The Copper Market is Poised for Extraordinary Growth

Discover why copper's reliable demand, supply constraints, and essential role in electrification make it a compelling investment opportunity in today's resource market.

- Copper has demonstrated remarkably stable demand growth over the past 50 years, adding 3-4 million metric tons per decade despite technological shifts and economic cycles.

- The world's major copper mines are aging (many over 100 years old), while new discoveries face decades of permitting delays and significant capital requirements.

- While electric vehicles and AI are significant growth drivers, copper remains essential for global construction, infrastructure, and electrification regardless of technological trends.

- Major powers including China are making geopolitical moves to secure copper resources, recognizing its critical role in the energy transition.

- Successful copper discoveries offer outsized returns due to the scale of projects and their increasing scarcity, with majors actively seeking quality assets.

The Copper Market Dynamics

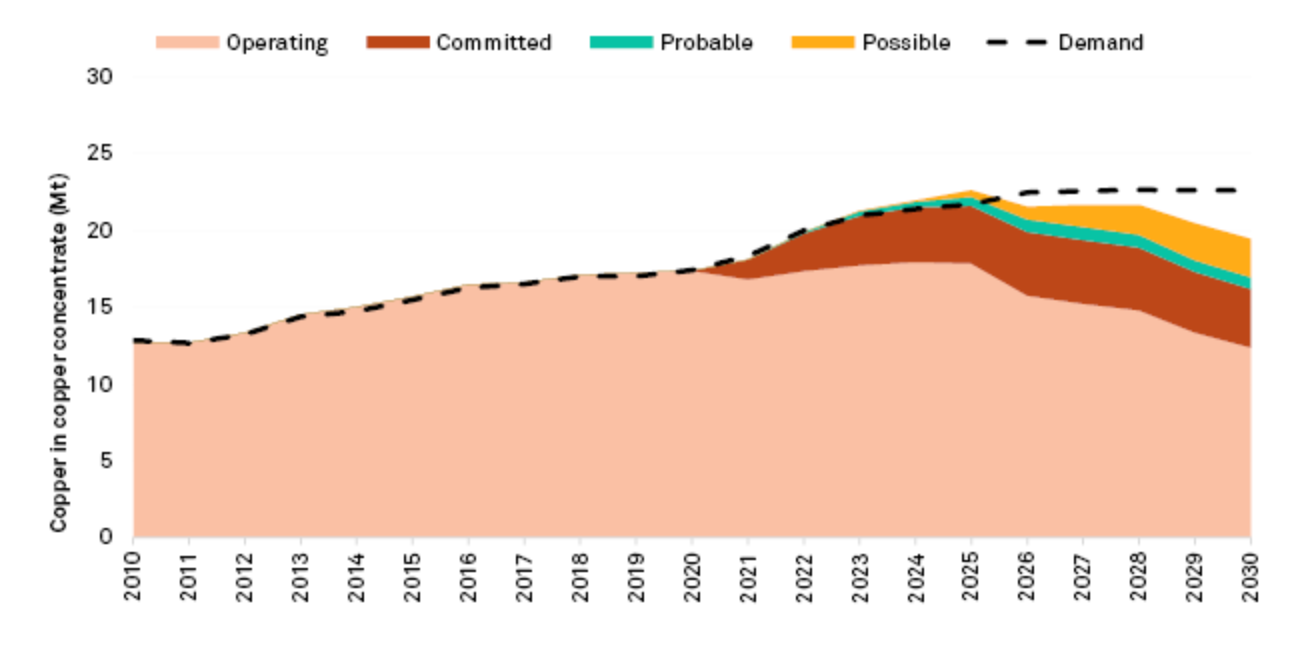

Copper remains an essential industrial metal whose price movements have historically provided insight into the broader economic outlook. But today's copper market presents a compelling investment thesis that goes beyond its traditional role.

This fundamental truth is often overlooked amid trendy narratives about electric vehicles and artificial intelligence. Copper is essential and goes into virtually everything in our modern economy.

The copper demand story is remarkably consistent. When examining 50 years of copper consumption data, we see that decade over decade – from the 1970s through today – global demand has added approximately 3-4 million metric tons per decade. This growth persisted through technological revolutions (personal computers, the internet, smart technology) and multiple economic downturns.

This supply-demand dynamic creates a critical window for new projects. As Nico Cookson of Marimaca Copper notes:

"When we run our searches for comparable projects that can be delivering cathode or concentrate in the next three years, there is almost nothing, particularly nothing owned by single asset developers in the Americas."

This scarcity of near-term production creates opportunity for well-positioned developers.

While electric vehicles require significantly more copper than traditional vehicles, and data centers for AI processing are copper-intensive, these emerging technologies merely accelerate an already robust demand trajectory. Construction and infrastructure development, particularly in developing economies, remain the foundation of copper demand.

The global population has doubled from around 4 billion in the early 1980s to nearly 8 billion today. This demographic expansion drives construction and development worldwide. From urban renewal in developed nations to rapid infrastructure development in emerging economies, copper remains indispensable.

Perhaps most significantly for investors, copper prices remain relatively attractive compared to some other metals like gold, which has recently approached all-time highs. This pricing dynamic suggests copper may offer greater upside potential.

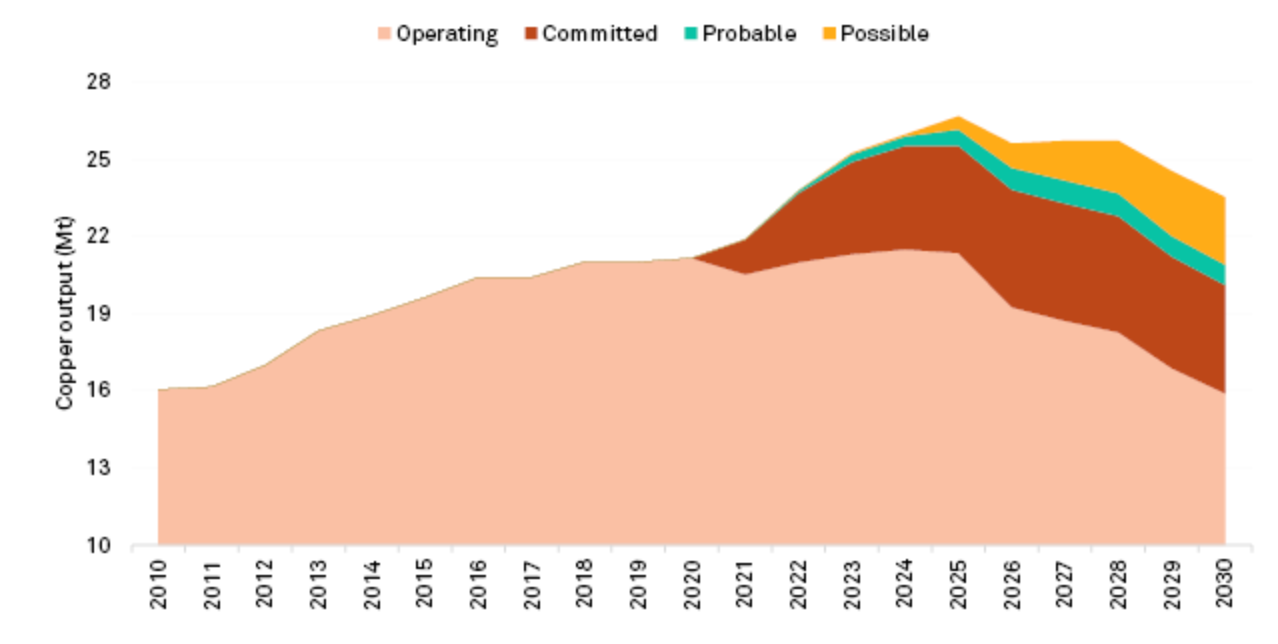

Supply Constraints & Historical Demand

The supply side of the copper equation presents an even more compelling investment case. The world's major copper mines are aging significantly, with many of the largest producers operating well past their prime:

- Rio Tinto's Bingham Canyon (Utah): 160+ years old

- Codelco's Chuquicamata (Chile): 115 years old

- Codelco's El Teniente (Chile): 100 years old

- BHP's Escondida (Chile): 45 years old

Industry leaders recognize the urgency of this supply challenge. As Ben Pullinger, President and CEO of ATEX Resources observes:

"I watched a presentation by BHP yesterday — we need to add an Escondida every two years... If you take all the projects and put them together, I don't think you get to an Escondida. So oversupply is not the problem."

This assessment is echoed by Merin Marr-Johnson, CEO of Fitzroy Minerals:

"The largest copper mines in the world—with the exception of Kamoa-Kakula—are all mature or in decline. At Escondida, the only thing they talk about in board meetings is how to maintain production."

These aging giants face declining grades, increasing depths, and rising production costs. Meanwhile, the pipeline of new projects remains constrained by several factors.

Even when significant new discoveries occur, the permitting process has become exceedingly lengthy. The Resolution Copper project in Arizona, a joint venture owned by Rio Tinto (55%) and BHP (45%) – containing a billion tons of ore at 1.5% copper (three times the global average grade) – has been stuck in permitting for 26 years despite being located in a mining-friendly jurisdiction with existing infrastructure.

The reality is stark: to change production tomorrow, we needed to start 25 years ago. And we didn't.

This supply constraint exists against a backdrop of increasing global electrification. Currently, approximately one billion people worldwide have no access to primary electricity, while another two billion have only intermittent or unaffordable access. As these populations gain reliable electricity, copper demand will accelerate.

Marr-Johnson notes:

"The copper demand profile has just ticked along every year—3.3%, 3% every single year. And with electrification and the rise of the middle class... the demand for copper is just continuing to grow."

The urbanization of China drove a commodities boom from 2000 to 2010. Today, similar urbanization continues across Africa, India, and parts of Southeast Asia. These demographic shifts create persistent demand that transcends short-term economic cycles.

Moreover, monetary policy continues to favor hard assets. Fiscal dominance and global liquidity expansion create an environment typically favorable for commodities like copper. Despite concerns about potential recessions, we believe inflationary pressures will persist, benefiting hard assets including copper.

Challenges in Copper Exploration & Permitting

The path from copper discovery to production has grown increasingly complex and time-consuming. Major copper discoveries are rare and typically require substantial capital, time, and expertise.

The easy discoveries have been made, forcing exploration into more challenging terrains, deeper targets, or regions with complex social and political dynamics.

Marr-Johnson of Fitzroy Minerals emphasizes this fundamental challenge:

"We are in this ongoing strategic long-term shortage of copper supply. There's a sustained supply-demand deficit coming. It's very hard to find new copper deposits." He further notes the extreme time and capital requirements: "Copper is hard to find. It takes 18 years and $6–8 billion to build a new major copper mine. And we need another million tons of copper by 2030—just for AI and data centers."

In this landscape, new discoveries in favorable jurisdictions offer disproportionate value. Tim Moody, President and CEO of Pan Global Resources highlights this advantage:

"We have one of the few new copper discoveries in Europe... With the discoveries at La Romana and Cañada Honda, we believe that the copper project that we have at Escacena is something that could be in production for this copper cycle, not two decades from now."

The scale of copper projects compounds these challenges. Unlike some precious metals operations that can start small and expand, copper mines typically require massive upfront capital expenditures. The economics of copper mining demand scale – the processing of enormous volumes of material to extract relatively small percentages of metal.

Permitting has become perhaps the most significant hurdle. Environmental regulations, community consultations, and political considerations can extend timelines dramatically. In Peru, home to some of the world's largest copper mines, major mines and major permitting challenges go hand in hand.

The social dimension often proves more challenging than government regulations. Companies must secure not only legal permits but also a "social license to operate" – genuine acceptance from local communities. This process can take years or even decades.

The combination of technical, financial, and social challenges creates a significant barrier to new copper supply. For investors, this supply constraint provides the foundation for a long-term bullish thesis – assuming one can identify the right opportunities.

Investment Strategies in Copper

Navigating the copper sector requires discernment. Not all projects offer equal potential, and many junior companies promote prospects with limited economic viability.

Current copper prices, while appearing strong in nominal terms, may not be sufficient to incentivize significant new production. Merlin Marr-Johnson observes:

"What we've seen so far today [in copper] is not an incentive price—we've just seen dollar devaluation. This is not the price that's going to trigger new production." He further notes: "If you look at the copper price in real terms—say, divided by gold—it's actually been on a 20-year downtrend. We're at a lower copper price in real money terms than we were 20 years ago."

When evaluating copper projects that have been known for decades but remain undeveloped, investors should question why. While higher copper prices might improve economics, input costs like energy, labor, and equipment typically rise in tandem, preserving the relative unattractiveness of marginal deposits.

For exploration companies, capital adequacy becomes paramount. How much capital they have and what they plan to do with it next is a fundamental question for any junior explorer. Copper exploration is capital-intensive, and inadequate funding often leads to dilution or project abandonment.

Management ownership provides another valuable indicator. If executives aren't purchasing shares of their company, particularly at depressed valuations, investors should question their conviction in the project's potential.

When considering producers, focus on companies operating in the lowest-cost quartile worldwide with the highest return on capital employed and at least ten years of mine life remaining. This approach emphasizes fundamental security analysis rather than speculative price movements.

For those seeking exploration exposure, team experience specifically in copper geology becomes crucial. Porphyry deposits (the source of most large-scale copper mines) require specialized knowledge. General mining experience doesn't necessarily translate to copper exploration expertise.

Finally, remember that scale matters tremendously in copper. The economics of developing a major copper mine typically requires billions in capital expenditure. Small, high-grade deposits rarely justify the risk involved. The idea of taking big risks for small rewards is fundamentally flawed. In the copper business, it really has to matter.

Future Prospects & Corporate Activity

The widening gap between copper supply and demand has created a heightened sense of urgency among major mining companies. Unable to discover enough copper internally, these corporations increasingly look to acquisitions to secure future production.

Major mining companies have under-invested in exploration and development for 25 years, and they know it. This recognition has created an environment where promising copper discoveries attract immediate attention from multiple major players.

Marr-Johnson sees this supply-demand imbalance continuing: "The copper market is going to really struggle to grow. The demand side continues to grow and so it really feels to me that the copper price has got a long way to go from here."

The financing model for copper projects is also evolving. Ben Pullinger of ATEX Resources observes:

"Copper is looking more like a consortium play now. It's no longer, go out, build the biggest project you can, use your balance sheet and then you have to sit around and wait five to ten years for cash flows to kick in." He points to examples of this trend: "Escondida has five people in there. Collahuasi has like four people in there... Codelco and Anglo Gold getting together on Los Bronces and Andina. Codelco taking a piece of Teck's QB2."

The competition extends beyond traditional Western mining companies. Chinese entities have integrated themselves into copper-rich regions, particularly in the Democratic Republic of Congo and parts of South America. Their approach often includes government-level relationships and strategic offtake agreements that secure copper supply regardless of market prices.

This dynamic reflects copper's strategic importance in the global economy. The modern-day game of thrones in resource acquisition is not purely about economics – it's also about global power and positioning. For investors, this strategic dimension adds another potential catalyst beyond traditional supply-demand economics. Companies that control significant copper resources in stable jurisdictions may command premium valuations as strategic assets.

Among major producers, industry consolidation appears increasingly likely. The potential merger discussions between Rio Tinto and Glencore exemplify this trend. Such combinations could reduce general and administrative expenses while creating entities with greater capital capacity to develop large-scale projects.

However, consolidation among existing producers doesn't address the fundamental supply challenge. Buying isn't building, so M&A activity doesn't bring any more copper into the world. The current market environment is also creating opportunities for projects with unique attributes. Justin Reid, President and CEO of Troilus Gold explains how the copper component of their primarily gold-focused project has become increasingly valuable:

"Copper concentrate funded this mine. And that was a bit of luck for us that our timing was perfect with commodity winds in our sails and also with Cobre Panama shutting down. So there is an absolute shortage of global concentrate right now... TC's & RC's [Treatment & Refining Charges] are negative. Benchmark pricing for Treatment Charges are $25. So everybody needs concentrate."

The ultimate solution requires successful exploration leading to major new discoveries. Companies capable of finding and developing significant new copper resources potentially offer the greatest upside for investors willing to accept the associated risks.

The Copper Investment Thesis

- Structural Supply Deficit: Aging mines, declining grades, and insufficient new discoveries create a persistent supply shortfall relative to steadily growing demand.

- Accelerating Demand Drivers: Traditional construction and infrastructure needs combine with emerging technologies (EVs, renewable energy, data centers) to amplify copper consumption.

- Strategic Value: Copper's essential role in electrification and the energy transition elevates it from commodity to strategic resource, attracting both corporate and national interest.

- Jurisdictional Premium: Projects in stable mining jurisdictions command increasing premiums as geopolitical competition for resources intensifies.

- M&A Catalyst: Major miners actively seeking quality copper assets creates potential exit strategies for successful explorers and developers.

- Inflation Protection: Hard assets like copper mines offer potential protection against monetary debasement and persistent inflation.

Copper sits at the intersection of several powerful global trends that collectively strengthen its investment case. The electrification of the global economy represents perhaps the most significant structural driver. The transition from fossil fuels to renewable energy requires massive copper inputs – from solar panels and wind turbines to energy storage systems and expanded electrical grids.

Electric vehicles represent just one aspect of this broader electrification trend. Each EV requires 2-4 times more copper than an internal combustion vehicle. As EV adoption accelerates globally, driven by both consumer preferences and government mandates, this creates substantial incremental copper demand.

Simultaneously, digitalization continues unabated. The proliferation of data centers to support artificial intelligence, cloud computing, and the internet of things creates another significant demand stream. These facilities require extensive copper for power distribution, cooling systems, and connectivity infrastructure.

Urbanization remains a powerful force, particularly in developing economies. The United Nations projects that 68% of the world's population will live in urban areas by 2050, up from 55% today. This shift necessitates massive construction of residential, commercial, and infrastructure projects – all copper-intensive.

Monetary policy provides another supportive factor. The era of fiscal dominance – where governments prioritize economic growth and social stability over monetary discipline – appears firmly established. This environment typically favors hard assets like commodities that cannot be created through financial engineering.

Geopolitical competition has added another dimension to the copper thesis. The world is increasingly divided into competing power blocs, and major nations view critical minerals, including copper, as strategic assets essential for economic security and technological leadership.

Environmental, social, and governance (ESG) considerations create yet another constraint on supply. While copper itself enables the green transition, copper mining faces increasing scrutiny regarding environmental impacts, water usage, and community relations. These factors extend development timelines and increase costs, further constraining new supply.

The timeline challenge is real for developers. As Nico Cookson from Marimaca Copper explains:

"There are more projects that can be delivering copper on a 10 year timeframe than there are on a five year timeframe... We feel like the end of this decade is the right time to be contributing to where we see the supply and demand dynamic to be the most exciting."

As these macro trends converge, copper appears positioned for sustained price appreciation. While short-term volatility will undoubtedly occur, the structural supply deficit amid accelerating demand creates a compelling long-term investment case. For investors seeking exposure to the electrification and decarbonization of the global economy, copper offers a fundamental pathway with multiple avenues for participation.

Company Profiles: Copper Explorers & Developers to Watch

Marimaca Copper (TSX: MARI)

Project Highlights: Marimaca is advancing its flagship copper oxide project in northern Chile, positioned to deliver copper cathode production by 2028. The project stands out for its near-surface mineralization, simple metallurgy, and location in a premier mining jurisdiction with excellent infrastructure.

Investment Thesis: Marimaca represents one of the few development-stage copper oxide projects that could enter production within this decade.

The company recently achieved a critical permitting milestone with the receipt of its DIA environmental approval, paving the way for project sanctioning in the first half of next year and copper production in 2028—precisely when the supply-demand gap is expected to widen significantly. With its relatively simple mining and processing requirements, Marimaca could deliver copper at a time when new supply will be most valued by the market.

Pan Global Resources (TSXV: PGZ)

Project Highlights: Pan Global is advancing its Escacena copper project in Spain's Iberian Pyrite Belt, a region with a rich mining history and excellent infrastructure. Recent discoveries at La Romana and Cañada Honda have expanded the resource potential significantly.

Investment Thesis: As Tim Moody emphasizes, Pan Global offers "one of the better low risk investment opportunities for people looking to invest in the copper space." The company's European location provides significant advantages, including proximity to smelters, stable permitting frameworks, and reduced geopolitical risk.

The company's metallurgical results "really sets us apart from all the other producers and development projects in the area," according to Moody. Their goal to define up to 100 million tons of resources containing approximately 400,000 tons of copper would create a project with sufficient scale to attract major mining companies. Perhaps most importantly, this is a project that could enter production "for this copper cycle, not two decades from now."

ATEX Resources (TSXV: ATX)

Project Highlights: ATEX is developing the Valeriano copper-gold project in Chile's prolific El Indio Belt. The project features both a substantial copper-gold porphyry system at depth and higher-grade supergene enrichment that could provide early production options.

Investment Thesis: ATEX represents a district-scale opportunity in one of the world's premier copper jurisdictions. As Ben Pullinger notes, "This is a district that we think once it gets up and running is in production for 200 years. Not a lot of places in the world you can do that."

The high-grade component is particularly compelling: "If you add 100 to 200 million tons at 2%, that generates so much cash flow, it can put just about anything into production." This high-grade starter resource could address the industry's challenge of financing massive projects in the current environment.

Pullinger identifies ATEX as fitting "very nicely into that niche between what's out there, what could be out there, and the projects of the future" – offering the potential for high margins with initial smaller-scale development that can be expanded over time. With major miners needing to "add an Escondida every two years" and falling short of this target, assets like Valeriano become increasingly strategic.

Troilus Gold (TSX: TLG)

Project Highlights: Troilus is developing its namesake copper-gold project in Quebec, Canada, a past-producing mine with substantial existing infrastructure and resources. The project benefits from strong ESG credentials and location in a premier mining jurisdiction.

Investment Thesis: While primarily a gold developer (80% of projected revenue), Troilus offers meaningful copper exposure as a critical component of its overall economics. As Justin Reid explains, "Copper funds the mine, gold drives the value."

The company has secured significant off-take interest, with Reid noting, "The majority of them were around raw material guarantees, meaning that we would supply copper and gold concentrate into... various refiners in the European Union, namely Germany, Sweden, and into Finland."

This copper component has proven instrumental in securing project financing in a challenging market: "If we were a pure gold producer right now, even with $3,000 gold, I don't know how we would have financed this mine without a strategic partner." With the closure of First Quantum's Cobre Panama mine creating "an absolute shortage of global concentrate," Troilus offers exposure to both gold upside and critical copper supply at a time when "everybody needs concentrate."

Fitzroy Minerals (TSXV: FTZ)

Project Highlights: Fitzroy Minerals is developing a portfolio of copper-gold projects, with a focus on advanced exploration in mining-friendly jurisdictions. The company pursues assets with significant resource potential that can be developed within the current copper cycle.

Investment Thesis: Fitzroy positions itself at the intersection of macro economics and resource development, offering investors exposure to what they see as the coming copper bull market. Their strategic thesis is built on the foundation that "We are in this ongoing strategic long-term shortage of copper supply. There's a sustained supply-demand deficit coming. It's very hard to find new copper deposits."

The company emphasizes the significance of copper's fundamentals against a backdrop of monetary devaluation: "If you look at the copper price in real terms—say, divided by gold—it's actually been on a 20-year downtrend. We're at a lower copper price in real money terms than we were 20 years ago." This perspective suggests substantial potential upside as the market comes to fully appreciate the severity of copper's supply constraints.

CEO Merlin Marr-Johnson also highlights the specific demand pressure coming from technological expansion: "We need another million tons of copper by 2030—just for AI and data centers." Combined with their view that current prices are "not an incentive price" sufficient to trigger meaningful new production, Fitzroy offers investors a leveraged opportunity to the coming supply-demand imbalance in the copper market.

Analyst's Notes

Subscribe to Our Channel

Stay Informed