must balance short-term technical risks with compelling long-term macro tailwinds that support higher gold prices and mining company valuations. Gold remains strategically relevant for portfolio diversification, with established miners across stable jurisdictions offering the most compelling risk-adjusted exposure to this macro theme.

TL;DR

Gold's record surge from $3,600 to $3,760 per ounce reflects a fundamental shift driven by Federal Reserve easing, persistent geopolitical instability, and unprecedented institutional demand. ETF holdings have reached three-year peaks while central banks continue record purchasing programs, creating structural supply constraints. This environment particularly benefits mining companies with strong balance sheets and low production costs, including established producers like Perseus Mining and developers approaching production such as West Red Lake Gold Mines and Integra Resources. The dovish monetary policy, currency debasement concerns, and geographic diversification strategies position gold miners for sustained outperformance as institutional capital increasingly views precious metals as essential portfolio components rather than merely crisis hedges.

FAQs (AI-Generated)

Federal Reserve easing policies, weakening U.S. dollar, geopolitical tensions, and unprecedented institutional buying through ETFs and central bank purchases are the primary catalysts behind gold's current rally.

Companies with strong balance sheets, low all-in sustaining costs, and diversified geographic exposure tend to outperform, including established producers and developers approaching commercial production with proven reserves.

Unlike previous speculative runs, current demand is driven by structural factors including central bank diversification, institutional portfolio allocation, and persistent geopolitical risks, suggesting greater sustainability.

Record central bank buying removes supply from private markets while signaling institutional confidence in gold's long-term value, creating upward pressure on prices and mining company valuations.

Primary risks include Federal Reserve policy surprises toward hawkishness, significant geopolitical de-escalation, or technical corrections following extended price advances, though structural demand factors provide downside support.

Analyst's Notes

Subscribe to Our Channel

Stay Informed