Why Silver Represents One of 2025's Most Compelling Investment Opportunities

Silver hits record highs as five-year supply deficit totals 820M oz. Industrial demand, tight supply, and macro support create compelling $65-95/oz upside case.

- Silver reached $53.14 per ounce on November 26, 2025, representing a 76.51% increase year-over-year, with the market experiencing its fifth consecutive annual supply deficit totaling approximately 820 million ounces since 2021, equivalent to an entire year of average mine output.

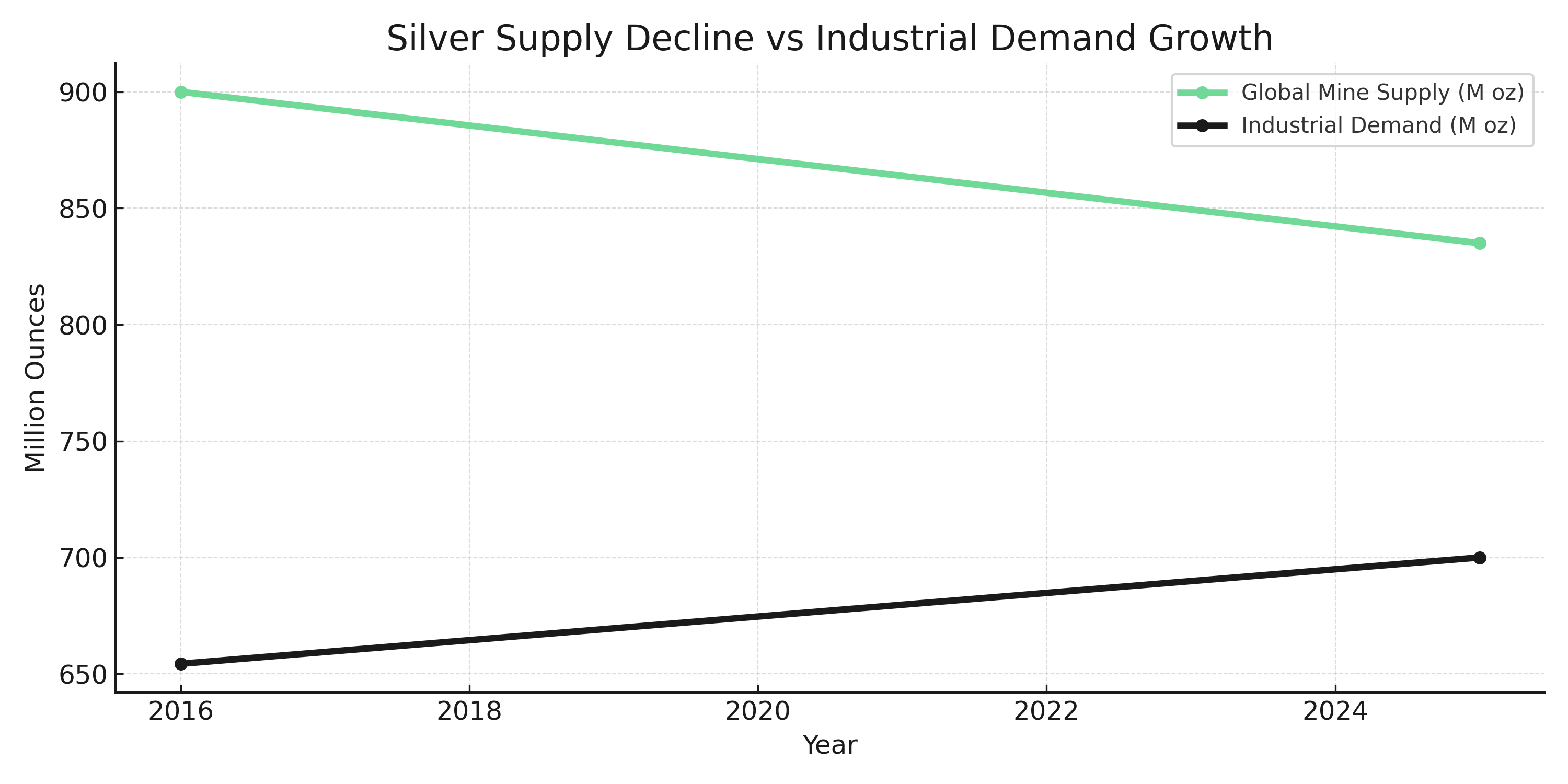

- Industrial fabrication is forecast to grow by 3% in 2025, with volumes projected to surpass 700 million ounces for the first time, driven by photovoltaic applications, electronics manufacturing, and electric vehicle production, establishing a stable consumption floor independent of investment cycles.

- Global silver mines are projected to yield 835 million ounces in 2025, representing a 7.23% decrease compared to 2016 levels, while mine output peaked in 2016 at 900 million ounces and has declined an average of 1.4% annually, with limited new projects coming online to offset production challenges.

- Bank of America raised its 12-month silver target to $65 per ounce after real yields narrowed and ETF inflows strengthened, with geopolitical tensions, trade policy uncertainty, and concerns about U.S. public debt driving portfolio diversification into precious metals.

- The gold-silver ratio remains elevated near 79:1 compared to the 25-year average of 69:1, suggesting silver is undervalued relative to gold and positioning it for potential catch-up gains as industrial demand intersects with safe-haven buying in a supply-constrained market.

Introduction: A Market Transformed

Silver has entered a new regime. After decades of trading in gold's shadow, the white metal has emerged as one of 2025's strongest-performing assets, driven by forces that extend far beyond traditional safe-haven demand. The convergence of structural supply deficits, accelerating industrial consumption, and a supportive macroeconomic environment has created conditions that many analysts believe could propel silver to price levels not seen in generations.

Silver reached an all-time high of $54.47 on October 17, 2025, surpassing its previous nominal peak and signaling a fundamental shift in market structure. This performance reflects more than speculative enthusiasm; it represents the intersection of tightening physical markets, strategic metal scarcity, and the metal's unique dual identity as both an industrial input and a monetary hedge.

For investors seeking asymmetric upside in a world of elevated valuations and geopolitical uncertainty, silver presents a compelling case. The metal trades at the nexus of multiple investment themes: the energy transition, technological advancement, monetary debasement concerns, and supply-chain nationalism.

The Structural Deficit: Five Years of Cumulative Scarcity

Unlike most commodities, silver's supply-demand imbalance is not cyclical; it is structural and deepening. The silver market is on track for its fifth straight supply deficit, with the cumulative 5-year market deficit projected to reach 820 million ounces, equivalent to an entire year of global mine production.

The silver market is forecast to record another significant deficit for the fifth consecutive year in 2025, with industrial demand remaining the key driver of this favorable supply-demand backdrop and volumes projected to hit a new record high. This is not a temporary mismatch; it reflects fundamental constraints on the supply side coinciding with structural growth in demand.

The persistence of this deficit matters. When markets remain in shortage for multiple consecutive years, above-ground inventories become the marginal source of supply. The silver market continues the chapter of structural undersupply, with deficits totaling almost 820 million ounces since 2021, providing an explanation for recent price spikes and temporarily strained liquidity at exchanges like the CME. This cumulative drawdown effect distinguishes silver from other industrial metals that can respond more quickly to price signals.

Industrial Demand: The Strategic Metal Story

Silver's industrial applications have fundamentally changed the metal's investment profile. Once dominated by jewelry and silverware, silver consumption is now anchored by technology sectors with secular growth trajectories.

Industrial demand for silver increased for the fourth year in a row in 2024, rising 4% and setting a record of 680.5 million ounces, attributed mainly to the green economy including photovoltaics and artificial intelligence. Photovoltaic applications alone account for a significant and growing share of this demand, with solar panel deployment exceeding expectations by 200% during the 2010s.

The clean energy transition provides a stable demand floor. Solar power has become cost-competitive with fossil fuels, making it attractive for large-scale deployment including data centers. Data center power demand over the next four years is expected to grow 21%, and AI is expected to see a 33% annual growth in electricity demand over the next four years, much of which will be met by solar installations requiring silver paste in photovoltaic cells.

Beyond solar, silver's unique properties make it irreplaceable in many applications. Electronics manufacturing, automotive electrification, 5G infrastructure, and medical devices all require silver inputs with limited substitution potential at current prices. This industrial demand base differs fundamentally from investment-driven demand, as industrial consumers are relatively price-inelastic in the short term.

Supply Side Constraints: Why Production Cannot Keep Pace

The supply response to higher silver prices has been muted, and structural factors suggest this will continue. Global silver mines are projected to yield 835 million ounces in 2025, a 7.23% decrease compared to 2016 levels, despite silver prices roughly doubling over that period.

Silver mine output peaked in 2016 at 900 million ounces, and up until last year, silver production had dropped by an average of 1.4% each year. Multiple factors drive this decline: reserve depletion at major mines, falling ore grades, mine closures, and underinvestment in exploration and development.

The nature of silver production adds another layer of constraint. Approximately 70% of mined silver comes as a by-product of base metal mining or gold mining. This means primary silver supply is largely determined by demand for other metals, not by silver prices alone. Mine production is expected to reach a seven-year high in 2025, rising by 2% to 844 million ounces, with increased output anticipated from both existing and new operations in several markets. However, this modest growth pales in comparison to demand increases.

The development timeline for new silver mines compounds the supply challenge. From discovery to production typically requires 10-15 years and hundreds of millions of dollars in capital investment. With limited exploration budgets during silver's extended bear market from 2011-2020, the project pipeline is thin.

Macroeconomic Tailwinds: Monetary & Geopolitical Support

Silver's 2025 surge has been amplified by macroeconomic factors that historically favor precious metals. Concerns about President Donald Trump's anticipated tariff policies have fueled short covering and deliveries of silver into CME warehouses since late 2024, coupled with rising economic and geopolitical uncertainties, underpinning a healthy recovery in silver prices.

Real interest rates represent a critical driver for non-yielding assets like precious metals. As of October 20, 2025, silver price movements are supported by a softer U.S. dollar, with the DXY hovering near 103.2, while U.S. 10-year Treasury yields have eased to 4.6% following Federal Reserve minutes that signaled a pause in further rate hikes.

Lower real yields reduce the opportunity cost of holding silver, making it more attractive relative to bonds and cash. This dynamic is particularly powerful when combined with concerns about currency debasement and fiscal sustainability. U.S. federal debt exceeding $35 trillion and persistent fiscal deficits have renewed interest in hard assets as portfolio insurance.

The Gold-Silver Ratio: A Valuation Opportunity

One of the most compelling arguments for silver comes from its relationship with gold. Since 2000, the gold-silver ratio has averaged 69:1; however, in 2025 it has been significantly higher, reaching 104:1 in May, and although it has fallen, the ratio remains above the 25-year average, reaching 79:1 in October. This elevated ratio suggests silver is undervalued relative to gold.

If gold continues rising and the gold-silver ratio reverts toward its historical average, silver could experience substantial appreciation. Using $3,700 per ounce gold and the average ratio going back to 2000 puts silver at $54, beyond that all-time high potentially easily just based on that ratio, with further upside possible if gold advances and the ratio compresses.

This mean-reversion dynamic has historically created explosive moves in silver. When the ratio reaches extreme levels and then snaps back, silver typically outperforms gold significantly over the subsequent 12-24 months.

Company Case Studies: Americas Gold & Silver: Consolidating Idaho's Silver Valley

Americas Gold & Silver is executing a transformational consolidation strategy in Idaho's historic Coeur d'Alene Mining District. The November 2025 announcement of the Crescent Mine acquisition for $56 million represents a watershed moment, adding approximately 3.8 million ounces of measured and indicated silver resources and 19.1 million ounces inferred, located just 9 miles from the company's existing Galena Complex. The acquisition delivers immediate value through processing synergies, as Galena's mills operate at roughly 400 tonnes per day against 1,558 tpd installed capacity.

The Galena Complex is experiencing a technical renaissance through near-mine discoveries. Recent results include the 034 Vein discovery intersecting 3.4 meters at 983 g/t silver plus copper, and the 149 Vein returning 0.21 meters at 24,913 g/t silver. The company also operates as the largest primary antimony producer in the United States with approximately 450,000 pounds produced year-to-date in 2025.

Americas Gold & Silver derives over 80% of revenue from silver and operates one of the world's highest-grade active silver mines at 480 g/t, yet trades at approximately 0.76× net asset value. Near-term catalysts include Crescent acquisition closing, the 2026 drilling program, and quarterly production scaling toward 3-4 million ounces annually.

Paul Andre Huet, Chairman and CEO, emphasized the strategic rationale:

"The addition of the high-grade silver Crescent Mine to Americas portfolio, located just 9 miles by road from our producing Galena Complex, is a very compelling and synergistic acquisition opportunity that immediately capitalizes on the spare milling capacity at our Galena and Coeur mills. I am also extremely encouraged by the strong exploration upside at Crescent."

GR Silver Mining: High-Grade Discovery and Resource Expansion

GR Silver Mining has established itself as a high-grade silver explorer advancing a 134 million ounce silver equivalent resource across its San Marcial Area and permitted Plomosas Mine in Mexico's Sierra Madre Occidental. The November 19, 2025 release of drillhole SMS25-12 results validates the company's thesis, with intercepts of 5.0 meters at 232 g/t silver including three distinct high-grade zones: 0.9 meters at 956 g/t, 0.2 meters at 2,602 g/t, and 0.3 meters at 1,061 g/t silver.

The San Marcial system represents a classic epithermal silver district with approximately 80% of the property remaining untested. GR Silver has allocated resources for a fully funded 15,000-meter step-out drilling program in H1 2026, with longer-term resource growth targets of 200-400 million ounces silver equivalent. The fully permitted Plomosas underground mine provides strategic de-risking capability through near-term bulk sample test mining.

With a market capitalization of approximately C$127.5 million and $12.4 million cash, GR Silver trades at conservative valuations. The stock gained 71% year-to-date in 2025. Near-term catalysts include ongoing drill results, bulk sample commencement, and a preliminary economic assessment for San Marcial scheduled for H2 2026.

Marcio Fonseca, President & CEO, articulated the growth vision:

"The recent success of step-out drilling at the San Marcial Area in 2025 further strengthens our confidence in a large, continuous silver-mineralized system at San Marcial. We are planning a significant step-out drilling program in the first half of 2026 that could potentially double the existing silver mineralization footprint to support resource growth at San Marcial."

Vizsla Silver: Fully Financed Development of World-Class Panuco

Vizsla Silver has transformed from explorer to fully financed developer through the November 24, 2025 closing of $300 million in convertible notes, providing more than double the capital required to construct its Panuco Project in Mexico toward first silver production in H2 2027. The 5% coupon represents approximately 50% lower cost than conventional project finance, while combined with approximately $200 million cash pre-financing, Vizsla now commands over $500 million in total financing capacity.

The Panuco Project delivers world-class economics: $1.137 billion post-tax NPV, 86% IRR, 9-month payback, and $9.40/oz all-in sustaining costs across a 10.6-year mine life. The January 2025 updated resource totals 222 million ounces measured and indicated silver equivalent plus 138 million ounces inferred. The 40,000+ hectare land package encompasses over 93 kilometers of mapped vein strike with only 30% drilled.

Despite world-class economics and full construction financing, Vizsla trades at significant discount to producers, with developers averaging 0.56× price-to-NAV versus producers at 1.59×. At approximately $1.41 billion market capitalization, the company trades below preliminary economic assessment NAV exceeding $10/share before incorporating unexplored district upside.

Michael Konnert, CEO, highlighted the financing advantages:

"Vizsla Silver greatly appreciates the strong support from a global institutional investor base for this Offering. The Notes' coupon reduces our previously expected debt service obligations during the expected construction and commissioning phase of the Panuco project, and the unsecured, covenant-light structure provides us with greater financial flexibility as we move towards developing Panuco while undertaking an aggressive exploration program across our portfolio."

Cerro de Pasco Resources: Innovative Tailings Reprocessing

Cerro de Pasco Resources pursues a fundamentally different approach to silver production: reprocessing historic mine tailings rather than conventional mining. The Quiulacocha tailings in Peru's Cerro de Pasco district contain an estimated 423 million ounces silver equivalent, representing one of the world's largest above-ground metal inventories. The November 2025 closing of $22.7 million in combined private placements funds drilling to validate historic estimates and transition toward NI 43-101-compliant resources.

The Phase 1 drilling program confirms high-value metals with average grades of 1.66 oz/t silver, 1.47% zinc, 0.89% lead, 53.2 g/t gallium, and 5.5 oz/t silver equivalent. The fundamental economic advantage centers on extraction costs of $1-2 per tonne versus $30-200 per tonne for conventional underground mining. Internal base case economics project $39/tonne profit and $2.9 billion life-of-mine profit over 20 years.

Beyond economics, the project addresses environmental remediation by removing acid mine drainage sources. Gallium exposure is particularly strategic, as China controls 98% of global production. With $270 million market capitalization reflecting $0.64 per in-situ silver equivalent ounce, Cerro de Pasco trades at substantial discount to conventional projects.

Guy Goulet, CEO, emphasized the financial milestone:

"With the completion of this financing, Cerro de Pasco is in a stronger financial position to advance the Quiulacocha Project through the full feasibility stage and toward pre-construction readiness."

Price Forecasts & Risk Considerations

Analyst projections for silver vary but trend decisively bullish. Bank of America raised its 12-month silver target to $65 per ounce, while analyst targets range between $33 and $65 per ounce, concentrating around mid-$40s under base-case assumptions. Speaking at the Metals Investor Forum, editor of Silver Stock Investor Peter Krauth noted that $95 isn't out of the question for silver over the next 12 to 24 months.

Silver's notorious volatility represents the primary risk. Macroeconomic reversal through rising real interest rates or a sustained dollar rally could pressure prices. Industrial demand sensitivity means a severe global recession could delay solar installations and reduce electronics consumption. However, technological substitution risk appears limited, as silver's unique properties make complete replacement difficult in most applications.

The Investment Thesis for Silver

- Allocate 5-10% of precious metals exposure to physical silver or silver ETFs as a hedge against monetary debasement and currency volatility, recognizing silver's low correlation with traditional financial assets and its dual role as both safe-haven and industrial metal.

- Target mid-cap silver producers and advanced-stage developers with low all-in sustaining costs (sub-$15/oz), strong balance sheets, and assets in stable jurisdictions; companies like Americas Gold & Silver, Vizsla Silver, and GR Silver Mining offer amplified returns when silver prices rise while providing exploration upside.

- Use dollar-cost averaging during price pullbacks toward the $40-45/oz support zone rather than chasing momentum; silver's volatility creates favorable accumulation opportunities during 5-10% corrections, and the current gold-silver ratio above 75:1 suggests undervaluation relative to gold.

- Track quarterly Silver Institute reports, photovoltaic deployment statistics, and COMEX inventory levels; sustained deficits exceeding 100 million ounces annually combined with declining exchange stocks represent key bullish signals warranting increased allocation.

- Set targets to reduce 25-33% of silver equity positions if prices reach $70-80/oz or if the gold-silver ratio compresses below 60:1, while maintaining core physical holdings; silver's historic tendency toward volatile boom-bust cycles argues for systematic profit-taking during parabolic moves rather than rigid buy-and-hold approaches.

- Combine physical metal holdings (40%), silver ETFs (30%), and mining equities (30%) to balance liquidity, storage considerations, and return potential; within equities, mix near-term producers with exploration-stage companies advancing high-grade discoveries for different risk-return profiles.

Silver stands at an inflection point. The convergence of structural supply deficits, accelerating industrial demand, and a supportive macroeconomic environment has created conditions that many believe could drive prices substantially higher. The metal's dual identity positions it uniquely for an era defined by technological transformation and monetary uncertainty.

For portfolio construction, silver warrants consideration as both a tactical opportunity and a strategic holding. Its performance correlation with other assets remains low, providing genuine diversification benefits. Its leverage to both industrial growth and monetary debasement offers a hedge against multiple scenarios. And its current valuation relative to gold suggests meaningful catch-up potential.

The bull case for silver is rooted in verifiable fundamentals: five consecutive years of deficits, record industrial consumption, constrained supply, and a macroeconomic environment that historically favors monetary metals. For investors seeking exposure to one of 2025's most compelling structural themes, silver deserves serious consideration.

TL;DR

Silver has surged 77% in 2025, reaching a record $54.47 per ounce, driven by the fifth consecutive year of supply deficits totaling 820 million ounces, an entire year of global production. Industrial demand hit record levels at 680.5 million ounces, led by photovoltaics and electronics, while mine output peaked in 2016 and has declined 1.4% annually since. The gold-silver ratio at 79:1 versus the 69:1 historical average suggests silver remains undervalued. Analysts project $65-95 per ounce over 12-24 months, supported by structural scarcity, clean energy growth, and monetary uncertainty. Companies like Americas Gold & Silver, Vizsla Silver, GR Silver Mining, and Cerro de Pasco Resources offer leveraged exposure to this multi-year bull market.

FAQs (AI-Generated)

Silver offers several advantages over gold including an elevated gold-silver ratio of 79:1 versus the historical average of 69:1 suggesting undervaluation, over 60% industrial demand providing a structural consumption floor that gold lacks, smaller market size creating 2-3× amplified gains during precious metals bull markets, and five consecutive years of supply deficits while mine production has declined 7% since 2016.

Silver carries higher volatility than gold with historical price swings of 20-40% during corrections, macroeconomic risks from rising real interest rates or strengthening dollar that pressure precious metals, industrial demand sensitivity where severe recession could delay clean energy projects and reduce electronics consumption, technological substitution risk in photovoltaics though offset by increased deployment volumes, and potential supply response from new mine development though 10-15 year timelines suggest this is longer-term rather than near-term.

The optimal approach depends on objectives and risk tolerance: physical silver provides direct ownership and systemic protection but involves storage costs and wider spreads; silver ETFs offer liquidity and transparent pricing but carry counterparty risk and expense ratios; mining stocks provide 2-5× leveraged returns during bull markets but carry operational, management, and jurisdictional risks; a diversified approach allocating 40% physical, 30% ETFs, and 30% quality mining equities balances these trade-offs.

Bank of America targets $65 per ounce within 12 months while some analysts including Peter Krauth suggest $95 over 12-24 months based on structural deficits and gold-silver ratio reversion, with longer-term projections through 2030 ranging from $80-100 per ounce from mainstream analysts and optimistic forecasts suggesting triple-digit prices if supply constraints persist and industrial demand accelerates, though timing depends on continued deficits, sustained solar demand growth, supportive monetary policy, rising gold prices, and increased investment flows.

These companies offer distinct value propositions: Americas Gold & Silver executes district consolidation with $56 million Crescent acquisition adding 3.8 Moz M&I resources 9 miles from processing infrastructure operating at 25% capacity; Vizsla Silver secured $300 million low-cost financing (5% versus 10%+ traditional) for Panuco Project with $1.1 billion NPV, 86% IRR, and $9.40/oz costs targeting H2 2027 production; GR Silver Mining discovers high-grade extensions at San Marcial with 5.0 meters at 232 g/t silver ahead of H2 2026 resource update and PEA.

Analyst's Notes

Subscribe to Our Channel

Stay Informed