Germany's 2045 Hydrogen Mandate Is Adding Demand to a Platinum Market Already Running a 350,000-Ounce Annual Deficit

Germany's 2045 hydrogen law drives platinum demand. Market runs 350koz deficit with 90% of supply in South Africa, less than 5 months coverage left.

- Hydrogen infrastructure developement is creating a new demand channel for PGMs, particularly platinum, in proton exchange membrane electrolyzers and fuel cells.

- Structural platinum and palladium supply deficits estimated at 500,000 to 700,000 ounces annually, combined with a 42% drawdown in above-ground stocks per World Platinum Investment Council data, are tightening PGM markets with less than five months of coverage remaining.

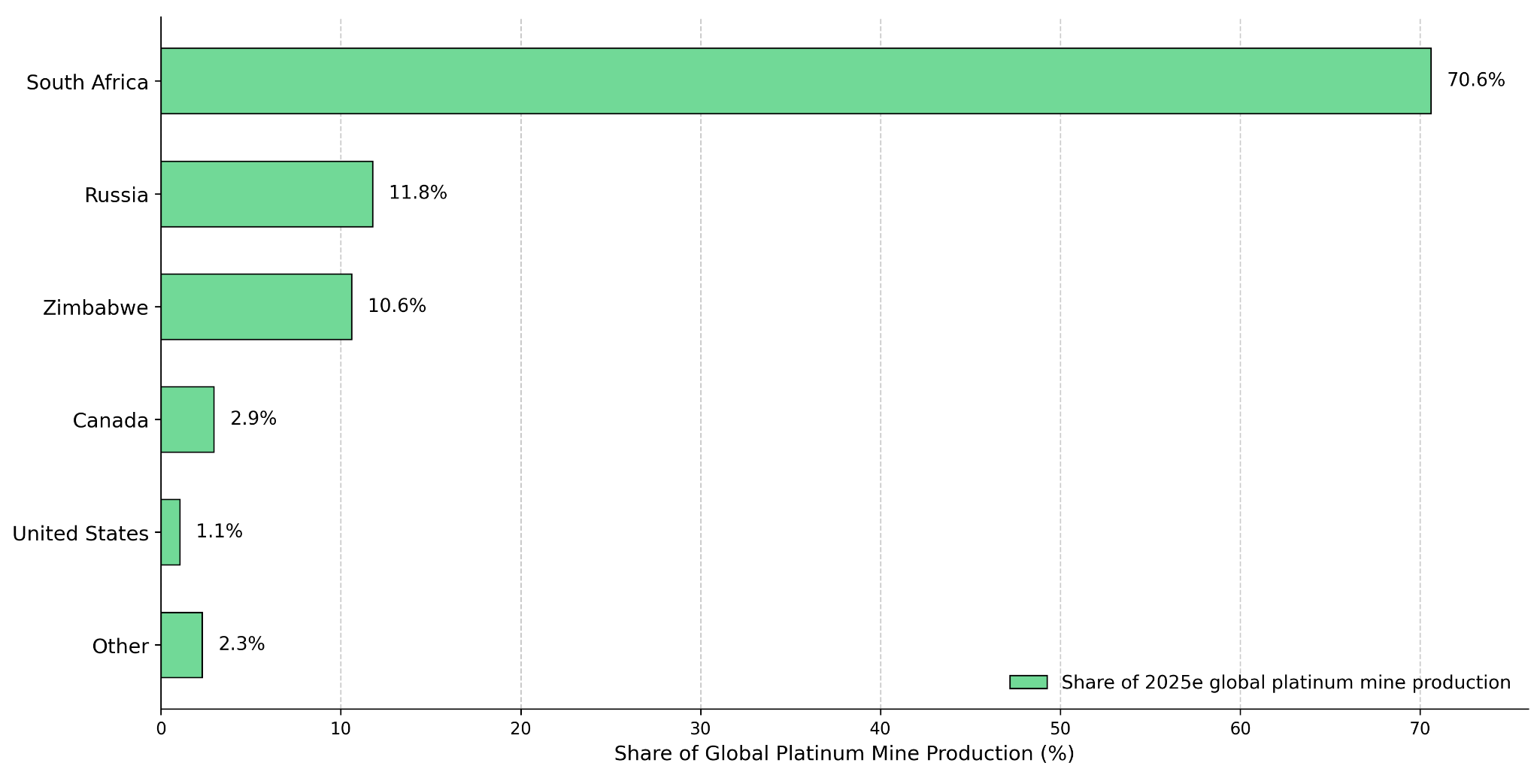

- Supply concentration risk is extreme, with approximately 90% of global PGM reserves located in South Africa and approximately 80% of global PGM production sourced from South Africa and Zimbabwe combined, limiting supply responsiveness to demand shocks.

- Policy-driven demand is becoming legally embedded, with Germany's Hydrogen Acceleration Act, approved by the Deutscher Bundestag, designating hydrogen production, import, storage, and transport as matters of overriding public interest through 2045, and China deploying capital across more than 510 hydrogen projects globally.

- Early-stage developers offer leveraged exposure to structural deficits, though investors must balance this against financing risk, permitting timelines, and metallurgical uncertainty.

Hydrogen Moves from Concept to Industrial System

The European Hydrogen Bank's third auction drew 58 bids requesting €8.4 billion against a €1.3 billion budget, and China has played a key role in operationalizing $110 billion across 510 global hydrogen projects, with fuel cell technology driving incremental platinum demand against a market running an annual deficit of approximately 350,000 ounces, a supply gap arising outside the automotive cycle that currently absorbs approximately 40% of total platinum offtake.

At the technical core of this transition is proton exchange membrane technology, used in both electrolyzers to produce hydrogen from water and in fuel cells to convert hydrogen back into electricity. Both applications require platinum as a catalyst due to its electrochemical stability under acidic, high-temperature operating conditions. Each hydrogen fuel cell truck currently in commercial operation requires approximately 100 grams of platinum, according to Fuel Cells Works, reporting on deployed Toyota fuel cell trucks in China.

A 1,150-kilometer hydrogen trucking corridor between China and Vietnam, which has completed nearly 7,000 runs, according to Fuel Cells Works (April 17, 2026), demonstrates that hydrogen is displacing fossil fuels in freight logistics where battery weight and range constraints make electrification commercially unviable. Fuel cell demand tied to contracted corridors and mandated green steel projects compounds a platinum deficit of approximately 350,000 ounces annually, a supply gap that exists independently of automotive production volumes.

Supply Constraints Meet Expanding Demand: The Emergence of Multi-Year Deficits

The demand described above is occurring against a supply backdrop with limited capacity to respond as annual platinum and palladium supply deficits at 500,000 to 700,000 ounces, with above-ground inventories declining by 42% and available coverage falling to less than five months. This drawdown, if sustained, eliminates the buffer that has dampened price volatility during demand surges.

Platinum-group metal supply is highly concentrated geographically, with South Africa dominant in both reserves and mine production, and South Africa and Zimbabwe together accounting for approximately 80% of global platinum output. This concentration limits supply elasticity and increases sensitivity to operational or regulatory disruption within a single region.

Automotive applications account for approximately 35-45% of total platinum consumption, while representing around 80% of combined palladium and rhodium demand. Hybrid vehicles require 10-20% more PGMs per unit than internal combustion engine vehicles, reinforcing rather than reducing automotive-sector consumption as battery electric vehicle adoption progresses more gradually than earlier projections indicated.

Policy Lock-In & Geopolitical Incentives: Hydrogen as Strategic Infrastructure

Hydrogen infrastructure has moved from voluntary climate commitment to legislative mandate. Germany's Hydrogen Acceleration Act, approved by the Deutscher Bundestag, designates hydrogen production, import, storage, and transport as matters of overriding public interest through 2045, providing regulatory priority for project approvals across the full hydrogen value chain. The third European Hydrogen Bank auction drew €8.4 billion in funding requests against a €1.3 billion allocation, confirming that private-sector demand for hydrogen project financing is substantially outpacing available public capital.

This legislative structure reduces the policy reversal risk that has historically discounted clean energy commodity investments. When a government embeds a commodity application into its national infrastructure framework for multiple decades, the resulting demand signal approaches the durability of utility-grade materials that are non-discretionary at the system level.

China's policy approach operates through coordinated industrial deployment. China has deployed capital across more than 510 hydrogen projects now entering construction or operation globally. Hydrogen Fuel News reports that China's Five-Year Plan to 2030 targets domestic hydrogen production costs of approximately €3 per kilogram, with strategic priorities covering heavy transport, industrial decarbonization, and export competitiveness in hydrogen-derived fuels, creating a demand base not solely reliant on European policy continuity.

Industrial Recovery as a Demand Multiplier for PGMs

PGMs retain their character as industrial metals, and current manufacturing data supports near-term baseline demand. The US ISM Manufacturing PMI reached 52.7 in March 2026, its strongest expansion reading since August 2022. China's NBS Manufacturing PMI registered 50.4 and the S&P Global China Manufacturing PMI reached 50.8, both released April 1, 2026, indicating a return to expansion.

These readings translate directly into improved output across automotive manufacturing, chemical processing, and electronics, each a primary PGM consumer at scale. A simultaneous cyclical upturn and structural demand expansion, occurring against constrained supply, creates conditions for sustained price appreciation rather than a short-cycle commodity bounce.

Scarcity Value in Emerging PGM Projects

The macro environment favors assets capable of delivering new PGM supply outside southern Africa's dominant supply base.

ValOre Metals' Pedra Branca Project in northeast Brazil is one of the few development-stage PGM assets outside southern Africa at a scale relevant to institutional screening. The project hosts a 2.2 million ounce inferred resource grading 1.08 grams per tonne across platinum, palladium, and gold. Nick Smart describes the mining method:

"Our mineralization goes right up to surface, the mining method we're looking at is open-cast mining."

Open-cast mining lower costs significantly versus underground extraction. Metallurgical advancement is progressing through testwork conducted with the University of Cape Town. Nick Smart outlines the initial extraction results:

"Indicating that with a leaching route combined with a pre-treatment step, we're getting extractions in the 70% range for palladium and platinum, 73% and 74% respectively. What we're looking at developing with UCT in this flowsheet is a low-cost processing route, with the primary focus being on whether we can do this heap leaching."

A near-surface open-cast project with confirmed metallurgical recoveries in a platinum market running a structural supply deficit carries a different risk profile than a deep underground development, lower capital requirement at entry, faster potential path to production, and direct leverage to platinum price movement.

ValOre's Pedra Branca holds 2.2 million ounces of platinum-group metals that can be mined from the surface rather than underground, lowering costs significantly. Early lab results show 73–74% metal recovery using a potentially low-cost heap leach process.

Development Timelines, Capital Intensity & Execution Risk

PGM projects typically require five to ten years from discovery to first production, encompassing multiple permitting stages and capital raises at each milestone. Metallurgical complexity and limited processing infrastructure outside South Africa extend these timelines further for PGM-specific assets.

The Investment Thesis for Platinum Group Metals

- Hydrogen economy scaling creates a new, policy-backed demand channel for platinum in PEM electrolyzers and fuel cells, with each commercially deployed fuel cell truck requiring approximately 100 grams of platinum, translating infrastructure buildout directly into measurable metal demand.

- Annual platinum and palladium supply deficits of 500,000 to 700,000 ounces and an above-ground inventory drawdown of 42% per World Platinum Investment Council data reduce market coverage to less than five months, establishing conditions for sustained price repricing rather than a short-cycle correction.

- Germany's Hydrogen Acceleration Act, approved by the Deutscher Bundestag, designates hydrogen production, import, storage, and transport as matters of overriding public interest through 2045, providing a multi-decade demand horizon with reduced policy reversal risk.

- Manufacturing recovery across the United States and China, evidenced by ISM and NBS PMI readings above 50 in March 2026, supports baseline industrial demand concurrently with structural growth from the hydrogen sector, amplifying the pricing effect of constrained supply.

- Geographic supply concentration, approximately 90% of global PGM reserves in South Africa and approximately 80% of production from South Africa and Zimbabwe combined, increases the value of development-stage projects in alternative jurisdictions with established logistics and infrastructure access.

- Development-stage assets with near-surface open-cast mineralization and heap leaching feasibility under evaluation offer higher price sensitivity to PGM market movements than producing royalties or diversified miners, at proportionally higher execution and financing risk.

- Resource conversion from inferred to indicated classification represents the near-term catalyst that can re-rate development-stage PGM equities independent of commodity price movement.

Germany has legally committed to hydrogen infrastructure through 2045, Europe received six times more funding applications than it could award in its latest hydrogen auction, and both the US and Chinese manufacturing sectors returned to expansion in March 2026, all three pointing toward platinum demand that existing mines, 90% concentrated in South Africa with only two new projects in global development, cannot meet at current output rates. The platinum market is already running an approximately 350,000 ounce annual shortfall, with less than five months of stockpiles remaining as a buffer.

The demand is no longer speculative, governments have signed it into law, corporations have committed capital to it, and trucks running on platinum-dependent fuel cells are already logging commercial kilometers. What remains open is whether new platinum supply can reach production within the five-to-ten years these projects require to build. That gap between committed demand and constrained supply is where platinum prices will be set, and where early-stage developers outside southern Africa stand to deliver returns that larger, more diversified miners cannot.

TL;DR

Germany's Hydrogen Acceleration Act mandates hydrogen infrastructure through 2045, creating policy-backed platinum demand for fuel cells and electrolyzers. The platinum market already runs a 350,000-ounce annual deficit with above-ground stocks down 42% and less than five months of coverage remaining. Manufacturing recovery in the US and China compounds baseline demand while 90% of global reserves remain concentrated in South Africa. Each fuel cell truck requires 100 grams of platinum, translating infrastructure buildout directly into measurable metal consumption. Development-stage projects outside southern Africa offer leveraged exposure to structural deficits, though investors face execution risk, long permitting timelines, and metallurgical uncertainty against supply constraints existing mines cannot resolve.

FAQs (AI-Generated)

Platinum serves as the catalyst in proton exchange membrane (PEM) electrolyzers that produce hydrogen from water and in fuel cells that convert hydrogen back to electricity. Platinum's electrochemical stability under acidic, high-temperature conditions makes it technically irreplaceable in these applications. Each commercially deployed fuel cell truck currently requires approximately 100 grams of platinum, translating infrastructure deployment directly into metal demand.

The platinum market is running an annual deficit of approximately 350,000 ounces, independent of automotive demand. Combined platinum and palladium deficits reach 500,000 to 700,000 ounces annually. Above-ground inventories have declined 42% per World Platinum Investment Council data, leaving less than five months of market coverage remaining—eliminating the buffer that historically dampened price volatility.

Approximately 90% of global PGM reserves are located in South Africa, with South Africa and Zimbabwe together accounting for roughly 80% of current production. This geographic concentration limits supply elasticity. PGM projects typically require five to ten years from discovery to first production, involving multiple permitting stages and capital raises. Supply cannot respond quickly to demand shocks occurring now.

Germany's Hydrogen Acceleration Act, approved by the Deutscher Bundestag, designates hydrogen production, import, storage, and transport as matters of overriding public interest through 2045. This legislative structure provides regulatory priority for project approvals and reduces policy reversal risk. When governments embed commodity applications into national infrastructure frameworks for multiple decades, demand signals approach the durability of non-discretionary utility-grade materials.

Development-stage assets face financing risk across multiple capital raises, permitting timelines extending five to ten years, and metallurgical uncertainty until flowsheet optimization is complete. Projects outside established mining jurisdictions may lack processing infrastructure. However, these risks must be weighed against higher price sensitivity to PGM market movements compared to producing royalties or diversified miners, particularly for near-surface open-cast deposits with heap leaching feasibility.

Analyst's Notes

Subscribe to Our Channel

Stay Informed