Highland Copper Nears Construction Decision as Copperwood NPV Triples on Copper Price Surge

Highland Copper advances fully-permitted Copperwood to H2 2026 construction decision with EXIM backing 60-70% of $425M capex; NPV triples to $507M at $5/lb copper consensus

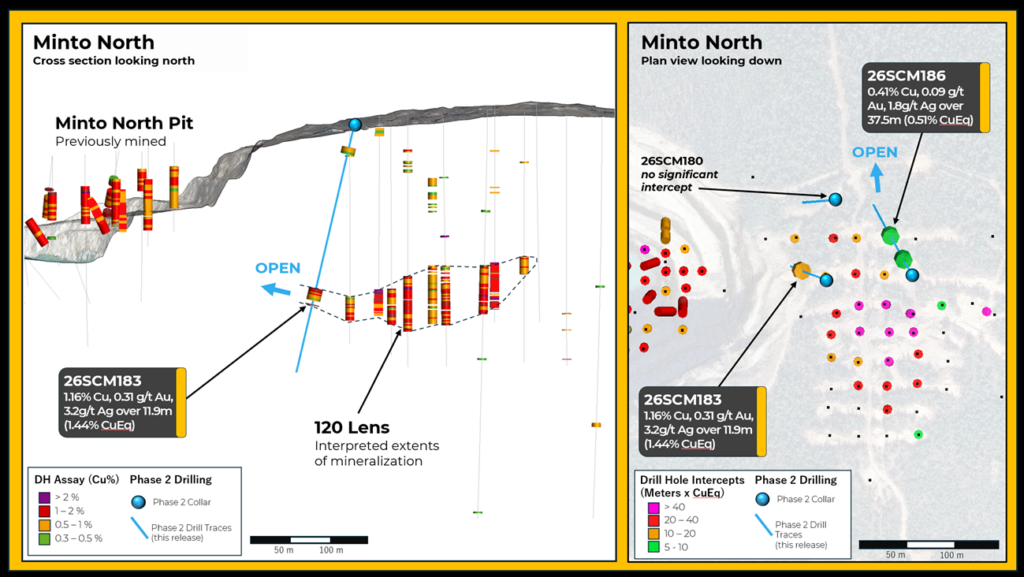

- Highland Copper targets construction decision in H2 2026 for Copperwood Project with copper production planned for 2029 supported by advancing engineering packages to 40% completion by Q4 2026.

- EXIM Letter of Intent represents 60-70% of the $425M capex, though currently non-binding and the company is working to convert to binding debt facility with strong federal support including White House recognition.

- Highland Copper sold remaining White Pine stake for $30M providing liquidity and strategic focus exclusively on the fully-permitted Copperwood project in Michigan's Upper Peninsula.

- The company holds significant copper price leverage as NPV increases from $170M at $4/lb copper to $850M at current spot of $6/lb with project economics robust even at lower price scenarios.

- Strong institutional backing from Orion Mines Finance (28%) and Condire (20%), with enhanced leadership including new Project Director Trace Arlaud, former Rio Tinto’s Resolution Copper GM, and interim CFO Peter Hemstead, Capstone Copper founding executive.

Highland Copper stands at a critical inflection point as one of the most advanced copper development projects in the United States. With a targeted construction decision in the second half of 2026 and planned production by 2029, the company's Copperwood project in Michigan's Upper Peninsula represents a rare fully-permitted domestic copper asset entering development at a time of surging demand for critical minerals. CEO Barry O'Shea discussed the company's progress, financing strategy, and the transformational impact of higher long-term copper prices on project economics in a recent interview.

Advancing Toward Construction Decision

Highland Copper continues to track toward its construction decision timeline, having committed significant capital to advancing engineering work. The company has awarded all detailed engineering contracts, partnering with DRA Global and other established engineering firms to push the project to 40% engineering completion by Q4 2026. This represents substantial progress from the feasibility study stage, as O'Shea emphasised:

"We've signed all contracts out particularly with DRA Global amongst other really well-reputed engineers so I think we're in a good position. We've restructured the company very well to make sure we're fully funded through to a final investment decision and then certainly excited about that."

The engineering advancement includes significant process improvements, notably the incorporation of Jameson cell ultrafine flotation technology announced in Q3 2025. This technology upgrade is expected to increase copper recoveries by approximately 2% points while simultaneously reducing plant size, power consumption, and reagent usage. The company is currently conducting parallel optimisation work on the mining side, evaluating improvements to mine height, pillar size, and ground support systems.

The Federal Financing Pathway

The cornerstone of Highland Copper's financing approach is a Letter of Intent from EXIM (Export–Import Bank of the United States) representing approximately 60-70% of the $425 million capital requirement. While currently non-binding, management is actively working to convert this into a binding debt facility. The company has received notable federal recognition, with recent White House publications identifying the Copperwood project as important to U.S. critical mineral and copper production.

O'Shea explained the significance of this federal engagement:

"As we're in the halls in DC, we're working at EXIM driving these early products into final binding products and other forms of grants and equity, I think we are in very good standing in terms of our visibility."

The debt capacity of the project has expanded with rising copper prices. At $4 per pound copper, debt capacity was estimated around $250 million, but management believes this has increased to potentially $300-325 million at current price assumptions. Beyond EXIM, the company is exploring additional debt sources through offtake agreements with refiners and strategic partners interested in their clean concentrate, which could provide favourable debt terms or equity participation.

Strategic Refocus on Copperwood

Highland Copper recently sold its remaining one-third stake in the White Pine project for $30 million, following an earlier sale of two-thirds of the asset three years prior. This divestiture provides immediate liquidity while allowing management to concentrate exclusively on Copperwood. The decision reflects a deliberate strategic choice based on project scale and permitting status.

White Pine, while potentially valuable, faces a longer development timeline with permits not yet submitted and an estimated capital requirement exceeding $1 billion. The $425 million Copperwood capex is considered more manageable and financeable for a company of Highland's size, particularly given its fully-permitted status which is a critical distinction in the U.S. regulatory environment where the average timeline from first drill hole to production approaches 20 years.

Interview with Barry O'Shea, CEO of Highland Copper

Transformational Copper Price Economics

The shift in long-term copper price consensus represents a fundamental change in Copperwood's investment proposition. At $4/lb copper, the project generates an NPV of approximately $170 million with an 18% IRR. However, with long-term consensus approaching $5/lb, the NPV triples to $507 million. At current spot prices of nearing $6/lb, the NPV nearly doubles again to $850 million.

This exponential leverage stems from Copperwood's position on the cost curve. As an underground operation in the United States, it sits on the higher end of the cost spectrum, requiring robust copper prices for economic viability. O'Shea candidly acknowledged this characteristic, stating:

"As you look back 1 to 5 years ago, Copperwood is an underground asset in the US. It is slightly on the higher end of the cost curve. So, it needs a pretty robust copper price. But now as long-term consensus has moved to nearing $5, we have incredible leverage to changes in copper price."

Building the Execution Team

Highland Copper has strengthened its technical and financial leadership to support project execution. The company hired Trace Arlaud as Project Director, bringing world-class credentials from her role as General Manager of Execution for Rio Tinto's Resolution Copper project. Arlaud also has relevant local experience, having spent several years at the Eagle Mine on Michigan's Upper Peninsula working on design, optimisation, and construction.

The interim CFO position is filled by Peter Hemstead, a founding executive at Capstone Copper who helped build that company into a significant intermediate producer through acquisition and organic growth. Hemstead brings extensive experience in both CFO and CEO roles. The company retained outgoing Project Director Wynand van Dyk on a technical advisory contract, ensuring continuity while he transitions to a professorship in South Africa.

A Fully-Permitted Development Asset

Copperwood contains 3.7 billion pounds of copper across all resource categories, with measured and indicated resources grading 1.5% copper. The project benefits from a complete feasibility study and full permitting - distinguishing factors that make it eligible for federal financing programs and particularly attractive in the current U.S. policy environment focused on domestic critical mineral production.

The 11-year mine life at feasibility stage is relatively conservative, as it only incorporates measured and indicated resources. Current optimisation work on mine recovery, pillar sizing, and cutoff grade could extend mine life while the process improvements are expected to boost copper recovery rates. The high-grade nature of the first four to five years of production creates robust payback economics that support debt financing.

Institutional Support Behind the Story

Highland Copper trades with a market capitalisation of approximately C$110 million, which management believes significantly undervalues the asset given the improved economics and de-risked development pathway. The company benefits from strong institutional support, with Orion Mine Finance holding 28% and Condire, a Texas-based natural resources fund, holding 20%. Notably, when Greenstone liquidated its fund position in late 2025, Condire increased its stake from 16% to 20%, demonstrating continued institutional conviction.

The Investment Thesis for Highland Copper

- Fully-permitted, advanced-stage U.S. copper project with complete feasibility study, eliminating years of permitting risk that affects competing domestic projects

- Near-term construction decision (H2 2026) with production targeted for 2029, offering relatively short pathway to cash flow in a rising copper price environment

- Strong federal alignment through EXIM Letter of Intent (60-70% of capex) and White House recognition as strategically important to U.S. critical minerals

- Exceptional copper price leverage: 3x NPV increase from $4 to $5/lb copper price, with further doubling to $850M at $6/lb spot pricing

- Strategic scale at $425M capex considered optimal for financing and execution compared to multi-billion dollar projects, while still providing meaningful production profile

- Experienced technical leadership including Rio Tinto Resolution Copper veteran as Project Director and Capstone Copper founding executive as interim CFO

- Focused single-asset strategy following $30M White Pine divestiture, concentrating resources and management attention exclusively on Copperwood development

- Strong institutional backing from long-term shareholders Orion Mines Finance (28%) and Condire (20%), with recent insider accumulation

- Engineering improvements underway incorporating Jameson cell technology for enhanced recoveries and reduced operating costs, with 40% engineering target by Q4 2026

- Significant market cap discount: ~$110M valuation versus $507M NPV at $5/lb copper consensus, suggesting substantial rerating potential upon EXIM binding commitment

Macro Thematic Analysis

The global energy transition and electrification trends are creating unprecedented copper demand at a time when new mine supply faces extended development timelines and permitting challenges. In the United States specifically, the average 20-year timeline from discovery to production has created a domestic supply deficit even as federal policy increasingly prioritises critical mineral security. Highland Copper's Copperwood project addresses this gap as one of the few fully-permitted, advanced-stage copper assets capable of near-term production. As O'Shea succinctly stated:

"There's a time and place for all assets and I think 2026, we're going to see some real value here."

The convergence of rising long-term copper price consensus (approaching $5/lb), federal financing support through programs like EXIM, and White House recognition of strategic importance creates a favourable environment for domestic copper developers who can demonstrate execution readiness.

TL;DR

Highland Copper is advancing its fully-permitted Copperwood project toward a H2 2026 construction decision, supported by EXIM financing commitments representing 60-70% of the $425M capex and strong federal recognition. The project's NPV triples from $170M to $507M as long-term copper consensus moves from $4 to $5/lb, with current spot at $6/lb offering $850M NPV potential. Copperwood project copper production is targeted by 2029. Recent White Pine divestiture at $30M provides liquidity and strategic focus, while enhanced leadership and engineering optimisation position the company for execution at a market cap of just over $110M.

FAQs (AI Generated)

The company is targeting a final investment decision in the second half of 2026, with copper production planned to commence by 2029 following a construction period of approximately two to two-and-a-half years.

The USXM Letter of Intent represents 60-70% of the $425M capex requirement and carries federal backing, though it remains non-binding. Converting this to a binding debt facility is management's key near-term priority.

The project shows exponential leverage: NPV of $170M at $4/lb copper, $507M at $5/lb (current consensus), and $850M at $6/lb spot pricing, reflecting its higher cost curve position.

White Pine required over $1B capex with permits not yet submitted, creating a longer timeline. The $30M sale funded Copperwood focus, which is fully permitted at manageable $425M capex scale.

Engineering advancement to 40% completion by Q4 2026, mine optimisation studies, updated feasibility study incorporating process improvements, and converting the USXM LOI to binding debt facility.

Analyst's Notes

Subscribe to Our Channel

Stay Informed