Marimaca Copper: The District Is the Thesis

Marimaca's district thesis rests on MOD execution, not silver assays. Three-stage sequencing targets growth without dilution, if financing holds.

- Marimaca Copper recently raised C$80 million from Australian, Canadian, and US investors, with management describing the company as very comfortable with its cash position, and the Definitive Feasibility Study (DFS) for the Marimaca Oxide Deposit (MOD) establishing a pre-production capital cost of just under US$600 million and a base case of 50,000 tonnes per annum of copper cathode production.

- Completed inductively coupled plasma assaying across all Pampa Medina drilling to date confirms silver is elevated and broadly correlated with copper across both oxide and sulphide zones over a 3-kilometre by 2-kilometre area of interest, but Phase I metallurgical programs remain incomplete, and copper equivalent grades cannot yet be reported.

- Properly infilling the Pampa Medina sulphide footprint requires 200,000 to 300,000 metres of drilling over several years; the company is targeting MOD production cash flow to self-fund that program without returning to equity markets.

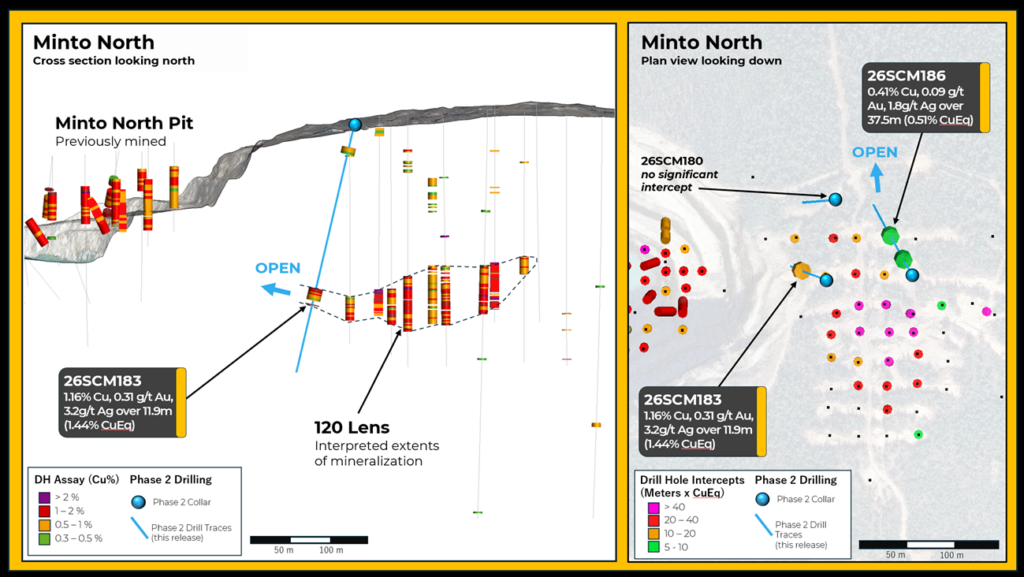

- Standout intercepts from Pampa Medina include 100 metres at 1.28% copper and 6.9 grams per tonne silver from 580 metres depth, including 6 metres at 11.98% copper and 82.0 grams per tonne silver, with true widths estimated at 80% to 90% of reported downhole intersection widths.

- The company is targeting an expansion of cathode production from 50,000 tonnes per annum to 70,000 or 75,000 tonnes per annum by advancing Pampa Medina oxide zones through Phase I metallurgical and geotechnical work, leveraging the MOD base case approximately 28 kilometres away.

Silver Is the Footnote, Not the Headline

Marimaca Copper (TSX: MARI | ASX: MC2) has completed inductively coupled plasma (ICP) assaying across all drilling at Pampa Medina, drawing attention to the silver results, attention that is ultimately misplaced. Phase I metallurgical programs remain incomplete, copper equivalent grades have not been reported, and the economic contribution of the silver component is not determinable at this stage. What the completed database does establish is deposit-wide continuity across a 3-kilometre by 2-kilometre area of interest, a scale confirmation that supports a system-level thesis, not a near-term resource catalyst.

The silver data provides additional upside to a development plan that does not depend on it. Standout intercepts - including 100 metres at 1.28% copper and 6.9 grams per tonne silver from 580 metres depth, and 102 metres at 1.20% copper and 12.2 grams per tonne silver from 250 metres - demonstrate that the system delivers consistent copper grades at depth with silver present and broadly correlated. True widths are estimated at 80% to 90% of reported downhole intersection widths. Marimaca has cited Capstone Copper's Mantos Blancos and Antofagasta Minerals' Cachorro as regional analogues, noting that precious metal by-products in large primary copper deposits can surface exceptional value for builders and operators. The data is not a near-term catalyst, with its economic relevance limited to the sulphide stage rather than the current phase.

The operative question is not what the silver assays show, but how the company is acting on them. The answer is to defer sulphide delineation, preserve the treasury, and advance the Marimaca Oxide Deposit (MOD) toward construction, which is the real signal.

The Three-Stage Value Stack

Marimaca Copper's asset base is structured as a sequential value-creation model across three stages, each funded by the one before it. The first stage is the MOD: a fully Definitive Feasibility Study (DFS)-backed oxide copper project with a pre-production capital cost of just under US$600 million, 50,000 tonnes per annum base case production, and industry-leading return on invested capital metrics based on a US$4.30 per pound copper price assumption. The MOD is the cash engine. Management is targeting build-readiness and construction commencement by the end of 2026.

The second stage is Pampa Medina oxide expansion. Situated approximately 28 kilometres east of the MOD, Pampa Medina's shallower oxide mineralisation offers an opportunity to expand cathode production by leveraging the MOD base case. Phase I metallurgical and geotechnical work is advancing to bring the project up the engineering maturity curve. The production target from this stage is an increase from 50,000 tonnes per annum to 70,000 or 75,000 tonnes per annum of copper cathode, subject to technical confirmation from the ongoing work.

The third stage is Pampa Medina sulphide delineation. With 200,000 to 300,000 metres of drilling required over several years to properly infill the 3-kilometre by 1.5-kilometre sulphide footprint, this stage is deliberately deferred to be funded by MOD production cash flow rather than equity issuance. The silver by-product optionality, once Phase I metallurgical work establishes recoveries and grades, accrues at this stage.

Hayden Locke, Chief Executive Officer and Director of Marimaca Copper, confirmed the growth confidence underpinning that sequencing:

"We're now growing in confidence. It will deliver at least an additional 25,000 tonnes of copper per annum to our MOD base case of 50,000 tonnes per annum."

The long-term funding strategy is explicit, with large-scale sulphide delineation deferred until MOD cash flow is generated, avoiding dilution of the current share structure.

Capital Discipline as Investment Thesis

The decision not to accelerate sulphide delineation is the clearest expression of Marimaca's investment proposition. Following its C$80 million raise, management has described the company as very comfortable with its cash position, but properly infilling the Pampa Medina sulphide footprint would require capital. Gating that spend preserves the balance sheet to advance the MOD toward construction and protects the share structure through what management acknowledges is a demanding execution phase.

The construction financing process is not a step in the plan; it is the gatekeeper of the thesis. The just-under US$600 million pre-production capital cost against the current treasury means Marimaca will require substantial external capital. Management is currently evaluating financing options, and the structure and terms of that outcome will directly determine whether the non-dilution thesis holds.

Locke outlined the objective:

"That also gives us the time to go through the financing process and consider all of the options available to us and hopefully come up with a really good financing structure that is the least dilutive for our current shareholders."

Locke has been direct about the consequences of getting it wrong, adding:

"I am very focused on delivering this and getting it right the first time rather than rushing it. That may be frustrating for some people, but I think in the long run that will pay dividends in terms of us not blowing up our capital structure by getting it wrong the first time."

This framing is best understood as a deferred risk model, not an eliminated one. Dilution risk is time-shifted and tied to execution; if construction proceeds on schedule, the sequencing works as intended. If it does not, the financing structure becomes the pressure point.

What the Pampa Medina Data Establishes

The completed ICP assay program resolves one open question: whether silver is a system-wide feature or confined to isolated zones. The answer is system-wide. Silver is elevated and broadly correlated with copper across both the oxide and sulphide mineralised envelopes over the full 3-kilometre by 2-kilometre area of interest, including zones affected by post-mineralisation faulting and dyke intrusions. That structural resilience, consistent hits through interruptions in continuity, supports a laterally extensive sediment-hosted system rather than isolated high-grade pockets.

What remains unresolved is the economic weight of the silver component. Copper equivalent grades require completed metallurgical recoveries for silver. Those recoveries remain pending from Phase I metallurgical programs. Until those results are available, the silver data informs the geological model but does not alter the financial model. The DFS economics for the MOD were established without silver by-product credit from Pampa Medina.

Marimaca currently has 5 rigs operating at Pampa Medina, with a rig count increase targeting acceleration of the 2026 drilling program through April and May 2026. That activity is directed at the oxide zone and step-out targets, consistent with the targeted oxide production growth pathway rather than sulphide resource infill.

Execution Risk: What Still Needs to Be Proven

The three-stage thesis carries execution dependencies at each stage. The MOD must reach build-readiness and commence construction by the end of 2026 and advance within the just-under US$600 million capital estimate. Any cost overrun or construction delay might extend the timeline to production cash flow and, by extension, the timeline to sulphide delineation funding. The capital cost against the current treasury, recently bolstered by the C$80 million raise, requires external financing to be secured. The terms of that financing will determine the extent of shareholder dilution, if any, at the construction stage.

Locke has been explicit about the design philosophy governing that construction process, framing the operability trade-off directly:

"Every single design change that we make that reduces capex has to be thought about within the greater impact on risk of the project, and that's around operability."

The Pampa Medina oxide expansion thesis depends on Phase I metallurgical and geotechnical results confirming the technical viability of expanding cathode production. Those results have not yet been released. If they do not support the expansion case, the 70,000 to 75,000 tonnes per annum production target would require reassessment. The sulphide self-funding model is similarly contingent on MOD production rates and copper prices holding at or above the US$4.30 per pound DFS base case assumption; any material downward deviation would extend the self-funding timeline.

Investment Thesis for Marimaca Copper

- Marimaca Copper recently raised C$80 million, is fully permitted, and is targeting construction commencement by the end of 2026 against a definitive feasibility study-defined pre-production capital cost of just under US$600 million.

- The Marimaca Oxide Deposit definitive feasibility study confirms industry-leading return on invested capital metrics at a US$4.30 per pound copper base case, supporting 50,000 tonnes per annum of copper cathode production over the life of mine.

- Pampa Medina sulphide delineation, requiring 200,000 to 300,000 metres of drilling, is being deferred until Marimaca Oxide Deposit cash flow is available, designed to eliminate exploration-driven equity raises and preserve the existing share structure through the construction phase.

- Subject to Phase I metallurgical and geotechnical confirmation, the company is targeting a production increase from 50,000 to 70,000 or 75,000 tonnes per annum through Pampa Medina oxide expansion, leveraging Marimaca Oxide Deposit infrastructure approximately 28 kilometres away.

- Completed inductively coupled plasma assaying confirms silver is elevated and broadly correlated with copper across a 3-kilometre by 2-kilometre area at Pampa Medina in both oxide and sulphide zones, adding by-product optionality to future sulphide economics not yet reflected in the definitive feasibility study base case.

- The thesis is contingent on construction financing on acceptable terms, on-schedule delivery within the just-under US$600 million capital estimate, metallurgical confirmation of Pampa Medina oxide viability, and copper prices holding at or above the US$4.30 per pound definitive feasibility study base case.

The Marimaca Copper investment case is not driven by a single catalyst but by its capital sequencing. That sequencing is logical and internally consistent but conditional, with the non-dilution thesis depending on MOD construction proceeding on schedule and financing being secured on acceptable terms. Investors assessing the three-stage structure, Marimaca Oxide Deposit as the cash engine, Pampa Medina oxide as incremental growth, and Pampa Medina sulphide as long-dated upside, are evaluating a fundamentally different risk profile, assuming execution holds.

TL;DR

Marimaca Copper's April 2026 silver confirmation at Pampa Medina adds by-product optionality to a district thesis already anchored by a DFS-backed oxide deposit with industry-leading return on invested capital metrics at a US$4.30 per pound copper base case. The company's decision to gate sulphide delineation until MOD cash flow is available is a deliberate capital structure decision to fund district-scale resource growth without equity dilution. Build-readiness is targeted by the end of 2026. The silver economics are not yet determinable pending Phase I metallurgical results.

FAQs (AI-Generated)

MOD first: DFS-backed, just under US$600 million pre-production capital, 50,000 tonnes per annum base case, construction targeted by end-2026. Then, Pampa Medina oxide expansion toward 70,000 to 75,000 tonnes per annum, subject to Phase I metallurgical and geotechnical confirmation. Then, sulphide delineation, requiring 200,000 to 300,000 metres of drilling over several years, funded from MOD cash flow rather than equity.

Properly infilling the sulphide footprint requires 200,000 to 300,000 metres of drilling over several years, a capital commitment management has chosen to gate until MOD cash flow is available. Spending that ahead of production would require returning to equity markets, diluting the existing share structure before the MOD has generated a single dollar of cash flow.

ICP assaying confirms silver is elevated and broadly correlated with copper across a 3-kilometre by 2-kilometre area in both oxide and sulphide zones, establishing system-wide continuity. What it does not confirm is economic contribution: copper equivalent grades require Phase I metallurgical recoveries, which remain incomplete. Silver is not a near-term catalyst.

The DFS confirms industry-leading return on invested capital metrics at a US$4.30 per pound copper base case, supporting 50,000 tonnes per annum of cathode production. Pre-production capital cost is just under US$600 million. Construction is targeted for the end of 2026. The C$80 million raise bolsters the treasury, but substantial external financing will still be required.

The entire non-dilution thesis hinges on securing a financing structure that is the least dilutive for our current shareholders. Marimaca needs substantial external capital to reach construction. The financing outcome, not the drill results, is the primary variable to watch.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed