Kazakhstan's 10% Production Cut & the $90/lb Uranium Contract Force Utilities to Finance Western Development

Kazakhstan's 10% production cut drives long-term uranium contracts to $90/lb, forcing utilities to finance origin-assured Western development.

- Kazakhstan's Kazatomprom reduced its 2026 nominal production target by 10% to 29,697 tonnes of uranium oxide, removing approximately 8 million pounds of global primary supply.

- December 2025 legislative amendments in Kazakhstan eliminated third-party greenfield exploration incentives, constraining future supply growth from the primary producing basin.

- Great British Energy Nuclear committed £2.6 billion to Rolls-Royce SMR, and the United States awarded $2.7 billion in enrichment contracts, accelerating contracted uranium demand.

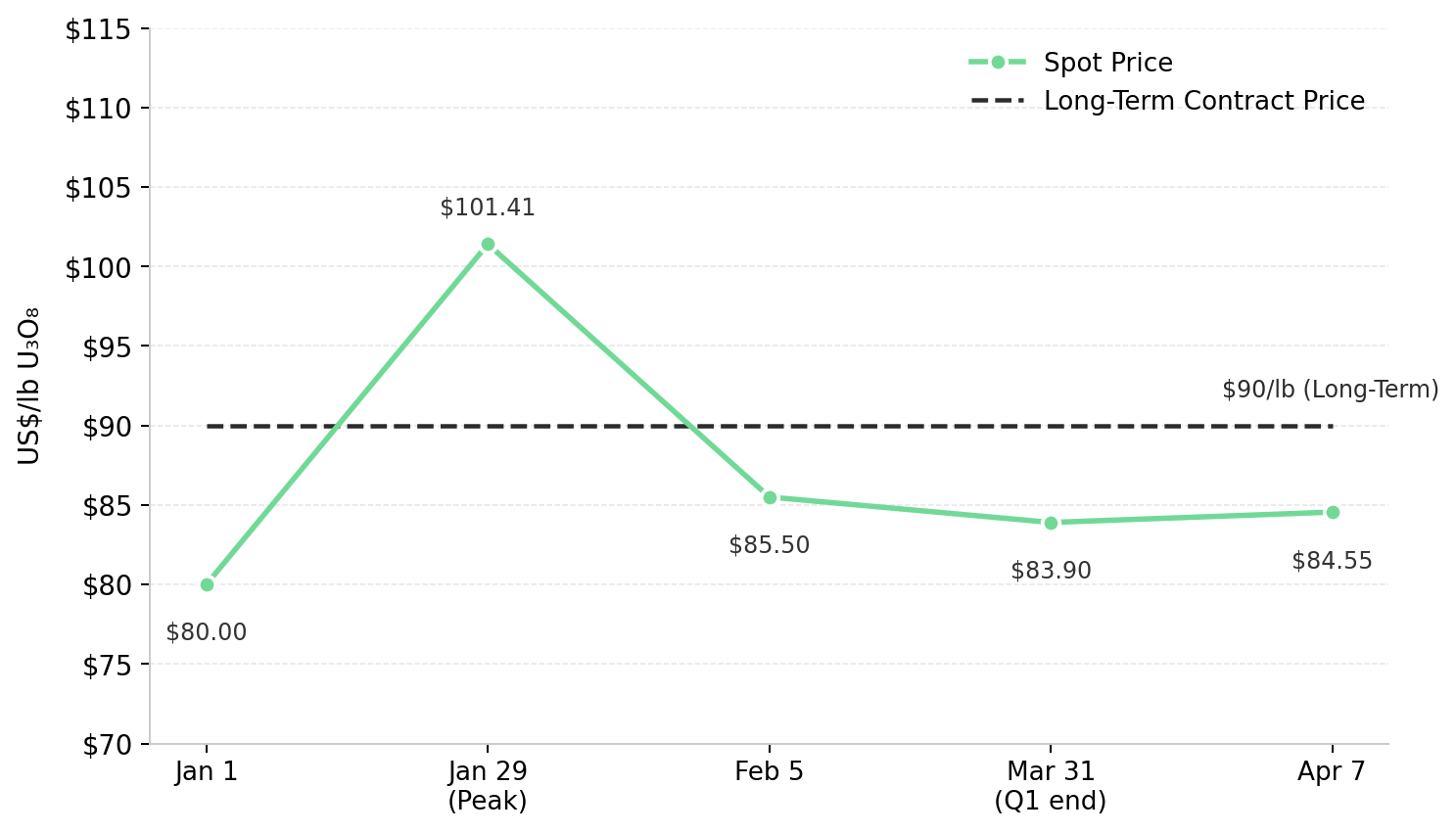

- The long-term uranium contract price reached $90/lb in the first quarter of 2026, establishing a 14-year high that improves the economic viability of Western-aligned development projects.

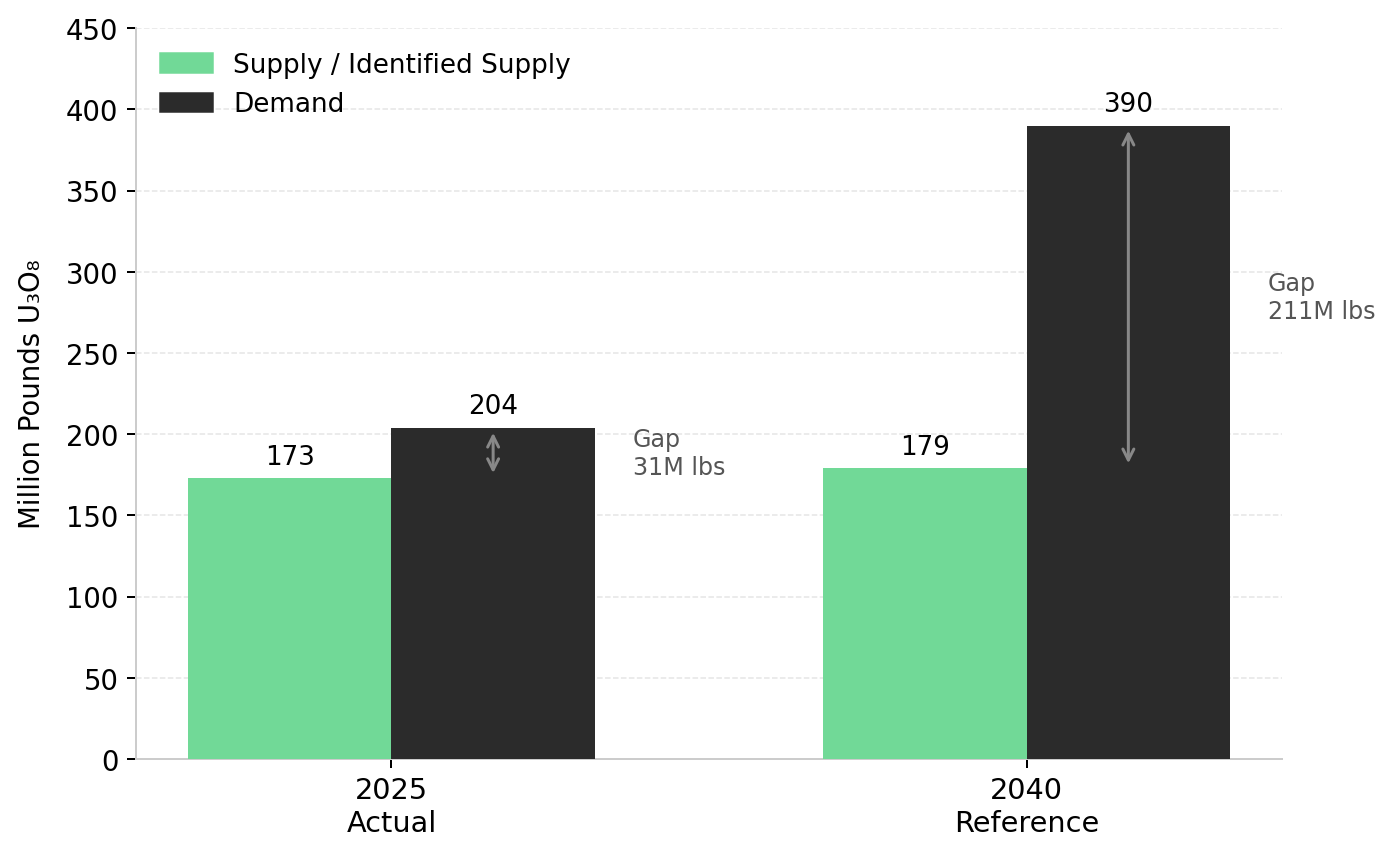

- World uranium production of approximately 173 million pounds in 2025 fell short of the 204 million pound primary demand, leaving a 31 million pound deficit covered by secondary supply.

A Supply Chain Under Simultaneous Compression

Kazakhstan's Kazatomprom contributed approximately 38% of global mine output in 2024, giving its production decisions an outsized impact on global supply availability. The company reduced its 2026 production target from 32,777 to 29,697 tonnes of uranium oxide due to insufficient pricing, directly removing forward availability for Western utilities. This constraint is amplified by China importing approximately 70 million pounds of uranium in the most recent reporting period, equating to roughly 40% of world primary production, which redirects significant material away from Western markets. Kazakhstan, Canada, and Namibia account for approximately 75% of global mine output, meaning a production cut from the primary basin reduces forward availability precisely as reactor additions accelerate contracted demand.

The resulting supply constraint places an immediate premium on active domestic production capacity capable of capturing margin expansion. Companies in the production phase, such as enCore Energy Corp. and Energy Fuels Inc., hold a distinct structural advantage over exploration peers during sudden supply shocks. Because these operators already possess licensed processing infrastructure, they can immediately negotiate higher-margin offtake agreements as the long-term contract price reaches $90/lb per Cameco's Supply and Demand Report. This allows current operators to directly capitalize on Kazakhstan's primary supply removal while bypassing the decade-long permitting delays that constrain new market entrants.

The Strait of Hormuz & the Energy Security Premium

The outbreak of hostilities involving Iran in early 2026 caused a short-term spot price decline from $101.41/lb on January 29 to $85.50/lb by February 5, reflecting financial de-risking by capital allocators. Despite this volatility, the World Nuclear Association issued a formal statement on April 10, 2026, calling on all parties to protect civilian nuclear infrastructure following incidents near the Bushehr Nuclear Power Plant, highlighting the fragility of regional energy networks. However, the long-term contract price remained stable at $90/lb throughout April 2026, confirming that the spot market volatility did not alter underlying physical supply-demand fundamentals for utility buyers.

This geopolitical volatility forces utilities to diversify supply sources toward stable African jurisdictions to mitigate Middle Eastern transit risks. Atomic Eagle Ltd. holds the Muntanga Uranium Project in Zambia, a jurisdiction ranking third among African nations in the Fraser Institute's 2024 Annual Survey, positioning the 58.8 million pound JORC resource as a strategic diversification asset. The January 2025 Feasibility Study models the project at a $32.20/lb all-in sustaining cost, generating a $243 million after-tax net present value and a 3.5-year capital payback at a $90/lb uranium price.

Phil Hoskins, Chief Executive Officer of Atomic Eagle, defines the competitive advantage of advancing feasibility-stage assets over greenfield exploration during periods of acute supply insecurity:

"People talk 15 to 20 years to develop a uranium mine from greenfields exploration through to permitting, financing, and construction. We've got a very sound technical platform that's been provided by the feasibility study. So we know it works, we know the recoveries, we know the acid consumption."

Policy Commitments & Capital Deployment

On April 13, 2026, Great British Energy Nuclear formalized a contract with Rolls-Royce SMR utilizing £2.6 billion from the 2025 Spending Review, targeting 1.4 gigawatts of grid power from the mid-2030s. Simultaneously, the United States directed $2.7 billion toward enrichment contracts and launched a Section 232 critical minerals investigation carrying a 180-day update window that could impose price floors on imported material. Furthermore, Cameco Corporation formalized a C$2.6 billion supply agreement with India in March 2026 covering nearly 22 million pounds over nine years, structurally removing available pounds from the spot market and forcing utilities to compete for remaining uncontracted production.

These domestic supply mandates directly benefit operators holding permitted processing infrastructure within the United States capable of delivering critical minerals alongside uranium. Energy Fuels Inc. operates the White Mesa Mill in Utah, holding the only United States Nuclear Regulatory Commission license to process uranium-bearing monazite at a commercial scale. The facility targets 1.5 to 2.5 million pounds of uranium production in 2026, generating approximately $157.5 million in implied revenue at the midpoint using a $90/lb long-term contract price, while simultaneously advancing a Phase 2 rare earth expansion targeting 6,000 tonnes per annum of neodymium-praseodymium oxide.

Mark Chalmers, outgoing Chief Executive Officer of Energy Fuels, defines the specific operational barrier to entry that protects this critical minerals moat from new market competitors:

"I think what people are seeing is that we've got this critical mass with those steps and they don't just happen overnight. You really have to acquire those skills. You can't just grow them organically because it will take years."

The Structural Supply Gap & Grade Scarcity

World uranium production reached approximately 173 million pounds in 2025, falling 31 million pounds short of the 204 million pound primary demand and forcing drawdowns from secondary supply stockpiles. Furthermore, the World Nuclear Association projects a 2040 reference demand of 390 million pounds against 179 million pounds of identified supply, leaving a 212 million pound residual gap that requires significant new mine development. Compounding this deficit, Wells Fargo estimates that artificial intelligence data center growth will add approximately 323 terawatt-hours of United States electricity demand by 2030, presenting a baseload-intensive load that nuclear power is uniquely positioned to serve at capacity factors above 90%.

This long-term deficit necessitates the advancement of high-grade deposits capable of replacing depleted legacy mines with favorable unit economics. IsoEnergy Ltd. controls the Hurricane deposit in Saskatchewan, containing 48.6 million pounds Indicated at 34.5% uranium oxide, and confirmed new mineralization up to 560 meters along strike east of the resource footprint during its 2026 winter program. Additionally, the company initiated a 2,000-tonne bulk sampling program at the Tony M Mine in Utah demonstrating uranium recovery exceeding 90%, utilizing toll milling access to save more than $1 million in permitting costs versus greenfield development alternatives.

Philip Williams, Chief Executive Officer of IsoEnergy, quantifies the procurement pressure accumulating as utilities address this looming structural supply cliff:

"When you look at demand doubling or more by 2040 and no real understanding of where the supply is coming from, prices I think do have to stay higher for longer in order to incentivise that. Western utilities are behind and they're going to have to be scrambling to play a game of catch-up."

Basin-Scale Exploration & The 2040 Supply Gap

While active producers capture near-term pricing premiums, resolving the projected 212 million pound residual gap by 2040 per the WNA's 2025 Nuclear Fuel Report requires advancing basin-scale exploration assets. ATHA Energy Corp. controls 6.8 million acres across Canada's most prominent uranium basins, deploying three simultaneous diamond drill rigs funded by a CAD $63 million treasury closed in February 2026. This program targets follow-up on the RIB North maiden hole that returned 34.7 meters of composite mineralization grading up to 8.16 percent uranium oxide over 0.5 meters. Establishing a compliant mineral resource estimate serves as the primary de-risking milestone for this capital deployment.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, categorizes the urgency driving exploration capital into reliable North American jurisdictions as long-term supply tightens:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career. The sentiment, the real demand that's being built up, coupled with some of the supply-side risk, is a structural setup like we have not seen in the uranium space."

Domestic Production & The In-Situ Recovery Imperative

The 116 million pounds of utility contracting executed in 2025 marks the 13th consecutive year that procurement fell below the 150 million pound annual replacement rate. Resolving this chronic under-contracting requires immediate offtake agreements with active, low-cost domestic producers capable of scaling near-term output to bridge the gap before new conventional mines can be permitted and constructed. If the current administration implements a Section 232 price floor for utility procurement, it will directly raise the minimum clearing price in the market and materially improve the project economics of existing domestic operators.

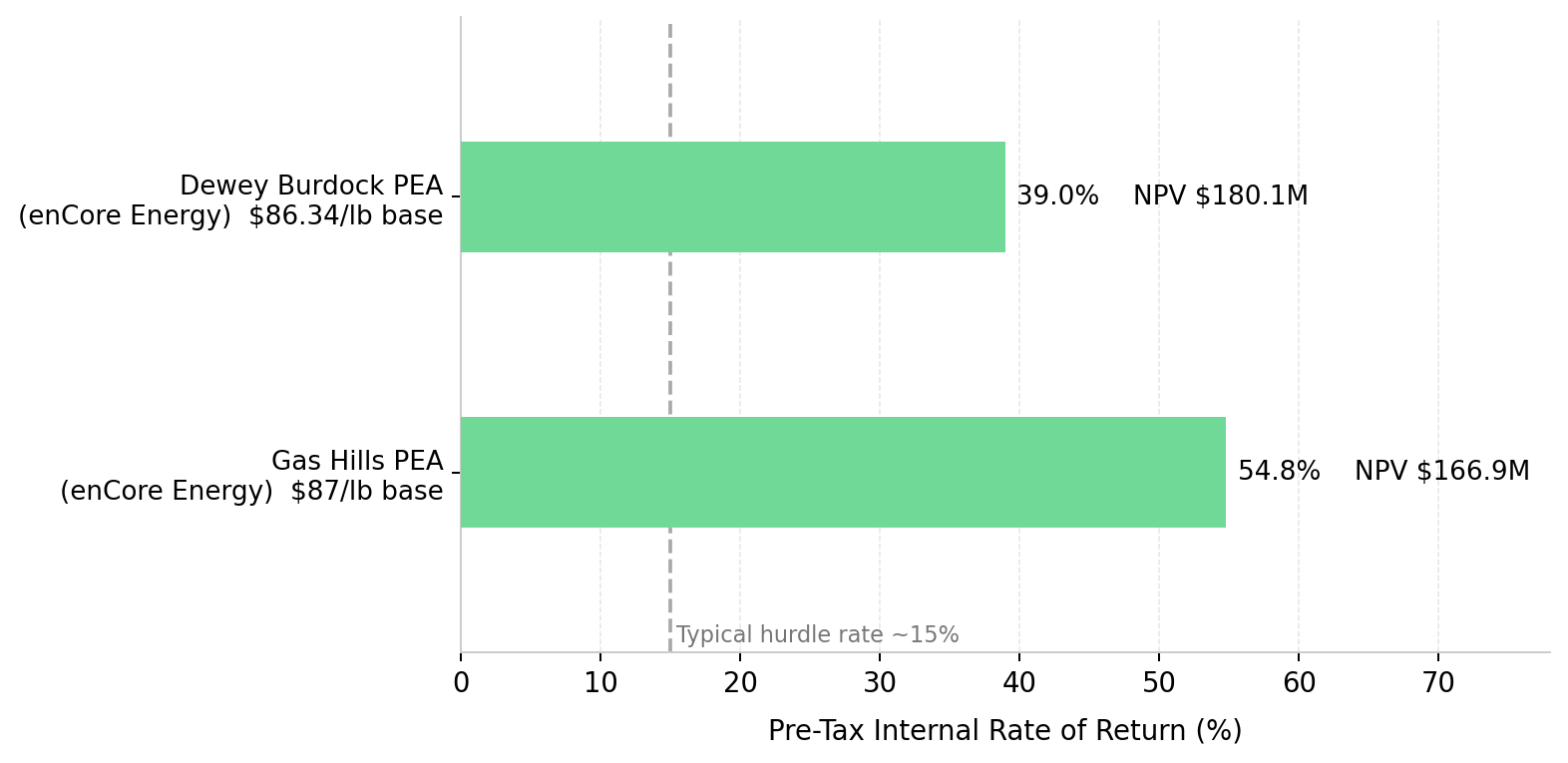

Active in-situ recovery producers present the most direct pathway to addressing domestic shortfalls while capturing these pricing premiums. enCore Energy Corp. operates the Rosita and Alta Mesa central processing plants in South Texas at a Q3 2025 production cost of approximately $38/lb against a $68.28/lb contract price. Furthermore, the company published preliminary economic assessments for the Dewey Burdock and Gas Hills projects projecting pre-tax internal rates of return of 39.0% and 54.8%, respectively, with net present values exceeding $166 million at base-case pricing well below current spot levels.

William Sheriff, Executive Chairman of enCore Energy, establishes the operational and financial thresholds required for viable domestic in-situ recovery operations to attract institutional capital:

"In terms of the ISR business, you're going to have to have some producers that produce more than a million pounds a year or you're going to be essentially running a mom-and-pop grocery store on the corner. You need to have several billion market cap and you're not going to do that with a million pounds a year production."

The Investment Thesis for Uranium

- Structural supply deficits require sustained long-term incentive pricing above current $90/lb levels to finance the new mine development necessary to satisfy projected 2040 demand.

- Jurisdictions offering transparent permitting frameworks and origin-assured material capture a premium valuation as Western utilities prioritize supply chain security over pure cost competition.

- Producers holding licensed, operational processing infrastructure possess a critical competitive advantage by bypassing the decade-long permitting delays that constrain greenfield developments.

- Development-stage assets demonstrating pre-tax internal rates of return above 30% at current long-term contract pricing provide high-leverage exposure to the ongoing utility procurement cycle.

- Exploration portfolios funded by robust treasuries without the need for immediate dilutive financing present risk-adjusted discovery optionality within proven mineralized basins.

- Asset portfolios resilient to geopolitical shocks and integrated with domestic policy mandates attract steady institutional inflows as governments mandate critical mineral independence.

Kazakhstan's deliberate 10 percent production cut removes approximately 8 million pounds of forward supply from a market already facing a 31 million pound primary deficit in 2025 per UxC data. Concurrently, utilities are ending a 13-year cycle of deferred procurement where annual contracting fell below the 150 million pound replacement rate per Cameco's Supply and Demand Report. This physical shortfall forces utility buyers to secure origin-assured contracts at elevated incentive prices to maintain uninterrupted power generation.

Closing the 212 million pound residual gap by 2040 requires utility capital commitments at contract prices above the current $90/lb level. Investors capture this mandated capital inflow by allocating funds toward producers operating licensed domestic infrastructure. Developers publishing quantified feasibility economics and explorers advancing fully funded drill programs provide risk-adjusted leverage to these rising contract rates. These specific asset classes are financially positioned to capture margin expansion as the structural deficit forces utilities to sign contracts at higher market-clearing prices.

TL;DR

Kazakhstan's deliberate 10% uranium production cut and Western sovereign capital commitments, including £2.6 billion toward United Kingdom small modular reactors and $2.7 billion in United States enrichment contracts, compress the procurement deferral window for utilities that have under-contracted for 13 consecutive years. The long-term contract price reaching $90/lb, combined with a 31 million pound 2025 supply deficit, establishes the structural necessity for sustained higher incentive pricing to clear the market. Equity investors capture this macro repricing through producers controlling licensed United States processing infrastructure, developers holding advanced feasibility studies, and explorers advancing basin-scale land packages in tier-one jurisdictions.

FAQs (AI-Generated)

The spot price reflects near-term transactional activity influenced by financial buyers, fund flows, and short-term sentiment, demonstrated by the $101.41/lb peak in January 2026 followed by a 16% pullback within seven days on geopolitical risk-off conditions per Investing News Network. The long-term contract price reflects the price at which utilities sign multi-year supply agreements covering fuel requirements years into the future. When the long-term price reaches $90/lb, its highest level since 2008 per Cameco's Supply and Demand Report, it signals that utilities accept higher incentive prices to secure supply, establishing the benchmark that determines whether a project's internal rate of return and net present value justify construction capital.

Kazakhstan's Kazatomprom supplies approximately 38% of global uranium mine output and, together with Canada and Namibia, accounts for approximately 75% of world production per the WNA's 2025 Nuclear Fuel Report. A deliberate 10% cut removes roughly 8 million pounds, or approximately 5% of global primary supply, from 2026 availability. The impact on Western buyers is compounded by December 2025 legislative amendments eliminating the incentive structure for private greenfield exploration within the basin, ensuring future supply growth from the world's largest uranium-producing geography remains constrained for years. China's concurrent import of approximately 70 million pounds, roughly 40% of world primary production, further reduces the pool of Western-aligned material per Investing News Network's Q1 2026 Uranium Price Review.

Section 232 of the Trade Expansion Act of 1962 authorizes the United States President to impose tariffs or price floors on imports that threaten national security. Uranium was excluded from the April 2, 2026 tariff package but is explicitly included in the ongoing critical minerals investigation, carrying a 180-day update window per Sprott's February 2026 Uranium Report. If the administration implements a price floor for utility procurement of domestically produced or Western-allied uranium, it would raise the minimum clearing price in the United States market and materially improve the project economics and contract pricing power of domestic in-situ recovery producers and allied-jurisdiction developers.

The uranium investment opportunity is not uniform across development stages. Active in-situ recovery producers with licensed processing facilities offer direct exposure to current uranium prices and contract revenues but face permitting timelines that constrain near-term production growth. Dual-commodity producers with processing infrastructure combine uranium revenue with rare earth element optionality underpinned by a regulatory licensing position no United States competitor currently replicates. Advanced developers with globally significant grade assets offer leverage to uranium price increases through resource quality without requiring full production-stage capital costs. Feasibility-stage developers provide quantified project economics at defined uranium price assumptions. Basin-scale explorers offer maximum optionality but carry the greatest geological and timeline uncertainty pending a first compliant resource estimate.

According to the World Nuclear Association's 2025 Nuclear Fuel Report, total identified supply from all sources covers approximately 46% of 2040 reference demand, leaving a residual gap of approximately 212 million pounds. This gap begins compounding in the early 2030s as existing high-volume mines plateau and secondary supply sources, including stockpiles and reprocessed material, are progressively depleted. Closing the gap requires sustained long-term incentive pricing above current levels to justify the capital required to bring new mines into production, combined with accelerated utility contracting to provide the revenue visibility project financiers require before committing construction capital. Because a uranium mine typically requires 10 to 20 years from greenfield exploration to first production, capital deployment decisions required today to close the 2035 gap are already overdue.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed