Marimaca Copper Targets End-2026 Build-Readiness as Detailed Engineering and Senior Hiring Advance

Marimaca Copper is advancing toward a construction decision on its flagship oxide deposit while managing the organisational risks that most builders confront too late.

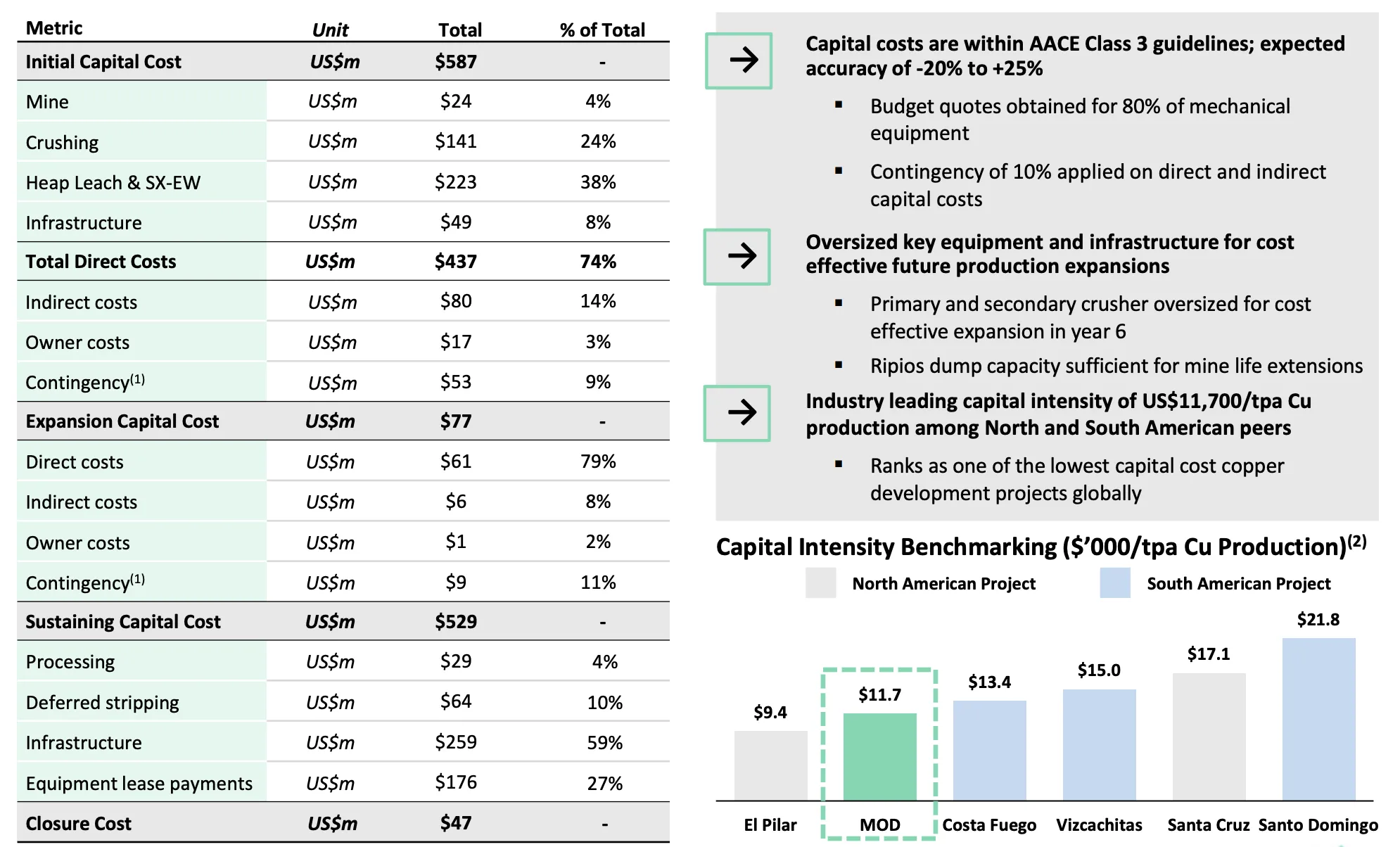

- Marimaca Copper is targeting build-readiness for the Marimaca Oxide Deposit (MOD) by the end of 2026, with a pre-production capital cost of just under US$600 million and a post-tax net present value at an 8% discount rate (NPV8%) of US$1.1 billion at a 39% internal rate of return (IRR) at US$5.05 per pound copper.

- The company is actively hiring for the senior execution team required to lead the build phase, with capital discipline and cultural fit as primary selection criteria, alongside technical qualifications.

- Management has identified operability over engineering elegance as the governing design principle, explicitly separating decisions that reduce capital expenditure (capex) from those that increase operational risk.

- Budget quotes have been obtained for 80% of mechanical equipment, with a final investment decision (FID) targeted in the second half of 2026.

- The company holds a US$165.6 million cash position and zero debt, providing runway to reach FID without near-term equity dilution while continuing a 100,000-metre drill program at Pampa Medina.

What Has Happened

Marimaca Copper (TSX: MARI, ASX: MC2) completed its Definitive Feasibility Study (DFS) for the Marimaca Oxide Deposit (MOD) in 2025 and received Environmental Approval (EA) in November 2025. The company is now in the engineering maturation and team-building phase that precedes a construction decision, targeting a final investment decision (FID) in the second half of 2026. In April 2026, Marimaca released consolidated silver assay results from all Pampa Medina drilling, confirming silver mineralisation as a deposit-wide feature broadly correlated with copper grade across a 3-kilometre by 2-kilometre area of interest. These developments indicate a shift from de-risking toward execution preparation. At this stage, geological and permitting risks have been largely addressed, while execution and delivery risks have become more prominent.

Engineering Discipline Begins Before the First Shovel

Most discussions of mining project risk focus on geology, permitting, or commodity prices. However, cost overruns and delays are often driven earlier in the process, in decisions made during detailed engineering and in the organisational culture that determines how quickly issues are identified and escalated.

Marimaca has identified operability as a key design constraint for the build phase. The principle distinguishes between technically optimal designs and those that can be reliably operated in practice.

Chief Executive Officer and President of Marimaca Copper, Hayden Locke, described the tradeoff:

"It's like an architect designing a house. It can be a beautifully designed, architecturally brilliant house which is just not functional. So we've got to find the balance between what is operable."

The practical application of this principle has clear capital implications. Each design change that reduces pre-production expenditure is weighed against the operational risk it introduces. Management gives an example of removing a redundant pump, which might save US$2 million to US$3 million, but that saving is rejected if it materially increases the risk of a plant shutdown. This discipline is being applied systematically throughout the current engineering phase, before the award of construction contracts.

Hiring for Capital Discipline & Organisational Transparency

The hiring process underway at Marimaca is not simply a staffing exercise. Management has identified that the Chilean mining industry carries a cultural tendency to avoid delivering adverse information upward through an organisation - a dynamic that, left unaddressed, converts manageable problems into material ones.

Locke described the culture the company is attempting to build:

"We're trying to create a culture where you don't get in trouble for delivering bad news up. It will be much worse if you don't deliver bad news up."

This framing reflects an emphasis on elevating issues early rather than suppressing adverse information. The senior leaders being recruited are selected in part on their alignment with this expectation. The company has indicated that it is satisfied with the engagement of the candidates identified so far, though the hiring process remains ongoing.

The board appointments announced in March 2026 reflect the same logic applied at the governance level. Zenon Wozniak, formerly Director, Projects at First Quantum Minerals, joined as an Independent Non-Executive Director effective March 27, 2026, and will chair the Project Steering & Technical Committee. Giancarlo Bruno Lagomarsino, a mechanical engineer with 35 years of executive mining management experience in Chile and a former Chief Executive Officer of Mantos Copper SA, was concurrently appointed Independent Non-Executive Chair. Both appointments add direct mine-building and in-country operational experience to the board at the precise stage when construction governance becomes the primary risk variable.

Marimaca is a first-time builder and has stated this as a factor in allowing additional time in 2026 to advance engineering maturity before committing to construction. The objective is to reduce variation between plan and outcome during execution, which is intended to improve capital cost predictability at the project scale.

Project Control Architecture

Beyond culture, the practical infrastructure for managing the build phase involves real-time visibility into project data. Marimaca's management has described targeting dashboard-level access to budget, schedule, and progress metrics, with the intent that senior leadership can identify drift from plan as it occurs rather than after a reporting cycle has elapsed. This approach reflects a common principle in large capital project management, where the cost of correcting deviations increases with time. A budget overrun identified at 5% of project completion is structurally different from the same overrun identified at 50%. The systems being developed are intended to compress the detection-to-response interval.

Marimaca confirms that budget quotes have been obtained for 80% of the mechanical equipment, a data point indicating the engineering program has sufficient definition to support procurement-level pricing. This level of cost visibility at the pre-FID stage aligns with management’s stated objective of narrowing the gap between DFS estimates and executed costs.

What Does The MOD Economics Support

The DFS for the MOD, completed in 2025, establishes a pre-production capital cost of US$587 million and a base case production rate of 50,000 tonnes per annum of copper cathode over a 13-year mine life. The post-tax net present value at an 8% discount rate (NPV8%) of US$1.1 billion at a 39% internal rate of return (IRR) was modeled at US$5.05 per pound of copper, with an initial DFS base case run at US$4.30 per pound. A capital intensity of US$11,700 per tonne of annual production capacity places the project among the lowest-capital-intensity copper developments globally.

All-in sustaining costs (AISC) average US$2.09 per pound over mine life, placing the MOD in the second quartile of global copper producers. The project delivers first-5-year C1 cash costs of US$1.45 per pound, with expansion capital of US$77 million in year 6, increasing throughput capacity from 12 million to 16 million tonnes per annum. The DFS carries AACE Class 3 accuracy of minus 20% to plus 25%, meaning the current engineering program is targeting a tighter cost envelope before FID is declared.

One constraint on the economy that management has flagged is inflation. The longer the period between DFS completion and construction commencement, the greater the exposure to input cost escalation in Chilean labour and materials markets. This consideration is embedded in the timeline decision: targeting build-readiness by year-end 2026 rather than extending engineering into 2027 reflects, in part, a judgment about inflation exposure relative to the benefits of engineering maturity.

Pampa Medina: Silver Confirms the Geological Model

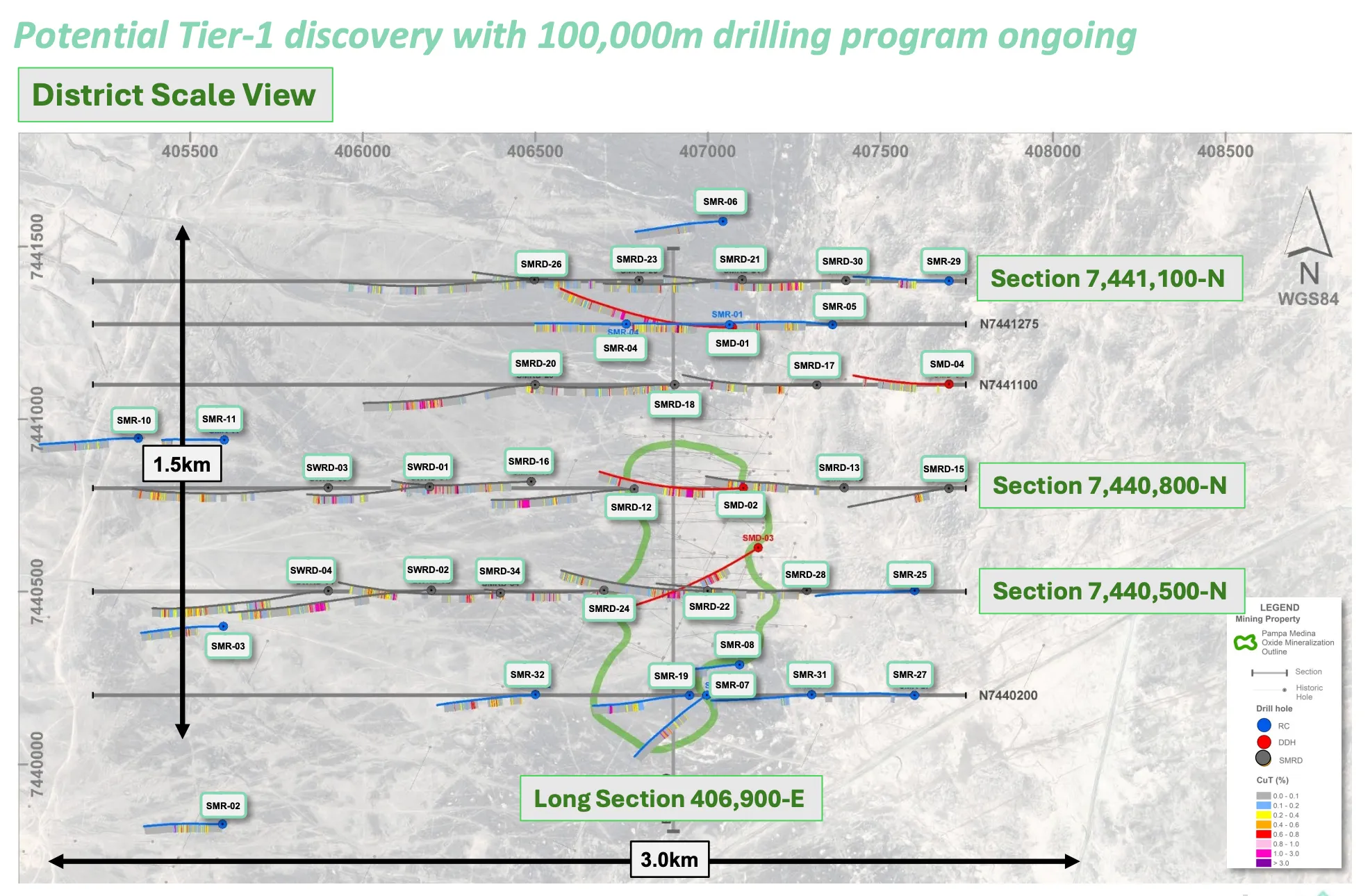

Marimaca consolidated silver assay results from all Pampa Medina drilling provide a second data layer on a copper system that has been building since Marimaca consolidated the project area in 2024. These results are not yet incorporated into MOD economics - Phase I metallurgical programs remain incomplete, meaning silver by-product credits cannot yet be calculated - but they confirm the scale and consistency of the system. The completion of inductively coupled plasma (ICP) assays across all holes confirms that silver mineralisation is present throughout the full deposit area, in both oxide and sulphide zones, and is broadly correlated with copper grade.

Standout intercepts from the consolidated dataset include 6 metres at 11.98% copper and 82 grams per tonne silver, within a broader interval of 100 metres at 1.28% copper and 6.9 grams per tonne silver, from a depth of 580 metres. Another highlight is 18 metres at 5.11% copper and 53.4 grams per tonne silver, within 102 metres at 1.20% copper and 12.2 grams per tonne silver from 250 metres. Step-out drilling to the west returned 74 metres at 1.21% copper and 7.9 grams per tonne silver from 520 metres, along with 38 metres at 1.43% copper and 11.8 grams per tonne silver from 694 metres. Silver by-products are consistent with nearby Chilean manto-type deposits, including Mantos Blancos and Cachorro.

The silver dataset does not alter the current financial model. The 2026 drill program - targeting 100,000 metres with 5 rigs on site and an increase in rig count targeted through April and May - is focused on 3 priorities: defining the high-grade sulphide-dominant central zone, delineating oxide extensions, and further step-out drilling to test the broader system identified in geophysical work. Full sulphide delineation across the 3-kilometre-by-1.5-kilometre footprint is estimated to require 200,000 to 300,000 metres of drilling over several years.

The Capital Structure Governs the Sequencing

Marimaca's ability to pursue both MOD construction preparation and Pampa Medina drilling simultaneously is a function of its US$165.6 million cash position and zero debt balance as of the April 2026 corporate presentation. The C$80 million raise completed in 2025, which was described as massively oversubscribed, provides runway to reach FID without a near-term equity raise.

Financing for the MOD build - a process that will involve evaluating project finance debt, strategic partnerships, and other structures - is being progressed in parallel with engineering through 2026. Management has stated that the objective is to minimise dilution to current shareholders through the construction phase. The hub-and-spoke infrastructure model, in which key processing equipment at the MOD is intentionally oversized to receive future Pampa Medina oxide feed at low incremental capital cost, supports production growth from 50,000 towards 70,000 to 75,000 tonnes per annum without a proportionate increase in capital expenditure (capex).

What to Watch Next

The key milestone for the investment case is FID readiness. The company is targeting a three-month window on either side of year-end 2026 to build readiness, contingent on advancing detailed design and engineering to a point where cost-variation risk is deemed acceptable. Financing is closely linked. Options for the US$587 million pre-production capital requirement are being evaluated through 2026, with a stated objective of minimising shareholder dilution, although the structure and timing of any announcement remain undisclosed. A third near-term marker is the build-out of the senior execution team, with key construction leadership roles currently being filled.

On the exploration side, the 100,000-metre 2026 drill program at Pampa Medina is underway, with 5 rigs on site and a planned increase in rig count through April and May 2026. Ongoing step-out results represent the nearest-term reporting points, with the first copper-equivalent grade calculations incorporating silver credits contingent on the completion of Phase I metallurgical programs.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed