Thor Exploration Generates $70 Million Quarter Revenue Supporting Multiple 2026 Development Catalysts Across African Assets

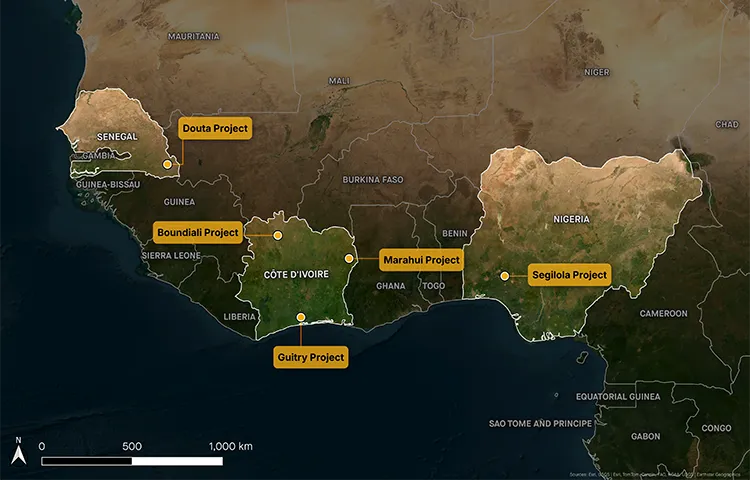

Thor Explorations: Nigerian gold producer advances Senegal project to construction whilst drilling extends Segiola mine life and Côte d'Ivoire discoveries materialise.

- Thor Explorations operates the 100%-owned Segilola gold mine in Nigeria, producing 90,000–95,000 ounces annually at all-in sustaining costs below $1,000 per ounce, generating operating margins exceeding $3,000 per ounce at current gold prices above $4,000, which enables the company to pay quarterly dividends whilst self-funding aggressive exploration and development programmes across West African jurisdictions without equity dilution.

- The company produced 22,600 ounces in Q3 2025 and strategically withheld 3,000 ounces to sell in Q4 at prices above $4,000 per ounce, generating approximately $70 million in quarterly revenue whilst maintaining a debt-free balance sheet, creating financial flexibility for capital allocation decisions across its multi-stage project pipeline.

- Thor has deployed five drilling rigs exploring beneath the Segilola pit, intersecting high-grade underground mineralization averaging 5.5 grams per tonne (g/t) alongside satellite deposits within a 50-kilometre radius, with an updated resource estimate targeted for Q1 2026.

- The Douta project in Senegal is weeks away from completing a preliminary feasibility study with capital costs estimated at $250–$300 million, of which $150 million will be self-funded from operational cash flows, targeting first gold production in Q1 2028 following an investment decision expected in H1 2026, which would materially increase Thor's production profile through a larger resource base with 10 years of mine life.

- Early-stage exploration success in Côte d'Ivoire has delineated six mineralized lenses at Guitry with high-grade intersections, whilst the Marahui project has identified 8 kilometres of drill targets with surface rock chips returning 10–17 g/t, both advancing toward maiden resource estimates in H1 2026 with continuous drilling programmes funded entirely from internal cash generation.

Strong Operational Performance Generates Investment Capacity

Thor Explorations' Segilola gold mine in Nigeria generates the cash flows underpinning an aggressive exploration and development strategy spanning near-term mine life extension, advanced-stage project construction, and genuine greenfield discoveries in Senegal and Côte d'Ivoire. CEO Segun Lawson explains, the company has positioned itself to capitalise on the current gold price environment through operational efficiency and strategic optionality:

"We are in our fourth calendar year of production. We are looking to produce about between 90,000 and 95,000 ounces of gold this year, that enables us to fund internally our exploration activities across West Africa."

Thor Explorations' Q3 2025 operational results demonstrate the financial strength underpinning the company's growth strategy. The company produced 22,600 ounces during the typically challenging rainy season quarter, selling 19,600 ounces at just over $3,500 per ounce to generate approximately $70 million in revenue. The decision to withhold 3,000 ounces for sale in Q4 at prices above $4,000 per ounce exemplifies management's tactical approach to metal sales optimization.

The company's all-in sustaining costs below $1,000 per ounce create substantial operating margins at current gold prices. This margin expansion has enabled Thor to return quarterly dividends to shareholders whilst simultaneously funding an extensive drilling campaign across three countries. Thor has completely repaid its project debt, strengthening its balance sheet month-on-month and creating flexibility for capital allocation decisions. The debt-free status represents a significant milestone for a company that financed Nigeria's first gold mine and provides strategic optionality for future development decisions.

Segilola Mine Life Extension: Converting Success into Value

The Segilola operation represents Thor's immediate value creation opportunity. With all infrastructure capital expenditure already sunk and operational expertise established, every additional ounce discovered creates what Lawson characterizes as "super ounces" – mineralization that requires minimal incremental capital to extract.

The company has deployed five drilling rigs beneath the existing pit, systematically testing extensions of the high-grade ore body. Underground drilling has intersected mineralisation averaging 5.5 grams per tonne (g/t), compared to the open pit grade of just over 4 g/t. Whilst underground mining will inevitably increase unit costs, substantial margins remain viable even at conservative gold price assumptions.

Thor targets an updated resource estimate in Q1 2026, though management emphasises this represents a milestone rather than a comprehensive assessment. The drilling programme continues to expand the known mineralisation envelope, with work focused on both a shallow-dipping plunge in the south and a steeply dipping chute in the north. This dual-zone approach aims to maximise throughput by mining from multiple areas simultaneously.

The company has also recalibrated pit optimisation parameters to reflect current metal prices.

As Lawson explains, "When we did the bankable feasibility study, gold was at $1,600 per ounce. At the beginning of the year, gold was at $2,600 per ounce. So the pit design can be optimised certainly at $4,000 and taken deeper in the south where we are to try and recover additional ounces before we transition into that underground."

Beyond the main Segilola deposit, Thor has established a 50-kilometre exploration radius around the processing plant, identifying multiple satellite deposits suitable for toll treatment. These smaller, high-grade deposits averaging approximately 5 g/t can be mined and stockpiled for processing, extending the plant's productive life without major capital investment.

The company plans a pilot mining operation in 2026 at one southern target, having completed permitting and land acquisition. This material will supplement an existing stockpile of over 44,000 ounces grading 0.85 g/t – representing more than $175 million in contained gold value at $4,200 per ounce gold prices.

Interview with Segun Lawson, CEO, Thor Explorations Ltd

Douta Project: Near-Term Production Growth in Senegal

Thor's Douta project in Senegal represents the company's most advanced growth opportunity, with a preliminary feasibility study completion imminent. This detailed engineering work, conducted alongside EPC and mining contractors over 18 months, provides the foundation for a rapid transition to construction. Lawson emphasises the study's practical orientation:

"The project economics are certainly material to the value of the company and it's a very detailed PFS using real quotes with our real contractors. So it's not an academic study."

The capital cost estimate ranges between $250 to $300 million, with Thor Exploration planning to self-fund $150 million from existing cash flows and operational proceeds. The remaining $100 million would be sourced through debt financing, eliminating equity dilution. Thor maintains a strong relationship with Africa Finance Corporation, which financed the Segilola project and holds an equity stake in the company.

Management targets first gold production in Q1 2028 following an investment decision in the first half of 2026 and equipment orders beginning in Q1 or early Q2 2026. Permitting has progressed for approximately one year, with full approval expected by June 2026 following environmental impact assessment validation. The project features a larger resource base than Segilola albeit at lower grades with a mine life targeted at approximately ten years. This production profile would materially increase Thor's consolidated output and provide geographic diversification within the West African gold sector.

Lawson highlights the contrast with Thor's previous financing experience:

"When we were in Nigeria, we had to tick all the boxes and get the financing. Even from signing the financing deal to our first draw down was 14 months. Here, whilst we're getting our finances in place, we have the ability because we have cash flow from Nigeria, we have the ability to pay for long lead items, the mills, and we have the ability to start doing earthworks."

Côte d'Ivoire Exploration: Early-Stage Resource Upside

Thor's Côte d'Ivoire portfolio encompasses two projects at different exploration stages, both demonstrating characteristics consistent with significant gold systems. The Guitry project, acquired from Endeavour Mining, has advanced from surface geochemistry to resource definition drilling, whilst the Mari project has just commenced its maiden drilling programme.

At Guitry, Thor reinterpreted geological data and redesigned the drilling approach following acquisition. The company completed 4,600 metres of drilling earlier in 2025, delineating six parallel mineralised lenses that remain open along strike and at depth. High-grade intersections include 10 metres at 10 g/t, 10 metres at 9 g/t, and 2 metres at 16 g/t. The company has designed drill programmes for two additional areas within this footprint and has drilling underway. An extended rainy season and presidential elections in Côte d'Ivoire delayed the programme by nearly two months, pushing the maiden resource estimate into the first half of 2026, though the company now has eight months of dry season drilling ahead.

The Marahui project presents a compelling greenfield opportunity with 8 kilometres of drill targets identified across two structures. Surface rock chip samples from in-situ bedrock have returned grades of 10–17 g/t along the entire strike length of drilling targets. Whilst rock chip results require drill confirmation, the consistency and continuity of high-grade surface mineralisation provide encouragement ahead of the maiden drilling programme that has just commenced.

Thor plans continuous drilling at Marahui through to the July rainy season, aiming to define the system's geometry and extent before pursuing resource estimation. The project's early stage provides significant blue-sky potential should drilling confirm the surface geochemical indicators.

Financial Strength Enables Portfolio Approach

Thor's operational success at Segilola has created the financial capacity to advance multiple projects simultaneously without external capital requirements. The company's internally funded exploration programmes span three jurisdictions and multiple development stages, from advanced feasibility studies through greenfield drilling.

This self-funding capability provides management with disciplined acquisition criteria. When questioned about potential M&A activity in the current market environment, Lawson emphasized the quality of Thor's internal pipeline:

"When we look at inorganic opportunities then it has to be extremely compelling to leapfrog what we have. It's expensive out there and I think we've got great projects internally to leapfrog what we have internally in terms of use of cash."

The company's balance sheet strength, debt-free status, and quarterly dividend capacity demonstrate management's confidence in sustaining current operational performance whilst funding growth initiatives. The strategic flexibility this creates extends to construction financing options, with corporate debt, revolving facilities, and project finance all viable alternatives to traditional development funding.

Multiple Catalysts Through 2026

Thor enters 2026 with numerous value catalysts across its portfolio:

- The Douta preliminary feasibility study release will provide the first economic assessment of the Senegal project, followed by investment decision-making and equipment ordering in H1 2026.

- The Segilola resource update in Q1 2026 will quantify underground potential and satellite deposit aggregation.

- Maiden resource estimates at both Guitry and Marahui in H1 2026 will establish these projects' scale and quality.

Operationally, the company expects continued strong financial performance supported by elevated gold prices and operational efficiency. Lawson anticipates:

"Another potentially transitional year for us next year – more production, hopefully stabilized gold prices where they are, mine life extension, going into construction, and two maiden resources in Côte d'Ivoire."

The Investment Thesis for Thor Exploration

- Cash-Generative Production Base with Exceptional Margins: Thor produces 90,000–95,000 ounces annually from its 100%-owned Segiola mine in Nigeria at all-in sustaining costs below $1,000 per ounce, creating operating margins exceeding $3,000 per ounce at current gold prices above $4,000, which funds quarterly dividends whilst simultaneously financing aggressive exploration and development programmes across three West African jurisdictions without equity dilution.

- Near-Term Mine Life Extension with Low-Risk Resource Growth: The company has deployed five drilling rigs exploring beneath the Segiola pit, successfully intersecting high-grade underground mineralisation averaging 5.5 g/t alongside satellite deposits within a 50-kilometre radius of existing infrastructure, where every additional ounce discovered creates exceptional value given the sunk capital and established operations, with an updated resource estimate targeted for Q1 2026.

- Material Production Growth Through Senegal Development: Thor's Douta project in Senegal is weeks away from completing a preliminary feasibility study with estimated capital costs of $250–$300 million, of which $150 million will be self-funded from operational cash flows, targeting first gold production in Q1 2028 following an investment decision expected in H1 2026, which would materially increase the company's production profile through a larger resource base with approximately 10 years of mine life.

- Genuine Exploration Success Creating Discovery Upside: Early-stage drilling at Guitry in Côte d'Ivoire has delineated six mineralised lenses with high-grade intersections including 10 metres at 10 g/t across just 15% of an 8-kilometre by 5-kilometre geochemical footprint, whilst the Marahui project has identified 8 kilometres of drill targets with surface rock chips returning 10–17 g/t, both advancing toward maiden resource estimates in H1 2026 with continuous drilling programmes through the dry season.

- Financial Strength Enables Self-Funded Growth Without Dilution: Thor's debt-free balance sheet, growing cash position, and quarterly dividend capacity demonstrate operational resilience whilst providing the financial flexibility to simultaneously advance multiple projects across different development stages, eliminating reliance on equity markets or external financing for exploration and eliminating equity dilution risk for the Douta construction phase.

- Geographic and Stage Diversification Reduces Portfolio Risk: The company's portfolio spans a producing asset in Nigeria, an advanced development project in Senegal weeks from feasibility completion, and two early-stage exploration projects in Côte d'Ivoire, creating a phased development timeline that spreads capital deployment across multiple years whilst management's proven track record delivering Nigeria's first gold mine provides execution credibility.

- Multiple Near-Term Catalysts Through 2026: Investors can expect the Douta preliminary feasibility study release providing first economic assessment of the Senegal project, an updated Segiola resource estimate quantifying underground and satellite deposit potential in Q1 2026, maiden resource estimates at both Guitry and Marahui in H1 2026, construction decision-making and long-lead item ordering at Douta, and continued strong operational cash generation supported by elevated gold prices.

Macro Thematic Analysis: High-Grade Gold Production as Portfolio Ballast in Uncertain Markets

Gold's advance above $4,000 per ounce reflects a fundamental shift in institutional positioning and central bank behaviour, driven by concerns about sovereign debt sustainability, currency debasement through persistent fiscal expansion, and geopolitical fragmentation. This environment particularly favours producers with low-cost, high-grade operations capable of generating substantial free cash flow across various price scenarios.

Thor Explorations exemplifies the strategic value of high-grade assets in the current cycle. With all-in sustaining costs below $1,000 per ounce, the company captures operating margins exceeding $3,000 per ounce at current prices – creating financial resilience that enables organic growth funding without reliance on equity markets or commodity price volatility. This self-sufficiency becomes increasingly valuable as capital markets potentially reprice risk amid broader macro uncertainty.

The gold sector faces a structural challenge where reserve replacement has lagged production for over a decade, creating scarcity value for companies demonstrating genuine exploration success. Thor's Côte d'Ivoire discoveries and Segiola resource expansion occur against this backdrop of industry-wide discovery deficit, potentially attracting strategic interest from larger producers seeking to replenish depleting inventories.

As CEO Segun Lawson articulates:

"We are also in a very healthy financial position given our low costs of below $1,000 per ounce and the prevailing high gold prices, that's enabled us to return dividends back to our shareholders on a quarterly basis, where our value is underpinned by a very strong cash flow and profitability. However, we do think we continue to be a growth company with a very strong organic pipeline diversified by stage of development and jurisdiction."

West Africa's emergence as a premier gold jurisdiction benefits from established infrastructure, supportive fiscal regimes designed to attract investment, and geological prospectivity demonstrated by major discoveries over the past two decades. Thor's multi-jurisdictional approach across Nigeria, Senegal, and Côte d'Ivoire provides geographic diversification whilst maintaining regional operational synergies and shared regulatory familiarity.

TL:DR

Thor Explorations operates Nigeria's Segilola gold mine producing 90,000–95,000 ounces annually at all-in sustaining costs below $1,000 per ounce, creating operating margins exceeding $3,000 per ounce that fund quarterly dividends and aggressive organic growth without equity dilution. The company has completely repaid project debt and generated approximately $70 million in Q3 2025 revenue. Thor is pursuing mine life extension at Segilola through five drilling rigs exploring high-grade underground mineralisation averaging 5.5 g/t with a resource update targeted for Q1 2026. The Douta project in Senegal is weeks from completing a preliminary feasibility study with $250–$300 million capital costs, targeting Q1 2028 production with $150 million self-funded and investment decision expected H1 2026. Early-stage exploration at Guitry in Côte d'Ivoire has delineated six mineralised lenses with high-grade intersections whilst Marahui has identified 8 kilometres of drill targets, both targeting maiden resources H1 2026. Thor's debt-free balance sheet, cash-generative operations, and multi-jurisdictional portfolio spanning producing assets through greenfield discoveries create a phased development timeline with multiple near-term catalysts throughout 2026 whilst eliminating reliance on equity markets for growth funding.

Frequently Asked Questions (FAQs) AI-Generated

Thor combines immediate cash generation from low-cost, high-grade production (sub-$1,000 AISC, 90,000–95,000 ounces annually) with a self-funded, multi-stage development pipeline spanning three jurisdictions. The company's debt-free balance sheet and operating margins exceeding $3,000 per ounce enable simultaneous advancement of mine life extension, advanced-stage project construction, and genuine greenfield exploration without equity dilution. This financial strength provides strategic flexibility unusual amongst mid-tier producers, allowing Thor to order long-lead items and commence earthworks at Douta prior to debt closure whilst maintaining quarterly dividends and aggressive exploration programmes.

Near-term catalysts include the Douta preliminary feasibility study release (imminent, providing first economic assessment of the Senegal project), Segilola resource update in Q1 2026 (quantifying underground potential and satellite deposits), maiden resource estimates at Guitry and Marahui in H1 2026 (establishing scale of Côte d'Ivoire discoveries), investment decision and equipment ordering for Douta construction in H1 2026, pilot mining operation at southern satellite deposit, and continued operational cash generation with Q4 2025 potentially delivering record quarterly financial performance following strategic metal sales above $4,000 per ounce.

Thor will self-fund $150 million from operational cash flows generated by Segilola, leveraging its debt-free balance sheet and substantial operating margins. The remaining $100 million will be sourced through debt financing, with Africa Finance Corporation (which financed Segilola and holds an equity stake) representing the first point of contact. Thor's cash-generative position provides multiple financing options including project finance, corporate loans, or revolving facilities, with management expecting more favourable terms than the original Segilola financing given Thor's established operational track record and improved credit profile. The company can begin ordering long-lead items and commencing earthworks using internal cash whilst finalising debt arrangements, accelerating the development timeline.

Segilola presents multiple extension opportunities: five drilling rigs are exploring beneath the existing pit, intersecting underground mineralisation averaging 5.5 g/t (versus 4+ g/t in the open pit), with work focused on a shallow-dipping plunge in the south and steeply dipping chute in the north to maximise throughput. Pit optimisation at current gold prices ($4,000+ versus the $1,600 assumption in the original bankable feasibility study) enables deeper mining before transitioning underground. Thor has identified multiple satellite deposits within a 50-kilometre radius averaging 5 g/t suitable for stockpiling and toll treatment, including a pilot mining operation planned for 2026. The existing stockpile contains over 44,000 ounces (0.85 g/t) representing more than $175 million in contained gold value. Management characterises additional ounces as "super ounces" given sunk infrastructure capital and established operations.

Guitry has delineated six parallel mineralised lenses remaining open along strike and at depth across just 15% of an 8km x 5km geochemical footprint, with high-grade intersections including 10m at 10 g/t, 10m at 9 g/t, and 2m at 16 g/t from 4,600 metres of drilling. Active drilling programmes target two additional areas within the footprint, with potential to replicate or extend discoveries significantly. Marahui presents genuine greenfield discovery potential with 8 kilometres of drill targets across two structures showing surface rock chip grades of 10–17 g/t along entire strike lengths. Both projects advance toward maiden resource estimates in H1 2026 with continuous drilling through the eight-month dry season, all funded internally from operational cash flows.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed