Higher Oil Prices Extend Restrictive Rate Regime, Suppressing PGM Equities Despite Multi-Year Supply Deficit

Oil shock, high rates, and tariffs suppress PGM prices despite a 500k-700k oz deficit, creating undervalued developer opportunities tied to supply tightening.

- The US naval blockade of Iran and the closure of the Strait of Hormuz, which previously handled approximately 20% of global crude oil transit, has driven Brent crude to $118.03 per barrel and is reinforcing a higher-for-longer rate that can suppresses dollar-denominated PGM prices.

- The Federal Open Market Committee held the federal funds rate at 3.5% to 3.75% with an 8-4 dissent vote, the highest level of FOMC dissent recorded since October 1992, and explicitly cited elevated global energy prices as the inflation driver constraining policy flexibility.

- The 132.83% US preliminary antidumping duty on Russian palladium issued under the Tariff Act of 1930 is restructuring a supply chain in which approximately 80% of global PGE output originates from Southern Africa, with further concentration in Russia.

- A multi-year structural deficit of 500,000 to 700,000 ounces and a 42% drawdown in above-ground stocks are not reflected in PGE developer equity valuations, with the development pipeline limited to two major greenfield projects globally targeting near-term production.

- Re-rating of development-stage PGE equities is contingent on dated technical deliverables including hydrometallurgical scale-up testing, Preliminary Economic Assessment delivery, and Environmental Impact Assessment commencement, with ValOre Metals targeting PEA completion at end of 2026.

Strait Of Hormuz Disruption Is Driving A Second-Order Monetary Transmission

Brent crude futures closed at $118.03 per barrel, a single-session move of approximately 6%, after President Trump stated the US naval blockade against Iran would continue until a nuclear agreement is reached. The Strait of Hormuz previously accounted for approximately 20% of global crude oil transit, with Iran refusing to reopen the strait until the US lifts its naval blockade.

The transmission to monetary policy was made explicit in the FOMC post-meeting statement, which stated that inflation remains elevated in part reflecting the recent increase in global energy prices. The committee voted 8-4 to hold the benchmark federal funds rate in the 3.5% to 3.75% range, the highest level of FOMC dissent recorded since October 1992.

For the platinum group metals, this transmission chain converts a regional oil disruption into a sustained pricing headwind. Higher oil prices extend the restrictive rate regime, which in turn supports a stronger US dollar and elevated real yields, both of which compress dollar-denominated commodity valuations.

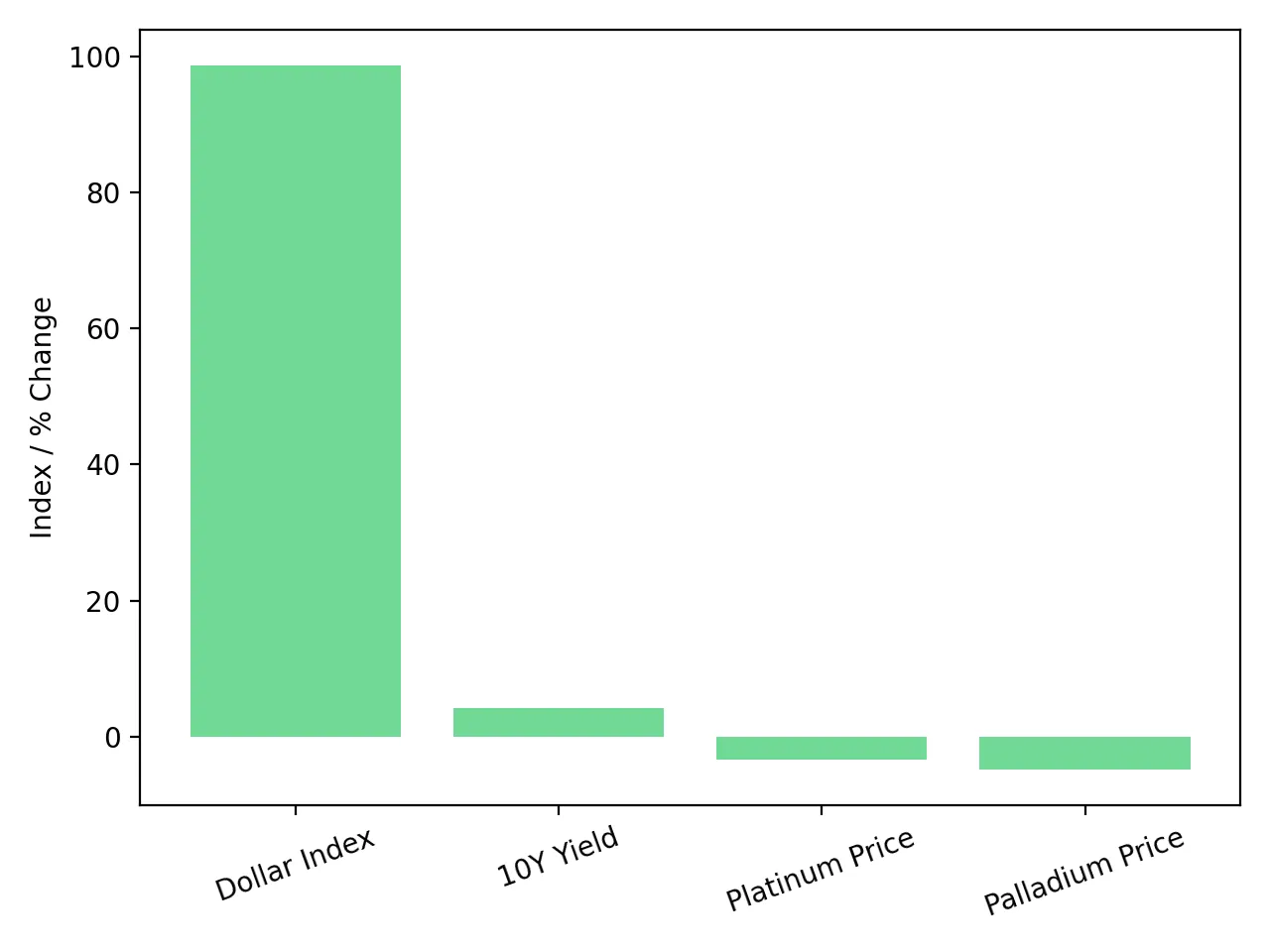

Real Yields & Dollar Strength Are Setting The Floor For PGM Pricing

The US Dollar Index firmed to approximately 98.70, the 10-year US Treasury yield rose to 4.294%, and all four precious metals settled in negative territory, with platinum at $2,021.20 per ounce (down 3.33%) and palladium at $1,494.87 per ounce (down 4.83%) absorbing the steepest percentage losses of the session.

The opportunity cost mechanism rotates capital out of non-yielding commodities into Treasuries offering 4.294% on the 10-year. The currency mechanism reduces purchasing power for non-US autocatalyst manufacturers, who absorb approximately 40% of global platinum demand and approximately 80% of palladium demand. The liquidity mechanism tightens positioning across the precious metals complex as financial conditions remain restrictive.

The result is that the daily moves in platinum and palladium reflect a macro-driven repricing of the precious metals complex, not a deterioration in the physical PGM market. The entry point for long-duration capital is being defined by macro flow while the exit valuation is being set by physical fundamentals, and this disconnect is most acute in development-stage equities where the discount compounds across price-to-net-asset-value, enterprise value per ounce of resource, and forward earnings multiples.

The US Antidumping Duty Is Restructuring The Global Palladium Supply Chain

The US Department of Commerce preliminary antidumping determination of 132.83% on Russian palladium imports, issued under the Tariff Act of 1930 (19 U.S.C. § 1673), is one of the most consequential supply-side interventions in recent PGM market history. The underlying petition was filed in July 2025 by Sibanye-Stillwater and the United Steelworkers Union, citing a 35% increase in Russian palladium import volumes (from 20.4 million grams in 2022 to 27.6 million grams in 2024) against a concurrent 50% price decline. The Commerce Department final determination is targeted for April 2026 and the International Trade Commission injury assessment is targeted for June 2026.

Sibanye-Stillwater's Stillwater mine in Montana saw production fall approximately 50% to 300,000 ounces annually from a pre-dumping capacity of approximately 600,000 ounces, with restoration to that capacity requiring two to three years, according to the World Platinum Investment Council projection. The palladium price of $1,646.50 per ounce documented in that report reflected a 63% year-over-year recovery, indicating that procurement repositioning by downstream consumers began before the preliminary determination was issued.

Approximately 80% of global PGE supply originates from Southern Africa with further concentration in Russia, and South African electricity costs have risen approximately 60% over five years against deep-level underground operations dependent on diesel logistics.

Nick Smart, Chief Executive Officer of ValOre Metals, identifies the linkage between the Strait of Hormuz disruption and South African mining costs:

“South Africa is highly reliant on diesel imports, about 60% of its diesel comes through the Strait of Hormuz.”

The Multi-Year PGM Supply Deficit Is Not Being Resolved By The Price Cycle

The platinum and palladium market entered the current cycle carrying a multi-year structural deficit of 500,000 to 700,000 ounces, with above-ground stocks drawn down 42% to less than five months of coverage. Primary platinum mine production declined from a peak of more than 6 million ounces in 2021 to a forecast of approximately 5.5 million ounces in 2026. The autocatalyst demand base is approximately 40% of platinum and 80% of palladium and rhodium consumption, with hybrid vehicles carrying 10% to 20% higher PGE loadings than internal combustion engines.

Platinum surged past an all-time high of $2,700 per ounce before closing around $2,000 per ounce in late April 2026, a gain exceeding 160% over the prior year, while physical investment demand has added a discrete vector with platinum bar and coin demand in China growing from near zero in 2019 to more than 400,000 ounces in 2025. Switching just 1% of current global gold jewellery demand to platinum would double the annual platinum deficit per the same analysis.

Downside is bounded by the marginal cost curve of South African production, where rising electricity and diesel input costs raise the floor. Upside is leveraged to any combination of macro normalisation, supply disruption, autocatalyst demand surprise, or jewellery substitution, none of which is currently priced into the development-stage equity universe.

PGE Developer Equities Are Decoupled From The Commodity Cycle, Pending Technical Validation

Only two major greenfield PGE mines globally are currently targeting near-term production. The barriers are structural rather than sentimental: metallurgical complexity in oxidised near-surface deposits, where traditional sulfide flotation does not deliver comparable recovery rates; capital intensity and multi-year permitting timelines; limited analyst coverage relative to gold and copper; and jurisdictional concentration in Southern Africa.

ValOre Metals' Pedra Branca project in northeastern Brazil hosts 2.198 million inferred ounces of 2PGE+Au at 1.08 g/t across 63.6 million tonnes, against which the company carries a market capitalization of approximately C$26 million. Stillwater Critical Minerals trades at roughly C$126 million on 3.3 million inferred ounces of palladium and platinum at its Stillwater West project in Montana. Generation Mining sits at approximately C$236 million on 3.4 million ounces of palladium and platinum in proven and probable reserves at Marathon, Ontario. Bravo Mining commands roughly C$440 million on 10.4 million ounces of palladium-equivalent measured and indicated, plus 5 million ounces inferred, at Luanga in Brazil's Carajás Mineral Province. Platinum Group Metals holds approximately C$389 million in market capitalization against 23.4 million four-element ounces of proven and probable reserves at Waterberg, South Africa.

Metallurgical Validation & PEA Delivery Define The Re-Rating Catalyst Sequence

ValOre Metals’ Phase II metallurgical testwork conducted by the University of Cape Town's Centre for Minerals Research achieved bioleaching recoveries of 72.88% platinum and 74.07% palladium from weathered Esbarro deposit material over a 22-day leaching period, replicating prior 60-day results with improved kinetics. Caustic cracking pre-treatment applied to chromitite material returned recoveries of 66.42% platinum and 78.81% palladium, targeting high-grade mineralisation grading 6.4 to 8.5 g/t 2PGE+Au, which represents approximately 5% of the total inferred resource. Weathered material accounts for roughly 30% of the total inferred PGE ounces.

ValOre is targeting stirred-tank reactor testing for completion in Q3 2026, column tests for heap leach simulation in Q4 2026, and process economics evaluation in Q4 2026, supporting a Preliminary Economic Assessment targeted for completion at end of 2026 with Lycopodium Ltd as lead process engineering consultant. The corporate identity question runs in parallel: the disposition of the Hatchet Uranium Corp interest to Future Fuels Inc carries an outside date of 30 April 2026, after which ValOre's interest in HUC reduces from 51% to 38% on debenture conversion at closing, completing the transition to a pure-play precious metals company.

Risk Factors That Could Falsify The PGM Re-Rating Thesis

A diplomatic resolution reopening the Strait of Hormuz would ease crude oil prices, lower inflation expectations, and restore Federal Reserve flexibility on rate cuts, removing the macro tailwind for the PGM accumulation case. A US trade ruling that modifies or eliminates the 132.83% duty on Russian palladium would re-supply the domestic market and compress the geographic premium currently embedded in supply chains. Faster-than-expected battery electric vehicle adoption would shorten the autocatalyst demand runway, particularly if hybrid vehicle market share declines.

Failure modes include metallurgical underperformance at industrial scale relative to bench-scale recoveries above 70%, capital cost overruns relative to PEA assumptions targeted for end of 2026, and permitting delays beyond targeted Environmental Impact Assessment commencement.

The Investment Thesis For Platinum Group Metals

- Energy-driven inflation linked to the Strait of Hormuz disruption is extending the higher-for-longer rate regime, with the FOMC holding the federal funds rate at 3.5% to 3.75%.

- The 132.83% US preliminary antidumping duty on Russian palladium is restructuring global palladium trade flows and creating a durable strategic premium for supply located outside the South Africa and Russia concentration that accounts for approximately 80% of global PGE production.

- A multi-year structural deficit of 500,000 to 700,000 ounces and a 42% drawdown in above-ground stocks are not reflected in development-stage equity valuations, creating asymmetric exposure for long-duration capital aligned with supply scarcity.

- Jurisdictional diversification away from the dominant South African and Russian supply base is functioning as a measurable valuation factor, with Brazil offering paved-highway access to deep-water port logistics in Ceará, established mining engineering services capacity, and no direct exposure to the energy supply chain risks tied to Strait of Hormuz disruptions.

- Jurisdictional diversification away from the dominant South African and Russian supply base is functioning as a measurable valuation factor, with Brazil offering paved-highway access to deep-water port logistics in Ceará, established mining engineering services capacity, and no direct exposure to the energy supply chain risks tied to Strait of Hormuz disruptions.

- Macro-driven sell-offs in the precious metals complex, including recent declines in platinum and palladium prices, are creating accumulation opportunities in PGE developers and producers positioned at the lower end of the projected cost curve with credible near- to medium-term catalyst sequences.

Federal Reserve rate policy, and commodity pricing through to developer equity valuations. In the short term, this chain is suppressing PGM prices through elevated Treasury yields and a strong US dollar, alongside continued policy constraint reflected in recent FOMC voting dynamics. In the medium term, the same chain is tightening physical supply through the 132.83% US antidumping duty on Russian palladium and the rising input cost base of South African production, where electricity costs have increased materially in recent years and a significant portion of diesel supply transits the Strait of Hormuz. The 500,000 to 700,000 ounce annual deficit and 42% above-ground stock drawdown documented in industry data confirm the structural tightness; the macro environment determines when that tightness will be reflected in price. That inflection will be driven by either a reversal in the rate cycle, a discrete supply disruption, or successful delivery of development-stage milestones from assets at the lower end of the cost curve.

TL;DR

A Strait of Hormuz-driven oil spike is reinforcing a higher-for-longer rate environment, strengthening the dollar and real yields, key forces suppressing platinum group metal (PGM) prices despite a clear structural deficit of 500,000 to 700,000 ounces and shrinking inventories. At the same time, U.S. tariffs on Russian palladium and rising South African input costs are tightening supply, creating a disconnect where physical fundamentals remain strong but developer equities stay undervalued. This gap presents a potential entry point, with re-rating dependent on macro normalization or project-level milestones.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed