Peace Deal Optimism Cuts Brent to $88, but 13%US Distillate Deficit Keeps Higher Oil Price Risk

Peace deal optimism pushed Brent to $88, but a 13% US distillate deficit and Hormuz shipping risks keep higher oil prices and mining fuel costs in focus.

- Brent fell 2.3% to $88.27 per barrel and WTI fell 2.2% to $85.81 after Trump cancelled planned strikes on Iran and signaled a potential peace deal, pushing oil to a two-month low and reducing the market-implied probability of an October Fed rate hike to 36% from 51%.

- Iranian forces blocked a tanker from transiting the Strait of Hormuz without coordination, indicating that shipping disruptions remained possible despite market optimism over a potential peace deal.

- ING analysts forecast Brent could reach $120-130 per barrel by late July if Hormuz oil flows do not resume, as falling inventories and stronger seasonal demand tighten the market.

- US distillate inventories were 13% below their five-year average while distillate demand ran 7.2% above year-ago levels, indicating diesel supply remained tight despite progress toward a potential peace deal.

- OPEC cut its 2026 oil demand growth forecast to 970,000 bpd from 1.17 million bpd while raising its 2027 outlook, indicating that oil demand has been delayed rather than eliminated and could support higher prices after Hormuz reopens.

Peace Deal Signals Cut Oil Prices, but Strait of Hormuz Disruption Risk Remains

US President Donald Trump cancelled planned strikes on Iran and signaled that a peace deal could be reached soon, increasing expectations of a de-escalation in Middle East tensions. Brent fell 2.3% to $88.27 per barrel, its lowest level in two months, while WTI fell 2.2% to $85.81. The market-implied probability of an October Fed rate hike fell to 36% from 51%, while two-year Treasury yields settled at 4.073% and gold fell 0.7% to $4,183 per ounce.

Iran stated that no final agreement had been reached, while Iranian forces blocked a tanker from transiting the Strait of Hormuz without coordination, indicating that shipping risks remain unresolved. The Strait of Hormuz carries about 20% of global oil and LNG shipments. IG analyst Tony Sycamore said Brent holding above the low-$80s support level would keep the risk of higher oil prices intact.

US Distillate Inventories Remain 13% Below Average as Diesel Supply Stays Tight

Oil prices fell on expectations that Hormuz shipping will resume, not because flows have already recovered. US crude inventories fell by 7.2 million barrels in the latest week, while distillate inventories remained 13% below their five-year average and crude imports were 5.8% below year-ago levels. Distillate demand was 7.2% above year-ago levels. Strong demand and constrained supply continue to support diesel prices, and that imbalance will not be resolved until fuel inventories rebuild and shipping flows normalize.

ING analysts said Brent could rise to $120-130 per barrel by late July if Hormuz oil flows do not resume, as lower inventories and stronger seasonal demand tighten supply. ING warned that a ceasefire alone may not hold if nuclear negotiations fail to advance. Avoiding ING's $120-130 oil price scenario requires both a recovery in Hormuz shipping and continued progress in nuclear negotiations.

Nuclear Talks Hold the Key to ING's $120-130 Oil Price Scenario

National Australia Bank's Ray Attrill said diplomatic progress appeared more credible, while ING warned that a ceasefire may not hold without progress in nuclear negotiations. Iran's decision to block a tanker in the Strait of Hormuz despite improving diplomatic signals shows that shipping disruptions remain a near-term risk.

A ceasefire and a recovery in Hormuz shipping would likely keep Brent near current levels. However, distillate inventories remain 13% below their five-year average, keeping diesel costs for miners above pre-conflict levels until inventories recover. If nuclear talks stall and Hormuz flows fail to recover, Brent could rise toward ING's $120-130 per barrel target, increasing operating costs for miners with unhedged diesel-intensive operations.

Hormuz tanker transit volumes will be the clearest indicator of whether oil supply conditions are improving after any peace deal. Iran blocked tanker transit despite improving diplomatic signals, showing that shipping flows have not yet recovered and supply risks remain in place.

High Diesel Costs Keep Pressure on Open-Pit Mining Margins

Fuel accounts for 20-30% of cash operating costs at many open-pit gold, copper, and bulk commodity mines, with limited short-term hedging options. OPEC cut its 2026 demand growth forecast to 970,000 bpd from 1.17 million bpd while raising its 2027 outlook, suggesting that oil demand has been delayed rather than eliminated. A reopening of Hormuz could remove some supply-risk premium, but recovering demand may continue to support oil prices.

Miners' fuel cost exposure depends on whether H2 2026 budgets were based on pre-conflict oil prices or the higher prices seen during the conflict. US refineries operated at 95.3% of capacity, indicating that most available refining capacity is already in use and leaving limited room to increase fuel production if demand rises further. Miners without fuel hedges remain exposed to ING's $120-130 oil price scenario, while high refinery utilization limits the industry's ability to increase fuel supply if demand strengthens.

The oil outlook remains uncertain because Iran has not approved a final agreement and shipping disruptions in the Strait of Hormuz continue. Investors should monitor weekly US distillate inventories, which remain 13% below their five-year average. If the inventory deficit does not narrow after a peace agreement, diesel supply will remain constrained and fuel costs are likely to stay above pre-conflict levels.

Brent in the Low $80s and Falling Inventory Deficits Would Signal Oil Market Normalization

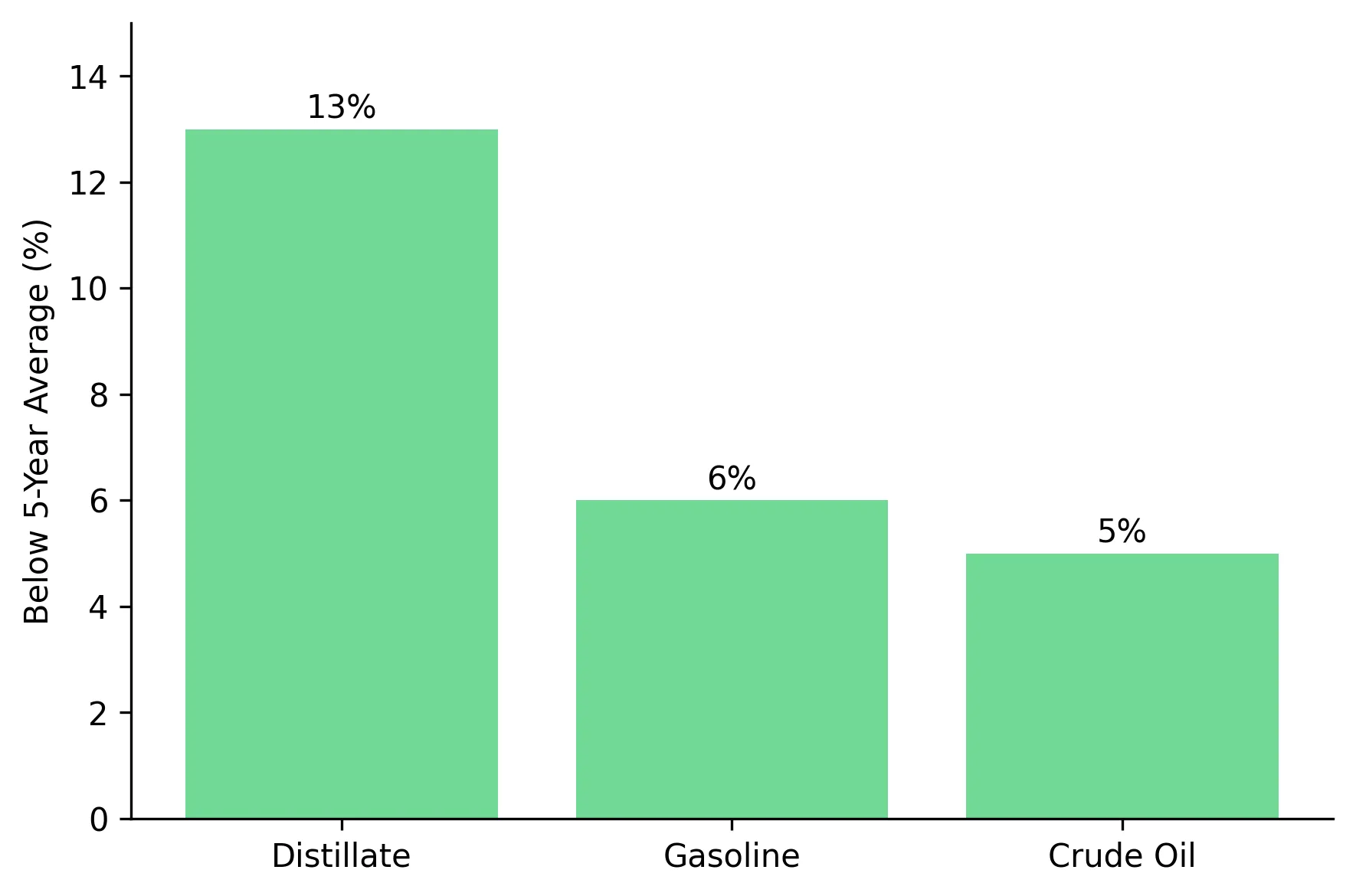

Oil prices continue to be supported by tight inventories and ongoing shipping risks in the Strait of Hormuz. US distillate inventories were 13% below their five-year average, while gasoline inventories were 6% below and crude inventories were 5% below. These inventory deficits will take weeks to rebuild and are unlikely to normalize immediately following a peace agreement.

A sustained move by Brent into the low $80s would signal that oil prices are stabilizing, but that requires a recovery in Hormuz tanker traffic rather than diplomatic announcements alone. ING's $120-130 per barrel scenario depends on whether oil flows resume before late July, making physical shipping data more important than political commitments.

Weekly US distillate inventory data provides a key measure of whether fuel markets are tightening or recovering. Investors should watch whether the distillate inventory deficit narrows from its current level of 13% below the five-year average. A deficit that narrows to within 5% of the five-year average over multiple weeks would indicate that fuel supply is recovering and reduce the likelihood of ING's $120-130 oil price scenario. OPEC's next demand forecast will show whether oil consumption is recovering faster than expected. An upward revision from 970,000 bpd toward 1.17 million bpd would support higher oil prices even if supply conditions improve.

Analyst's Notes

Subscribe to Our Channel

Stay Informed