Kazatomprom's Production Shock: A Structural Repricing Catalyst in Uranium Markets

Kazatomprom’s 2025 production cut exposes uranium’s fragile supply chain, accelerating a structural repricing as demand outpaces new mine development globally.

- Kazatomprom's updated 2025 production guidance (~20% below prior expectations) exposes a structurally fragile uranium supply chain.

- Demand growth from electrification and energy security policies is colliding with decade-long underinvestment in new uranium capacity.

- Uranium price softness (-15.5% YoY) may mask tightening fundamentals, creating asymmetric upside for low-cost, near-term producers.

- US and Canadian juniors in stable jurisdictions with shovel-ready or high-grade projects are poised to benefit from rising security-of-supply premiums.

- Investors should assess jurisdictional advantage, asset readiness, and exploration leverage when allocating to uranium equities amid geopolitical volatility.

Decarbonization to Defense: Uranium's Return to Strategic Commodity Status

The post-Fukushima decade witnessed a systematic dismantling of nuclear capacity across developed markets, with Germany's complete phase-out and Japan's reactor shutdowns creating a sustained bear market in uranium. This period of underinvestment coincided with the emergence of two transformative trends: the acceleration of decarbonization mandates requiring 24/7 clean baseload power and the development of small modular reactor (SMR) technology promising safer, more flexible nuclear deployment. The convergence of climate imperatives and energy security concerns following Russia's invasion of Ukraine has catalyzed a fundamental reassessment of nuclear power's role in the global energy mix.

The production cut from the world's dominant uranium supplier has intensified focus on alternative supply sources, particularly as companies like ATHA Energy, IsoEnergy, Energy Fuels, and Global Atomic demonstrate differentiated exposure to high-grade, low-cost, or near-term production capabilities. With uranium prices stabilizing after a brief 5% correction, the long-term fundamentals support sustained institutional positioning in nuclear-linked assets across the development spectrum.

Supply Shock Dynamics: Why Kazatomprom's Cut Matters

Kazakhstan's dominance in global uranium production, accounting for approximately 40% of primary supply, means any variance in Kazatomprom's output reverberates through the entire nuclear fuel cycle. The 20% production cut translates to roughly 5,000-6,000 metric tons of U₃O₈ annually, equivalent to removing Canada's entire production from the market. This disruption arrives as utilities extend fuel procurement horizons from 3-5 years to 7-10 years, creating competitive dynamics that favor security of supply over price optimization.

The structural nature of Kazatomprom's challenges reflects broader constraints across the uranium mining sector. A decade of prices below incentive levels has resulted in chronic underinvestment in exploration, development, and even sustaining capital at existing operations. The World Nuclear Association's assessment that current mine development pipelines are insufficient to meet projected demand growth through 2040 understates the challenge, lead times for new uranium projects typically span 10-15 years from discovery to production, creating an unbridgeable gap between supply capacity and demand growth.

The market impact extends beyond immediate supply availability to reshape contracting dynamics fundamentally. Long-term contract prices, historically trading at modest premiums to spot, now incorporate scarcity premiums of 20-30% as utilities prioritize supply security over price optimization.

Supply Chain Concentration & Investment Risk

The geographic concentration of uranium production in Kazakhstan, Niger, and Russia, collectively representing over 60% of global supply, intersects with deteriorating geopolitical stability to create unprecedented supply chain risks. The US ban on Russian uranium imports (H.R.1042) removes approximately 20% of American nuclear fuel supply, while political instability in Niger threatens another 5% of global production. European utilities face similar constraints as they navigate energy security mandates requiring supply diversification away from Russian sources.

This creates explicit value for production from stable jurisdictions. ATHA Energy's strategic positioning in Canada's Nunavut territory exemplifies this opportunity. The company's recent drilling success at its Angilak project, where CEO Troy Boisjoli notes:

"We have hit mineralization in the first hole along a 31 km long trend"

This demonstrates the exploration potential in underexplored regions of politically stable countries. The company's careful attention to stakeholder engagement, including agreements with Nunavut Tunngavik Incorporated, positions it to benefit from the premium utilities will pay for socially licensed, geopolitically secure uranium sources.

The Risk Premium of Production Reliability

Traditional discounted cash flow models fail to capture the evolving risk dynamics in uranium markets, where security of supply increasingly trumps cost considerations. The repricing of uranium assets must incorporate not just commodity price assumptions but also reliability premiums that vary dramatically by jurisdiction and project maturity. Assets in tier-one jurisdictions, particularly Canada, Australia, and the United States, now command valuation multiples 30-50% higher than comparable projects in traditional producing regions like Niger or Kazakhstan.

This risk-adjusted valuation framework particularly benefits companies with proven operational track records and near-term production visibility. Production guidance volatility from major suppliers erodes market confidence, creating a flight to quality that rewards execution certainty over exploration upside. The market's willingness to pay premium valuations for de-risked projects reflects hard-learned lessons from previous cycles where promising deposits failed to achieve commercial production due to technical, political, or social challenges.

IsoEnergy's Hurricane deposit epitomizes the attributes commanding premium valuations: exceptional grade, tier-one jurisdiction, and proximity to existing infrastructure. As COO Marty Tunney emphasizes:

“Hurricane represents the highest grade uranium deposit in the world with indicated resources grading 34% U₃O₈, located just 40 kilometers from Orano's McClean Lake Mill”

This combination of grade, location, and infrastructure access creates a risk-adjusted return profile that justifies premium valuation multiples despite the project's pre-development status.

Mismatch Between Long-Term Demand & Project Pipeline

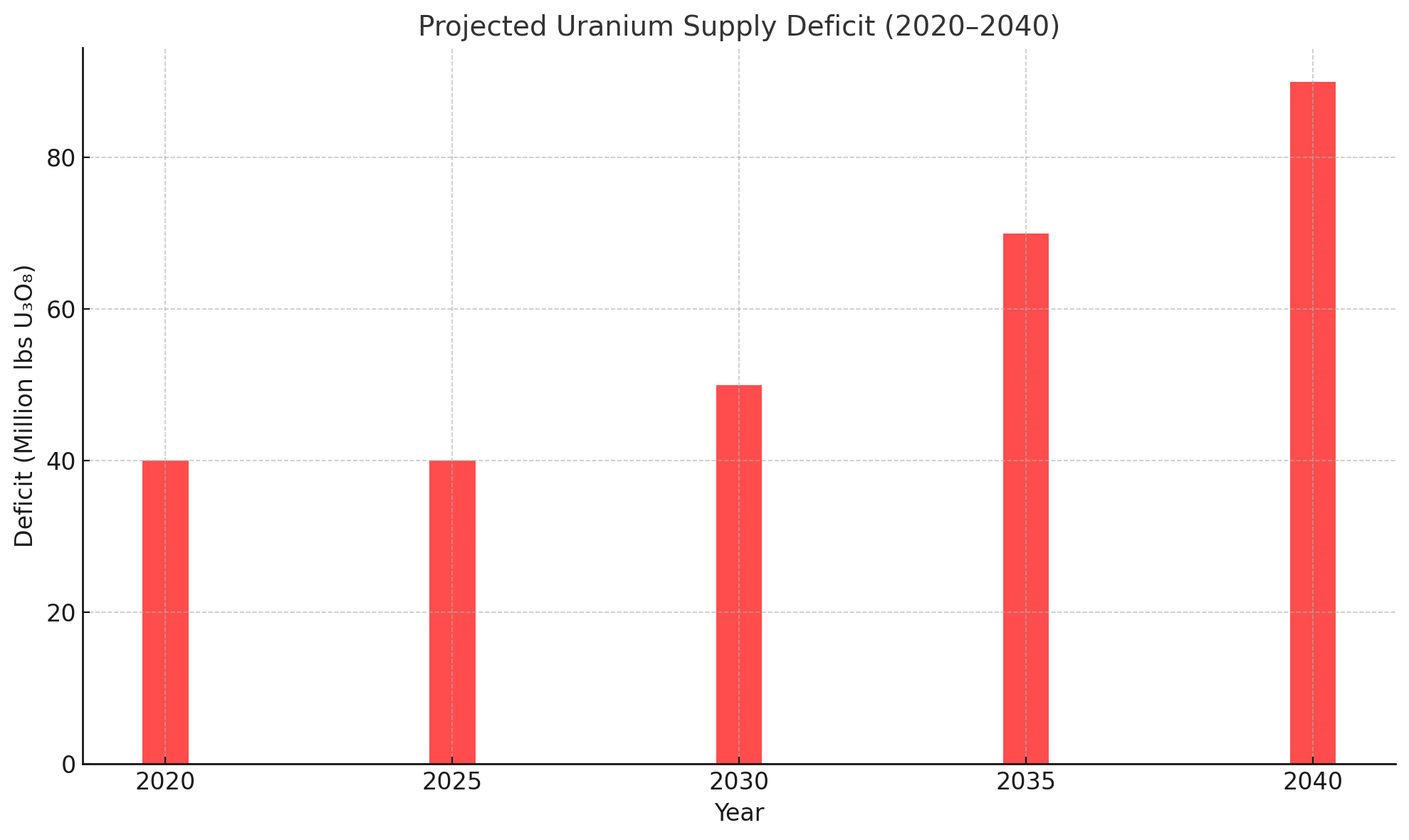

The structural supply deficit emerging in uranium markets stems from a fundamental temporal mismatch between demand growth and supply response capability. The World Nuclear Association's projection of tripling nuclear capacity by 2050 requires annual uranium demand to reach approximately 200 million pounds, compared to current production of 140 million pounds. This 43% increase in production must occur despite a development pipeline that falls far short of replacement requirements, let alone growth.

The challenge extends beyond raw production capacity to include the entire nuclear fuel cycle infrastructure. Conversion and enrichment facilities operate at high utilization rates with limited expansion capability, creating additional bottlenecks that amplify the impact of mining supply constraints. The 10-15 year development timeline for new uranium mines means that projects must advance to construction decisions by 2030 to contribute meaningfully to supply before 2040.

This temporal mismatch creates extraordinary value for companies with near-term production capability or advanced development projects. The ability to deliver pounds into a structurally undersupplied market commands premium valuations that extend well beyond traditional net asset value calculations.

Capex Discipline, Inflation Risk, & Investor Return Profiles

The post-pandemic inflationary environment has fundamentally altered project economics across the mining sector, with uranium projects experiencing particular pressure due to specialized equipment and skilled labor requirements. Capital cost inflation of 30-50% since 2020 has pushed marginal projects below investment thresholds, concentrating development capital on high-grade, low-risk opportunities. This capital discipline, while constraining near-term supply additions, creates favorable conditions for companies with existing infrastructure or low-capital restart opportunities.

Successful navigation of this environment requires innovative approaches to capital deployment. Companies pursuing phased development strategies, toll milling arrangements, or restart opportunities can achieve production with a fraction of greenfield capital requirements. The internal rate of return (IRR) differential between restart projects (often exceeding 100%) and new builds (typically 20-40%) drives capital allocation decisions increasingly focused on near-term, low-capital opportunities.

Energy Fuels exemplifies this capital-efficient approach through its integrated strategy leveraging the White Mesa Mill's dual capacity for uranium and rare earth processing. CEO Mark Chalmers articulates the company's differentiated strategy:

"We're not pretenders, we're building a company, we're not building a promotion.”

By utilizing existing infrastructure and focusing on near-term production from fully permitted mines like Pinyon Plain, Energy Fuels minimizes capital requirements while maintaining significant leverage to uranium price appreciation. The company's ability to operate "campaigns of uranium, campaign of rare earth" provides operational flexibility and multiple revenue streams from a single capital base.

Rebalancing Risk in Institutional Portfolios

Institutional capital allocation to uranium reflects broader portfolio rebalancing toward commodities with structural supply deficits and policy support. The sector's inclusion in ESG mandates, nuclear power prevents 2.5 billion tons of CO₂ emissions annually, has expanded the investor base beyond traditional resource funds to include pension funds, sovereign wealth funds, and clean energy-focused allocators. This diversification of capital sources provides more stable funding for project development while reducing the sector's historical reliance on volatile retail flows.

The emergence of physical uranium trusts and sector-specific ETFs has created additional investment vehicles that directly impact market dynamics. These funds, holding approximately 60 million pounds of physical uranium, represent nearly six months of global consumption removed from market availability. This financialization creates a positive feedback loop where rising uranium prices drive fund inflows, further tightening physical markets and supporting equity valuations.

Near-Term Leverage to a Contracting Upswing

Kazatomprom's production announcement has intensified contracting urgency among utilities, creating immediate opportunities for projects with signed offtake agreements and clear production timelines. Global Atomic's Dasa project in Niger stands as the only fully permitted greenfield uranium development currently under construction globally, with four offtake agreements already in place, including three with US utilities.

The project's economic profile demonstrates the potential returns available in today's uranium market, with a $308 million capital expenditure generating a 57% internal rate of return at $75 per pound uranium, escalating to 92.9% IRR at $105 per pound.

Jurisdictional Arbitrage in a Fragmented Supply Landscape

The transformation of uranium from commodity to strategic asset has created distinct valuation tiers based on jurisdictional risk. Tier-one jurisdictions, Canada, Australia, and increasingly the United States, capture valuation premiums reflecting both geological prospectivity and political stability. The US Inflation Reduction Act's provisions for domestic uranium production, including tax credits and purchase guarantees, exemplify policy support translating directly to project economics.

Canada's dominant position in high-grade uranium resources, combined with established regulatory frameworks and social acceptance, positions Canadian developers optimally for the emerging market structure. ATHA Energy's systematic exploration across multiple Canadian provinces demonstrates the value creation potential in underexplored districts. The company's drilling success at Angilac, achieving "100% hit rate" in expanding mineralization footprints, validates the geological model while their CMB discovery opens an entirely new uranium district.

The US market presents unique opportunities given government support for domestic production and existing infrastructure. The ability to leverage facilities like Energy Fuels' White Mesa Mill, the only operating conventional uranium mill in the United States, creates competitive advantages for companies with nearby resources.

Permit-Led Timelines & the Value of Shovel-Ready Assets

Permitting represents the critical constraint in uranium project development, with timelines varying from 2-3 years in established mining jurisdictions to indefinite delays in jurisdictions with evolving regulatory frameworks. The value differential between permitted and pre-permit projects has widened dramatically, with permitted projects trading at 2-3x the valuation multiples of exploration-stage peers.

IsoEnergy's strategic acquisition of permitted, past-producing mines in Utah demonstrates the value capture potential in acquiring de-risked assets. COO Marty Tunney notes:

“Well over $100 million was spent in capex on these projects, which IsoEnergy acquired for a fraction of replacement cost.”

With permits intact and a toll milling agreement with Energy Fuels' White Mesa Mill, IsoEnergy can achieve production in 2025 with minimal capital expenditure. This near-term production capability, while developing the world-class Hurricane deposit in parallel, exemplifies optimal capital allocation in the current market environment.

The toll milling arrangement between IsoEnergy and Energy Fuels highlights the value of vertical integration and infrastructure sharing in capital-constrained markets. By utilizing existing processing capacity, junior producers can achieve economics that would be impossible with standalone operations, while mill operators benefit from increased throughput and diversified feed sources.

Building Portfolios for Structural Scarcity

Optimal portfolio construction in uranium markets requires balancing exposure across the risk-return spectrum while maintaining focus on structural supply deficit themes. Physical uranium exposure through trusts like Sprott Physical Uranium provides direct commodity exposure without operational risk, while equity positions offer leveraged returns to rising prices. Within equities, a barbell approach combining near-term producers with advanced developers captures both immediate cash flow generation and development upside.

The sector's unique characteristics, including long-term contracting dynamics, binary development outcomes, and significant operational leverage, demand sophisticated risk management. Diversification across jurisdictions, development stages, and corporate strategies mitigates single-asset risk while maintaining thematic exposure. Companies demonstrating multiple paths to value creation, such as Energy Fuels' uranium-rare earth integration or IsoEnergy's near-term production plus development pipeline, warrant overweight positions relative to single-asset stories.

ESG Integration & Permitting Readiness

Environmental, social, and governance considerations have become integral to uranium investment decisions, with investors favoring assets that demonstrate clear compliance pathways and community engagement frameworks. Global Atomic's EP4 environmental compliance, ATHA's Indigenous partnership agreements, and Energy Fuels' mine cleanup and restoration partnerships exemplify the governance standards now expected by institutional capital.

The Investment Thesis for Uranium

- Exposure to multi-decade nuclear demand growth supported by institutional policy shifts (World Bank, WNA), with nuclear capacity required to triple by 2050 to meet decarbonization targets.

- Scarcity premium for high-grade, tier-one jurisdiction assets like those of IsoEnergy (Hurricane at 34% U₃O₈) and ATHA Energy (Angilac with expanding high-grade footprint in stable Canada).

- Operational leverage from permitted and producing infrastructure at Energy Fuels' White Mesa Mill, providing immediate production capability with minimal capital requirements.

- Exploration catalysts and resource expansion potential across Canadian and US portfolios, with ATHA Energy's 100% drilling success rate and new district discovery validating untapped potential.

- Alignment with US policy incentives and global supply chain realignment away from high-risk regions, creating explicit premiums for North American production.

- Strategic optionality through existing infrastructure, toll milling agreements between IsoEnergy and Energy Fuels, and future M&A potential as the sector consolidates.

- Cost discipline and low debt positioning amid inflationary capital environments, with companies like IsoEnergy maintaining $50 million cash positions for opportunistic development.

- Favorable long-term contracting dynamics with utilities extending contract tenors and accepting 20-30% premiums for secure supply, supporting sustained price appreciation. Global Atomic represents the only fully permitted greenfield development project globally, with established long-term offtake agreements providing revenue certainty in a rising price environment.

Kazatomprom's 20% production cut crystallizes a structural reality that will define uranium markets for the next decade: the collision of accelerating demand with constrained supply creates an asymmetric investment opportunity rarely seen in commodity markets. This is not merely another cyclical upturn but a fundamental repricing of uranium from industrial commodity to strategic asset. The convergence of decarbonization imperatives, energy security concerns, and chronic underinvestment has created conditions where even optimistic supply scenarios fall short of baseline demand projections.

For investors, the uranium sector offers a compelling combination of policy support, structural supply deficits, and clear beneficiaries positioned to capture value through the transition. Companies with tier-one jurisdiction assets, near-term production capability, and operational flexibility stand to generate exceptional returns as the market re-prices to reflect physical scarcity.

The window for positioning ahead of this structural shift remains open, but narrowing as utilities compete for limited supply and financial buyers accumulate physical inventory. In a world demanding reliable, carbon-free baseload power, uranium's transition from overlooked commodity to strategic asset represents one of the most compelling macro investment themes of the decade.

Analyst's Notes

Subscribe to Our Channel

Stay Informed