How Copper Supply Deficits Are Reshaping the Critical Minerals Landscape

Copper supply faces 30% deficit by 2035 as demand surges for EVs and renewables. IEA warns of critical shortfall threatening energy transition goals.

- The International Energy Agency (IEA) projects a critical 30% copper supply shortfall by 2035, with demand rising from 27 Mt in 2024 to 37 Mt by 2050 while mine output is expected to decline after the late 2020s.

- Structural challenges are intensifying across the industry. Copper ore grades have declined 40% since 1991, mine development timelines now average 17 years, and only 14 new copper deposits have been discovered in the past decade compared to 225 in the previous 23 years.

- Electric vehicles, renewable energy infrastructure, data centers, and grid modernization are driving unprecedented copper requirements. AI data centers alone could potentially consume 250-550 kt annually by 2030, representing 1-2% of global demand.

- Supply concentration risks are mounting as China controls 45% of global copper refining capacity, while the top three mining countries account for 46% of production. This creates potential supply chain vulnerabilities as geopolitical tensions persist.

- Companies like Marimaca Copper, Gladiator Metals, Pan Global Resources, and Fitzroy Minerals are advancing strategic projects that could help bridge the supply gap with shorter development timelines and favorable jurisdictions.

The Scale of the Problem

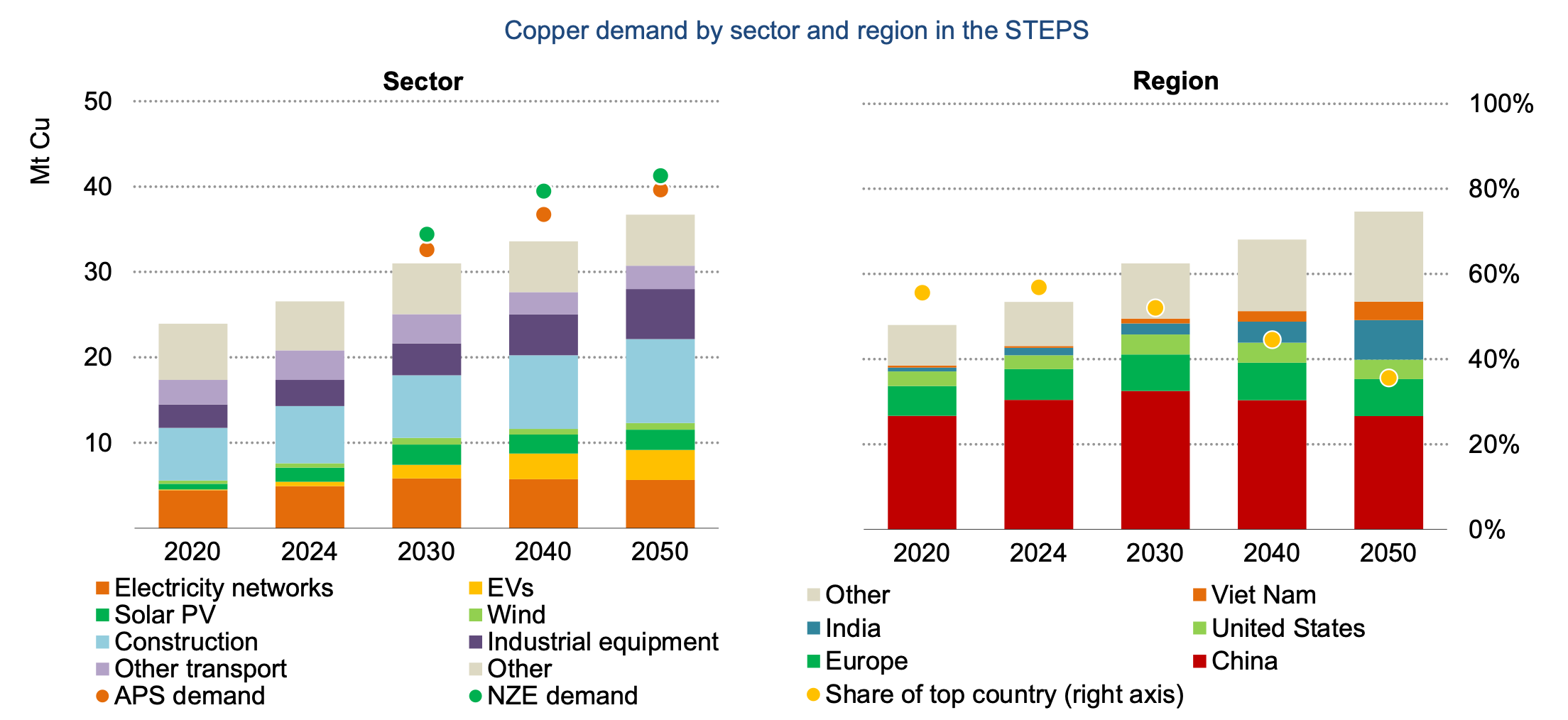

The copper market faces an unprecedented supply-demand imbalance that threatens to constrain the global energy transition. According to the IEA's Global Critical Minerals Outlook 2025, global refined copper demand reached nearly 27 million tonnes in 2024 and is projected to grow to 33 Mt by 2035 and 37 Mt by 2050 under their Stated Policies Scenario (STEPS).

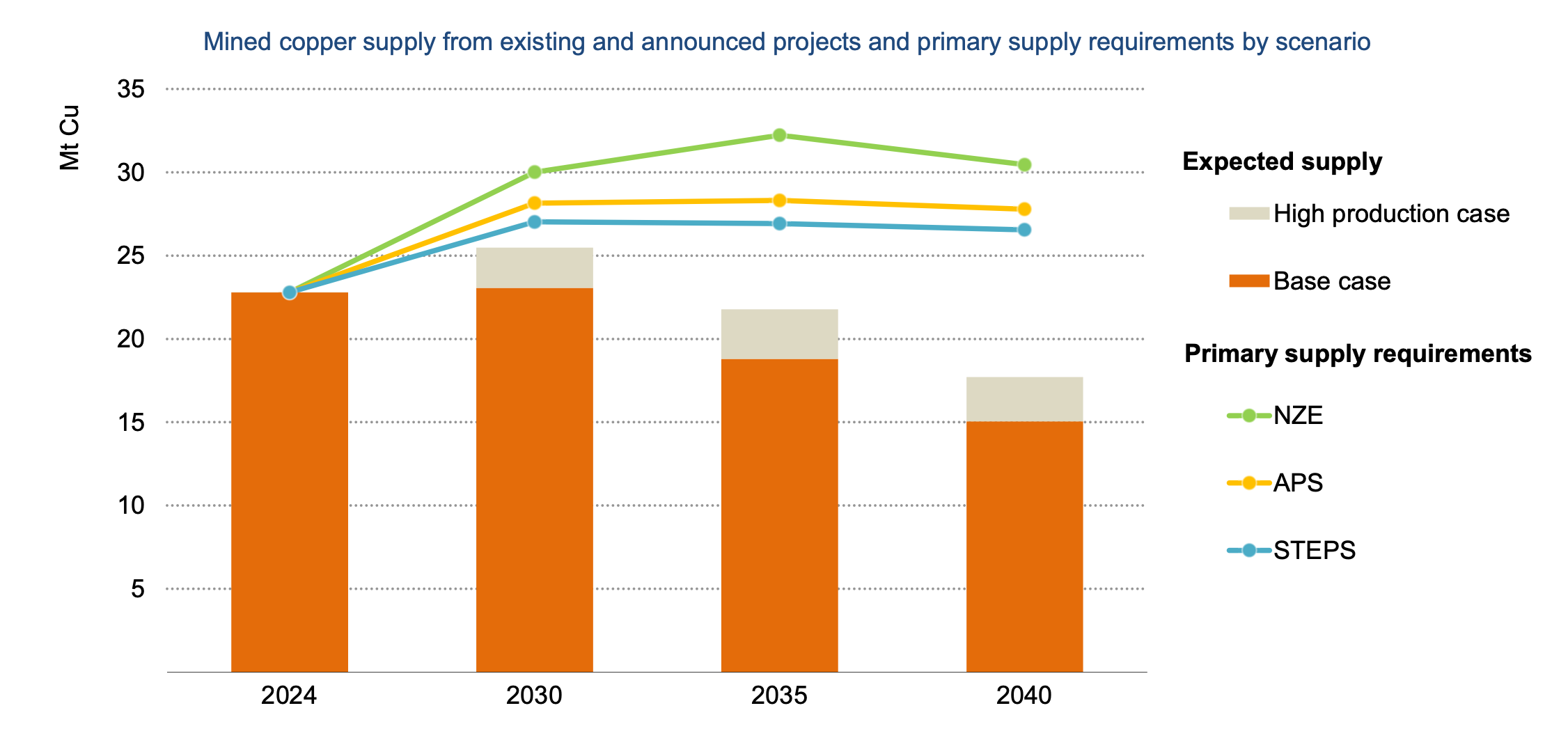

However, based on the current pipeline of existing and announced mining projects, the industry faces a 30% supply deficit by 2035. This gap widens significantly under more aggressive climate scenarios, reaching 35% in the Announced Pledges Scenario (APS) and over 40% in the Net Zero Emissions Scenario (NZE).

The deficit becomes even more concerning when examining the trajectory of mine supply. Global mined copper output reached 22.8 Mt in 2024, with production expected to peak around the late 2020s at just over 24 Mt before declining noticeably to less than 19 Mt by 2035. This decline reflects a combination of factors including declining ore grades, asset retirements, and reserve depletion.

Even under optimistic assumptions in the IEA's high production case, which assumes faster project development and higher success rates, a 20% supply deficit persists by 2035 under the STEPS scenario.

Structural Headwinds Constraining Supply

Declining Ore Grades & Rising Costs

The fundamental challenge facing copper mining is the steady deterioration of ore quality. Average copper ore grades have declined approximately 40% since 1991, a trend that is only partially explained by technological advances such as solvent extraction and electrowinning that have enabled the processing of lower-grade deposits.

This grade decline has significantly increased capital costs and operational complexity. In Latin America, the world's leading copper-producing region, average brownfield project capital intensities have increased 65% since 2020, approaching levels typically associated with greenfield developments.

Extended Development Timelines

New copper mines face increasingly lengthy development cycles, with the average timeline from discovery to production now spanning 17 years. Major projects including Oyu Tolgoi in Mongolia and Quebrada Blanca 2 in Chile have experienced significant delays and cost overruns, highlighting the challenges of bringing new supply online.

This extended timeline is particularly problematic given the urgency of the supply deficit, as projects beginning development today will not reach production until well into the 2040s.

Discovery Drought

Perhaps most concerning is the dramatic slowdown in new copper discoveries. Of the 239 copper deposits discovered between 1990 and 2023, only 14 were found in the past decade. This represents a critical constraint on future supply potential, as the industry depends on a robust pipeline of new discoveries to replace depleting reserves.

The shift in global exploration budgets away from grassroots discovery programs toward lower-risk brownfield expansions has contributed to this trend, but it also reflects the increasing difficulty of finding new, high-grade deposits in accessible locations.

Demand Drivers Intensifying Pressure

Electrification & Clean Energy

The clean energy transition is fundamentally reshaping copper demand patterns. Electric vehicles represent the fastest-growing demand segment, with consumption projected to increase sevenfold from 2% of global copper demand in 2024 to 10% by 2050 in the STEPS scenario.

Electricity networks and renewable energy infrastructure remain significant demand drivers, with solar and wind installations requiring substantially more copper per unit of capacity than conventional power generation. Grid modernization efforts to accommodate renewable energy sources are adding further to copper requirements.

Industrial & Construction Demand

Beyond clean energy applications, traditional demand sources continue to grow. Industrial machinery and equipment demand is expected to nearly double by 2050, driven by manufacturing expansion and electrification across emerging economies. Construction demand, while growing more moderately, remains the largest single application for copper.

Emerging Technologies

Artificial intelligence and data center expansion represent a new frontier for copper demand. The IEA estimates that copper use in data centers could range from 250 kt to 550 kt by 2030, representing 1-2% of global demand. AI-enabled data centers require particularly copper-intensive power distribution systems and advanced cooling infrastructure.

Geographic Shifts & Supply Security Risks

Production Concentration

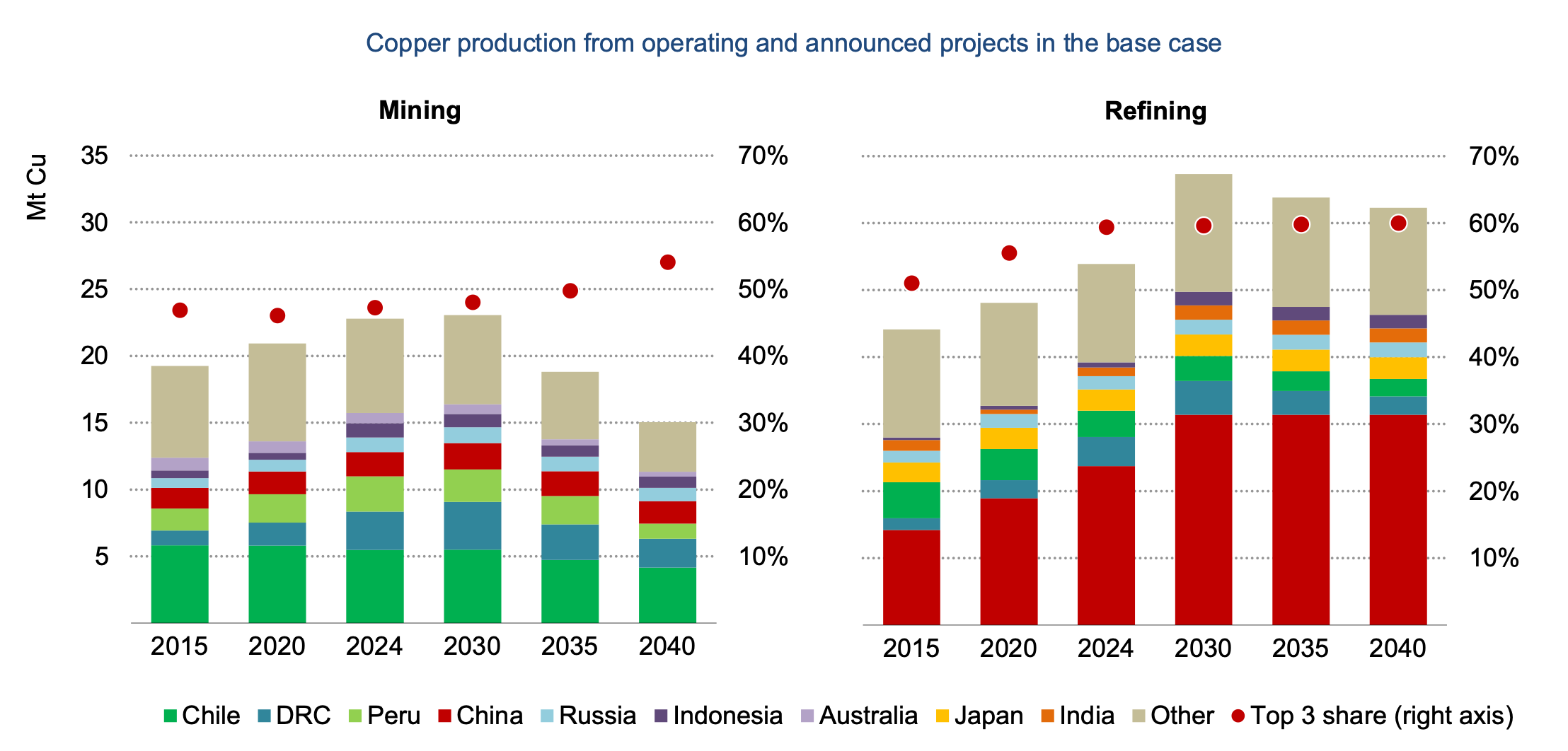

Current copper production remains geographically concentrated, with Chile supplying approximately 25% of global output and maintaining its position as the world's largest producer. The Democratic Republic of Congo (DRC) has emerged as the second-largest producer, overtaking Peru in 2024.

Major near-term supply growth is expected from the DRC, particularly from projects such as Kamoa-Kakula and Tenke Fungurume, which are projected to increase combined output to over 1.3 Mt by 2028 from 900 kt in 2024. The Oyu Tolgoi expansion in Mongolia represents another significant source of near-term growth, with production targeted to reach around 600 kt by 2028.

Refining Dominance

Supply security concerns are particularly acute in copper refining, where China controls 45% of global capacity and is projected to increase its share to 50% by 2040. This concentration has created challenging market dynamics, with Chinese smelter capacity expansion driving spot treatment and refining charges to record lows and creating competitive pressures for facilities in other regions.

The DRC overtook Chile in 2024 to become the world's second-largest copper refiner, producing 8% of global supply, but this still leaves the refining sector heavily concentrated among a small number of countries.

Emerging Demand Centers

While China dominated copper consumption with nearly 60% of global refined demand in 2024, new consumption centers are emerging in Asia. India is projected to rapidly overtake the United States as the third-largest source of refined copper demand, growing from 3% in 2024 to over 10% by 2050. Vietnam is also expected to emerge as a major consumer, increasing from 1% to 6% of global demand over the same period.

Junior Companies as Part of the Solution

Against this backdrop of supply constraints and growing demand, a new generation of copper development companies is advancing projects that could help bridge the supply gap with shorter timelines and strategic advantages.

Marimaca Copper: Chilean Oxide Efficiency

Marimaca Copper is developing what represents one of the few globally significant copper discoveries of the past decade in Chile. The Marimaca project hosts 900 kt of copper in Measured & Indicated resources plus 141 kt in Inferred resources, with 86% of the total resource base already classified as M&I.

The project's strategic advantages include its proximity to existing infrastructure, located 25 km from Mejillones port and 40 km from Antofagasta. The deposit's favorable geometry enables a low-strip-ratio, heap leach operation that the company estimates will produce 38% lower carbon emissions than traditional flotation methods.

Water security, often a critical constraint for Chilean copper projects, has been de-risked through secured water rights, while the location on government land reduces social permitting risks that have plagued other regional developments.

Gladiator Metals: Rediscovering Canadian Potential

Gladiator Metals is systematically exploring the historically productive Whitehorse Copper Belt in Canada's Yukon Territory, a 35-kilometer strike length that produced copper in the past but has been underexplored using modern techniques.

The company's approach focuses on multiple shallow, high-grade copper-gold prospects including Cowley Park and the Chiefs Trend, with grades ranging from 1.5-2%+ copper equivalent. The Yukon jurisdiction offers political stability and established mining regulations, while existing infrastructure including road access, hydroelectric power, and laboratory facilities could enable faster development timelines than typical greenfield projects.

The company's recent agreement with the Kwanlin Dün First Nation demonstrates early community engagement that could facilitate permitting processes.

Pan Global Resources: European Strategic Play

Pan Global Resources is advancing the La Romana deposit within Spain's Iberian Pyrite Belt, one of the world's most productive volcanogenic massive sulfide (VMS) districts. The near-surface discovery has been defined through over 188 drill holes and demonstrates exceptional metallurgical characteristics with 88% copper recovery and 32.5% copper concentrate grades.

The project's copper-tin-silver system provides revenue diversification beyond copper alone, while Spain's supportive mining regulations and established permitting frameworks could enable faster development than in many other jurisdictions. The proximity to European smelting and processing infrastructure reduces both capital requirements and transportation costs.

Pan Global controls over 5,700 hectares across multiple targets including Bravo, Pantoja, and Cañada Honda, providing exploration upside beyond the initial La Romana development.

Fitzroy Minerals: Chilean Discovery Potential

Fitzroy Minerals is developing the Buen Retiro iron oxide copper gold (IOCG) deposit in Chile, featuring both oxide and sulfide mineralization across a 3x2 kilometer zone. Recent drilling has returned significant intercepts including 110 meters at 1.94% copper and 135 meters at 0.73% copper.

The deposit's mineralogy, including tenorite, chalcocite, and native copper, is highly amenable to heap leaching, potentially enabling lower capital intensity development. Strategic location advantages include proximity to the Pan-American Highway and Pucobre's existing processing infrastructure.

Fitzroy maintains a diversified exploration portfolio across Chile and Argentina, including the Caballos, Polimet, and Taquetren projects, providing multiple pathways to discovery success.

Market Dynamics & Investment Requirements

Capital Investment Needs

Addressing the copper supply deficit requires substantial capital investment across the mining value chain. The IEA estimates that the industry needs between $500 billion and $800 billion of investment by 2040 to keep pace with demand under their various scenarios. BloombergNEF has projected even higher requirements, estimating $2.1 trillion in investment across energy-transition metals by 2050.

These investment requirements reflect not only the need for new mine development but also the increasing capital intensity of copper projects due to declining grades, more complex metallurgy, and stricter environmental and social requirements.

Secondary Supply Potential

Recycling represents a critical component of future copper supply, though current recycling rates remain below potential. Secondary copper supply accounted for less than 17% of total demand (excluding direct-use scrap) in 2024, down from 18% in 2015.

With appropriate policy support and improved collection infrastructure, the IEA projects that secondary copper supply could grow to nearly 35% of total demand by 2050. However, even aggressive recycling scenarios cannot fully address the projected supply deficit, emphasizing the continued need for new mine development.

Price Implications

Copper prices experienced significant volatility in 2024, reaching as high as $10,800 per tonne before declining due to various factors including Chinese property sector weakness and concerns about global economic growth. The structural supply deficit is expected to provide long-term price support, though short-term fluctuations will continue to reflect economic conditions and geopolitical developments.

Policy & Strategic Responses

Governments and industry stakeholders are beginning to recognize the strategic importance of copper supply security. Policy responses have included:

- Resource diplomacy: Developed countries are seeking to diversify supply sources through partnerships with resource-rich nations outside traditional suppliers.

- Domestic mining support: Countries including the United States and members of the European Union are implementing policies to support domestic copper production and processing capabilities.

- Recycling initiatives: Enhanced collection and processing infrastructure for copper scrap, though implementation timelines remain extended.

- Technology development: Investment in extraction technologies that could unlock lower-grade deposits or improve processing efficiency.

For Investors

The copper supply deficit represents one of the most significant challenges facing the global energy transition. With demand growth driven by electrification, renewable energy deployment, and emerging technologies, while supply faces structural constraints from declining ore grades, extended development timelines, and limited new discoveries, the industry requires coordinated action across multiple fronts.

While large-scale mining projects will remain essential for meeting long-term demand, junior developers advancing strategic projects in favorable jurisdictions could play an increasingly important role in bridging near-term supply gaps. Companies like Marimaca Copper, Gladiator Metals, Pan Global Resources, and Fitzroy Minerals represent examples of how focused development efforts on high-quality deposits could contribute meaningfully to global copper supply.

The resolution of the copper supply challenge will require sustained investment, policy support for mining development, aggressive recycling programs, and continued exploration success. The timeline for addressing these constraints is compressed, making near-term production additions from advanced development projects increasingly valuable in supporting the broader energy transition.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed