TC/RC Market Breakdown & Copper Supply Realignment: Why Investors Must Reassess the Concentrate-Dominant Cycle

Copper TC/RCs hit minus $60/t in 2025 as China dominates refining. Bilateral pricing replaces benchmarks. Developers like Marimaca & explorers like Fitzroy gain.

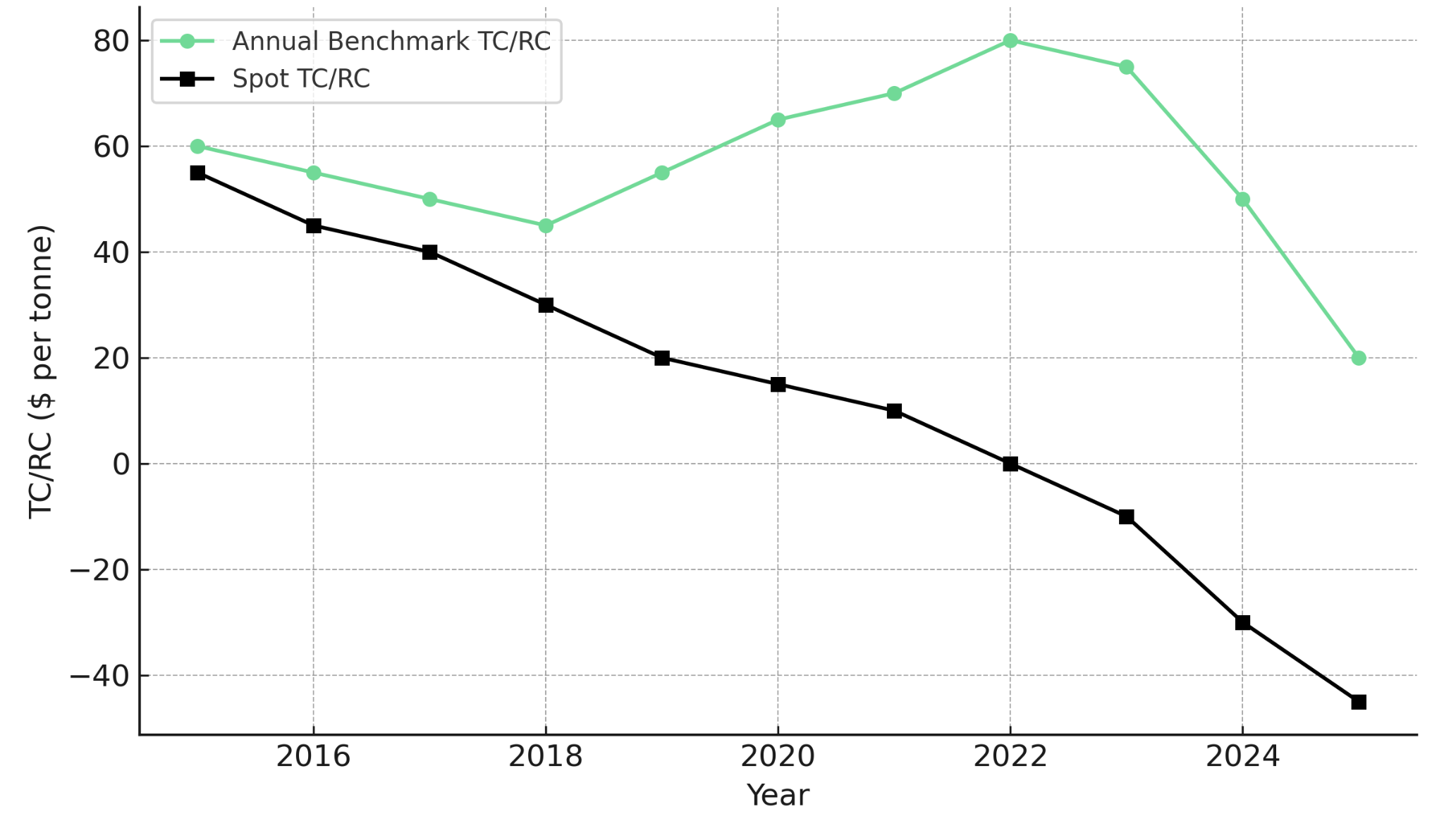

- The global copper market is undergoing its most extreme structural stress in decades, with treatment and refining charges (TC/RCs) collapsing to negative territory (minus $60 per tonne in 2025), a signal of acute concentrate scarcity and an unraveling of the benchmark pricing system that has governed commercial relationships for over two decades.

- China's smelting expansion, rising refined output (+9.7% year-over-year through October 2025), and dominance of concentrate procurement are crowding out non-Chinese smelters, triggering closures, bailouts, and forced coalitions in Japan, Korea, and Spain as margin compression reaches unsustainable levels.

- This new environment strengthens the strategic positioning of low-cost developers such as Marimaca Copper and high-grade discovery explorers such as Fitzroy Minerals as concentrate availability becomes the defining constraint on global supply and asset scarcity value intensifies.

- Analysts expect a shift away from the China-driven annual benchmark toward bilateral agreements, quarterly pricing, and capped TC/RC structures, reshaping commercial relationships between miners and smelters and introducing greater negotiation flexibility into off-take contracts.

- Investors must understand how this structural shift supports long-term copper prices, elevates asset scarcity value, and enhances the economics of well-positioned projects in Tier-1 jurisdictions, particularly those capable of bypassing the concentrate bottleneck or delivering high-grade discoveries aligned with supply-tight conditions.

A Global Pricing System Under Stress

The copper market is now facing a structural realignment that challenges the assumptions underlying two decades of supply-chain coordination. Treatment and refining charges (TC/RCs), which determine how revenues are split between miners and smelters, have collapsed into unprecedented negative territory. Spot charges falling to minus $60 per tonne in November 2025 represent the most acute signal of physical scarcity in the concentrate market since China's rapid smelting expansion began more than a decade ago.

This breakdown reflects the convergence of structural supply constraints, geopolitical fragmentation, and China's strategic dominance of refining capacity. The annual benchmark system, once a stable reference point for global contracts, is now being questioned by major miners and smelters alike as physical tightness renders traditional pricing mechanisms inadequate.

This article analyzes the macroeconomic forces and structural supply constraints reshaping the copper industry, examining how developers such as Marimaca Copper and explorers such as Fitzroy Minerals fit into this evolving landscape as capital shifts toward assets aligned with tight-supply conditions.

The Breakdown of the Copper TC/RC System

The crash in annual TC/RCs reflects a structural imbalance driven by concentrate shortages and overbuilt smelting capacity. Spot charges below zero indicate that smelters are now subsidizing miners, a reversal of traditional pricing incentives. Major miners, including Freeport-McMoRan, have signaled their intention to find alternatives to the benchmark as the system fails to reflect supply-demand realities.

Smelters operating under negative TC/RCs rely on by-product credits, particularly sulfuric acid, to offset losses. Chinese smelters benefit from surging sulfuric acid prices, which helps them mitigate the effects of low TC/RCs and maintain profitability even when concentrate processing margins are negative.

Emerging Alternatives to the Benchmark

CRU Group analyst Craig Lang expects a further breakdown of the annual benchmark system, with potential outcomes including bilateral agreements, possibly at different levels to the Chinese annual benchmark, and quarterly pricing. Several producers have discussed implementing caps and floors to protect smelters from prolonged losses while ensuring miners retain exposure to upside pricing during tight markets.

Developers such as Marimaca Copper and explorers such as Fitzroy Minerals are entering a copper market where negotiation norms are shifting. Future concentrate suppliers in this environment will benefit from greater contractual flexibility, particularly if they can demonstrate high-grade resources or the ability to produce cathode directly, bypassing the concentrate market entirely.

Structural Scarcity: Concentrate Tightness as the New Normal

The tightness in copper concentrate supply is structural. Years of disruptions at major mines, declining grades in aging districts, and permitting delays in Tier-1 jurisdictions have reduced the availability of new supply. Concentrate availability, rather than smelting capacity, has become the binding constraint on global refined copper production.

Mine Closures & Grade Declines Shift Market Power

Average head grades across major producers continue to decline, reducing concentrate output even when mining rates remain stable. Expansion capital for new mines remains constrained due to environmental, social, and governance (ESG) pressures and long permitting timelines.

Marimaca Copper's oxide-focused project is designed to produce Grade A cathode via heap leach and solvent extraction-electrowinning (SX-EW), avoiding exposure to the concentrate bottleneck. The project received formal environmental approval (RCA) in November 2025 and completed its definitive feasibility study in August 2025, demonstrating post-tax net present value of $709 million at an 8% discount rate and 31% internal rate of return, assuming a long-term copper price of $4.30 per pound.

Marimaca's President and Chief Executive Officer, Hayden Locke, highlights exceptional oxide mineralization at Pampa Medina:

"The first is that oxide intersection which was nearly 50 meters at 2% in a broader zone of 160 meters at 1%. That is a material extension to the oxide envelope and certainly higher grade than what our current interpretation of the block model is."

Exploration Becomes Critical to Filling the Gap

Fitzroy Minerals' Caballos porphyry intercept in drill hole CAB-DDH001 (200 meters at 0.46% copper with molybdenum and gold credits totaling 0.81% copper equivalent) represents the type of new discovery needed to offset global production declines.

Gilberto Schubert, Chief Operating Officer and Country Manager, describes the drilling success:

"We got 200 meters with copper, molybdenum, and gold, pure sulfide mineralization, chalcopyrite plus molybdenite... We have a very important amount of molybdenite in the breccia and also the gold because gold was very sporadic in surface but in the drill hole we have a continuous zone with more than 80 meters with gold. So it was a very good surprise for us."

China's Dominance & the Emerging Geopolitical Realignment

China continues to expand smelting capacity despite collapsing TC/RCs. China produced 9.7% more refined copper in the year through October 2025, driven by new smelter capacity brought online despite the collapse in TC/RCs.

Pressure on International Smelters Creates Policy Response

Non-Chinese smelters face severe margin contraction. Japan's JX Advanced Metals announced an output cut running into tens of thousands of tonnes in 2025, while Mitsubishi Materials stated conditions have significantly deteriorated. Glencore received a government bailout to keep its Mount Isa smelter and refinery in Australia running for another three years. The industry ministries of Japan, South Korea, and Spain issued a joint statement in late 2025 criticizing punitive TC/RCs.

These policy responses reflect growing recognition that smelting capacity has strategic value beyond market economics. Governments are increasingly willing to subsidize smelters to maintain domestic refining capability.

Strategic Implications for Developers & Explorers

Miners operating in stable, transparent jurisdictions become more attractive as smelters seek diversified supply sources. Chile is consistently characterized as a Tier-1 mining jurisdiction with predictable permitting processes and proximity to global shipping routes.

Schubert emphasizes Chile's jurisdictional advantages:

"We are close to Copiapó, one of the main mining towns in Chile, close to the Panamericana Road, to the main power grids of Chile, 40 kilometers to the coast in the middle of the desert. This type of location makes the projects easier and faster to be built."

How Copper Developers & Explorers Fit Into the New Supply Chain Reality

Marimaca's low capital intensity ($11,700 per tonne of installed capacity) aligns with investor preference for projects with clear margins under volatile cost structures. As of September 30, 2025, the company held $78.7 million in cash. The project is targeting final investment decision in the second half of 2026, with construction anticipated to begin in the third or fourth quarter of 2026.

Fitzroy Minerals, with C$11 million in cash as of November 2025, has allocated C$8 million for exploration in 2026, split equally between the Buen Retiro heap leach project and the Caballos porphyry discovery. This budget is fully funded by existing cash resources.

Project Milestones & Operational Visibility

Marimaca is currently executing a 10,000-meter extensional drilling program to define the Pampa Medina sulfides. The company is completing a standalone preliminary economic assessment for the Pampa Medina oxides, targeting delivery by year-end 2025. High-grade sulfide intercepts include 26 meters of 4.1% copper from 580 meters (including 6 meters of 12.0% copper) in drill hole SMRD-13.

Hayden Locke describes execution priorities:

"We celebrated our permit being awarded. We're starting to turn our attention to the execution strategy right now and in fact we're in the planning phase of all of the key hires that we need to make in the short and medium term."

Fitzroy's dual-asset strategy reduces project-level risk while maintaining exposure to discovery upside. The company has an option for 100% of the Buen Retiro project, with Pucobre S.A. holding a 30% clawback right exercisable by August 2028. The high-grade vein material at Buen Retiro offers near-term production optionality, while the Caballos porphyry provides long-term resource scale.

The presence of rhenium alongside molybdenum at Caballos adds by-product value. Schubert notes the project contains approximately 0.5 grams per tonne of rhenium. Chile is the second-largest rhenium producer globally, and the metal commands significant pricing premiums due to its use in superalloys for jet engines.

The Investment Thesis for Copper

- Structural concentrate scarcity driven by declining head grades, mine disruptions, and the collapse of smelter economics signals a tightening market that supports long-term copper prices and enhances the economics of well-positioned development and exploration assets.

- An unstable pricing framework creates opportunities for miners to negotiate bilateral agreements that offer greater contractual flexibility and upside exposure during tight markets, while smelters gain protection from prolonged losses through capped TC/RC structures.

- Geopolitical diversification accelerates investment toward copper assets in politically stable, mining-friendly jurisdictions as China's dominance of smelting capacity forces non-Chinese participants to seek alternative supply sources.

- Favorable economics for developers position low-cost, low-complexity projects such as Marimaca's cathode operation as strategic alternatives to concentrate-exposed assets, particularly as smelters face insolvency pressure and traditional off-take relationships deteriorate.

- High-grade discoveries gain scarcity value as the exploration success rate declines and the concentrate market tightens, with porphyry intercepts such as Fitzroy's Caballos discovery demonstrating the kind of new supply the system increasingly requires to offset production declines at aging mines.

- Capital rotation toward execution favors companies with permitting visibility, strong balance sheets, and clear development milestones, as investors shift toward assets capable of delivering near-term production or high-impact discoveries in supply-tight conditions.

A Copper Market Redefined by Scarcity, Strategy & Structural Change

The breakdown of the TC/RC system marks a fundamental shift in how copper is priced, traded, and supplied. China's aggressive expansion and the resulting pressure on smelters outside its borders are forcing the market into a new structure defined by bilateral agreements, concentrated scarcity, and geopolitical realignment.

For investors, the value is migrating upstream toward quality copper developers and explorers aligned with supply-tight conditions, located in stable jurisdictions, and capable of delivering low-cost production or high-impact discovery potential. The concentrate-dominant cycle is being redefined by structural scarcity, geopolitical fragmentation, and the collapse of legacy pricing mechanisms.

TL;DR

The global copper market faces unprecedented stress as treatment and refining charges collapse to minus $60 per tonne, signaling acute concentrate scarcity. China's 9.7% increase in refined output through October 2025 is crowding out international smelters, forcing production cuts in Japan and government bailouts in Australia. The annual benchmark pricing system is breaking down, with analysts expecting a shift toward bilateral agreements and quarterly pricing. This structural change benefits low-cost developers like Marimaca Copper, which bypasses the concentrate market through cathode production, and high-grade explorers like Fitzroy Minerals with significant porphyry discoveries. Investors should focus on projects in Tier-1 jurisdictions with strong balance sheets, permitting clarity, and the ability to navigate the new supply chain reality defined by concentrate scarcity and geopolitical realignment.

FAQs (AI-Generated)

Treatment charges and refining charges (TC/RCs) determine how revenues are split between copper miners and smelters. They serve as a critical pricing mechanism in the concentrate market. When TC/RCs collapse to negative territory (minus $60 per tonne as of November 2025), it signals extreme concentrate scarcity and indicates smelters are subsidizing miners—a complete reversal of traditional economics that threatens the viability of smelting operations outside China.

China produced 9.7% more refined copper year-over-year through October 2025 by continuing to expand smelting capacity despite collapsing TC/RCs. Chinese smelters maintain profitability through by-product credits, particularly surging sulfuric acid prices, which offset negative concentrate processing margins. This scale advantage allows China to dominate concentrate procurement, crowding out international competitors and forcing production cuts and government bailouts in Japan, Australia, Korea, and Spain.

The breakdown creates strategic advantages for projects that bypass the concentrate market entirely, such as Marimaca Copper's cathode operation via heap leach and SX-EW processing. High-grade discoveries like Fitzroy Minerals' Caballos porphyry (200 meters at 0.81% copper equivalent) gain scarcity value as concentrate becomes the binding constraint on global supply. Projects in Tier-1 jurisdictions with low capital intensity, strong balance sheets, and permitting clarity attract disproportionate investor interest.

Analysts expect bilateral agreements negotiated directly between miners and smelters, possibly at different levels than the Chinese benchmark, along with quarterly pricing mechanisms that allow more frequent adjustments to reflect physical market conditions. Producers are discussing caps and floors to protect smelters from prolonged losses while ensuring miners retain upside exposure. This shift provides greater contractual flexibility but introduces execution risk for both parties.

Governments recognize that smelting capacity has strategic value beyond market economics, particularly for defense industries, renewable energy infrastructure, and export-oriented manufacturing. Australia provided a bailout to keep Glencore's Mount Isa smelter operating for three more years, while Japan, South Korea, and Spain issued a joint statement criticizing punitive TC/RCs. These interventions reflect concerns about supply chain security and the concentration of refining capacity in China.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed