Fremont Gold (TSX-V: FRE) - Gold Explorer with the Right Fundamentals?

Is Fremont Gold a gold explorer with the right fundamentals? Gold investors want to know if this gold mining company has what it takes to make them money.

At close to US$2,000/oz, gold is the hottest it has ever been. In fact, it is even pricier than it was during the gold rush of mid-2011. This bull environment has seen the margins of gold producers grow immensely, and even high-cost producers have been benefiting. This capital has trickled down to gold developers, who have found getting their projects financed on good terms easier than getting out of bed in the morning.

However, all of this positivity doesn't necessarily create share price growth for gold explorers. Whilst producers and developers can give investors leverage to the soaring gold price, explorers are playing something of a more long-term game. This is not to say that these explorers necessarily plan on bringing these projects into production themselves, it is just the case that the company's ounces in the ground are not able to enter the market at this current point in the cycle, meaning explorers are reliant on a favourable long-term gold conditions to ensure these ounces deliver dramatic growth for investors. So, what exactly should investors be looking for when conducting their due diligence on gold explorers?

There is no point in wasting your time on gold losers. A gold explorer with poor fundamentals might attract short-term attention, but in the long-run, it is highly unlikely to make most investors money. What fundamentals should we be focussing on?

- Jurisdiction

- Asset Potential

- Level of Risk

- Balance Sheet

- Management Team

A company that recently came to the attention of Crux Investor is Nevada-based explorer, Fremont Gold (TSX-V: FRE). You can check out our recent interview with CEO, Blaine Monaghan, here. He impressed me with his candour and the fundamentals of the company appeared strong. It was time to dive in a little deeper to discern if this was an investment opportunity I should consider more seriously.

Jurisdiction

So, applying this set of criteria to Fremont Gold, let's kick off this analysis with jurisdiction. There are plenty of gold investment opportunities that are situated in jurisdictions with concerning issues. Take the Sahel (West Africa), an area that has been covered fairly extensively on the website, a gold explorer with assets here can expect a severe security threat from terrorism or criminal enterprise. Whilst the region had calmed down a little recently, due to the involvement of French security forces and interregional cooperation, the recent military coup in Mali has reignited tensions.

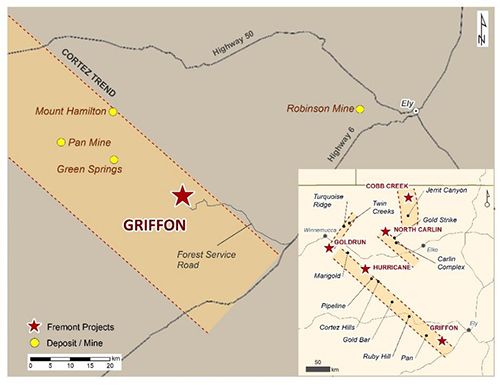

Fremont Gold doesn't have any of these issues. It is based in a tier-1 jurisdiction, Nevada, that is stable and also has favourable permitting practices.

Asset Potential

Let's take a look at this in terms of grade, economic strength and scale. Fremont Gold's flagship project and only focus right now is the Griffon gold project. Griffon is a past-producing asset and brownfield deposit that last produced ounces in 1999. It was acquired from Liberty Gold at the end of 2019.

The company also acquired Cobb Creek, another gold exploration play, from Contact Gold at the same time. Cobb Creek has not been drilled since 1992, but it contains a historical mineral resource estimate (not NI 43-101 compliant):

ResourceMineralizedCut-Off GradeOuncesClassificationZone(opt)Tons(opt)GoldIndicatedOxide0.011,362,2330.0454,864IndicatedSulphide0.012,378,0000.05118,134

However, despite the potential of 167 unpatented mining claims that haven't been drilled in over three decades, Griffon is the focus right now. Fremont Gold also has several additional exploration tenements: North Carlin, Hurricane and Goldrun. These are of a smaller scale and are sitting on the backburner waiting to be monetised once Fremont Gold receives a better valuation and can raise capital on terms more favourable to shareholders.

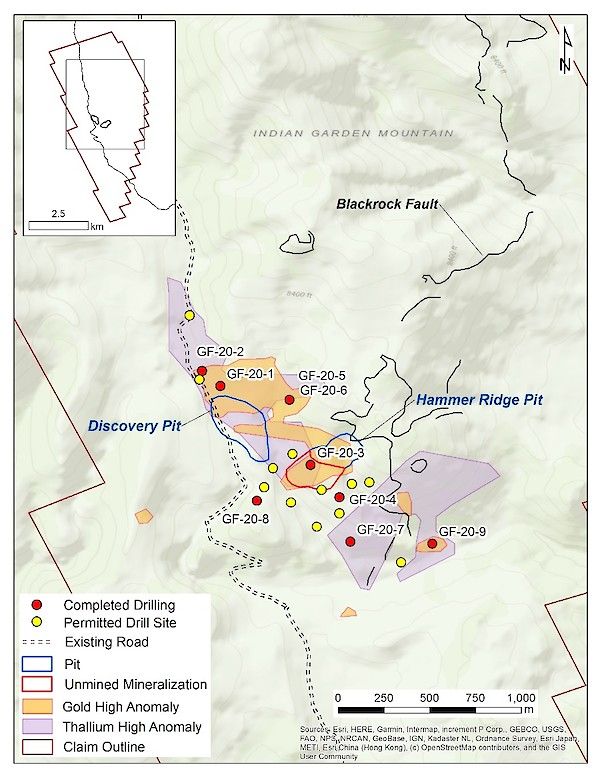

So, focussing on Griffon, let's take a look at some of the historical data. Griffon was first drilled in 1988. There has been fairly limited amount of shallow drilling at the property, totalling 214 drill holes. The aim of this drilling was to delineate the Discovery Ridge and Hammer Ridge deposits. This means the remainder of Griffon is practically untested. Between the years of 1997 and 1999, Alta Gold Co. produced gold at an average grade of 1.03g/t from Discovery Ridge and Hammer Ridge as part of an oxide heap-leach operation.

Griffon is host to an array of gravity, soil, and stratigraphic targets and is located strategically close to several gold mines and strong existing infrastructure.

Do company's let assets go if they are that promising? Fremont claims that Liberty Gold had invested into de-risking the project significantly, but it became distracted with other superior projects. Just because the project isn't the best around, it doesn't mean that it can't be extremely profitable in the current environment.

Level of Risk

Let's take a look at a selection of historical unmined drill intercepts.

HoleZoneFrom (metres)To (metres)Intervalg/t GoldGR94-76Discovery N3.016.813.70.41 22.935.112.20.58GR94-98Hammer SW4.613.79.10.51 57.982.324.40.79GR97-160Hammer SW22.948.825.91.10GR97-162Hammer SW30.567.136.60.93GR97-163Hammer SW38.162.524.40.69GR97-164Hammer SW9.156.447.20.89GR97-175Hammer SW22.980.857.90.86GR97-184Hammer SW32.076.244.20.58

This data is promising and exhibits the potential for Griffin to become a low-cost, bulk-tonnage operation with the potential of high-grade exploration.

Gold explorers always carry a high degree of risk. However, Fremont Gold appears to be in quite a unique position. Griffin's past-production combined with this historical data turns it into a substantially de-risked exploration proposition.

Investors may also want to consider that whilst Fremont Gold is currently directing all capital towards Griffon, this is not a single asset company, despite the market potentially valuing it as such. Cobb Creek looks equally promising, and with the company's remaining portfolio and low burn rate, Fremont is a company that has significant diversification. Plenty can go wrong in an exploration play, so Fremont appears to have several attractive contingency plans should Griffon not pan out as expected. In fact, the company would love to be firing on all cylinders at Cobb too, but it is keeping a tight grip on the pursestrings. I'm impressed. This company seems to understand that they are spending investors' money, not their own.

Balance Sheet

Most explorers have no discernible cash flow, so running a tight ship is incredibly important. Part of the reason that Fremont Gold presents a compelling case for investment is because of its strong balance sheet. Having raised US$1.5M in a February private placement, the company had $1M in the bank when we last spoke with low overheads. It appears to be in good shape to explore, de-risk and develop Griffon up until the PEA stage. That is when CEO Monaghan claimed the company will look towards a potential takeout.

The market appears to have exhibited a reasonable level of interest in Fremont. The company's $400,000, 2000m drill programme with four principle targets was ramped up to 2,275m in nine holes and remained within budget. Several of the assays are pending, but Fremont has received assay results from the first three holes. One hole intersected a significant interval of near-surface oxide gold mineralization: 50.3m of 1.05g/t gold starting at 29m. The market hasn't responded fully to this yet, and Fremont anticipates that further drilling will further uncover the value proposition that is available here. However, Monaghan feels these results already exhibit the potential for Carlin-type deposits.

Holes four to nine are still pending, and once these assays are received, this should set the stage nicely for an expanded phase II drill program.

I would expect those already invested to continue to follow their money, and these results have shown me nothing to demonstrate otherwise. I would expect an imminent financing to push this project forward. Is that the prime time to throw one's hat into the ring?

Management Team

When I first took a look at the board, it looked a little saturated to me. However, it is clear that Monaghan's claim that it is a "high-calibre team" is perfectly valid. Moreover, the actual management board is quite modest; it is the advisory side of things that looks a little saturated. However, more expertise is certainly a good thing. Monaghan is actually the only full-time employee of Fremont Gold. Investors will be hoping the other names in this story have enough free time to concentrate on the company when it needs their attention.

In terms of skin in the game, insiders own 17% of the company. I've seen companies with more insider ownership, but 17% is a sizeable amount. It aligns the team quite nicely with shareholders. Monaghan himself holds just over 1M shares (c. C$100,000 purchased from the open market). It is not enough to be meaningful, but the management team's continual purchasing of shares on the open market is a positive.

The real target for Monaghan is to drive liquidity into the stock. Trading volumes are not as high as they need to be, and during our interview with him, he was very transparent about this issue. It is clear that interest form retail investors in exploration-stage project has flagged somewhat over the last 9 years, but it is retail investors that Fremont is targeting to ignite this story. The company isn't currently looking towards corporate/strategic investment right now. Instead of being beholden to a separate commercial entity, the company wants to develop Griffon on its own terms. This is one of the few gold explorers that appears to have the ability to raise capital and develop projects without the involvement of some kind of external overseer.

All in all, Fremont Gold is shaping up excellently. However, it is worth stressing that there is still an awful lot of work to do before this company can deliver value where it counts: the share price. In a gold environment where anything seems possible, this company could be a well-positioned bet for investors who want to get in early.

What did you make of Blaine Monaghan and Fremont Gold?

Company Website: https://www.fremontgold.net/

Analyst's Notes

Subscribe to Our Channel

Stay Informed