Fed Rate Cut Expectations & a 46.3 Million Ounce Silver Deficit Tighten Physical Silver Markets

Six consecutive silver supply deficits and incoming Fed rate cuts are converging, signaling a re-rating opportunity for silver investors in 2026.

- On April 29, 2026, the Fed held rates at 3.50% to 3.75% as four officials dissented, while the policy statement signaled growing support for future rate cuts. Kevin Warsh’s Senate Banking Committee approval also increased expectations that the Fed could begin lowering interest rates after the June 16-17 meeting.

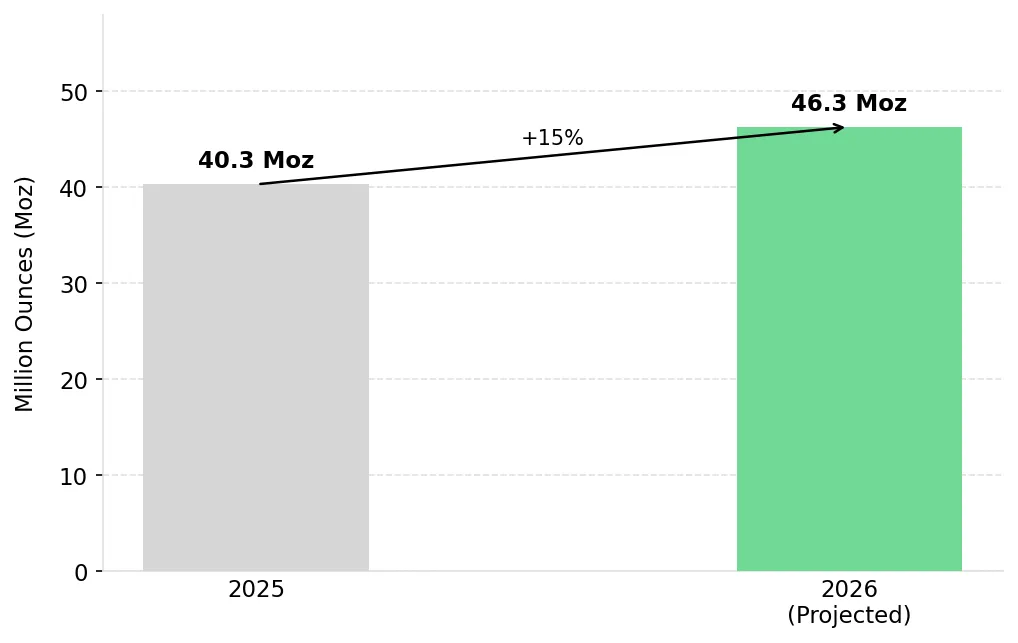

- The World Silver Survey 2026 confirms a sixth consecutive annual silver supply deficit of 46.3 million ounces, 15% larger than the 2025 shortfall, while cumulative above-ground silver inventories have declined by 762 million troy ounces since 2021.

- In September 2025, freely available silver in London vaults fell to 17% of total inventory, tightening physical supply and triggering a sharp increase in lease rates. Since then, approximately 100 million ounces have moved into COMEX warehouses in New York as traders reacted to potential Section 232 tariffs, further reducing silver available in the London spot market.

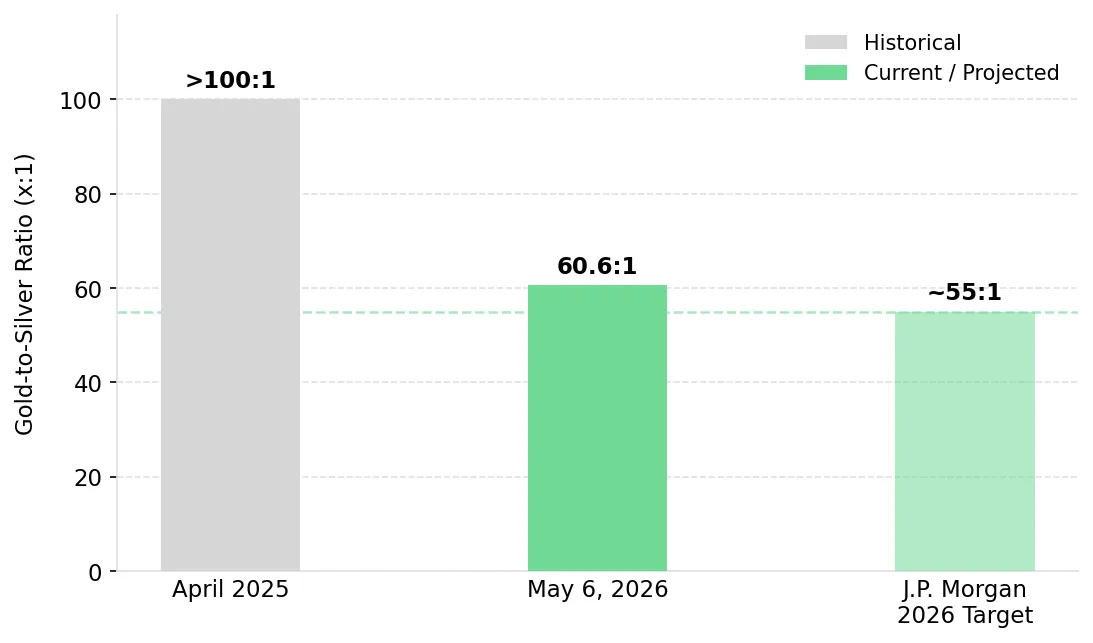

- US-Iran peace negotiations triggered a 5.5% to 6% rise in silver prices on May 6, 2026, outperforming gold’s 2.7% to 3.6% gain as lower geopolitical risk eased inflation concerns and increased expectations for future Fed rate cuts. The gold-to-silver ratio also compressed from 62.5 to 60.6.

- Silver producers, developers, and explorers provide different ways to gain exposure to tightening silver supply conditions, from producers adding high-grade ounces at relatively low capital costs in domestic jurisdictions, to developers advancing construction-ready projects, to explorers expanding resources at historical discovery costs below US$0.15 per ounce.

Fed Policy Division Increases Rate Cut Expectations for Silver

The Fed’s April 29, 2026 meeting mattered more for the unusually high level of policy disagreement than for the decision to hold rates steady. Four Federal Open Market Committee members dissented from the policy decision, the highest number of dissenting votes at a single meeting since late 1992. Three governors opposed language supporting future rate cuts because they believed inflation remained too high at 3.2% and was still increasing. One governor separately supported an immediate 25-basis-point rate cut.

Silver prices typically move opposite real yields, which are interest rates adjusted for inflation. Each 25-basis-point rate cut reduces the opportunity cost of holding non-yielding assets like silver, increasing the appeal of physical silver, silver ETFs, and silver mining equities. CME showed a 9.1% probability of a rate hike by December 2026, up from 0% the prior day, reflecting continued uncertainty around the Fed’s policy.

Potential Fed rate cuts and Trump administration support for domestic critical mineral production could improve financing conditions for US silver producers. Americas Gold and Silver operates the Galena Complex in Idaho’s Coeur d’Alene Mining District. The operation is the largest antimony mine in the US and one of the world’s highest-grade underground silver operations. Oliver Turner, Executive Vice President of Corporate Development at Americas Gold and Silver, contrasted the company’s valuation against broader silver sector peers:

“When you look at the price-to-NAV of this company using all eight analysts’ consensus numbers at spot prices, we’re somewhere between 0.6 and 0.7 times NAV. Where do the silver peers trade? Around 1.5 times NAV.”

June Fed Forecasts & Kevin Warsh’s Policy Outlook Support Silver

Kevin Warsh is targeting his first Federal Open Market Committee meeting as chair on June 16-17, the first meeting in 2026 to include the Fed’s updated dot plot rate forecasts. SoFi Technologies Chief Executive Officer Anthony Noto stated publicly that a Warsh-led Fed would be more willing to cut interest rates. If the June dot plot shifts toward two rate cuts in the second half of 2026, lower real yields would reduce the opportunity cost of holding silver. That would recreate monetary conditions similar to the environment that supported silver’s rally in early 2025. Silver began a 130% rally in early 2025 before peaking above $120 per ounce in January 2026.

Six Consecutive Silver Deficits Continue Tightening Physical Supply

The World Silver Survey 2026 confirms that global silver demand will exceed total supply for a sixth consecutive year in 2026. The market deficit is projected at 46.3 million ounces, 15% larger than the 2025 shortfall, extending a multi-year inventory drawdown that has already reduced above-ground silver stocks by 762 million troy ounces since 2021. Tight supply conditions are expected to persist in 2026 as total silver supply declines by approximately 2%, while mine production grows by only 1% and recycling volumes remain constrained by refinery bottlenecks. Physical market tightness is also visible in COMEX inventories, where registered silver stocks have fallen approximately 75% since 2020, declining from roughly 346 million ounces to approximately 88 million ounces.

Above-ground silver inventories continue to decline as global demand outpaces new supply, increasing the importance of exploration companies capable of expanding silver resources through active drilling programs. GR Silver Mining is advancing a 20,000-meter drill campaign at its San Marcial project in Mexico as the company works to grow its existing silver resource base during a period of tightening physical silver markets. Eric Zaunscherb, Executive Chairman of GR Silver Mining, emphasized the scale of the project’s expansion potential:

“We think we have a large opportunity here. Our main focus is on expanding the resource at this point in time. We have 134 million ounces of silver equivalent and we feel that that has a significant chance to grow through our 20,000 meter drill program.”

Declining London Silver Inventories Tighten Physical Supply

London’s physical silver market has faced increasing supply pressure since late 2025. The World Silver Survey 2026 reported that freely available silver in London vaults fell to 17% in September 2025. At that level, available inventories became too limited to absorb large institutional buying flows without triggering sharp price movements. Since then, approximately 100 million additional ounces have moved into COMEX warehouses as traders reacted to potential Section 232 tariffs on critical materials. That shift further reduced silver available in the London market. China’s Ministry of Commerce export restrictions on silver for 2026 and 2027 could further tighten metal availability in London and increase regional supply fragmentation

Middle East De-escalation Supports Both Investment and Industrial Silver Demand

On May 6, 2026, Washington and Tehran were finalizing a peace framework that included enhanced UN inspections, a halt to nuclear enrichment, and a gradual lifting of sanctions. Silver rose 5.5% to 6% to $77.47 per ounce, its highest level since April 21. Gold gained 2.7% to 3.6% during the same session, but silver outperformed as lower geopolitical risk improved both industrial demand expectations and the outlook for future Fed rate cuts.

The Strait of Hormuz closure raised global energy costs over a ten-week period, pushing inflation higher and limiting the Fed’s ability to cut interest rates. Lower geopolitical tensions could reverse that cycle by easing oil prices, reducing inflation pressure, and giving incoming Chairman Kevin Warsh more room to support future rate cuts. Lower real yields would improve silver’s relative attractiveness, while recovering manufacturing activity would support industrial silver demand, which accounted for approximately 60% of total annual demand in the Silver Institute’s 2026 data. Gold mainly benefited from lower rate expectations, while silver benefited from both monetary and industrial demand support.

Lower interest rate expectations and improving industrial demand conditions can support faster development activity across advanced silver projects. Vizsla Silver recently awarded a US$170 million Engineering, Procurement and Construction Management contract for its Panuco project following a November 2025 Feasibility Study that reported an after-tax NPV of US$1.8 billion and a 111% after-tax IRR.

The Gold-Silver Ratio at 60.6 Still Supports Further Silver Outperformance

The gold-to-silver ratio rose above 100:1 in April 2025 as Middle East conflict and tighter Fed policy weakened industrial demand expectations for silver. As of May 6, 2026, the ratio had declined to 60.6 but remained above the historical 50-to-55:1 range associated with periods when silver prices rose faster than gold. JPMorgan’s 2026 price targets of $85 silver and approximately $4,700 gold imply a gold-to-silver ratio near 55:1. That would represent roughly 10% additional compression from current levels and could materially increase net asset values for silver mining equities.

Solar Manufacturers Reduce Silver Usage as Industrial Demand Shifts to AI and EVs

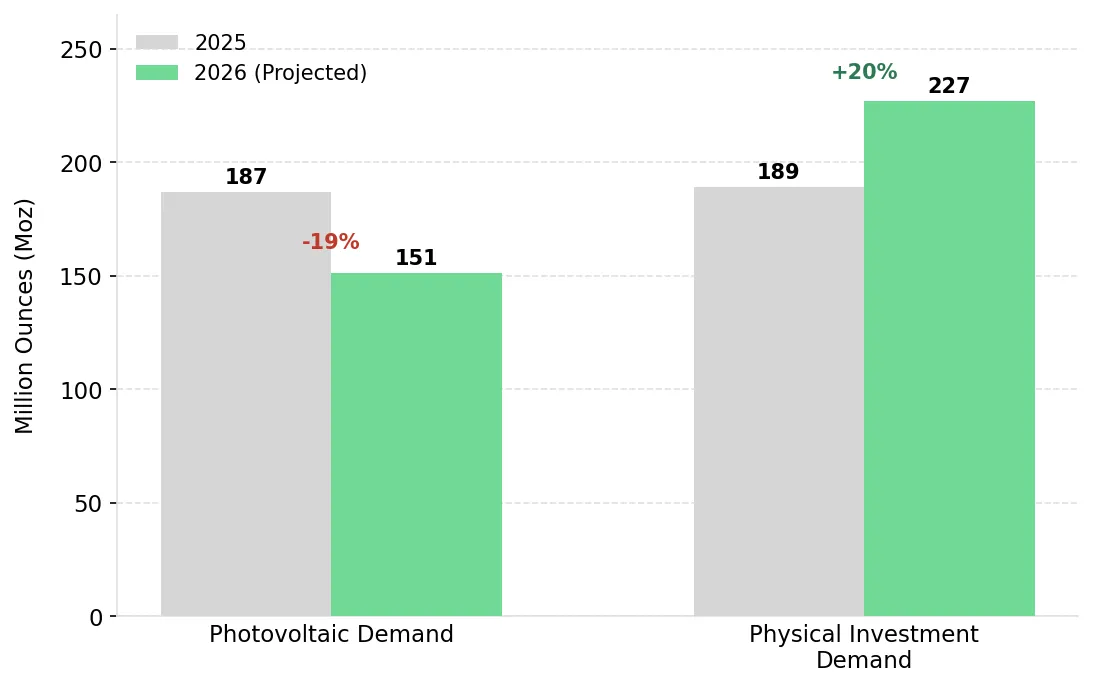

Investors should no longer assume that rising solar installations automatically translate into proportional growth in silver demand. According to the World Silver Survey 2026, photovoltaic silver demand is projected to decline 19% in 2026 to approximately 151 million ounces. That follows a 6% decline in 2025 to 186.6 million ounces. Solar installations continue to grow, but silver demand is declining because manufacturers are reducing silver paste content per cell as silver prices rise. Silver paste accounts for 10% to 20% of total solar cell costs, increasing pressure on manufacturers to reduce silver usage per panel. As a result, solar capacity growth no longer translates proportionally into silver demand growth in the 2026 data.

Artificial intelligence-driven data center expansion is increasing demand for silver used in high-performance electronics. Electric vehicle power electronics and battery management systems are also increasing industrial silver demand. The Silver Institute projects physical silver investment demand will rise 20% to a three-year high of 227 million ounces in 2026. The increase is driven by recovering Western retail demand and continued institutional buying in China and India. The projected 46.3 million ounce silver deficit reflects constrained mine supply meeting rising demand from both industrial users and investment buyers.

The Investment Thesis for Silver

- The World Silver Survey 2026 confirms a sixth consecutive annual silver deficit of 46.3 million ounces. Since 2021, cumulative above-ground silver inventories have declined by 762 million troy ounces, showing that global silver demand continues to exceed supply.

- The Fed’s April policy statement and Kevin Warsh’s expected leadership transition increased expectations for future rate cuts at the June 16-17 meeting. Lower real yields would reduce the opportunity cost of holding silver, which still trades 35% below its January 2026 high.

- US silver producers that also generate critical minerals could benefit from Trump administration policies supporting domestic mineral supply chains. That support could improve project economics and reduce reliance on silver prices alone to drive profitability.

- Silver developers with completed feasibility studies, after-tax IRRs above 100%, and active engineering contracts are moving closer to construction decisions. High-grade projects entering development during a tightening silver market could benefit from stronger pricing and improved project economics.

- Exploration companies expanding silver resources at historical discovery costs below US$0.15 per ounce could benefit from continued silver supply deficits. Companies with debt-free balance sheets and projects in established epithermal silver districts may also benefit from resource updates and economic studies that improve project valuations through 2026.

The silver market entered 2026 after six consecutive annual supply deficits and cumulative inventory drawdowns of 762 million ounces since 2021. Freely available silver inventories in London vaults had also fallen to 17% before the Iran peace talks, the April 29 Fed vote, and Kevin Warsh’s nomination. Those events could accelerate investor reassessment of a silver market already constrained by tight physical supply. The investment case is driven by six consecutive years of demand exceeding supply, declining above-ground inventories, and limited mine supply growth. Most silver production remains tied to copper, lead, and zinc mining rather than primary silver production. For investors with a 12-to-24-month time horizon, silver at $77 per ounce remains 35% below its January 2026 high despite continued supply deficits and tightening inventories. That imbalance could support further upside if demand conditions strengthen.

TL;DR

The World Silver Survey 2026 confirms the silver market has run a supply deficit for six consecutive years, with cumulative inventory drawdowns since 2021 reaching 762 million troy ounces. The Federal Reserve's April 2026 vote embedded a signal toward future rate cuts, and incoming Chairman Kevin Warsh is positioned to shift toward an easing cycle that mechanically reduces the cost of holding silver. A US-Iran peace framework, if finalized, would ease consumer inflation and restore manufacturing demand, engaging both silver's monetary and industrial demand channels simultaneously. At $77 per ounce, silver trades 35% below its January 2026 high against a market that remains structurally undersupplied.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed