From Surplus to Scarcity: How Slower Production Growth Is Driving a Structural Copper Deficit by 2026

The ICSG projects a 150,000-ton copper deficit by 2026 as production growth slows to 0.9%. Declining grades, rising capex, and electrification demand reshape the market.

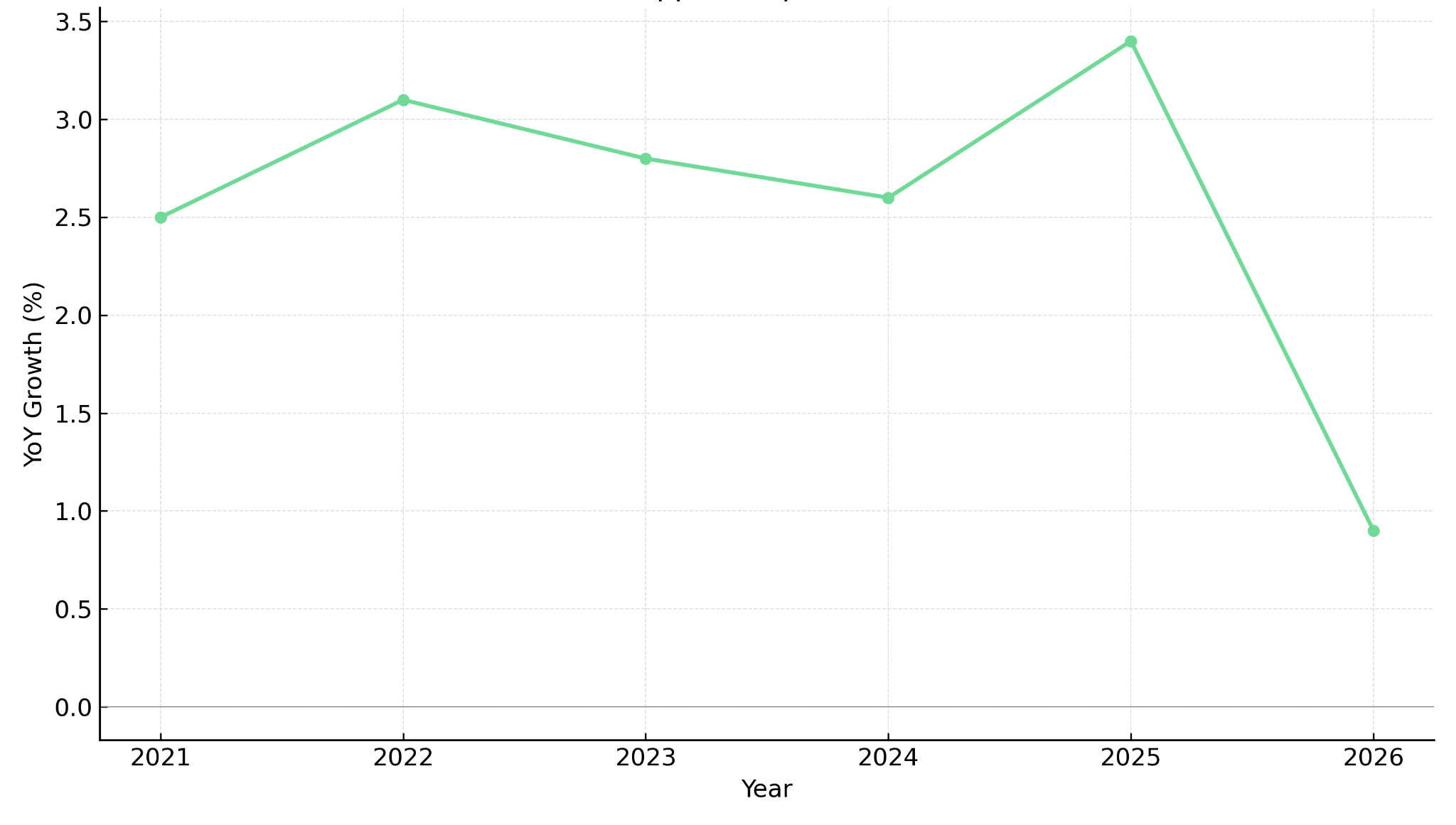

- The International Copper Study Group (ICSG) projects a refined copper deficit of 150,000 tons in 2026, reversing its earlier surplus forecast.

- The shift reflects structural supply constraints, driven by declining grades, rising capex intensity, and permitting delays, rather than temporary demand fluctuations.

- Refined production growth is slowing to just 0.9% in 2026, exposing the sector's chronic inability to deliver new tonnes even amid strong prices.

- Electrification, renewable power, AI infrastructure, and demographic growth are intensifying long-term demand.

- For investors, the transition from surplus to scarcity favors capital-efficient projects, high-grade discoveries, and stable jurisdictions, key factors shaping the next re-rating cycle for copper equities.

The Inflection Point: From Surplus to Structural Deficit

The International Copper Study Group's latest forecast marks a structural turning point for copper. After years of modest surpluses, the ICSG now expects the refined market to swing to a 150,000-ton deficit in 2026. The change is not cyclical, it is systemic.

Refined output growth is expected to slow to just 0.9% in 2026, compared to 3.4% in 2025. The key driver: the system can no longer produce new supply fast enough to match demand. Depletion rates are rising faster than replacement rates, leaving the global supply chain trapped in a self-reinforcing squeeze. This underlines copper's transformation from an industrial commodity to a strategic scarcity asset, one whose price trajectory will increasingly be defined by the physical limitations of mining itself.

The swing from surplus to deficit represents a durable shift in the investment thesis: copper prices are becoming a function of supply constraints, not demand shocks, rewarding exposure to disciplined, low-cost development projects.

Defining the Structural Deficit: A Systemic Breakdown in Supply Elasticity

Global copper grades have fallen from 1-2% historically to below 0.7%, forcing miners to process exponentially more rock per tonne of copper. Even multi-billion-dollar reinvestments, such as BHP's $10 billion at Escondida, are only maintaining flat output. This "running to stand still" phenomenon reveals how geological exhaustion has replaced cyclical volatility as the sector's defining feature.

Exploration-focused companies are responding by seeking higher-grade, near-surface mineralization in lower-risk environments. In Canada's Yukon, Gladiator Metals is drilling the historic Whitehorse Copper Belt, an area with demonstrated grades of >1.5% copper equivalent (CuEq), including recent intercepts of 98 meters at 1.49% copper with zones exceeding 7%. The company is targeting over 100 million tonnes at above 1% copper. With a maiden resource expected in the first quarter of 2026, Gladiator highlights how high-grade discovery in stable jurisdictions can deliver disproportionate leverage in a supply-constrained market.

The historic production from the belt underscores the quality of the mineralization. Jason Bontempo, Director and Chief Executive Officer of Gladiator Metals, references past operations:

"Hudbay Mining had operated from one small deposit on the belt and they'd mined 10 and a half million tons at 1.5% copper and almost a gram of gold."

Rising Capital Intensity & Financing Challenges

The average capital intensity for new mines has doubled, from $8,000–12,000 per annual tonne of capacity to $15,000–20,000, limiting new project sanctioning. In contrast, projects that can deliver new copper under $12,000 per tonne of installed capacity demonstrate how capital discipline can become a structural differentiator.

Marimaca Copper's oxide project in coastal Chile outlines a 39% internal rate of return (IRR) and net present value at 8% discount rate (NPV8%) of $1.1 billion, underpinned by a low strip ratio and second-quartile all-in sustaining cost (AISC) of $2.09 per pound. The project benefits from proximity to the Port of Mejillones (25 kilometers), power infrastructure (10 kilometers), and Antofagasta (40 kilometers). The company is targeting a Final Investment Decision (FID) in the second half of 2026, with construction expected to commence in 2026.

Marimaca's capital efficiency positions it among the most competitive new developments globally. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, quantifies the advantage:

"We are in the bottom decile of capital intensity for new development stage copper projects globally… We're sub $12,000 a ton of copper equivalent production which is a very nice place to be."

Permitting Paralysis & Jurisdictional Risk

Average permitting times now span 3–5 years in major jurisdictions, slowing project delivery. This complexity is driving a major geographic reallocation of capital toward South American opportunities, introducing new jurisdictional risks regarding social license and political stability.

Gladiator Metals benefits from its proximity to Whitehorse, eliminating the need for fly-in/fly-out camps. The company has already secured a Capacity Funding Agreement with the Kwanlin Dün First Nation, demonstrating early social license establishment in Yukon, Canada, a Tier-1 jurisdiction offering existing infrastructure and transparent regulatory frameworks.

Structural deficits reward capital efficiency and regulatory predictability. Investors should favor high-grade exploration and low-capex development in jurisdictions with transparent permitting systems.

Demand Is Accelerating: Electrification & AI Redefine Copper's Role

Copper's supply challenges are colliding with an unprecedented demand surge driven by the energy transition and AI revolution.

Electrification Multiplier Effect

Every electric vehicle uses four times more copper than a combustion car, 85–95 kilograms per electric vehicle (EV) compared to 20–25 kilograms for internal combustion vehicles. The global EV rollout, projected to exceed 60 million units annually by 2030, could add several million tons of incremental demand.

Renewable & Grid Infrastructure

Renewable power systems are copper-intensive: 3,000–5,000 tons per gigawatt (GW) for solar and up to 9,500 tons per gigawatt for offshore wind. Projects like Marimaca Copper's heap leach operation illustrate how the next generation of producers is aligning with green infrastructure economics. Heap leaching reduces carbon intensity by approximately 38% compared to conventional flotation, a critical environmental, social, and governance (ESG) differentiator.

Marimaca is also pursuing a hub-and-spoke district integration strategy, with exploration at Pampa Medina targeting sediment-hosted copper sulphides, a style potentially unique to Chile that could extend mine life significantly. The company's development timeline aligns with the tightening supply-demand balance. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, outlines the strategy:

"We're talking about a multi-prong strategy. We're very focused still on the mod being pushed forward, permitting and debt finance by the end of the year."

AI & Data Centers as Emerging Demand Drivers

AI data centers add a new, high-volume use case. Each hyperscale facility requires extensive copper for power distribution and thermal systems. Multi-metal explorers like Fitzroy Minerals, with exposure to copper, molybdenum, and rhenium, are capturing early positioning in metals critical to both clean energy and advanced computing applications.

Fitzroy's Caballos project represents a new copper-molybdenum-gold-rhenium mineralizing system, with Chile supplying 50–60% of the global rhenium market. The company's Buen Retiro IOCG copper deposit has yielded high-grade intercepts of 110 meters at 1.94% copper, with ongoing Phase 2 drilling exceeding 8,000 meters targeting shallow, leachable oxides that facilitate low-capex heap leach development.

Strategic metals exposure provides additional upside optionality beyond copper. Gilberto Schubert, Chief Operating Officer and Country Manager of Fitzroy Minerals, highlights the multi-commodity value proposition:

"Together with molybdenum, we have rhenium which is a very important element. Chile is the second largest rhenium producer in the world. It's a very important material for the military and aerospace industry.

Demand is no longer cyclical, it is structural and policy-driven. Projects aligned with green supply chains and technological adoption cycles will benefit from both premium pricing and capital inflows.

Repricing the Copper Cost Curve

The structural deficit reshapes how investors value copper equities. Operating efficiency and capital discipline matter more than scale.

Rising Incentive Prices

The cost of bringing new production online implies incentive prices rising toward $4.50–5.00 per pound, compared to approximately $3.00 per pound in the last cycle. Developers capable of economic returns below this range gain strategic advantage in an environment where funding is increasingly selective.

Margin Preservation Over Volume Growth

Producers are prioritizing EBITDA margin stability. Fitzroy Minerals' strategy centers on identifying opportunities with low capital intensity potential and short timelines to production. The company benefits from a unique risk mitigation feature: a Pucobre S.A. 30% Clawback Right on the Buen Retiro option, which, if exercised, provides a cash payment equal to three times invested capital to date.

The Exploration Premium

With fewer than 10 significant copper discoveries in the past decade, the global copper pipeline faces a critical shortage of development-ready projects. The exploration success rate has declined as easily accessible deposits are exhausted, creating a discovery premium for high-grade finds in stable jurisdictions. This scarcity of new supply sources intensifies the structural deficit outlook and elevates the strategic value of exploration success.

The dearth of significant new discoveries over the past decade has created a fundamental imbalance between the rate of mine depletion and the rate of reserve replacement. Major producers are increasingly forced to extend mine life at existing operations rather than develop greenfield projects, underscoring how geological scarcity is reshaping industry economics and elevating the strategic importance of exploration-stage companies with credible discovery potential in Tier-1 jurisdictions.

The Investment Thesis for Copper

- The 2026 structural deficit confirms copper's shift from cyclical metal to scarcity asset, creating a multi-year investment opportunity defined by supply constraints rather than demand volatility.

- Grade decline and cost inflation ensure a durable pricing floor near incentive levels, rewarding developers capable of economic returns at $4.50–5.00 per pound copper.

- Capital-efficient projects like Marimaca demonstrate how low capex and permitting readiness can command institutional attention, particularly when combined with low-carbon production methods aligned with ESG capital flows.

- High-grade discoveries in Tier-1 jurisdictions, such as Gladiator's Yukon belt, offer discovery-driven leverage in a market starved for new, high-quality tonnes, with valuation premiums expanding as resource confidence grows.

- Explorers with multi-metal exposure, such as Fitzroy, provide optionality across strategic material markets, capturing demand from both electrification and emerging technology applications like AI infrastructure.

- Jurisdictions offering regulatory stability and permitting transparency are attracting capital reallocation, with Canada and Chile emerging as preferred destinations for copper investment.

- Development timelines aligned with multi-year demand growth trends position advanced-stage projects to deliver new supply precisely when the market enters sustained deficit, maximizing pricing capture.

- Operational strategies adapted for inflationary environments favor projects with access to existing infrastructure, grid power, and established community relations, minimizing execution risk.

- The copper market now rewards patience, selectivity, and quality over quantity, aligning portfolio exposure with scarcity economics rather than short-term price momentum.

The Repricing Era Has Begun

The copper industry's challenge is structural: grades are falling, capital costs are rising, and regulatory hurdles are expanding. The ICSG's projected 150,000-ton deficit is not an anomaly, it is a preview of what sustained underinvestment looks like when it collides with geological exhaustion and accelerating demand from electrification and AI infrastructure. As the global economy electrifies and digitizes, copper's role as the backbone metal of progress becomes irreplaceable. Companies that combine discipline, grade, and jurisdictional strength will define the winners of the next copper cycle.

TL;DR

The copper market is undergoing a fundamental shift from surplus to structural deficit. The ICSG now projects a 150,000-ton deficit by 2026, driven not by demand volatility but by the mining industry's inability to deliver new supply. Global ore grades have plummeted from 1-2% to below 0.7%, while capital intensity has doubled to $15,000-20,000 per tonne of production capacity. Permitting delays averaging 3-5 years compound the challenge. Meanwhile, electrification, renewable energy, and AI infrastructure are creating unprecedented demand layers. For investors, this marks a repricing era where capital-efficient projects, high-grade discoveries in stable jurisdictions, and disciplined developers will outperform. The investment thesis has shifted from cyclical exposure to structural positioning in a scarcity-driven asset class.

FAQs (AI-Generated)

The deficit stems from three converging factors: declining ore grades (from 1-2% historically to below 0.7%), rising capital costs (doubled to $15,000-20,000 per tonne of capacity), and permitting delays (3-5 years average). Production growth is slowing to just 0.9% in 2026 while demand from electrification and AI infrastructure accelerates, creating a supply-demand imbalance.

An electric vehicle requires 85-95 kilograms of copper, approximately four times more than a conventional internal combustion vehicle which uses 20-25 kilograms. With global EV production projected to exceed 60 million units annually by 2030, this electrification multiplier represents several million tons of incremental copper demand.

Investors prioritize capital efficiency (below $12,000 per tonne of production capacity), high ore grades (above 1% copper), jurisdictional stability (Tier-1 locations like Canada and Chile), low all-in sustaining costs (second quartile or better), and clear permitting pathways. Projects combining these factors are positioned for re-rating as the market reprices structural scarcity.

Three sectors are creating structural demand growth: electrification (EVs, charging infrastructure, grid modernization), renewable energy (solar requires 3,000-5,000 tons per gigawatt, offshore wind up to 9,500 tons per gigawatt), and AI data centers (hyperscale facilities require tens of thousands of tons for power distribution and cooling systems over their lifespan).

Incentive prices represent the copper price level needed to justify developing new mines and bringing production online. These are rising toward $4.50-5.00 per pound (from approximately $3.00 per pound previously) due to doubled capital intensity, lower ore grades requiring more processing, and extended permitting timelines that increase project risk and financing costs.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed