Kuya Silver Eyes Profitability as Mill Acquisition and Production Ramp Converge in Peru

Kuya Silver nears first profitable quarter as $9M Camila mill purchase closes, new underground ramp advances, and drilling resumes after five-year hiatus.

After years of careful capital allocation and steady progress at its Bethania Silver Mine in central Peru, Kuya Silver is approaching an inflection point that CEO David Stein believes the market has yet to fully recognise.

The company is on track to deliver its first profitable quarter within the next two reporting periods. That milestone hinges on the imminent closure of a $9 million acquisition that eliminates a longstanding operational vulnerability: third-party toll milling.

In January, Kuya announced an agreement to purchase the Camila processing facility outright, with closing expected before month-end. The 350-tonne-per-day plant sits 150 kilometres from the mine, positioned conveniently on the route to the port where concentrate is sold. More significantly, it's connected to the hydro grid - translating into cleaner, cheaper power that partially offsets the cost of hauling ore. Stein explained during a recent interview at PDAC,

"When you're operating with a third party, you just don't know if they're going to mess it up. Having that [Camila] under our control with real top professional management is worth something to us."

The financial logic is straightforward. Cost savings from eliminating toll fees carry a roughly five-year payback. But the strategic value runs deeper. Owning the mill opens the door to third-party processing revenue from smaller regional miners - creating both incremental cash and potential deal flow in a district that has seen little modern consolidation.

Unlocking Underground Throughput

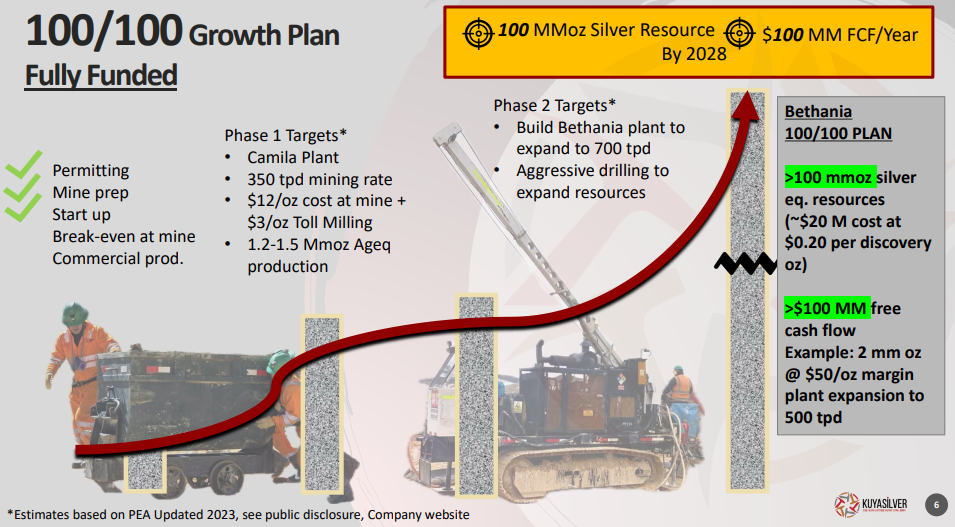

With approximately $15 million on the balance sheet following the acquisition and a $23.5 million January financing, Kuya has earmarked $3 million for two critical projects: underground drilling and a new ramp.

The ramp addresses a legacy bottleneck. Bethania currently relies on a horizontal adit serving upper levels and a 45-degree decline fitted with a rail-and-winch system. Functional, but inefficient. The new ramp will enable vehicle access and provide the infrastructure backbone to eventually scale throughput to 750 or even 1,000 tonnes per day in later phases.

More immediately, drilling has resumed after a five-year pause. Two underground rigs are now targeting a 50-metre vertical extension below the existing resource. Stein estimates that every 10 metres drilled should yield roughly one million ounces based on the grade profile above. A 200-metre vertical push could add up to 20 million ounces of inferred material.

That drilling hiatus wasn't accidental. Kuya deliberately funneled what capital it had into production rather than exploration - a discipline that's now paying off as the company shifts into expansion mode.

Interview with David Stein, President & CEO of Kuya Silver

The District Play

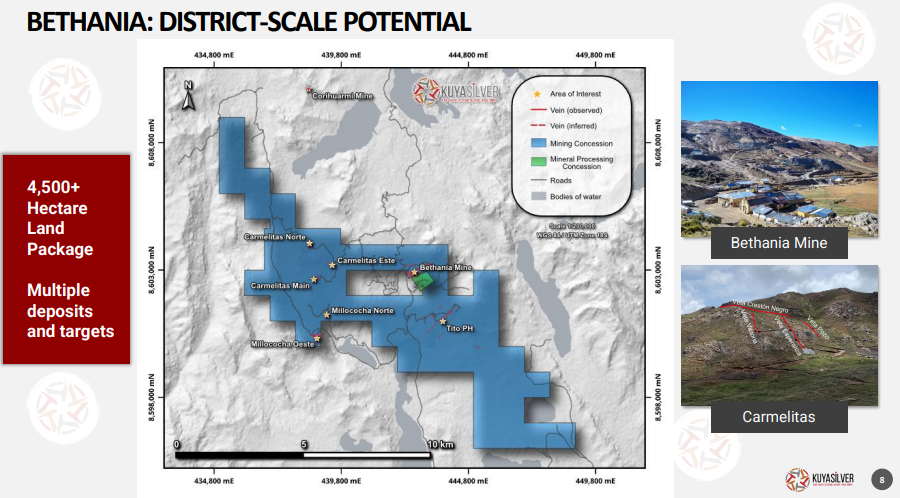

The real exploration story sits outside the mine fence. Kuya's land position has ballooned from 45 hectares to 4,500 - a hundredfold expansion. Surface work has identified six additional silver vein systems within five kilometres of Bethania, all tied to old artisanal workings.

The current resource - 4.3 million indicated ounces and 5.6 million inferred - occupies less than 0.3% of that land package. Recent sampling at targets like Millococha Oeste and Carmelitas has returned grades north of 2,000 grams per tonne silver equivalent, signaling the district's broader potential.

"The goal is to get the resource up to 100 million ounces of silver. We feel very strongly we can do that in the next three years."

A surface rig is slated for Q3, with a second potentially following by year-end. Management's longer-term vision involves two processing facilities running in parallel by 2028 - Camila and a future Bethania plant - producing around three million ounces annually. The Bethania plant design is already permitted; construction would be funded from operating cash once Camila is optimised.

Re-Rating on the Horizon

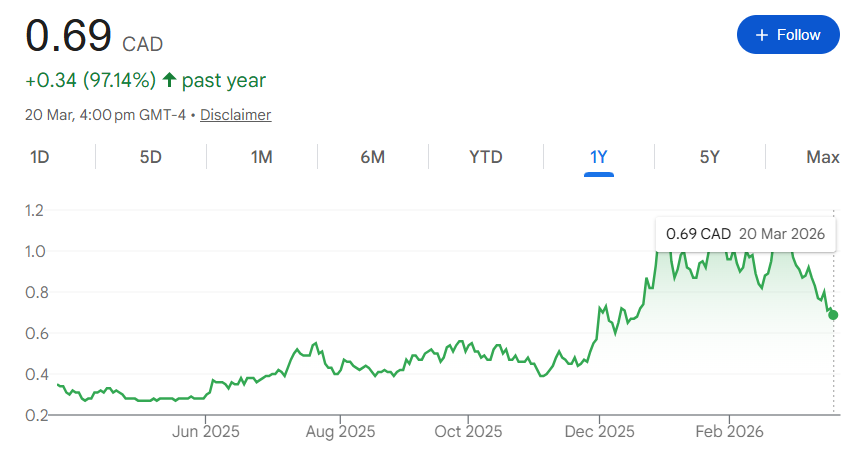

Kuya's share price has nearly doubled over the past year, climbing 97% to CAD$0.69 by late March. Yet Stein argues the company still trades at a discount to peers that have crossed into sustained profitability.

"With these silver prices, dare I say, this is going to generate a shocking amount of cash flow by the end of this year."

At current silver levels, the first profitable quarter should act as a catalyst. Comparable producers with demonstrated cash generation trade at materially higher multiples. Kuya derives roughly 90% of its revenue from silver - a relatively pure exposure in a market where most production comes as a byproduct of base metals mining. That structural supply constraint, combined with durable industrial demand from solar and electrification, has kept the silver price environment constructive.

The company also holds optionality in Ontario's historic Cobalt district, where recent drilling at its Silver Kings project intersected bonanza-grade mineralisation - 15,372 grams per tonne silver over 3.34 metres. It's early-stage, but it diversifies the portfolio geographically and offers another avenue for resource growth.

What Comes Next

Kuya enters the end of Q1 with the operational pieces aligned: the Camila acquisition closing imminently, the underground ramp under construction, and two drill rigs turning. The company is funded through this phase without needing to tap equity markets, and the first profitable quarter is no longer a theoretical milestone - it's a reportable event that's one or two quarters away.

For a company that spent years navigating capital constraints and building production credibility, that's meaningful progress. The challenge now is execution. If Kuya delivers on the near-term plan and the drill bit cooperates on resource expansion, the re-rating Stein anticipates may prove justified. The market tends to reward clarity - and for the first time in Kuya's history, the path from here to sustainable cash generation is unusually clear.

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

Stay Informed