Sovereign Metals - A Category Killer for Graphite

Sovereign Metals' Kasiya Project offers investors exposure to the world's only by-product graphite operation with production costs that could undercut even Chinese producers.

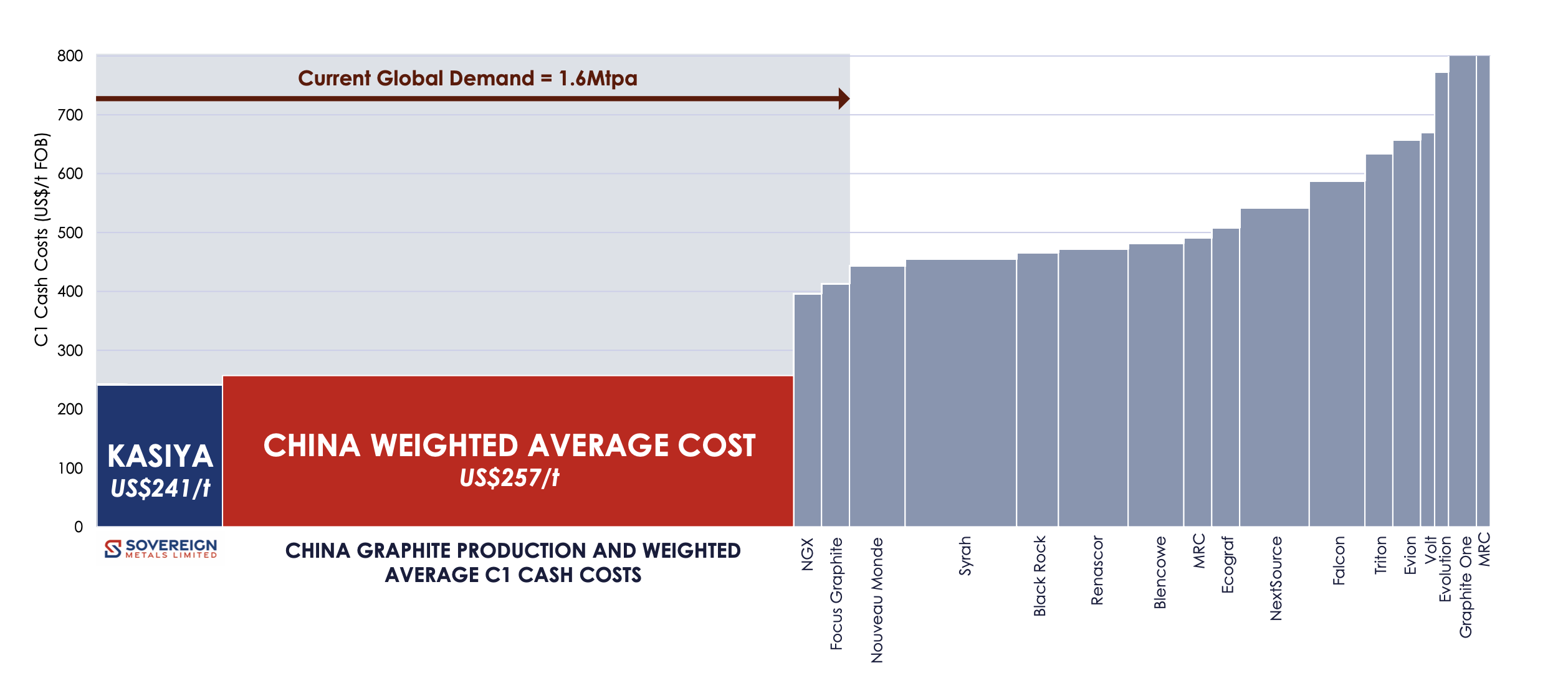

- Kasiya is positioned as a "category killer" in the graphite industry with the world's lowest production costs ($241/t) that can compete directly with Chinese producers ($257/t average).

- Unlike competitors, Kasiya is primarily a rutile project where graphite comes as a by-product, dramatically reducing costs while producing premium large flake graphite.

- A $60 million strategic investment and 19.9% ownership by mining giant Rio Tinto provides technical expertise, validation, and potential pathways to full development.

- Kasiya's weathered ore body yields higher-value graphite with lower processing costs and significantly better flake size distribution (68% medium/large/jumbo flakes versus just 11% at competitor Balama).

- The pre-feasibility study shows a $2.3 billion pre-tax NPV with 64% operating margins and potential to be the world's largest rutile producer while simultaneously disrupting the graphite market.

Sovereign Metals & Kasiya Project

The mining industry occasionally witnesses the emergence of a truly exceptional project - one that can completely redefine the economics of a commodity sector. Sovereign Metals' (ASX: SVM) Kasiya project in Malawi appears to be such a case. As Chairman Ben Stoikovich described in a recent presentation:

"Kasiya was discovered by Sovereign in 2018 and it is a massive deposit. It's world class, covering over 200 square kilometres. It's the largest rutile deposit ever discovered and globally it ranks as the second largest natural graphite deposit."

What makes Kasiya truly unique, however, is its dual-commodity nature. Stoikovich explained:

"The way we think about Kasiya is that it is a primary rutile deposit and the graphite will be produced as a by-product. In fact, it's the only known deposit where graphite is a by-product."

This distinction is crucial for understanding why Kasiya represents such a disruptive force in the graphite market. While most graphite projects must stand on their own economic merits, Kasiya's graphite production costs are partially absorbed by the economics of its primary rutile operation. This creates a cost structure that fundamentally changes the competitive landscape.

The deposit itself is remarkable not just for its size but for its geological characteristics. Located in Malawi, East Africa, it features "blanket-style mineralisation hosted in a soft friable saprolite." In layman's terms, the ore body exists in completely weathered material, which creates significant processing advantages. The soft nature of the ore means it's "free dig" and contains very low levels of sulfur - a critical advantage for graphite destined for the battery anode market.

"Most other graphite projects in the world are hosted in transitional or fresh rock where the ore increases in hardness with depth and sulfur levels," notes Stoikovich. High sulfur content negatively impacts graphite's suitability for battery applications, making Kasiya's low-sulfur product particularly valuable for this growing market segment.

The scale of the resource is staggering. According to the mineral resource estimate, Kasiya contains 17.9 million tonnes of rutile and 24.4 million tonnes of graphite, making it a globally significant deposit for both minerals. With Rio Tinto as a strategic partner holding a 19.9% stake, the project has attracted the attention and backing of one of the world's premier mining companies.

Ben Stoikovich, Chairman of Sovereign Metals

Graphite Production & Market Dynamics

Understanding Kasiya's potential impact requires examining the current state of the global graphite market. Natural graphite demand was approximately 1.6 million tonnes in 2023, with China dominating production at around 1.2 million tonnes per annum - representing approximately 75% of global supply. Chinese producers operate at an average production cost of $257 per tonne, setting the global cost floor. This means that life just got distinctly harder for all the other public graphite companies.

This Chinese dominance creates significant challenges for new entrants. As Stoikovich bluntly states:

"The rest of the world simply cannot compete."

Most non-Chinese graphite projects feature significantly higher production costs, making them economically unviable without moving downstream into value-added processing like battery anode material production.

What makes the Kasiya project remarkable is its potential to break this paradigm. With projected production costs of just $241 per tonne, it would be positioned below even the Chinese average cost curve. Stoikovich emphasised:

"Kasiya is right at the bottom end of the real cost curve and we'll always be able to sell graphite into the market at healthy margins."

The graphite market itself has several challenging characteristics. First, the mineral "isn't scarce" - global known resources exceed 800 million tonnes, representing about 500 years of supply at current demand levels. Second, market pricing is opaque, with no terminal market and widely varying specifications based on flake size and purity. Third, securing development finance can be particularly challenging for graphite-focused projects.

These dynamics have created a situation where many Western graphite projects find themselves high on the global cost curve, struggling to compete with Chinese production. When examining the "real global graphite cost curve" that includes Chinese production, Sovereign's analysis shows why many non-Chinese projects are failing to advance. With China already producing 1.2 million tonnes annually and Kasiya potentially adding another quarter million tonnes at industry-leading costs, "there is unlikely to be demand for many of these higher cost projects unless of course the often predicted dramatic increase in global graphite demand materialises."

This has pushed many competitors to pursue vertical integration strategies into battery anode manufacturing, attempting to capture margins downstream rather than in the mining segment. Sovereign, by contrast, has no need for this approach. Stoikovich stated emphatically:

"Where other companies need to go downstream to capture margin and make a return on investment, we don't need to, and we have no intention to."

Cost Advantages & Flake Size Comparison

Kasiya's competitive advantage extends beyond just low production costs. The deposit's unique weathered geology and simplified processing flow sheet create additional value by preserving graphite flake sizes during extraction.

Stoikovich highlighted this advantage through direct comparison with competitors: "Here we compare the flake sizes we can produce at Kasiya with other graphite mines that are in production around the world. Take for example the Balama mine in Mozambique, owned by the largest listed global graphite producer, Syrah Resources. They mine in transition and fresh rock and they end up with nearly 90% of their graphite product in the low value small flake size category that sells last quarter at a price of around $560 per tonne."

The contrast with Kasiya is striking:

"At Kasiya, with a weathered ore body, only 30% of our product will end up in the small flake size category, with almost 70% in the medium, large and jumbo flake sizes that sell for up to $1,200 US dollars a tonne."

This superior flake size distribution is directly related to the simplified processing flow sheet. Traditional hard-rock graphite operations require multiple energy-intensive steps including drilling, blasting, crushing, and grinding - all of which tend to break down graphite flakes into smaller, less valuable particles. Kasiya's soft, weathered ore allows for a much simpler process involving only loading, hauling, and scrubbing, which helps preserve the larger, premium-priced flake sizes.

The economic impact is substantial. While "small" graphite flakes (-100 mesh) sold for around $564/tonne in Q4 2024, medium flakes commanded $860/tonne and large/jumbo flakes reached $1,140-1,193/tonne. With 68% of Kasiya's production falling into these higher-value categories (compared to just 11% at Balama), the project's revenue potential per tonne is significantly enhanced.

Beyond flake size, Kasiya graphite has demonstrated suitability for all major end markets. Sovereign has completed test work showing their product "can be used for all major end use markets. In fact, it's suitable for 94% of graphite end uses." This includes both battery anode applications and "the far higher value refractories and expandable market."

This versatility is strategically important because it allows Sovereign to target the highest-value markets rather than being constrained to the battery sector. While lithium-ion batteries represent 63% of natural graphite demand, traditional applications like refractories (26%) and expandable graphite (5%) often command premium pricing, especially for larger flake sizes.

Rio Tinto's Strategic Partnership & Project Development

In mid-2023, mining giant Rio Tinto made a strategic investment in Sovereign Metals, providing both capital and technical expertise to advance the Kasiya project. "To date, Rio have invested $60 million and are a 19.9% shareholder," Stoikovich noted, adding that the project "is now overseen by a joint Sovereign-Rio technical committee and a small army of Rio Tinto subject matter experts are closely involved in the project."

This partnership represents significant validation from one of the world's premier mining companies and brings extensive technical and operational expertise to the project. The 19.9% ownership level is particularly noteworthy as it approaches but remains just below the 20% threshold that would trigger mandatory takeover provisions under Australian regulations.

With Rio's backing, Sovereign has achieved several critical development milestones. In 2024, they completed a pilot mining program that provided "substantial empirical data that has informed our forward project design." This real-world operational experience extracted 170,000 cubic meters of material at a 10-hectare site over six months, demonstrating both technical feasibility and environmental sustainability. "We have now rehabilitated the land and returned it to farmers," Stoikovich highlighted. "They didn't even miss a planting season."

The data from this pilot phase informed an optimised pre-feasibility study (PFS) published in January 2025. The economic results were exceptional, showing "a pre-tax NPV of over 2.3 billion US dollars with an annual average EBITDA of over 400 million." The project would position Sovereign as "the world's largest rutile producer" with a 64% operating margin.

Most critically for the graphite strategy, the PFS confirmed:

"Our incremental cost to produce a tonne graphite as a byproduct from the Kasiya project will only be 241 US dollars per tonne."

This extraordinarily low cost basis allows Sovereign to pursue a unique strategy in the graphite market.

Following the successful PFS, the joint Sovereign-Rio team is now advancing toward a definitive feasibility study (DFS) targeted for completion in Q4 2025. This rigorous technical and economic evaluation will further de-risk the project and potentially position it for a final investment decision.

The partnership with Rio Tinto not only enhances technical execution but also significantly improves Kasiya's access to development capital - addressing one of the key challenges facing graphite projects globally. With Rio's backing and Sovereign's exceptional project economics, Kasiya has a clear pathway to becoming a transformative player in both the rutile and graphite markets.

Global Graphite Supply & Demand Challenges

To fully understand Kasiya's potential impact, it's essential to examine the broader graphite market dynamics and the challenges facing both producers and consumers. The industry currently exhibits a stark divide between low-cost Chinese production and higher-cost projects elsewhere.

Stoikovich presented what he described as "the real global graphite cost curve, because it includes China, which up until now, most investors have never seen before." This analysis reveals why "many non-Chinese graphite projects are struggling. They are simply too high on the real cost curve."

The current market structure shows Chinese producers dominating with approximately 1.2 million tonnes of annual production at an average cost of $257 per tonne. Global demand stands at about 1.6 million tonnes annually, leaving space for only the most competitive non-Chinese producers to remain viable.

This has created a challenging environment for Western graphite developers. Most have production costs significantly above Chinese levels, making standalone mining operations difficult to justify economically. As a result, "many of these higher cost projects are aiming to move downstream from mining into battery anode manufacturing in an attempt to capture some form of profitability."

Sovereign's analysis shows most competing projects clustering in the $400-800 per tonne cost range - well above Chinese production costs and the current market prices for most graphite products. For comparison, small flake graphite suitable for battery applications sold for approximately $564 per tonne in late 2024.

This cost disadvantage has pushed many Western graphite companies to pursue vertical integration strategies, developing capabilities in spheronisation, purification, and coating to produce battery-ready anode materials. Companies like Syrah Resources, Nouveau Monde Graphite, NextSource Materials, and others have all announced downstream integration plans to improve project economics.

Kasiya, by contrast, requires no such strategy. With its $241 per tonne cost structure, it would be profitable selling graphite concentrate directly into the market, even at current price levels. Stoikovich emphasised:

"We are a mining company, not a chemistry company. Kasiya will potentially compete with low-cost Chinese production even in today's market."

This fundamental cost advantage positions Sovereign to potentially disrupt the global graphite supply landscape. If Kasiya advances to production at its projected 265,000 tonnes per annum of graphite, it would represent a significant portion of the non-Chinese supply and could potentially reshape industry dynamics.

As Stoikovich summarised:

"Kasiya is the best graphite project in the world because it's actually a high value, rutile titanium project where the graphite comes out as a byproduct at the very, very low cost of $241."

For Investors: Kasiya's Competitive Edge in Graphite Production

The Kasiya project represents a potential paradigm shift in the graphite industry - a "category killer" that combines unprecedented production costs with premium product characteristics. While most competing projects struggle to justify standalone economics, Kasiya's by-product strategy creates a fundamentally different cost structure that could allow it to thrive even in challenging market conditions.

Sovereign's approach differs markedly from industry peers. Rather than pursuing vertical integration into battery materials to capture margins, the company is focusing on its core strength as a mining operation. "Where other companies need to go downstream to capture margin and make a return on investment, we don't need to," Stoikovich explained.

The project's advantages are multi-faceted:

- Unmatched Cost Position: At $241 per tonne, Kasiya would be the lowest-cost graphite producer globally, undercutting even Chinese operations.

- Premium Product Quality: The weathered ore body yields high-quality graphite with very low sulfur levels and superior flake size distribution (68% medium/large/jumbo).

- Dual-Commodity Resilience: As primarily a rutile project with graphite as a by-product, Sovereign offers investors exposure to two distinct markets, reducing single-commodity risk.

- Market Versatility: Test work confirms suitability for 94% of graphite end uses, including higher-value traditional markets like refractories and expandables.

- Tier-1 Strategic Partner: Rio Tinto's $60 million investment and 19.9% ownership provides technical expertise, financial backing, and potential pathways to full development.

- Exceptional Project Economics: The optimised PFS demonstrates robust financial returns with a $2.3 billion pre-tax NPV and 64% operating margins.

- Market Disruption Potential: As the only graphite producer that doesn't need to "go downstream" to be profitable, Sovereign could fundamentally reshape industry economics and potentially eliminate competing higher-cost projects.

The implications for the graphite market could be profound. As Stoikovich noted:

"With China already producing 1.2 million tonnes per year and Kasiya potentially contributing a further quarter of a million tonnes, there is unlikely to be demand for many of these higher cost projects."

This suggests Kasiya could effectively crowd out competing developments, particularly those without downstream integration strategies.

For investors, Sovereign offers exposure to a potentially transformative project in the critical minerals space, backed by one of the world's premier mining companies. While many graphite developers face challenging economics and uncertain demand growth, Kasiya's dual-commodity nature provides significant risk mitigation and a clear path to profitability even in conservative market scenarios.

Macro Analysis: Critical Minerals in a Changing Landscape

The global transition to renewable energy and electrification continues to drive demand for critical minerals, creating both opportunities and challenges for resource developers. Natural graphite occupies a unique position in this transition - while essential for lithium-ion battery anodes, it faces a complex supply-demand balance that differs markedly from other battery materials.

Unlike lithium or cobalt, which have experienced severe supply constraints, natural graphite is abundant globally. As Sovereign notes, "known global resources are over 800 million tonnes" - sufficient for approximately 500 years at current consumption rates. This abundance means the key differentiator for successful projects isn't resource size but rather production costs and product quality.

China's dominance in graphite processing represents both a supply security concern for Western economies and a competitive challenge for non-Chinese producers. The United States and European Union have both classified graphite as a critical mineral, emphasising the need for supply diversification. This has created supportive policy environments for projects outside China, including potential financial incentives and strategic partnerships.

However, the fundamental economics of graphite production remain challenging. As Sovereign highlights, China produces approximately 75% of global supply at an average cost of $257 per tonne - a benchmark that most Western projects cannot match. This has pushed many developers toward downstream integration, attempting to capture margins in anode material production rather than mining operations.

The battery industry's rapid growth presents both opportunities and risks. While graphite demand is projected to increase substantially if electric vehicle adoption continues its current trajectory, technological developments could potentially disrupt this outlook. Silicon-graphite composite anodes are already entering commercial use, reducing graphite intensity per battery. More speculative technologies like solid-state batteries could potentially reduce graphite requirements further, though commercial timelines remain uncertain.

Within this complex landscape, Kasiya's by-product strategy offers a uniquely resilient position. Unlike pure-play graphite developers, Sovereign's economics are not entirely dependent on graphite market dynamics. The primary rutile operation provides both revenue diversification and the cost subsidy that enables industry-leading graphite production costs. This creates a fundamental competitive advantage that transcends near-term market fluctuations.

For investors considering the critical minerals space, this dual-commodity exposure offers an alternative to pure-play battery material investments while maintaining exposure to the energy transition theme. Sovereign effectively provides optionality on both the traditional titanium dioxide market (through rutile) and the emerging battery supply chain (through graphite) - a diversification that few junior resource companies can match.

Analyst's Notes

Subscribe to Our Channel

Stay Informed