Record Inflows into Silver ETPs Driving Investor Returns

Institutional silver demand surges with record $40B ETP inflows in 2025. Supply deficits driven by green energy create opportunities for mining stocks.

- Institutional demand for silver is surging, evidenced by record inflows into silver ETPs, over $40 billion in assets and 95 million ounces added in 2025 alone.

- Silver's structural deficit is deepening, fueled by green energy adoption, electrification, and industrial resilience, underpinning its role as both a monetary and industrial metal.

- Mining equities with high silver exposure and low AISC stand to benefit disproportionately as silver prices approach a 14-year high.

- Americas Gold & Silver, Cerro de Pasco Resources, and Vizsla Silver offer differentiated strategic leverage to this macro trend through scale, asset quality, and production visibility.

- Capital rotation into silver is gaining momentum amid dollar weakness, policy risk hedging, and a global hunt for alternative stores of value.

Institutional demand for silver is reaching an inflection point. Silver exchange-traded products have absorbed over 95 million ounces in 2025, already surpassing the 88 million ounces added throughout 2024. With more than $40 billion in silver ETP assets under management globally, the scale of institutional reallocation signals a fundamental shift in how sophisticated capital views silver's role within diversified portfolios.

This surge reflects silver's unique positioning as both a store of value and critical industrial input. The World Gold Council and Metals Focus report that silver now comprises 7% of all precious metals ETF holdings globally, up from 4% in 2020. The reallocation is consistent with a broader institutional rotation toward real assets and hard collateral during periods of monetary policy uncertainty and deglobalizing trade flows.

Silver's Evolving Role in Global Finance

Silver's hybrid nature, combining monetary store of value properties with essential industrial utility, positions it distinctly within current macro environments. Unlike gold, which primarily serves institutional portfolios as a monetary hedge, silver's industrial demand profile creates additional value drivers that institutional allocators are increasingly recognizing.

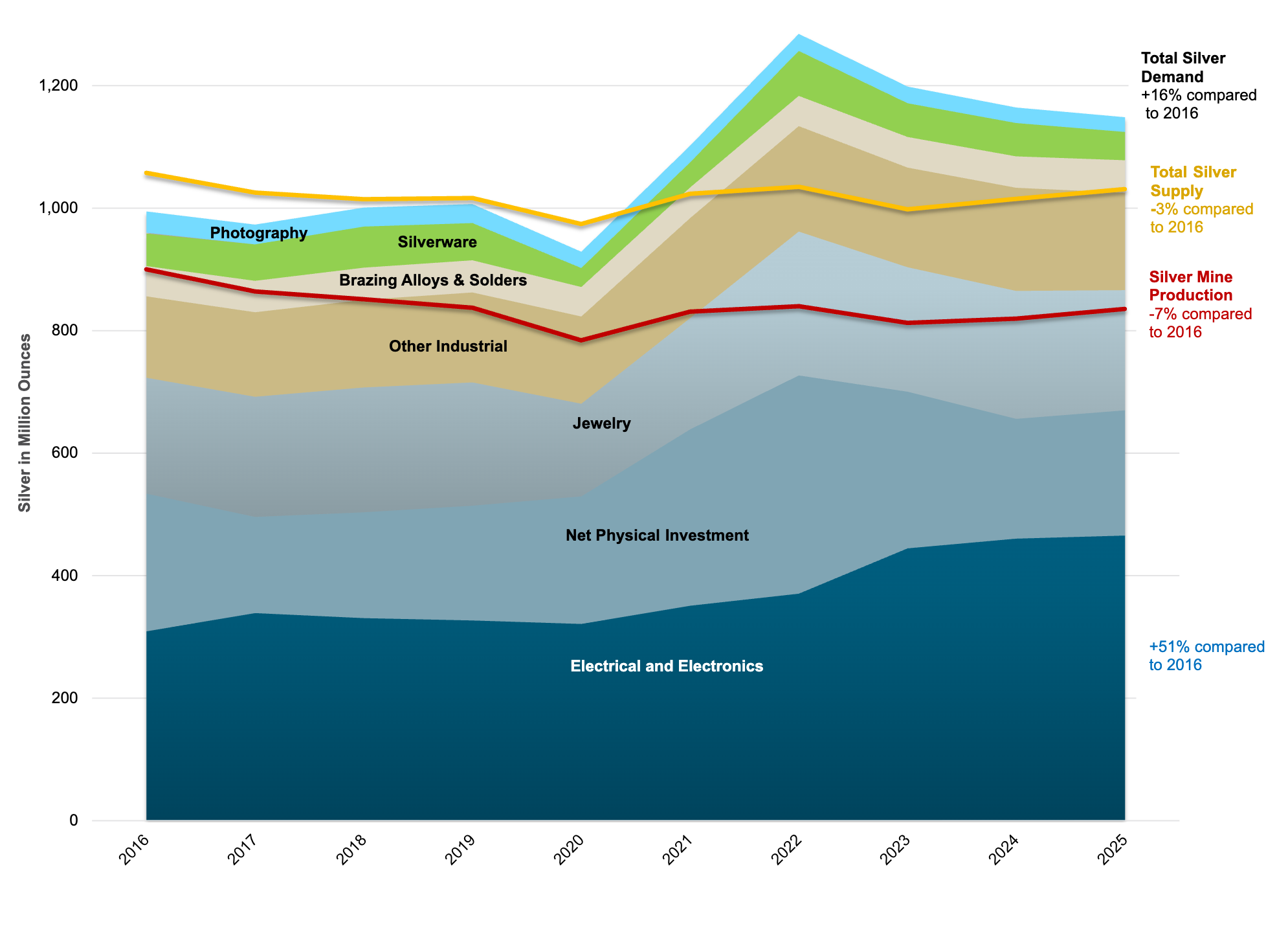

The metal's supply-demand fundamentals are tightening materially. Supply has declined 0.9% annually since 2020 while demand has grown 3.6%, according to Metals Focus. The 2023 deficit of 184 million ounces is projected to expand 17% in 2024, driven primarily by accelerating photovoltaic and electric vehicle demand. Silver used in photovoltaics reached 232 million ounces in 2024, four times the 2015 level. Paul Huet, Chief Executive Officer of Americas Gold & Silver notes:

"We're at about 80% of our metals coming directly from silver, so that's quite unique. I don't think there are too many groups out there that have 80% of their revenue stream coming from silver."

This pure-play exposure positions companies with high silver concentration to benefit disproportionately from the metal's structural deficit.

The Supply-Demand Gap: A Deficit That Matters

Industrial silver demand is accelerating beyond traditional applications. Solar panel manufacturing, electric vehicle components, and energy storage systems are creating sustained demand growth that traditional mining supply cannot match.

Simultaneously, primary silver mine production faces headwinds from declining ore grades, permitting delays, and capital allocation constraints within the broader mining sector. This supply-side pressure amplifies the significance of companies with existing production capacity and near-term development timelines.

Systemic Risk & Asset Repricing Across Cycles

Real Assets in a De-Dollarizing Environment

Dollar weakness, negative real yields, and accelerating global foreign exchange diversification are channeling institutional flows toward precious metals. The institutional rotation appears defensive in nature, hedging monetary policy uncertainty, fiat currency debasement risks, and interest rate volatility.

Silver's price performance relative to gold reflects differentiated institutional allocation patterns. While gold maintains its traditional safe-haven premium, silver ETPs are leading precious metals inflows year-to-date, suggesting institutional recognition of silver's industrial demand sustainability and potential for monetary premium expansion.

Repricing Risk & Safe-Haven Rotation

Geopolitical instability and persistent inflation volatility are driving silver's monetary premium higher. Capital is rotating out of growth-sensitive sectors including technology and real estate investment trusts into hard assets, driven by tighter capital markets and increasing correlation between real assets and portfolio protection strategies.

Capital Formation & Strategic Deployment in Mining

Institutional Capital Is Shifting to Developers & Producers

Silver-focused mining companies are demonstrating strong institutional appeal. Americas Gold & Silver has seen institutional ownership rise from 8% to over 60% of its shareholder base, reflecting broader market reallocation toward companies with direct silver exposure and operational leverage.

Access to non-dilutive financing mechanisms further validates institutional confidence. The company recently secured a $100 million debt facility alongside a concurrent equity raise, providing capital for operational expansion without diluting existing shareholders. This financing structure, combined with offtake agreements securing 100% of concentrate sales, demonstrates how institutional capital is supporting operationally de-risked silver producers.

Deployment Timing & Asset Scarcity

Companies with established resources and near-term production timelines are attracting premium institutional allocations. Vizsla Silver's $200 million cash position and zero debt profile exemplify the capital discipline institutional investors demand during development-heavy phases.

The company's discovery costs of $0.41 per ounce silver equivalent and projected nine-month payback period align with institutional preferences for rapid value realization. Vizsla’s COO Simon Cmrlec notes:

"We set ourselves a target to have more than 200 million ounces from the mining areas in measured and indicated, and more than 20 million ounces in the measured category. .We outshot both of those things, we've ended up with nearly 40 million ounces in the measured category, 222 million ounces measured and indicated."

Project Readiness in a Dynamic Market Environment

Development Visibility & Operational De-Risking

Operational visibility provides institutional investors with measurable risk mitigation. Americas Gold & Silver's Galena Complex contains 140-160 million ounces of silver resources with high-grade ore averaging 980 grams per tonne over 3.4 meters. The company's planned operational upgrades, including long-hole mining implementation and batch plant installations, are designed to restore production to historical levels of 5.6 million ounces annually.

The EC120 zone at the company's Mexican operations is expected to deliver materially higher grades by Q4 2025, providing near-term production growth catalysts that institutional investors can model with confidence.

Low-Capex: High-Impact Models

Alternative extraction approaches are attracting institutional attention for their capital efficiency and reduced technical risk. Cerro de Pasco Resources' tailings reprocessing operation targets 10,000-20,000 tonnes per day with modeled profits reaching $610 million annually at operational costs below $2 per tonne. The approach eliminates traditional exploration and permitting risks while leveraging existing mineral inventory. Cerro de Pasco Resources' Executive Chairman Steven Zadka explained:

"There's less mining risk in the sense that it's all above surface and therefore there's a cost component to that, you save a lot of money,"

Feasibility Timelines & Resource Visibility

Project timelines aligned with silver market cycles provide institutional investors with strategic entry points. Vizsla Silver's feasibility study, expected in H2 2025, builds upon approximately 86.1 million ounces of measured and indicated resources with an 86% internal rate of return and $1.1 billion net present value at current silver prices.

The company's bulk sampling program validates metallurgical assumptions while the ongoing 10,000-meter drilling campaign targets high-priority expansion areas within the vastly underexplored Panuco district.

Thematic Exposure & Resource Allocation Strategies

Aligning Exposure with Long-Term Demand Trends

Industrial re-onshoring, energy transition acceleration, and defense application expansion create multiple demand vectors for silver that traditional supply sources cannot sustainably meet. This multi-vector demand profile appeals to institutional investors seeking exposure to structural economic trends rather than cyclical commodity price movements.

Companies with pure-play silver exposure command premium enterprise value multiples in bullish silver markets. Vizsla's pure-play identity and Americas Gold & Silver's 80% silver revenue concentration align with institutional preference for clean thematic exposure without base metal dilution.

The Investment Thesis for Silver

- Exposure to macro themes like inflation hedging, de-dollarization, and energy transition demand

- Jurisdictions offering permitting transparency and low sovereign interference (USA, Mexico, Peru)

- Favorable cost structures with low AISC and minimal capex in near-term production candidates

- Development timelines aligned with projected structural silver deficits

- Operational readiness amid high-grade resource areas, modernized mining techniques, and infill validation

- Optionality for value expansion via exploration, M&A, or strategic metals recovery

- Strategic ESG overlap in reprocessing, community remediation, and energy equity

- Robust institutional backing, allowing execution without dilutive capital raises

Momentum Meets Readiness

The silver market's institutional inflection is evident in capital flows, structural fundamentals, and strategic demand signals. Record ETP inflows, persistent deficits, and industrial demand acceleration are reshaping silver's investment profile from a traditional precious metal allocation to a critical materials play with monetary characteristics.

As institutional capital continues reallocating toward hard assets, companies with tier-one resources, production visibility, and financial discipline are positioned to deliver alpha through the emerging cycle. For institutions seeking strategic exposure, operational leverage, and thematic alignment, silver equities represent a high-conviction macro allocation with multiple value catalysts converging simultaneously.

Analyst's Notes

Subscribe to Our Channel

Stay Informed