Gold Miners: The Ultimate Leverage Play for 2025

Gold's structural bull market driven by central bank diversification, constrained supply, and institutional demand creates compelling opportunities in quality mining companies.

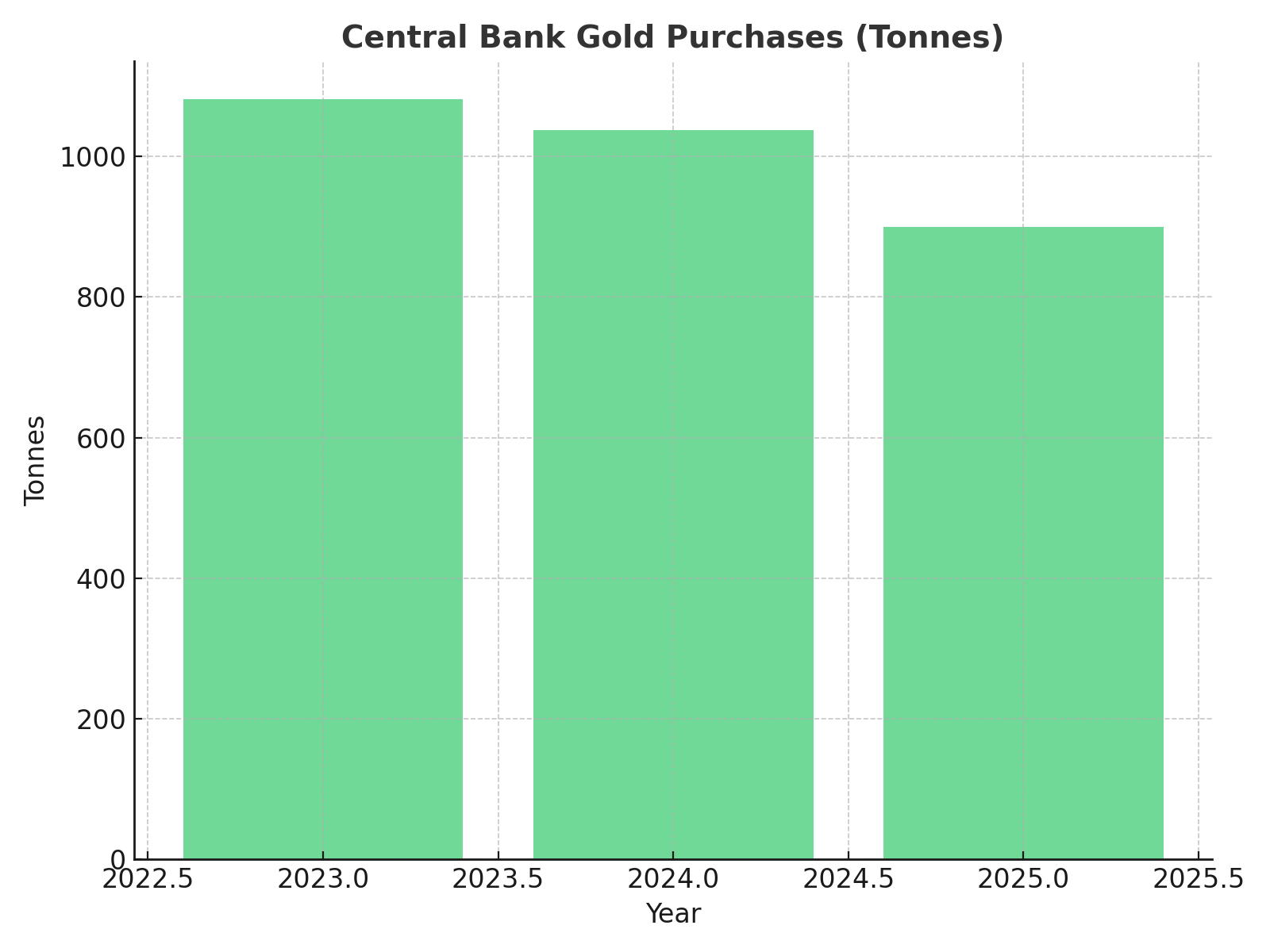

- Central bank gold purchases are projected to reach 900 tonnes in 2025), maintaining the structural diversification away from USD reserves that has driven sustained institutional buying across emerging markets

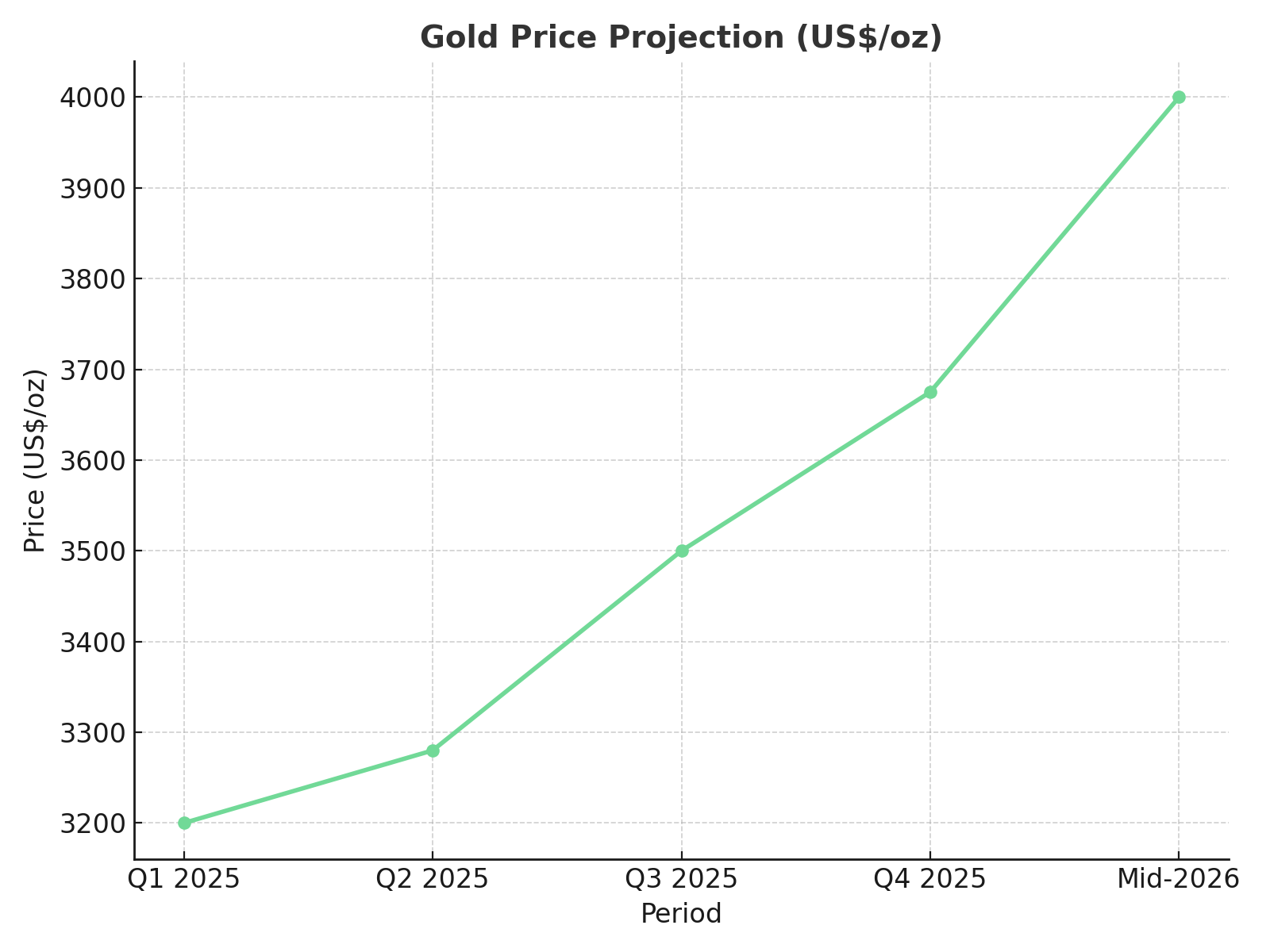

- Gold prices are expected to average $3,675/oz by Q4 2025 and climb toward $4,000 by mid-2026 (J.P. Morgan Research), with gold increasing by more than 28% year-to-date in US dollars and reaching 40 new record highs

- Global gold mine production reached 909 tonnes in Q2 2025 (World Gold Council), contributing to a 3% year‑on‑year increase in total supply, while total Q1 gold demand was 1% higher y/y at 1,206t – the highest for a first quarter since 2016

- Two consecutive quarters generated the strongest first half for bar and coin investment since 2013, while US-listed ETFs added 203t across H1 2025, bringing total holdings to 1,785t (World Gold Council tracking)

- Average quarterly gold price reached a record US$3,280.35/oz, up by 40% y/y and 15% q/q, creating significant operational leverage for well-positioned producers as all-in sustaining costs rise modestly compared to revenue gains

Why Invest in Gold: The Case for Precious Metals in 2025

Gold has increased by more than 28% year-to-date in US dollars, trading 22% higher on average this year than during 2023, reasserting its role as the ultimate safe-haven asset. Gold reached 40 new record highs year-to-date and total gold demand in the third quarter surpassed US$100 billion for the first time, demonstrating its enduring appeal to both institutional and retail investors.

The current investment landscape presents a compelling case for gold exposure through both physical holdings and equity investments in leading mining companies. As central banks accelerate their diversification and investors seek inflation hedges amid policy uncertainty, gold stands positioned for continued outperformance.

Global Trends: The Structural Shift Toward Gold

The most significant structural driver supporting gold prices is unprecedented central bank purchasing. This represents a fundamental shift in reserve management strategies based on documented central bank purchases.

Diversification away from U.S. dollar reserve holdings, while still moderate, has been accelerating in recent years, according to the latest Currency Composition of Official Foreign Exchange Reserves data from the International Monetary Fund. The strategic implications are profound, nearly 36,200 tonnes and account for almost 20% of official reserves, up from around 15% at the end of 2023 (IMF COFER data).

Key emerging market central banks continue to lead this trend with documented purchases. The People's Bank of China reported adding 13 tonnes to its gold reserves in Q1 2025, with reported gold reserves climbing to 2,292 tonnes by the end of the quarter, nudging gold's share of total reserves to 6.5%. The National Bank of Kazakhstan added 6 tonnes during the quarter, lifting its official gold reserves to 291 tonnes, while the Czech National Bank's gold reserves rose by 5 tonnes in Q1, lifting gold holdings to 56 tonnes by the end of Q1 (respective central bank disclosures).

Investment Demand Surges

Professional money managers and institutional investors have returned to gold in force. A sharp revival in gold ETF inflows fuelled a more-than-doubling of total investment demand to 552 tonnes (+170% y/y), reaching its highest level since Q1 2022 (World Gold Council demand statistics). This represents renewed confidence in gold's role as a portfolio hedge.

The retail investment story is equally compelling. Bar and coin demand remained elevated at 325 tonnes – 15% above the five-year quarterly average of 283 tonnes. China drove much of this increase, posting its second-highest quarter of retail investment on record (World Gold Council retail investment tracking).

Supply Challenges: The Mining Industry Under Pressure & Production Growth Lags Demand

While demand has surged, supply growth remains constrained. For 2025, forecasted global gold mine production is expected to climb 1% to approximately 3,694 tonnes, buoyed by new mining projects in Mexico, Canada and Ghana (World Gold Council production forecasts). This modest increase pales in comparison to robust demand fundamentals.

The mining industry faces significant structural challenges that limit rapid supply responses to higher prices. The World Gold Council reports that the gold mining industry is suffering from a scarcity of economic gold deposits globally, with discovery rates declining and average ore grades falling at existing operations.

Leading Gold Companies in Production

Among top-tier producers, one company stands out for its operational excellence based on reported production and cost metrics.

Perseus Mining demonstrates exceptional operational performance. The company delivered group production of 496,551 ounces gold at AISC of US$1,235/oz, generating revenue of US$1.25 billion and EBITDA of US$740 million in FY2025 (Perseus Mining annual results).

As Managing Director and Chief Executive Officer Jeff Quartermaine explains:

"By having a number of assets located in different geopolitical settings, means that consistently over time we are producing on target the consistency such that investors can rely on what is coming down the turnpike."

Company Case Studies: Excellence in Execution & High-Growth Developers: i-80 Gold Corp

i-80 Gold Corp represents the emerging generation of Nevada-focused gold developers. The company's strategy targets production of approximately 600,000 ounces annually by the early 2030s, supported by a robust portfolio of five core Nevada assets including Granite Creek, Cove, Ruby Hill, and Lone Tree processing facility (company development timeline).

Recent developments highlight the company's momentum. High-grade assays from the South Pacific Zone delivered exceptional results, including 33.6 g/t Au over 2.9 meters and 29.7 g/t Au over 3.6 meters in November 2025 drilling programs (company drill results).

Tyler Hill, VP Geology at i-80 Gold, notes:

"At Granite Creek Underground, the first six holes from our infill drill program continue to show robust high-grade mineralization throughout the South Pacific Zone and suggest that the deposit has the potential to expand to the north and at depth."

The company's Granite Creek Underground Preliminary Economic Assessment demonstrates strong economics with an 8-year mine life averaging 60,000 ounces per year at AISC $1,597/oz (NI 43-101 PEA). After-tax NPV of $155 million at base case gold pricing of $1,800/oz expands to $344 million at current spot prices, illustrating the leverage inherent in well-positioned developers.

Established Producers: Integra Resources

Integra Resources exemplifies successful operational execution. The company operates the Florida Canyon Mine while advancing the DeLamar Project through development stages, with a combined resource base of 7.0 million ounces AuEq Measured & Indicated plus 3.1 million ounces AuEq Inferred across all projects (NI 43-101 resource estimates).

A significant milestone was achieved in September 2025 when the Bureau of Land Management accepted Integra's Mine Plan of Operations for the DeLamar Project. This is the first major federal permitting milestone and initiates the formal NEPA Environmental Impact Statement review process.

Dale Kerner, VP Permitting at Integra Resources, provides insight into the process:

"Mining projects are very complex. Of course, we have the NEPA process with the federal agency, the Bureau of Land Management. At Stibnite, the NEPA process took about eight years. With the BLM, we anticipate that the process is going to be much shorter. But it's still a considerable amount of analysis of the project. We anticipate a NEPA process that's a bit shorter, but it still is robust and we need to provide good data for that."

The company's 2025 guidance targets 70–75 thousand ounces gold production from Florida Canyon (company guidance), combined with the development pipeline including DeLamar's projected 136,000 ounces AuEq annually over 8 years at AISC US$814/oz (DeLamar Feasibility Study), positioning Integra for substantial growth.

Operational Excellence: West Red Lake Gold Mines

West Red Lake Gold Mines demonstrates successful mine restart execution. The company acquired the distressed Madsen Mine in June 2023 and achieved operational restart in 2025, with bulk sample results of 14,490 tonnes at 5.72 g/t Au producing 2,664 ounces of gold with 95% metallurgical recovery (company operational reports).

Vice President of Communications Gwen Preston articulates the company's ambitious vision:

"We want to chart a path, show that we are heading to become a mid-tier gold miner, a producer of scale so that we can offer our investors this ride by amplifying our production during the gold bull market."

The January 2025 Pre-Feasibility Study shows NPV of C$496 million with AISC of US$1,681/oz and production of 67,600 ounces annually over 6 years (Madsen PFS). The Rowan Project adds near-term growth potential with 35,200 ounces annually for 5 years and IRR of 42% (Rowan PEA).

Emerging Growth: New Found Gold

New Found Gold Corp represents significant discovery potential in Newfoundland & Labrador's tier-1 mining jurisdiction. Recent leadership changes include Dr. Andrew Furey (former Premier) as Independent Director and Hashim Ahmed as CFO, strengthening governance and financial stewardship capabilities.

CEO Keith Boyle emphasizes the systematic approach to company building:

"There are steps that you've to take to go ahead and, you know, build a company, both an operating company, and you've got to have the right team. And so we're pretty pleased with what we've been able to accomplish."

The Queensway Project Preliminary Economic Assessment was completed in July 2025, with project expansion through acquisition agreements increasing total project size by approximately 33% to 234,050 hectares (company filings). Strong financial backing includes Eric Sprott at approximately 23.1% ownership stake.

International Excellence: Serabi Gold

Serabi Gold demonstrates sustainable gold production with organic growth in Brazil's Pará State. The company operates the Palito Complex with over 20 years operating history producing 30–40 thousand ounces annually, while developing the Coringa mine to achieve 60,000 ounces annually by 2026 (company production guidance).

Chief Executive Michael Hodgson outlines the company's operational optimization strategy:

"Our objective initially has been to maximise production from existing facilities. That's a process plant that's capped at about 650 tonnes per day, 230,000 tonnes per year. We're actually getting more out of that plant by high grading. We don't grade the mine, we take the ore out of the mine, we put it through two ore sorters, so we're just upping that feed grade going into that plant and that gets us to 60,000 ounces. What we want to do is build a 100,000 ounce producer plus."

H1 2025 results show EBITDA of US$26.3 million and net profit of US$18.9 million with Q2 2025 AISC of US$1,792/oz (company financial statements). The company maintains strong ESG credentials with 68% of workforce from Pará State, zero tailings dams, and CO₂ intensity of 0.53 tCO₂e/oz.

Brazilian Development: Cabral Gold

Cabral Gold owns 100% of the Cuiú Cuiú district in Brazil's Tapajós Region. The company filed its NI 43-101 Technical Report in September 2025, confirming the gold-in-oxide starter operation Preliminary Feasibility Study with no material differences from previous results (company technical filings).

Country Manager Brazil Ruari McKnight provides valuable perspective on the Brazilian opportunity:

"If it was easy, there wouldn't be any opportunities, right? And we're in a region which has produced in excess of 30 million ounces of gold. In a similar district in Canada or Australia, you'd have 50 or 60 or 70 mines operating in this region. Therein lies the opportunity. The challenges also provide opportunities."

Indicated mineral resources include 450,200 ounces in fresh basement material and 216,182 ounces in oxide material (NI 43-101 resource estimate), positioned in the historic Tapajós Gold Province that produced an estimated 30-50 million ounces between 1978-1995 (geological surveys).

Technical Analysis: Price Trajectory & Targets

The technical picture for gold remains overwhelmingly bullish based on fundamental analysis. J.P. Morgan Research forecasts gold prices to average $3,675/oz by the fourth quarter of 2025 and climb toward $4,000 by mid-2026, driven by continued central bank purchases and supply constraints.

Investment Implications: Positioning for the Gold Super-Cycle

Financial advisors increasingly recommend meaningful gold allocations as portfolio insurance against monetary and geopolitical risks. The traditional allocation may prove insufficient given current macro dynamics, with a diversified approach across physical gold, ETFs, and carefully selected mining equities providing both diversification and upside participation.

Best Gold Mining Companies for Investment

Based on comprehensive analysis of operational metrics, financial strength, and growth prospects:

- Large-Cap Producers: Newmont and Agnico Eagle offer established operations with predictable cash flows. Perseus Mining provides exceptional margins and cash generation in international markets.

- Mid-Cap Growth: Companies like Integra Resources and Serabi Gold combine operational cash flow with meaningful growth projects, offering higher leverage to gold prices while maintaining operational stability.

- Development-Stage Leverage: i-80 Gold, New Found Gold, West Red Lake Gold, and Cabral Gold provide maximum leverage to rising gold prices through development of high-grade deposits. While riskier, these companies offer potential for substantial returns as projects advance.

ESG & Sustainability: The New Mining Paradigm

Leading gold companies increasingly prioritize environmental, social, and governance factors. Serabi Gold's sustainability initiatives demonstrate industry best practices: 68% of workforce from local regions, zero tailings dams, and CO₂ intensity of 0.53 tCO₂e/oz. Integra Resources signed a Relationship Agreement with the Shoshone-Paiute Tribes in August 2025, aligning cultural and environmental stewardship with project development.

These ESG commitments reduce operational risks, enhance community relations, and secure long-term mining permits while attracting premium valuations and lower-cost capital.

The Investment Thesis for Gold

- Target established producers like Newmont and Agnico Eagle during market corrections, focusing on companies with declining all-in sustaining costs and strong operational track records

- Allocate exposure to mid-tier producers like Perseus Mining and Integra Resources that offer production growth while maintaining strong balance sheets and permitting momentum

- Evaluate high-conviction development stories like i-80 Gold and New Found Gold that offer significant leverage to metal price appreciation through high-grade project advancement

- Maintain exposure balance between Tier-1 jurisdictions (North America, Australia) and higher-growth emerging markets, particularly proven mining districts

- Prioritize companies with strong environmental records and community relations, as demonstrated by Serabi Gold and Integra Resources, as these factors determine permitting success

- Scale into positions ahead of key catalysts like feasibility studies (i-80 Gold Q1 2026), permitting approvals (Integra DeLamar EIS), and production ramp-ups

Key Takeaways & Investor Implications

The case for gold investment in 2025 rests on multiple convergent factors: structural central bank demand, constrained supply growth, renewed institutional interest, and technical momentum toward $4,000+ per ounce. The combination creates a compelling multi-year outlook for both the commodity and well-positioned mining companies.

Investors seeking exposure should consider a diversified approach combining physical gold holdings, ETF exposure, and carefully selected mining equities. The latter offers the greatest leverage to rising prices while providing potential dividend income and operational growth.

The current cycle differs from previous gold rallies in its fundamental underpinnings of strategic portfolio repositioning and monetary diversification. For investors willing to endure volatility inherent in mining operations, the current environment presents exceptional opportunities in best-in-class gold companies positioned for the next phase of the super-cycle.

TL;DR Summary

Gold has entered a structural bull market with central banks purchasing 900 tonnes in 2025 (World Gold Council) and investment demand doubling to 552 tonnes. Supply constraints limit production growth to 1% annually while gold reaches record highs above $3,200/oz. Major banks target $4,000-5,000/oz by 2026 based on fundamental analysis. Leading miners like Newmont (3.38M oz H1 production) and Perseus (496k oz annual production) offer exposure with strong margins, while developers like i-80 Gold (600k oz target) and Integra Resources (7M oz resources) provide higher leverage through project advancement. The combination of record prices, expanding margins, and robust fundamentals creates exceptional opportunities. A diversified approach across established producers, growth-stage companies, and geographic regions maximizes risk-adjusted returns in this super-cycle environment driven by monetary diversification and supply scarcity.

FAQs (AI Generated)

Based on the company materials reviewed, top choices include Newmont Corporation (NEM) as the world's largest producer with 3,383 thousand ounces H1 2025 production, Perseus Mining (PRU) for exceptional margins at AISC of US$1,235/oz, i-80 Gold (IAUX) for Nevada development leverage targeting 600,000 oz/year by early 2030s, and Integra Resources (ITR) for permitting advancement with the DeLamar project's 7.0 million ounce AuEq resource base.

The analysis shows central banks are purchasing a projected 900 tonnes in 2025 as part of strategic diversification away from USD reserves. Central bank gold holdings now account for almost 20% of official reserves, up from around 15% at the end of 2023, reflecting concerns about geopolitical risks and currency volatility. Key buyers include the People's Bank of China (adding 13 tonnes in Q1), National Bank of Kazakhstan (6 tonnes), and Czech National Bank (5 tonnes).

According to the research, J.P. Morgan Research forecasts gold averaging $3,675/oz by Q4 2025 and climbing toward $4,000 by mid-2026. Major investment banks including JP Morgan and Goldman Sachs have issued forecasts suggesting gold could reach $4,000 to $5,000 per ounce by 2026, driven by structural demand drivers and constrained mine supply growth projections.

The analysis highlights i-80 Gold with its Nevada portfolio targeting 600,000 oz/year by early 2030s and Granite Creek Underground PEA showing 8-year mine life economics, New Found Gold with its expanded Queensway Project covering 234,050 hectares in Newfoundland & Labrador, West Red Lake Gold with its successful Madsen mine restart showing 67,600 ounces annually over 6 years production potential, and Cabral Gold with 666,382 total ounces in indicated resources in Brazil's Tapajós Gold Province.

The research emphasizes companies like Serabi Gold with 68% local workforce from Pará State, zero tailings dams, and CO₂ intensity of 0.53 tCO₂e/oz, plus Integra Resources' Relationship Agreement with Shoshone-Paiute Tribes signed in August 2025. Strong ESG credentials reduce operational risks, enhance community relations, and secure long-term mining permits while attracting premium valuations and lower-cost capital.

Analyst's Notes

Subscribe to Our Channel

Stay Informed