US Tariff Fragmentation & Copper Supply Chain Repricing Shift Capital Toward Near-Term Producers

Copper markets are repricing around tariffs and sulfuric acid shortages, driving capital toward near-term SX-EW copper developers.

- Goldman Sachs maintained its 2026 average copper price forecast of US$12,650 per tonne and its projected 490,000-tonne market surplus, while identifying Strait of Hormuz disruption and China’s sulfuric acid export restrictions as material risks to the SX-EW market, which accounts for roughly 17% of global copper supply.

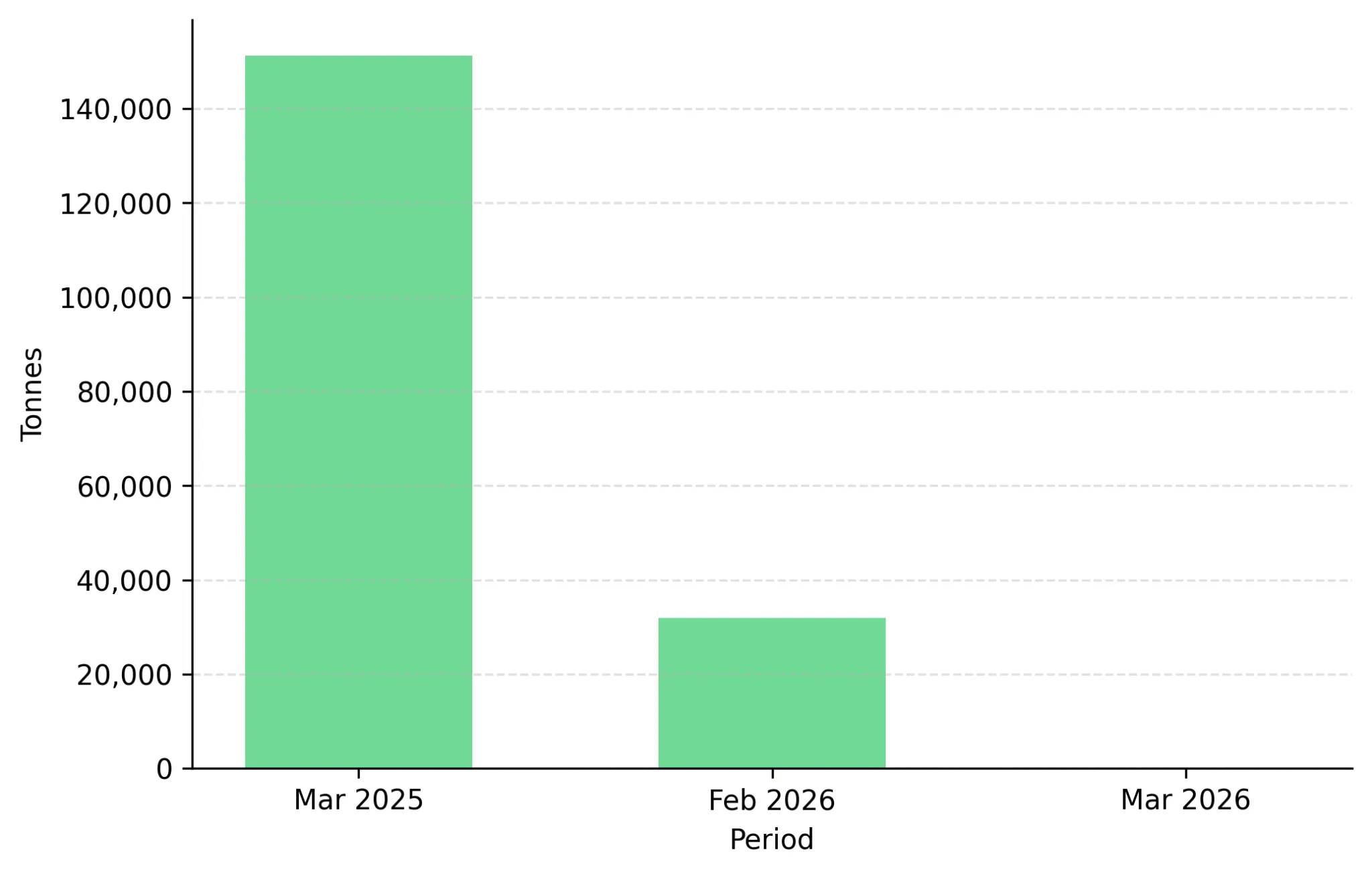

- Chinese sulfuric acid shipments to Chile declined from 151,268 tonnes in March 2025 to zero in March 2026, exposing part of Chile’s approximately 1.1 million tonnes of leached copper production to acid supply risk.

- The COMEX-LME premium re-emerged in April 2026, with COMEX copper inventories reaching 544,887 tonnes compared with 395,575 tonnes in the LME system as of April 22, 2026, contributing to the redirection of refined cathode into US warehouses ahead of the expected July 2026 Section 232 decision.

- Capital is increasingly reallocating toward copper developers with sub-US$600 million pre-production capex, existing infrastructure access, and construction timelines within the next eighteen months.

- Strategic financing participation from sector operators, including Discovery Silver Corp.’s expected 9.9% ownership stake in Abitibi Metals Corp. through a C$30.75 million placement announced in April 2026, reflects growing institutional backing for advanced-stage copper development assets.

Copper Pricing Has Decoupled from Synchronized Industrial Demand

Three-month London Metal Exchange copper traded at $13,441 per tonne on April 22, 2026, the highest level since February 27, 2026. The price reflects two simultaneous mechanisms rather than synchronized global industrial demand: the re-emergence of the COMEX-LME premium that redirected refined cathode into US warehouses, and the chemical-input supply constraint imposed by China's sulfuric acid export ban.

COMEX copper inventories rose 2% from mid-April to 544,887 tonnes by April 22, 2026, within 980 tonnes of the February 2026 record of 545,867 tonnes, while LME stocks stood at 395,575 tonnes after sustained outflows from Asian warehouses. Goldman Sachs maintained its 2026 average copper price forecast at $12,650 per tonne and its 490,000-tonne 2026 surplus estimate, while identifying the Democratic Republic of the Congo (DRC) and Chile as the two jurisdictions most exposed to Strait of Hormuz shipping disruption affecting sulfur flows. The mechanism into mining equity valuations is observable: refined cathode able to reach Western buyers before mid-2027 captures both the COMEX premium and the acid-driven Chilean output curtailment risk currently priced into the forward curve.

Sulfuric Acid Supply Risk Has Become a Quantified Constraint on Chilean & Congolese Cathode Output

Sulfuric acid is the indispensable reagent in heap-leach and SX-EW circuits, which produce LME-grade copper cathode directly from oxide and supergene ores without smelter dependency. The combination of China's export ban and Strait of Hormuz shipping disruption has converted acid availability from a commodity input into a measurable constraint on Chilean and Congolese cathode output.

China’s Export Ban Removes ~200,000 Tonnes from Chile’s Acid-Linked Copper Balance

Chinese sulfuric acid shipments to Chile fell from 151,268 tonnes in March 2025 to 31,870 tonnes in February 2026 before dropping to zero in March 2026, marking the first zero-shipment month since July 2023. China accounted for roughly one-third of Chile’s sulfuric acid imports in 2025, with Chinese supply also estimated to represent around 20% of the acid used in Chilean copper leaching operations.

Goldman Sachs estimates that a year-long Chinese export ban could place approximately 200,000 tonnes of Chilean cathode production at risk, equivalent to about 1% of global copper supply, while extended disruption in the Strait of Hormuz beyond late May 2026 could reduce Democratic Republic of the Congo copper production by another 125,000 tonnes this year.

SX-EW Cathode Producers Bypass the Smelter Chokepoint

SX-EW projects produce LME-grade copper cathode directly, avoiding the need for concentrate processing and reducing exposure to global smelter capacity, particularly in China, which refined 14.72 million tonnes of copper in 2025. Marimaca Copper is advancing the Marimaca Oxide Deposit in Chile’s Antofagasta Region, where its 2025 Definitive Feasibility Study outlined pre-production capital costs of just under US$600 million, expected annual copper cathode production of 50,000 tonnes, a strip ratio of 0.8:1, and a 39% internal rate of return based on a US$4.30 per pound copper price. The company is targeting the start of construction by the end of 2026.

Capital Discipline Has Replaced Resource Scale as the Preferred Development Test

Pre-production capital intensity for new copper projects typically ranges from US$15,000 to US$25,000 per tonne of annual production capacity, with several large-scale greenfield developments facing delays or scope reductions in the current market environment. At the Marimaca Oxide Deposit, Marimaca Copper estimates capital intensity at approximately US$11,700 per tonne based on its 2025 Definitive Feasibility Study, placing the project below the broader industry range. The lower capital requirement is supported by a 0.8:1 strip ratio, compared with the more typical 2:1 to 4:1 range for copper projects, as well as the project’s proximity to established port infrastructure in Chile’s Antofagasta Region.

Sequential Development Reduces External Financing Requirements

Marimaca Copper raised C$80 million in early 2026 per company disclosures. The Pampa Medina sulphide footprint covering approximately 3 kilometres by 1.5 kilometres requires 200,000 to 300,000 metres of drilling for proper resource definition. Management has stated this program will be funded from MOD production cash flow rather than equity raises, deferring dilution risk from the exploration phase to the construction financing phase.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, anchored the engineering process to capital discipline rather than absolute capex reduction:

“We do want to reduce capex, but every single design change we make to lower capex has to be evaluated within the broader context of the project’s overall risk.”

Strategic Financing from Sector Operators Validates Technical Quality

Abitibi Metals announced a C$30.75 million non-brokered private placement on April 23, 2026, with Discovery Silver Corp. expected to acquire an approximately 9.9% ownership stake upon closing. The financing includes 11.76 million charity flow-through shares priced at C$0.85 and 35.78 million hard-dollar shares priced at C$0.58, alongside participation rights that allow Discovery Silver to maintain its proportional ownership in future financings. The announcement follows Abitibi’s confirmation of 80% ownership of the B26 polymetallic copper-gold deposit in Québec in March 2026, as well as recent drill results that returned 2.71% copper-equivalent over 7 metres within a broader interval grading 1.81% copper-equivalent over 15 metres in the project’s western down-plunge zone.

Jonathon Deluce, President and Chief Executive Officer of Abitibi Metals, anchored the deposit growth profile to its option period:

“Since optioning the project, we’re up more than 125% in terms of tonnage growth.”

Infrastructure Access Is Quantifiably Reducing Pre-Production Capital Requirements

Existing roads, power, water rights, and underutilized SX-EW capacity are scarce assets in established copper districts. Where developers integrate with operating infrastructure rather than constructing standalone facilities, pre-production capex and permitting timelines compress in measurable ways.

Operational SX-EW Tank Houses Eliminate a Capex Line Item

Fitzroy Minerals signed a non-binding letter of intent with Sociedad Punta del Cobre S.A. regarding the Buen Retiro Copper Project near Copiapó, Chile. Under the agreement, Pucobre would make available at least 80% of the nameplate capacity at its Planta Biocobre electrowinning facility, which is capable of producing 800 tonnes of copper cathode per month, or approximately 9,600 tonnes annually. The processing facility is located around 70 kilometres by road from Buen Retiro, which itself is positioned close to existing infrastructure, including the Pan-American Highway and the Pacific coast.

Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, identified the specific capital and permitting reductions enabled by the LOI:

“Fitzroy benefits from access to an operational EW tank-house, which reduces capital expenditure and simplifies the permitting process.”

Brownfield Districts Compress the Capital-to-Revenue Timeline

Pucobre operated the Manto Negro copper oxide mine on the Buen Retiro property from 2005 to 2009, producing 34.4 million pounds of copper, establishing site-specific operational and environmental baselines. The Buen Retiro project sits in the Punta del Cobre copper belt that hosts Lundin Mining's Candelaria copper-gold mine, which produced 145,000 tonnes of copper in 2025 per Lundin disclosures. District-level analogue operations reduce the geological and metallurgical risk premium applied to development assets relative to greenfield discoveries.

Under the Buen Retiro option agreement signed in January 2023, Sociedad Punta del Cobre S.A. retains a 30% claw-back right that can be exercised following completion of the project’s Final Technical Report, requiring reimbursement of 90% of eligible expenditures, or at least US$10.2 million, to Fitzroy Minerals Inc. Fitzroy is targeting completion of all four option stages by the second quarter of 2027, while commercial tolling terms for the Planta Biocobre facility are expected to be finalized within roughly 90 days to support the project’s pre-feasibility study economic model.

Copper's Supply Deficit Is Driven by Logistics & Processing, Not Reserve Depletion

Goldman Sachs’ April 2026 outlook projects a 490,000-tonne global copper surplus for 2026, while also warning that sulfuric acid supply disruptions could curtail as much as 325,000 tonnes of combined production in Chile and the Democratic Republic of the Congo. The bank’s analysis suggests that the longer-term copper market outlook is increasingly tied not only to resource availability, but also to whether refined cathode can reliably reach Western end markets.

Three members of the China Smelter Purchase Team (CSPT) issued 2026 cathode production guidance that maintained or increased output despite the trade body’s 2025 commitment to reduce production by more than 10%. Jiangxi Copper raised 2026 guidance to 2.39 million tonnes from 2.38 million tonnes produced in 2025, while Yunnan Copper increased guidance to 1.71 million tonnes from 1.64 million tonnes. Daye Nonferrous guided for a slight reduction to 713,000 tonnes from 716,000 tonnes. Continued smelter capacity expansion against constrained concentrate supply has shifted bargaining power toward miners with concentrate to sell, while reinforcing the strategic appeal of SX-EW projects that bypass third-party smelting.

Goldman Sachs and Citigroup analysts have continued to forecast that the US could impose Section 232 copper import tariffs of up to 25%. Inventory movements have already begun reflecting that expectation, with COMEX inventories rising to 544,887 tonnes by April 22, 2026 while outflows from Asian LME warehouses accelerated, indicating refined copper supply is increasingly being redirected toward the US market ahead of the anticipated July 2026 tariff decision.

The Investment Thesis for Copper

- Heap-leach and SX-EW projects monetize copper as LME-grade cathode without smelter dependency, capturing the negative TC/RC structure confirmed by the China Smelter Purchase Team's fifth consecutive quarter without TC/RC guidance per Reuters reporting on April 2, 2026.

- Developers operating with pre-production capital intensity below US$12,000 per tonne sit 25% to 40% below the US$15,000 to US$25,000 peer range per S&P Global's 2024 Mining Capital Intensity Database, reducing absolute external financing requirements during periods of elevated interest rates.

- Existing third-party processing infrastructure access can reduce standalone plant capex and shorten permitting timelines, with established Chilean SX-EW tank houses offering quantifiable underutilized cathode capacity within trucking distance of advanced exploration assets.

- Strategic financing participation from sector operators in non-brokered placements at the C$30 million-plus scale signals institutional rather than retail capital underwriting development-stage copper assets.

- Sequential development models that fund expansion from operating cash flow rather than equity issuance preserve the existing share structure through construction, with copper developers deferring multi-year drilling programs until first-stage production cash flow is available.

- Jurisdictional alignment with Western procurement frameworks supports offtake premiums for cathode produced under verified supply chains under the European Critical Raw Materials Act and US Inflation Reduction Act sourcing requirements.

- Developers with construction targets before mid-2027 capture the COMEX-LME premium and the acid-driven Chilean curtailment risk currently priced into the forward copper curve.

The April 2026 LME copper price of US$13,441 per tonne, alongside Goldman Sachs’ 2026 average forecast of US$12,650 per tonne, reflects two intersecting market mechanisms: COMEX-LME premium-driven redirection of refined cathode into the US ahead of the expected July 2026 Section 232 decision, and a quantified 200,000-tonne risk to Chilean cathode supply linked to China’s sulfuric acid export restrictions. Capital is increasingly reallocating toward developers targeting construction before mid-2027, particularly those with infrastructure advantages and staged funding models that can limit equity dilution through the buildout phase. The investment question for institutional capital is shifting from where the next major copper resource will be discovered to which developers can deliver LME-grade cathode into increasingly fragmented Western supply chains within the window created by current acid and tariff constraints.

TL;DR

Copper prices are increasingly being driven by supply chain fragmentation rather than pure industrial demand, as US tariff expectations and China’s sulfuric acid export restrictions disrupt global copper flows. Goldman Sachs maintained a bullish long-term copper outlook despite forecasting a 2026 surplus, warning that sulfuric acid shortages could threaten Chilean and Congolese SX-EW copper production. Investors are responding by reallocating capital toward advanced-stage copper developers with low capex intensity, existing infrastructure access, and the ability to produce LME-grade cathode before mid-2027. Companies such as Marimaca Copper, Abitibi Metals, and Fitzroy Minerals are benefiting from this shift due to their staged financing models, infrastructure advantages, and strategic institutional backing.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed