Vox Royalty Posts Record Q1 as Management Unveils Path to $66 Million by 2030

.jpg)

VOXR: Record Q1 ($16M receipts, $0.36 EPS), 1st 2030 guidance ($66M). Trades ~$300/GEO vs peers $1,200-1,800. No debt, $75M credit line.

- Record Q1 2026 results: $16.0 million in royalty and net precious metal receipts (vs. $2.7 million in Q1 2025), $24.5 million net income ($0.36/share, including a $16.5 million non-cash revaluation gain), $15.2 million operating cash flow, and $12.7 million Adjusted EBITDA ($0.18/share) - all company records.

- First-ever long-range guidance: Management raised 2026 receipts guidance to $32–37 million (from $28–32 million) and issued inaugural 2030 guidance of approximately $66 million, based entirely on the existing portfolio and explicitly excluding the Red Hill litigation outcome.

- GEO valuation discount thesis: Vox discloses an implied valuation of ~$300 per gold equivalent ounce (GEO) against >1 million total GEOs (240,000 from producing assets), compared with ~$1,200/GEO for Triple Flag and ~$1,800/GEO for Franco-Nevada.

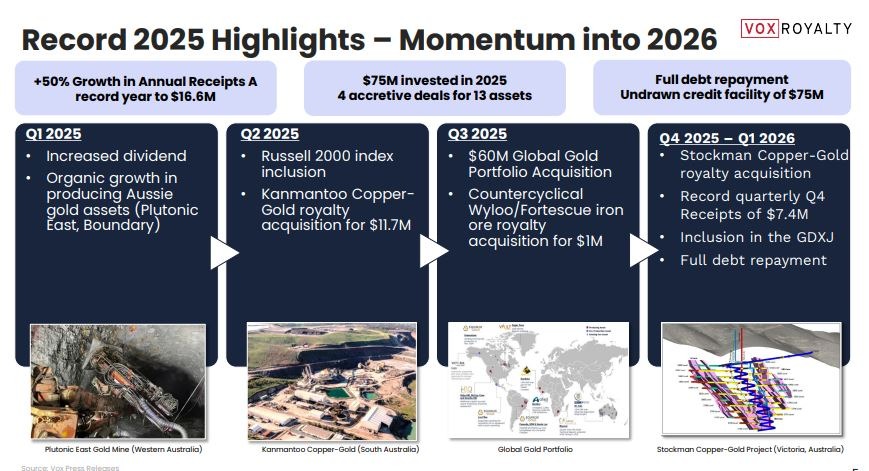

- Unlevered balance sheet: $15.9 million cash, zero debt, and a fully undrawn $75 million Bank of Montreal revolving credit facility (~$90 million total capital availability), alongside a 20% quarterly dividend increase (March 2026) marking the fourth consecutive year of dividend growth.

- Organic catalyst crystallizing: Bonikro's disclosed mine life was extended from 2029 to 2036 (a 400% increase in life-of-mine production) per Allied Gold's June 10, 2026 update, supporting 120,000+ oz/year of mine production and ~60,000 oz/year of deliveries to Vox under an uncapped 50% gold offtake-stream.

Vox Royalty Corp operates in the precious metals royalty and streaming sector, a capital-light business model in which the company acquires fixed-percentage or net-revenue interests in third-party mining projects rather than taking on direct operating, exploration, or capital expenditure exposure. The sector has historically commanded valuation premiums over operating miners, reflecting high incremental margins, limited cost inflation exposure, and optionality tied to underlying mine life extensions and exploration success. This dynamic has been reinforced over the past eighteen months by a sustained rally in gold prices, which traded above $3,000 per ounce from March 2025 and surpassed $5,000 per ounce by January 2026. For a company with a 92% gold-weighted receipts base in Q1 2026, this commodity backdrop has provided a substantial tailwind, both through direct price exposure on offtake-stream deliveries and indirectly by encouraging underlying operators to expand mill capacity, extend cut-off grades, and lengthen mine plans. Vox, with a market capitalization of approximately $389 million as of June 1, 2026, sits at the smaller end of the publicly listed royalty universe, which is the central tension explored throughout this report: a track record of organic growth and balance sheet discipline set against a valuation that management argues does not yet reflect it.

Record Q1 2026 Performance and Capital Position

Vox reported royalty and net precious metal receipts of $16.0 million for the first quarter of 2026, compared with $2.7 million in the prior-year period, representing the strongest quarter in the company's history. Net income reached $24.5 million, or $0.36 per share, a figure that included a $16.5 million non-cash revaluation gain tied to a reforecast of realized margins on the Global Gold Portfolio acquired in September 2025. Excluding this one-time item, underlying operating performance remained strong: operating cash flow of $15.2 million and Adjusted EBITDA of $12.7 million ($0.18 per share) were also quarterly records. The company delivered 77,293 ounces of gold under its offtake-stream structures during the quarter at an average net precious metal income margin of $179.41 per ounce, a figure that benefits from the mechanics of offtake contracts, under which Vox selects its purchase price within a multi-day quotation window before reselling the metal at a separately chosen price point - a structure that provides leveraged exposure to rising gold prices without direct commodity price risk on the purchase side. Following these results, management raised full-year 2026 receipts guidance to $32–37 million, up from a prior $28–32 million range, with total gold deliveries for the year expected to reach 230,000 ounces. The balance sheet remains unlevered: as of March 31, 2026, the company held $15.9 million in cash, zero debt outstanding (having repaid a $6.7 million facility balance during the quarter), and a fully undrawn $75 million revolving credit facility with Bank of Montreal, providing approximately $90 million of total capital availability ahead of any further capital raise.

First-Ever 2030 Guidance: A Disclosure Inflection Point

In conjunction with its Investor Day materials, Vox issued its first long-range financial guidance, projecting royalty and net precious metal receipts of approximately $66 million by 2030 - roughly double the midpoint of current 2026 guidance. Management has stated this figure reflects only assets already held in the portfolio, with no contribution assumed from future acquisitions, and explicitly excludes any contribution from the Red Hill royalty, which remains subject to ongoing litigation. The decision to provide multi-year guidance follows a pattern set by larger peers such as Royal Gold and Franco-Nevada, and management has characterized the timing as a function of increased confidence in underlying operator disclosures rather than a change in business strategy. Investors should note that, as with all forward guidance in the royalty sector, the 2030 figure is derivative of third-party operator mine plans, reserve estimates, and production guidance over which Vox has no operational control. The June 2026 Bonikro mine life extension, discussed below, represents one of the clearest disclosed examples of the type of organic, non-acquisitive growth embedded in this projection, but the guidance as a whole still depends on continued favorable disclosure from a wide range of third-party operators across multiple jurisdictions.

The GEO Valuation Gap and Comparable Company Analysis

Central to management's investment case is a comparison of Vox's implied valuation per gold equivalent ounce (GEO) against larger, more established peers. Vox discloses over one million GEOs across its royalty portfolio at an average royalty rate of approximately 1%, of which roughly 240,000 GEOs are attributable to currently producing assets. On this basis, management calculates an implied market valuation of approximately $300 per GEO, compared with approximately $1,200 per GEO for Triple Flag Precious Metals and approximately $1,800 per GEO for Franco-Nevada. The company also cites a 28% return on invested capital since inception as evidence of underwriting discipline comparable to, or exceeding, larger peers. These comparisons carry caveats that management itself acknowledges: Franco-Nevada and Triple Flag operate at substantially larger scale, with deeper diversification, longer operating histories, and lower portfolio concentration risk, all of which typically command valuation premiums independent of per-ounce metrics. The GEO comparison also does not adjust for differences in asset quality, jurisdictional risk, or the proportion of resource-stage versus reserve-stage ounces, meaning the stated discount, while directionally informative, should be treated as one data point among several rather than a precise measure of intrinsic undervaluation.

Portfolio Catalysts: Bonikro, Los Filos, and Red Hill

Three assets anchor near-term catalyst discussion. Bonikro, an uncapped 50% gold offtake-stream in Côte d'Ivoire acquired as part of the September 2025 Global Gold Portfolio transaction, saw its disclosed mine life extended from four years (to 2029) to twelve years (to 2036) following an updated Allied Gold production plan announced June 10, 2026, with average annual production guided above 120,000 ounces, implying approximately 60,000 ounces of annual deliveries to Vox. Los Filos, a 50% gold stream acquired for a nominal $1 and currently suspended pending a community agreement with Equinox Gold, represents an embedded option that management values at $30 million to $50 million if production resumes; the timing of any resolution sits outside Vox's control. Red Hill, a 4.0% uncapped gross revenue royalty in Western Australia, covers a resource recently upgraded 58% to approximately 1.9 million ounces, with the underlying Fimiston mill undergoing a A$1.5 billion expansion to 27 million tonnes per annum. However, Northern Star Resources is disputing the assignment of the Red Hill royalty to Vox, and the company is defending the claim as a second defendant in ongoing litigation, introducing a binary, unresolved risk that is explicitly excluded from formal guidance.

Track Record of Capital Allocation: A More Nuanced Picture

Vox highlights several fully-paid-back royalty acquisitions, including Kookynie (approximately 14x total cost), Graphmada (approximately 11x), and Segilola (approximately 5x), alongside three additional assets that reached payback in 2025. These figures support the company's stated discipline in sourcing legacy, often-overlooked royalties through its proprietary 8,500-royalty database. However, the same disclosure shows that across the broader set of acquisitions made between 2019 and 2024, aggregate total cost of $50 million has generated $45 million in total receipts through 2025 - a ratio modestly below one times invested capital on a portfolio-wide basis. This does not necessarily indicate underperformance, since many positions remain in earlier stages of their cash flow curve and the company's separately disclosed 28% ROIC figure appears to apply a different calculation methodology or time period. Nonetheless, the gap between headline multiples on selected winners and the blended portfolio figure is a detail institutional investors should reconcile directly with management rather than rely on the selected examples alone.

Conclusion

Vox enters the second half of 2026 with a materially strengthened balance sheet, record quarterly operating metrics, and a first-ever long-range growth target that, if realized, would nearly double current receipts by 2030 without further acquisitions. The core re-rating thesis rests on a GEO-based valuation discount to larger peers, a discount that is directionally supported by the data but subject to legitimate questions around scale, diversification, and asset quality. Near-term shareholder value will likely be determined less by the long-range guidance itself and more by the resolution of identifiable, binary catalysts: the Red Hill litigation outcome, the Los Filos community agreement, and continued execution on disclosed mine life extensions such as Bonikro. Investors should weigh these catalysts against the company's structural reliance on third-party operator disclosure, concentration in Australian jurisdiction (67% of asset base by count), and continued sensitivity to commodity price reversals.

Executive Summary (TL;DR)

Vox Royalty enters the second half of 2026 with the strongest financial profile in its history, anchored by record Q1 2026 receipts of $16.0 million, raised full-year guidance of $32–37 million, and its first-ever long-range target of approximately $66 million in receipts by 2030 using only currently-held assets. The investment case rests on a disclosed valuation gap - roughly $300 per gold equivalent ounce versus $1,200–$1,800 per ounce for larger royalty peers - supported by a debt-free balance sheet with $90 million of total liquidity and a growing dividend. Near-term share price catalysts are concrete and identifiable: the June 2026 Bonikro mine life extension to 2036, a potential Los Filos community agreement that could unlock an asset acquired for $1, and the unresolved Red Hill royalty litigation, none of which are reflected in formal guidance. The central question for investors is whether continued execution on these catalysts, combined with disciplined capital deployment, will be sufficient to close the disclosed valuation gap relative to scale peers.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed