Western Mines Develops Australia's Largest Nickel Deposit with 5.3 Million Tons of Nickel

Western Mines discovers Australia's largest nickel sulfide deposit as market forms $15K floor. 5.3M tons contained nickel with massive sulfide upside potential.

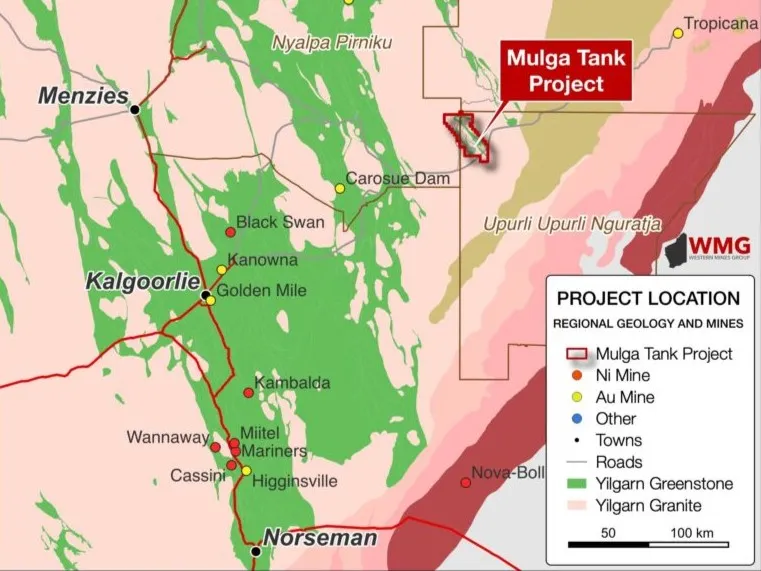

- Western Mines Group has discovered Australia's largest nickel sulfide deposit at their Mulga Tank project near Kalgoorlie, containing 5.3 million tons of nickel across a nearly 2 billion ton resource with grades of 0.27% nickel.

- The nickel market appears to be forming a price floor at $15,000/ton, with demand remaining robust at 6-7% annual growth in stainless steel and emerging defense applications growing at over 10% annually.

- Indonesian nickel producers are experiencing financial pressure leading to increased capital discipline and potential supply rationalization.

- Western Mines' Mulga Tank deposit represents a "hybrid system" combining large-scale disseminated mineralization with massive sulfide potential, positioning it as both a low-cost operation and high-grade discovery opportunity.

- The company has identified 91 occurrences of massive sulfide evidence in recent drilling, suggesting potential for a perseverance-style deposit worth 50 million tons at 2% nickel at depth.

The global nickel market stands at a critical inflection point, presenting compelling opportunities for investors willing to navigate near-term volatility for long-term structural gains. With prices having established what appears to be a durable floor around $15,000 per ton, the sector offers both defensive characteristics and significant upside potential as supply-demand dynamics realign.

Nickel Market Fundamentals Signal Recovery

The nickel market's current positioning reflects classic commodity cycle dynamics where sustained low prices drive supply discipline while demand remains structurally supported. Stainless steel demand continues growing at 6-7% annually, while emerging applications in defense and specialty alloys are expanding at double-digit rates. Perhaps most significantly, the battery sector, despite recent softness, maintains growth trajectories of 25-30% in key Western markets.

According to Caedmon Marriott, Managing Director of Western Mines Group,

"'Buy when prices are low' I think is often the mantra. But yeah, I mean there's some commentators out there talking about a breakout. We've seen a very much a descending wedge in prices. We've been bumping along the bottom now at that pretty hard floor of $15,000 a ton."

This price floor represents more than technical support – it reflects the economic reality that marginal producers across the globe are operating at break-even or loss-making levels, creating conditions for supply rationalization.

Indonesian Supply Discipline

Indonesia's dominance in global nickel production has been a persistent concern for investors in Western nickel assets. However, recent developments suggest this dynamic may be shifting favorably. The Indonesian nickel conference in June 2024 revealed a markedly subdued industry mood, with even large Chinese producers acknowledging profitability challenges at current price levels.

The Indonesian government has implemented measures that are inadvertently supporting higher nickel prices by limiting ore supply and discussing increased royalty rates.

Marriott observed, "This year was a lot more subdued mood and even the large Chinese producers, the guys with economies of scale, were commenting that absolutely nobody is making money at these prices."

Thes policy changes, combined with the natural progression toward lower-grade deposits as higher-grade resources are depleted, suggest a structurally higher cost environment for Indonesian production. This represents a fundamental shift from previous years when expansion plans and capital investments were prominent discussion topics.

The Green Nickel Premium

Environmental considerations are increasingly influencing nickel sourcing decisions, particularly in battery applications where carbon intensity regulations are becoming mandatory. European battery passport requirements for electric vehicles will require detailed CO2 accounting, with nickel representing 30-35% of a Tesla's entire CO2 budget. This regulatory framework creates structural advantages for Western sulfide producers, who typically operate at the bottom of the CO2 intensity curve.

Western sulfide producers like Western Mines Group are uniquely positioned to benefit from these converging trends. Their operations typically feature lower carbon intensity, established regulatory frameworks, and proximity to key battery manufacturing markets in North America and Europe.

Marriot emphasized,

"If that's 16,000-18,000 tons, and if you can be a western world sulfide producer which is always going to come in towards the bottom end of the cost curve and CO2 intensity curves and all that sort of good green nickel stuff, then there is structural headroom for you to make a margin for the life of your project."

While price premiums for "green nickel" remain uncertain, supply chain security considerations and environmental regulations are driving preferences toward Western producers over Chinese-controlled Indonesian operations. This trend aligns with broader geopolitical shifts toward supply chain diversification and critical mineral security.

Mulga Tank: Australia's Largest Nickel Sulfide Deposit

Western Mines Group exemplifies the strategic opportunities available in the nickel sector. The company's Mulga Tank project represents Australia's largest nickel sulfide deposit, containing 5.3 million tons of nickel across a nearly 2 billion ton resource. This scale positions the project among the top 10 globally, with grades of 0.2% nickel that compare favorably to Canadian peers while offering four times the sulfur content.

Resource Quality & Scale

The deposit's geological characteristics suggest significant economic advantages. With a sulfur-to-nickel ratio approaching pentlandite composition and enrichment in chalcophile and platinum group elements, the mineralization represents high-quality nickel sulfide. The company has defined this resource using a 0.2% nickel cutoff, double the threshold used by many Canadian projects, demonstrating conservative resource estimation practices.

The indicated portion of the resource contains approximately 1.6 million tons of nickel at 0.28% grade across 560 million tons, with an additional 3.7-3.8 million tons in the inferred category. This scale enables low-cost, high-volume operations typical of successful large-scale mining projects.

Beyond the large-scale disseminated resource, Western Mines has identified compelling evidence for massive sulfide deposits that could dramatically enhance project economics. Recent drilling has revealed 91 occurrences of massive sulfide evidence, including structurally remobilized material and large immiscible sulfide globules described as "tennis ball-sized."

The statistical probability of encountering these features across such a limited drilling program suggests a substantial massive sulfide system at depth. If Western Mines can delineate a "Perseverance-style" deposit of 50 million tons at 2% nickel, it would transform the project's development profile and timeline.

Interview with Managing Director, Caedmon Marriott

Operational Advantages

The project's location in Western Australia provides significant operational and jurisdictional advantages. Government support through exploration incentive schemes demonstrates regulatory backing for critical mineral development. The deposit's shallow nature, with mineralization beginning at 50-60 meters below surface, and low anticipated strip ratios of less than 2:1 support low-cost mining scenarios.

Benchmarking against successful large-scale operations like Boddington Gold Mine, which processes 37 million tons annually at 0.6 grams per ton gold, suggests that scale can overcome grade concerns when unit costs are controlled effectively.

Development Pathway & Risk Considerations

Western Mines has established a systematic development approach that balances near-term value demonstration with longer-term upside potential. The company's strategy involves advancing metallurgical testing and scoping studies on the defined resource while simultaneously pursuing high-grade massive sulfide targets through ongoing drilling programs.

The modular development concept, potentially starting at 10 million tons annually before scaling to 40 million tons, offers a risk-managed approach to capital deployment. This strategy allows for operational learning and cash flow generation to fund subsequent expansion phases.

Current drilling programs, supported by government grants totaling $220,000, focus on extending known mineralization and testing massive sulfide targets at depth. Results from these programs will provide critical data for resource upgrades and economic assessments expected in early 2025.

The Investment Thesis for Western Mines Group

- Scale Advantage: With 5.3 million tons of contained nickel, Western Mines owns Australia's largest nickel sulfide deposit and ranks among the world's top 10, providing significant economies of scale for long-term operations.

- Quality Resource: The deposit offers superior metallurgical characteristics with four times the sulfur content of Canadian peers and grades 25% higher than comparable projects, supporting enhanced nickel recovery and processing efficiency.

- Exploration Upside: Recent drilling has identified 91 massive sulfide occurrences, suggesting potential for a "Perseverance-style" high-grade deposit at depth that could accelerate development timelines and enhance project economics.

- Jurisdictional Benefits: Western Australian location provides political stability, established mining infrastructure, and government support through exploration incentive schemes, reducing operational and regulatory risks.

- Market Timing: Entry at current nickel price levels near $15,000 per ton provides defensive positioning with significant upside potential as supply discipline and demand growth drive price recovery.

- Strategic Optionality: The hybrid nature of the deposit allows for flexible development scenarios, from large-scale low-grade operations to higher-grade standalone developments, optimizing capital deployment based on market conditions.

- Environmental Positioning: As a Western sulfide producer, the company is well-positioned to benefit from increasing preference for low-carbon nickel in battery applications and supply chain security considerations.

The nickel sector presents a compelling investment opportunity characterized by defensive price levels, improving supply-demand fundamentals, and structural shifts favoring Western producers. Western Mines Group exemplifies these trends through its world-class resource, strategic location, and systematic development approach. The company's ability to demonstrate both large-scale resource potential and high-grade exploration upside positions it favorably for multiple development scenarios as market conditions evolve.

Investors should consider nickel exposure as both a defensive commodity play at current price levels and a strategic position in the energy transition. The sector's current distressed state masks underlying strength in demand fundamentals and emerging supply constraints that could drive significant price appreciation over the medium term.

Macro Thematic Analysis: The Nickel Transition

The global nickel market is experiencing a fundamental transition driven by the intersection of traditional demand growth, emerging energy storage applications, and evolving geopolitical dynamics. This transition presents both challenges and opportunities that will reshape the competitive landscape over the next decade.

Traditional stainless steel demand continues providing a stable foundation with 6-7% annual growth, while newer applications in defense and specialty alloys are expanding at double-digit rates. The battery sector, despite recent volatility, maintains structural growth potential as electric vehicle adoption accelerates and grid storage requirements expand. These demand drivers create a robust foundation for long-term nickel consumption growth.

Supply-side dynamics are equally compelling, with Indonesian dominance creating both opportunities and risks. While Indonesia's low-cost lateritic nickel has pressured prices, environmental regulations and supply chain security concerns are driving preferences toward Western sulfide producers. The natural progression toward lower-grade Indonesian deposits, combined with increasing royalty rates and environmental compliance costs, suggests structurally higher production costs over time.

The most significant development is the emergence of carbon intensity as a competitive factor. European battery passport requirements and corporate sustainability commitments are creating tangible advantages for low-carbon nickel producers. This trend extends beyond environmental considerations to encompass supply chain security and geopolitical risk management.

This structural positioning suggests that current market conditions may represent a generational opportunity for investors to access high-quality nickel assets at attractive valuations before broader market recognition of these fundamental shifts drives significant revaluation.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed