West African Gold Sector: A Golden Opportunity for Investors

West Africa emerges as a premier gold region with rising production, favorable geology, and undervalued stocks poised to benefit from high gold prices and political stabilization.RetryClaude can make mistakes. Please double-check responses.

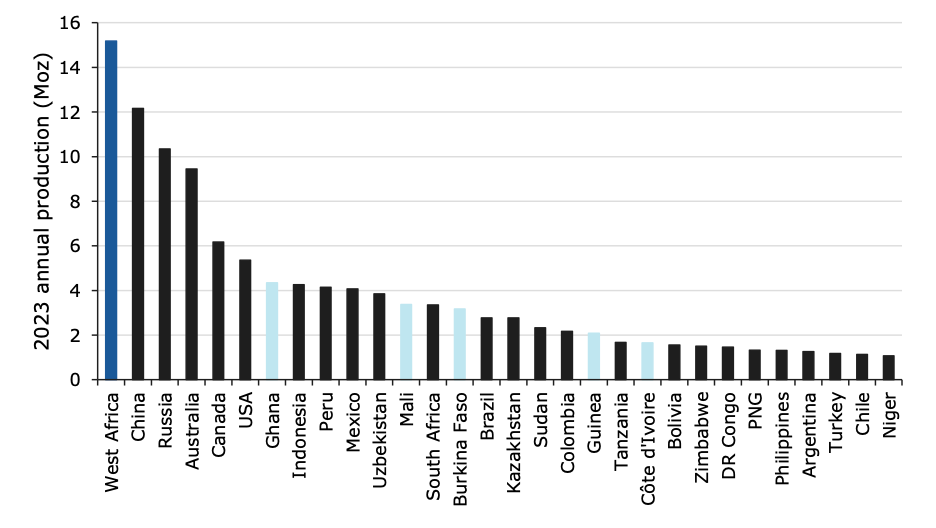

- West Africa has emerged as one of the world's largest gold producing regions, with over 15Moz produced in 2024

- Despite favorable operating conditions, West African gold stocks have historically traded at significant discounts to peers in other regions

- Recent political stabilization combined with high gold prices may present a compelling investment opportunity as country risks are increasingly mitigated by strong fundamentals

- The region has seen an acceleration in M&A activity (valued at ~US$4bn in 2024 vs ~US$300m in 2023), with Chinese acquirers emerging as significant players

- West Africa's exploration potential remains substantial, with 95Moz of gold discovered in the last 20 years, compared to Canada's 61Moz and Australia's 29Moz

The Rise of West Africa as a Global Gold Hub

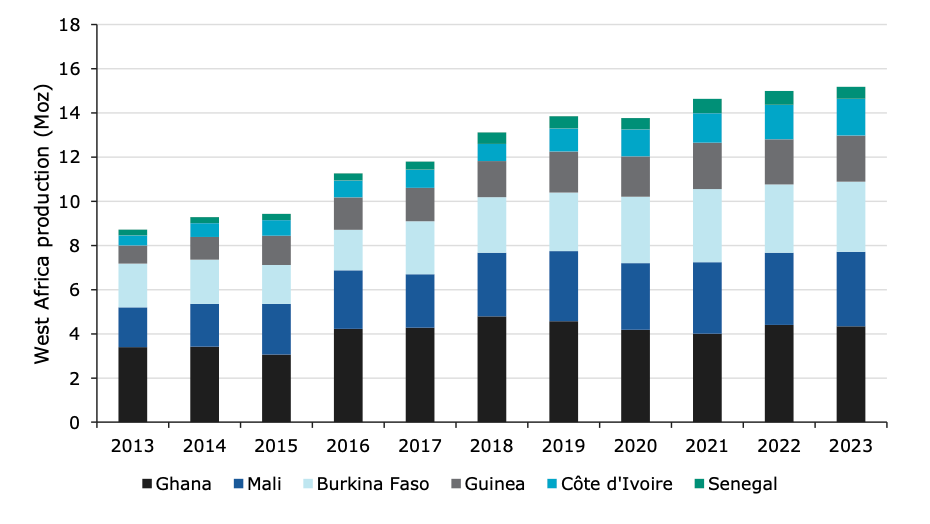

West Africa, encompassing Ghana, Mali, Burkina Faso, Côte d'Ivoire, Guinea, and Senegal, has steadily grown to become one of the world's key gold producing regions. Despite periodic political instability in countries like Mali and Burkina Faso, gold production from the region has increased steadily over the last decade to exceed 15 million ounces in 2024.

This impressive growth can be attributed to several factors. The region boasts highly favorable geology, particularly the mineral-rich Birimian Greenstone Belt which has yielded over 95 million ounces of gold discoveries since 2004. Historically supportive mining legislation with moderate royalty rates and tax incentives has encouraged investment. Rising gold prices (up 152% over the last decade) have incentivized exploration while improving the economics of lower-grade deposits.

The operational advantages of mining in West Africa are substantial. Companies operating in the region generally benefit from faster permitting times compared to those in "lower risk" jurisdictions like Australia or North America. Capital intensities are notably lower, with average upfront capex of US$93 per resource ounce versus US$119 in South America and US$138 in Europe. Construction lead times are typically shorter, and production costs are generally competitive on a global scale.

The "African Discount" & Changing Investor Sentiment

Despite these favorable attributes, West African gold stocks have historically traded at significant discounts compared to peers with operations in other jurisdictions. Current EV/EBITDA multiples for African gold producers show discounts of 40-80% versus North American and Australian peers. Similarly substantial discounts are evident across metrics like P/NAV, EV/FCF, and FCF yields.

However, recent share price performance suggests a potential shift in investor sentiment. West African gold indices have outperformed global benchmarks since January 2024, driven primarily by rising gold prices but also influenced by signs of political stabilization, increasing exploration activity, and accelerating M&A interest.

Several factors have contributed to the historical discount:

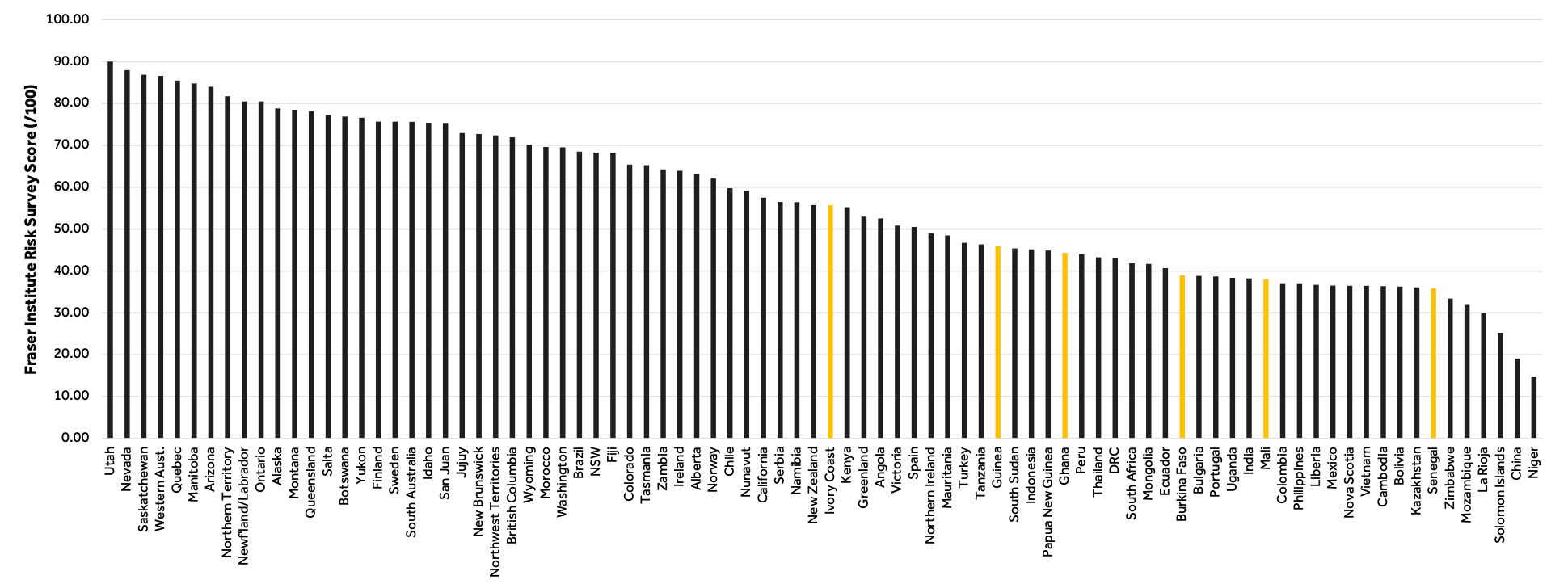

- Political and country risk: West African countries have experienced periods of political instability, including military coups, border issues, and revisions to mining codes with fiscal terms changes.

- Perceived operational risks: Despite excellent geology, operations in the region are often viewed as having higher risks related to labor issues, infrastructure limitations, and regulatory uncertainties.

- ESG considerations: Investors are increasingly sensitive to environmental, social, and governance factors, which may affect perceptions of the region.

- Market perception and bias: Investors may hold preconceived notions about West Africa that lead to undervaluation despite strong operational and financial performance by companies in the region.

The performance of companies like Perseus Mining and West African Resources demonstrates that these perceptions do not always align with reality. Both companies have consistently met or exceeded production guidance, establishing impressive operational track records that challenge the notion of elevated operational risk in the region.

Political Landscape & Mining Code Evolution

The West African gold sector has experienced significant political changes in recent years. Military coups in Mali (2021) and Burkina Faso (2022) brought transitional governments to power, while democratic transitions occurred in other countries like Ghana and Senegal.

These political shifts have often been accompanied by revisions to mining codes. Mali's 2023 Mining Code increased state participation from 10%+15% to 10%+20% and raised royalties from 6% to up to 11%. Similarly, Burkina Faso's 2024 Code increased state equity from 10% to 15% plus an additional 15% optional interest, with higher royalties and reduced mining permit tenure.

For investors, understanding the varied political landscape is crucial. Countries with dated mining codes might be at greater risk of revisions, but there's a clear correlation between a country's political stability, fiscal health, importance of mining to the economy, and the likelihood of significant changes.

Countries with stronger economies like Côte d'Ivoire, Ghana, and Guinea are more likely to balance any revisions with continued foreign investment incentives. Ghana, with one of the region's most attractive fiscal regimes (10% free carried interest and 5% gold royalties), has maintained relative stability in its mining legislation despite periodic updates.

Exploration Potential: The Geological Advantage

Africa hosts several prospective gold mineralized belts, but the West African Craton stands out as particularly significant. This geological formation spans approximately 4.5 million km² across several countries and hosts the highly prolific Birimian Supergroup.

The discovery rate tells an impressive story: over the last 20 years, 95 million ounces of gold have been discovered in West Africa, outpacing Canada (61Moz), Colombia (59Moz), and Australia (29Moz). The region's prospective geology, combined with favorable operating conditions, positions it for continued exploration success.

One particularly underexplored aspect is underground potential. While 60% of global operating gold mines have an underground component, only 30% of West African mines do. More mature mining regions like Canada and Australia show much higher proportions of underground operations (89% and 79% respectively). This suggests significant potential for depth extensions as West African mines mature.

With gold at all-time highs, a resurgence in exploration activity is anticipated. Companies actively exploring include Predictive Discovery in Guinea, Turaco Gold in Côte d'Ivoire, Toubani Resources in Mali, and numerous others seeking to tap into the region's rich geological endowment.

M&A Activity Heating Up

Merger and acquisition activity in West Africa has accelerated significantly over 2024 and early 2025, driven by high gold prices, improved cash balances, increasing script value, and scarcity of major global discoveries. The total value of West African gold M&A reached over US$4 billion in 2024, compared to approximately US$300 million in 2023.

Recent transaction data indicates African developer acquisitions commanded an average resource multiple of US$79/oz (versus Western averages of ~US$150/oz), while producer transactions averaged US$210/oz (versus Western averages of ~US$500/oz). These relatively lower valuations continue to make West African assets attractive M&A targets.

A notable trend is the increasing presence of Chinese buyers, who have typically paid premium multiples. In May 2024, Zhaojin Capital paid US$129/oz for Tietto Minerals' Abujar Project in Côte d'Ivoire, representing a ~60% premium to the African developer average. In October 2024, Zijin Mining paid US$1 billion for Newmont's Akyem project in Ghana at US$316/oz for resources and US$685/oz for reserves—premiums of 90% and 60% respectively over regional averages.

Beyond outright acquisitions, strategic equity investments in developers have increased. Lundin, Zijin, and Perseus have acquired stakes in Predictive Discovery, while Montage Gold established a strategic partnership with African Gold Limited. These investments potentially signal future M&A interest while supporting improved valuations for developers and explorers.

The most attractive M&A targets share common characteristics: large-scale or high-grade resources, near-term production potential, low technical risk (e.g., low strip ratios, free-milling ore), capital-efficient development pathways, and robust economics.

Companies Leading the West African Gold Sector

The West African gold sector features a diverse range of companies at various stages of development. Major producers with significant West African exposure include Newmont, Barrick Gold, Kinross Gold, and IAMGOLD, though these companies typically have diversified global operations. While these majors have important assets in the region, their West African operations represent only a portion of their global portfolios, with West African production comprising 12%, 20%, 25%, and 49% of their total gold production respectively.

Producers

Pure-play West African producers offer more direct exposure to the region's potential:

Perseus Mining has established itself as a premier mid-tier gold producer with operations spanning Ghana, Côte d'Ivoire, and Tanzania. The company operates three mines: Edikan in Ghana, Sissingué in Côte d'Ivoire, and Yaouré, its flagship operation also in Côte d'Ivoire. With a market capitalization of approximately US$3 billion, Perseus has demonstrated consistent operational performance, regularly meeting or exceeding production guidance. The company produced over 493,000 ounces of gold in FY2024 at an AISC of approximately US$1,050/oz, generating substantial free cash flow that has enabled both dividend payments and growth-focused investments.

Endeavour Mining stands as the largest pure-play West African gold producer with a market capitalization of around US$6.7 billion. The company operates a portfolio of mines across Senegal, Côte d'Ivoire, and Burkina Faso, producing over 1.1 million ounces annually. Endeavour has successfully executed a strategy of portfolio optimization, divesting non-core assets while developing high-margin, long-life operations. The company's flagship Houndé mine in Burkina Faso and Ity mine in Côte d'Ivoire anchor its production profile, while the Sabodala-Massawa complex in Senegal provides additional scale and diversification.

West African Resources has rapidly established itself following the successful development of its Sanbrado Gold Operation in Burkina Faso, which began production in 2020. The company has consistently delivered against guidance and recently expanded its footprint by acquiring the neighboring Kiaka project from B2Gold and Allied Gold. With a market capitalization of approximately US$1.7 billion, West African Resources is positioned for production growth, targeting over 400,000 ounces annually in the coming years as Kiaka is developed. The company's operations feature particularly high-grade open pit and underground resources, contributing to attractive margins.

Allied Gold is a relative newcomer to the public markets, having listed in 2023 after consolidating several assets. The company operates the Bonikro mine in Côte d'Ivoire and the Sadiola mine in Mali, with a combined production profile of approximately 240,000 ounces annually. With a market capitalization of around US$1.4 billion, Allied Gold has established a platform for growth through both existing asset optimization and potential M&A. The company's strategy focuses on establishing regional operating hubs in its core jurisdictions.

Resolute Mining operates the Syama mine in Mali and the Mako mine in Senegal, with a combined production of approximately 350,000 ounces annually. With a market capitalization of around US$620 million, Resolute has worked through operational challenges at Syama and has been implementing efficiency improvements to enhance margins. The Syama underground operation represents one of the few large-scale underground mines in West Africa, utilizing automated mining technology to access its substantial sulfide resource.

Development & Exploration Companies

Among developers and explorers, companies like Predictive Discovery (Guinea), Turaco Gold (Côte d'Ivoire), Newcore (Côte d'Ivoire), and Toubani Resources (Mali) represent the next generation of potential producers.

Predictive Discovery is advancing the Bankan Gold Project in Guinea, which hosts a substantial 5.38Moz gold resource. A 2024 Pre-Feasibility Study outlined a mine producing 269,000 ounces annually over a 12-year mine life at an attractive AISC of approximately US$1,150/oz. The company has attracted strategic investments from Lundin, Zijin, and Perseus, which collectively own significant equity stakes. Bankan's combination of scale, grade, and metallurgical simplicity positions it as one of the most promising undeveloped gold projects in West Africa.

Montage Gold is developing the Koné Gold Project in Côte d'Ivoire, which hosts a 4.01Moz reserve at 0.72g/t gold. Backed by the Lundin Group and with financing support from streaming partners Wheaton and Zijin, Montage has commenced construction with first production expected in Q2 2027. The project is forecast to produce an average of 233,000 ounces annually over its 16-year life, with the first three years averaging 349,000 ounces. With a market capitalization of approximately C$1.3 billion, Montage represents a fully-funded development story with significant exploration upside across its 2,138 km² land package.

Newcore Gold is advancing the Enchi Gold Project in Ghana, which currently hosts an Inferred resource of 1.4Moz at 0.62g/t gold. Located in the prolific Sefwi-Bibiani Gold Belt, Enchi benefits from excellent infrastructure and proximity to several operating mines. The company continues to expand the resource through ongoing drill programs, with multiple oxide gold targets across its 216 km² property. With modest capital requirements and favorable metallurgy, Enchi presents a potential pathway to production that aligns with the capital-efficient development model often seen in West African projects.

Turaco Gold is focused on the Afema Gold Project in Côte d'Ivoire, located in the southeastern part of the country near the border with Ghana. The company has identified multiple prospects across its extensive land package, with the Niamienlessa discovery showing particular promise. Turaco's strategic position in a relatively underexplored portion of the Birimian Greenstone Belt offers significant potential for resource growth. The company's management team brings substantial West African development experience, having previously been involved with successful projects in the region.

Toubani Resources is advancing the Kobada Gold Project in Mali, which has a resource base of approximately 3.1Moz. The project benefits from a high proportion of oxide ore, enabling a simple processing route with high recoveries. Located in southern Mali in a region with established mining operations, Kobada represents a scalable opportunity with relatively modest capital requirements. Toubani has focused on optimizing the project economics while navigating Mali's evolving regulatory environment, positioning the project for potential development as market conditions improve.

Beyond these established players, several emerging companies are advancing promising projects. African Gold Limited is exploring the Didievi Gold Project in Côte d'Ivoire, where it recently announced a strategic partnership with Montage Gold. Aurum Resources is developing the Boundiali Gold Project in northern Côte d'Ivoire, building on its 1.59Moz resource. Asara Resources is advancing the Kada Gold Project in Guinea's Siguiri Basin, while Awale Resources is exploring gold and copper targets at its Odienne project in Côte d'Ivoire.

Many Peaks Minerals is conducting exploration at its Ferké and Odienné projects in Côte d'Ivoire, while Montage Gold is developing the substantial Koné gold project in Côte d'Ivoire, which has a 4.01Moz reserve and is expected to begin production in 2027.

Investment Implications & Outlook

Following a relatively tumultuous period over 2021-2024 with numerous government changes and mining code revisions, the political landscape in West Africa appears to be stabilizing. Combined with gold prices near all-time highs and expectations for record free cash flow from producers, this creates a compelling opportunity for investors.

The substantial valuation discounts currently applied to West African gold companies may narrow as the gold cycle progresses. Intermediate West African producers are particularly appealing, with FCF yields projected to rise from single digits in 2024 to over 30% by 2026-2027, far exceeding developed market peers.

For investors, the key consideration is whether the risk premium demanded for West African exposure is excessive relative to the fundamental value offered. With strong operational performance from established producers, promising exploration upside, increasing M&A activity, and improving political stability, the case for increased exposure to West African gold equities is strengthening.

The region's combination of geological richness, operational advantages, and current undervaluation presents a potentially golden opportunity for investors willing to look beyond historical perceptions and focus on the evolving reality of West Africa as a premier gold-producing region.

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

.jpg)

Stay Informed