Western Supply Chain Realignment Drives Strategic Premium for Ex-China Critical Minerals Developers

Western policy is driving a structural repricing of critical minerals, favoring low-cost, ex-China projects with processing capacity.

- Western governments are systematically embedding critical minerals supply chain security into legislation, sovereign financing, and bilateral trade frameworks, creating a structural, not cyclical, repricing of ex-China mineral assets.

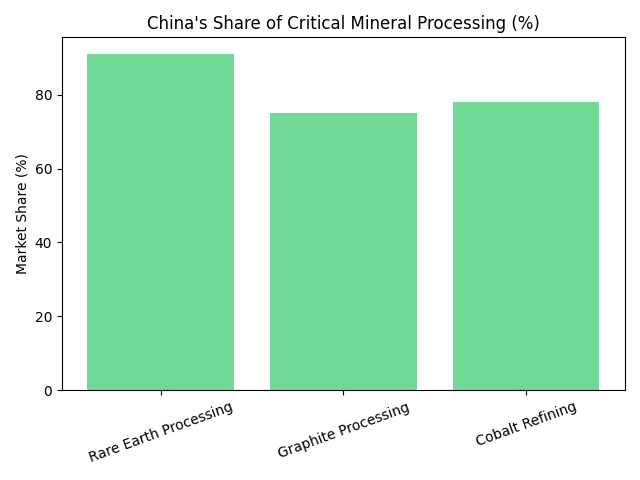

- China's dominance across rare earth processing (91%), nickel supply chains, graphite (75% of global processing), and cobalt refining (78%) represents a concentrated vulnerability that geopolitical friction is now forcing Western economies to address at speed.

- Policy-driven supply discipline, from Indonesia's 2026 RKAB quota cut to the DRC's cobalt export controls and China's rare earth export restrictions, is shifting commodity pricing from demand-pull dynamics to state-managed corridors, fundamentally altering how mining projects should be valued.

- The investment filter has narrowed: first-quartile all-in sustaining cost (AISC), processing route differentiation, permitting visibility, and jurisdictional alignment with Minerals Security Partnership countries now determine which development-stage projects attract institutional capital.

- Late-2026 Final Investment Decisions (FIDs) and construction starts across nickel, rare earths, graphite, and rutile represent the primary valuation inflection points investors should be tracking now.

The Policy Inflection Point: From Market Commodity to Strategic Asset

Critical minerals are no longer purely market-driven commodities. In just 18 months, Indonesia cut its 2026 nickel ore quota from 379 million tonnes to about 260 million; the DRC imposed cobalt export quotas that lifted CME cobalt prices from roughly $10/lb in early 2025 to $25/lb by February 2026; and China’s rare earth export controls pushed NdPr prices up 41% in early 2026. These moves reflect a broader pattern of resource nationalism reshaping global supply.

S&P Global’s 2026 Metals Price Outlook reflects this shift, projecting copper up 14.5% and cobalt up 57%, driven more by policy than demand cycles. A macro backdrop of 3.2% global GDP growth, AI-driven infrastructure investment, and a softer US dollar further supports critical minerals prices.

Western policy responses are also structural. The US passed H.R. 3617 mandating DOE critical mineral risk assessments, Canada and Australia joined the G7 Critical Minerals Production Alliance, and Chile and the United States launched rare earth and critical minerals cooperation under President José Antonio Kast. The result is a bifurcated market where traceable, ESG-aligned supply from allied jurisdictions commands a growing premium in capital flows, offtake agreements, and sovereign co-investment.

China's Processing Stranglehold: Why Mining Alone Is Not Enough

The case for ex-China critical minerals hinges on the gap between resource availability and processing capacity. China controls 69% of mined rare earth supply and 91% of processing, along with 94% of rare earth magnet production. It also processes about 75% of global natural graphite and refines 78% of cobalt despite relying on DRC feedstock. Western rare earth supply contracts still reference Chinese ex-works indices under Beijing’s 1998 Pricing Law, creating price opacity that distorts project economics for non-Chinese developers.

The Separation Bottleneck Across Rare Earths, Graphite & Nickel

Greenfield mining alone will not fix the processing bottleneck. S&P Global lists 161 ex-China rare earth projects, yet industrial-scale separation and magnet alloying remain concentrated in China. Permitting for radioactive materials, especially monazite processing, also makes existing separation facilities strategic assets.

Energy Fuels Inc. operates the White Mesa Mill in Utah, the only US facility able to process monazite into separated rare earth oxides. Benchmark Mineral Intelligence estimates its projects could supply up to 85% of US heavy rare earth oxide demand by 2032. A similar constraint exists in graphite: China processes roughly 75% of global supply, and although US antidumping duties on Chinese graphite anode materials may support regional premiums, the ex-China supply chain remains limited. Energy Fuels Chief Executive Officer Mark Chalmers has consistently framed the company's strategy around the structural gap that separates miners from downstream producers:

"To really compete with China, you have to have all those steps. You can't be missing a step in the middle of it. We've cracked the code by putting all these pieces together, from mining all the way through alloys."

The proposed ~US$299M acquisition of Australian Strategic Materials adds its Korean Metals Plant, one of the few non-China facilities producing NdPr, dysprosium, terbium metals, and NdFeB alloys. The combined company would become the largest fully integrated rare earth mine-to-metal-and-alloy producer outside China, a position difficult to replicate under current policy and development timelines.

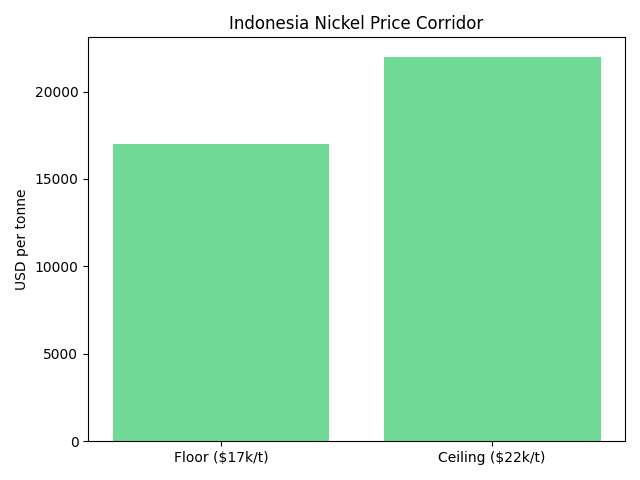

Indonesia's Managed Corridor: Nickel Pricing Shifts From Demand-Pull to Policy-Defined

For nearly five years, Indonesian nickel pig iron and HPAL expansions compressed margins, pushing Nickel prices down about 70% from the 2022 peak to ~$14,000/t by late 2025 and delaying Western FIDs. That dynamic now appears structural rather than cyclical.

Indonesia’s 2026 RKAB quota cut to ~260 Mt, alongside the IndoPhil Nickel Corridor covering ~75% of global output, signals coordinated supply discipline. Because Indonesia’s royalties are tied to prices, the implied corridor is roughly $17,000/t as a floor to protect revenue and ~$22,000/t as an informal ceiling to avoid triggering Western sulphide restarts.

China’s Share of Critical Mineral Processing (%). Source: Crux Investor Research

Cost Curve Position as the Primary Investment Filter

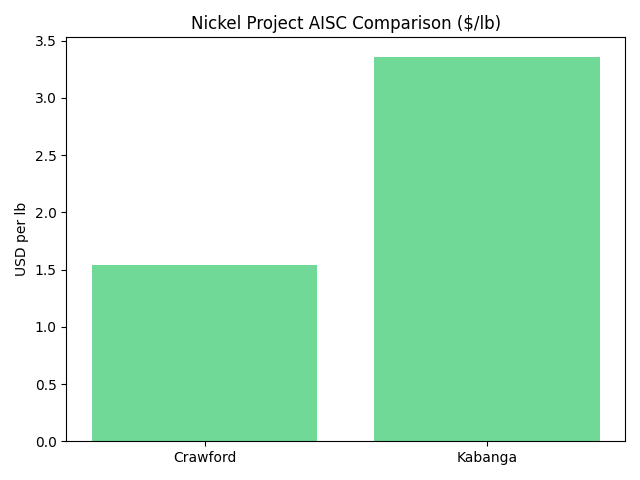

Within this managed price band, durable nickel investments share four traits: AISC below $4/lb, sulphide processing for traceability and lower emissions, alignment with Western jurisdictions, and credible, funded development timelines. Canada Nickel is advancing the Crawford Nickel Sulphide Project in Ontario, with C1 cash costs of $0.39/lb and AISC of $1.54/lb (March 2025 FEED). At $20,000/t nickel, Crawford ranks in the first global cost quartile with an after-tax NPV of $2.8B (8% discount) and a 17.6% IRR. It is also the only Canadian project with both federal and provincial backing, alongside a $500M Letter of Interest from Export Development Canada.

Canada Nickel Chief Executive Officer Mark Selby describes the district-scale opportunity that underlies Crawford's strategic value:

"Advancing the Crawford nickel sulfide deposit to a construction decision later this year, and unlocking the world's largest nickel sulfide district with the Timmins Nickel District. Over a 10- or 15-year period, you can get to 250,000 or 300,000 tons of nickel potentially coming out of this district."

Strategic Supply and Geopolitical Alignment

Lifezone Metals is advancing the Kabanga Nickel Project in Tanzania, a ~50 Mt high-grade (~2% Ni) sulphide deposit. The July 2025 Feasibility Study outlines an after-tax NPV of ~$1.58B (8% discount), a 23.3% IRR, and AISC of $3.36/lb after byproduct credits.

Infrastructure and permitting risks are largely addressed, with rail and grid power in place and a life-of-mine license secured. The US International Development Finance Corporation has completed due diligence, supporting Western financing ahead of a mid-2026 FID.

Lifezone Metals Chief Financial Officer Ingo Hofmaier has articulated the defense supply chain dimension that elevates Kabanga beyond a conventional mining investment:

"A deposit like Kabanga ensures traceability of nickel sulfates that ultimately go through Western smelters and end up in the defense industry. There's a very strong realization that this is a strategic asset."

Beyond Nickel: Rare Earth Processing, Graphite & Rutile Enter the Institutional Frame

The structural logic that governs nickel, processing bottleneck, policy premium, jurisdictional alignment, applies with equal force across rare earths, graphite, and rutile. Each commodity confronts a version of the same problem: Western resource availability substantially exceeds Western processing capability, and that gap is not closed by mine development alone.

Rare Earth Processing Infrastructure as a Strategic Barrier to Entry

Rare earth pricing in 2026 is policy-driven rather than demand-driven. NdPr is ~$130/kg (Europe), dysprosium ~$1,125/kg, and terbium ~$4,500/kg, levels reflecting China’s export controls and the lack of Western pricing benchmarks.

Energy Fuels Inc.’s January 2026 feasibility study for Phase 2 at White Mesa targets annual output of 5,513 t NdPr, 165 t dysprosium, and 48 t terbium over a 40-year life. Capex is ~$410M, with an NPV of $1.9B (8%) and a 33% IRR. US Department of Defense support, including a NdPr floor price framework, reinforces rare earth processing as a national security priority.

Graphite & Rutile: Battery Anode & Aerospace Exposure in a Tariff-Reshaped Market

China’s dominance in graphite processing mirrors rare earth vulnerabilities, now being priced into Western markets following US trade action. Sovereign Metals is advancing the Kasiya Rutile-Graphite Project in Malawi, the world’s largest known rutile deposit and second-largest natural graphite resource.

The January 2025 Optimised PFS outlines a $2.3B pre-tax NPV, 27% IRR, $665M capex, and ~$409M average annual EBITDA over 25 years. Saprolite-hosted mineralization eliminates drilling and blasting, enabling ultra-low graphite costs of ~$241/t. Japan’s $7B Nacala Corridor investment further de-risks logistics and supports strategic offtake potential.

Sovereign Metals Chairman Ben Stoikovich quantifies the competitive margin that Kasiya's cost structure creates even against current Chinese supply:

"The incremental cost to produce a ton of graphite as a by-product will only be $241 per ton. Where other projects can't make money in the current market, we'd be selling graphite at a 50% operating margin."

Rio Tinto has invested US$60 million and holds a 19.9% strategic stake in Sovereign Metals. The Kasiya project is now overseen by a joint Sovereign-Rio technical committee, and the definitive feasibility study is advancing under that combined oversight, a partnership structure that materially de-risks both the technical and financing pathways.

Government Capital as a De-Risking Mechanism: Permitting, Financing & Sovereign Co-Investment

Government endorsement is now a capital signal, not symbolic, compressing permitting timelines, unlocking financing, and attracting sovereign co-investment. Canada’s Major Projects Office designation for Crawford, alongside Ontario’s “One Project, One Process,” reduces permitting risk and could shorten timelines by 12-18 months on a >$2B project.

This pattern is consistent: where government capital leads, institutional capital follows. US DFC due diligence supports Kabanga’s financing, Department of Defense pricing frameworks improve revenue visibility for Energy Fuels Inc., and Japan’s Nacala Corridor investment de-risks Kasiya. These interventions act as first-mover signals in a market where execution risk remains the key constraint.

The Investment Thesis for Critical Minerals

- Indonesia’s $17,000–$22,000/t price corridor supports a durable floor, positioning low-cost sulphide projects like Crawford and Kabanga as structurally advantaged.

- Rare earth processing scarcity creates strong moats; Energy Fuels’ White Mesa Mill is unique strategic infrastructure that is difficult to replicate.

- Alignment with MSP countries and active government support reduces permitting and financing risk versus non-aligned projects.

- Kasiya’s low-cost graphite (~$241/t) enables ~50% operating margins, remaining competitive even against Chinese supply.

- Late-2026 FIDs for Crawford, Kabanga, and Kasiya are key valuation inflection points for 18-36 month investors.

- Processing route differentiation and traceability are now commercial requirements, driven by OEM supply chain due diligence.

The structural realignment underway in critical minerals markets is not a commodity supercycle. It is a policy-driven repricing of supply chain security, and it favors a narrow set of projects that combine first-quartile cost discipline, processing capability or partnerships, advanced permitting, and jurisdictional alignment with Western capital frameworks.

The previous cycle rewarded resource scale and volume growth. The current cycle rewards execution credibility. The projects approaching Final Investment Decision in late 2026,across nickel sulphide, rare earth processing, graphite, and rutile, are not simply well-positioned for a price recovery. They are structurally aligned with the investment architecture that Western governments, development finance institutions, and industrial original equipment manufacturers are building out for the next decade.

TL;DR

Western governments are actively reshaping critical minerals markets through policy, financing, and supply controls, turning them from cyclical commodities into strategic assets. China’s dominance in processing, not just mining, has exposed a structural bottleneck that Western economies are now racing to address, creating a premium for ex-China, traceable supply. As a result, only a narrow group of projects, those with low costs, integrated or partnered processing, strong permitting visibility, and alignment with Western jurisdictions, are attracting capital. Key assets like Crawford, Kabanga, and Kasiya, alongside infrastructure like Energy Fuels’ White Mesa Mill, sit at the center of this shift, with late-2026 Final Investment Decisions representing major valuation catalysts. The core takeaway: this is not a typical commodity cycle, but a policy-driven repricing where execution, integration, and geopolitics determine winners.

FAQs (AI generated)

Critical minerals are being repriced because governments are intervening directly in supply chains to secure strategic materials, rather than leaving pricing purely to market forces. Export controls, production quotas, and sovereign financing, such as Indonesia’s nickel quotas or China’s rare earth restrictions, are creating supply constraints that elevate prices. At the same time, Western policies are incentivizing domestic or allied supply, meaning capital is flowing preferentially into projects that meet geopolitical and regulatory criteria, not just economic ones.

China’s control is concentrated in processing rather than just mining, which is the most technically complex and capital-intensive part of the value chain. Even when raw materials are mined elsewhere, they often depend on Chinese refining and downstream conversion into usable products like magnets or battery materials. This creates a chokepoint that exposes Western industries, especially defense and energy, to supply disruptions, making processing capacity outside China strategically critical.

The investment bar has risen significantly. Projects now need to demonstrate first-quartile cost positions (e.g., low AISC), clear processing pathways (either in-house or via partnerships), strong permitting progress, and alignment with Western jurisdictions or Minerals Security Partnership countries. Institutional capital is no longer chasing resource size alone, it is prioritizing execution certainty, traceability, and geopolitical alignment.

Because the bottleneck is no longer resource availability, it’s conversion into usable materials. There are many known deposits globally, but very few facilities capable of separating, refining, and producing end-use materials at scale. Without processing, new mines cannot fully participate in supply chains or capture pricing premiums, which is why assets like the White Mesa Mill or downstream alloy capabilities are considered strategic infrastructure.

The most important catalysts are Final Investment Decisions (FIDs) and construction starts, particularly for projects like Crawford, Kabanga, and Kasiya targeting late 2026. These milestones signal that financing, permitting, and offtake agreements are secured, significantly reducing execution risk. Investors positioning ahead of these events are effectively betting on which projects will transition from development-stage narratives into fully funded, policy-aligned supply chain assets.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed