World Bank's Nuclear Financing Pivot Signals a Structural Repricing of Uranium

World Bank lifts nuclear financing ban, creating structural uranium repricing. Supply deficits meet policy support, favoring tier-one jurisdiction miners.

- The World Bank’s reversal of its long-standing ban on nuclear project financing represents a historic policy shift, unlocking multilateral capital for uranium-linked infrastructure.

- This move aligns with G7 energy security goals and comes amid structural underinvestment in uranium supply, creating a rare macro tailwind for the sector.

- Institutional financing could accelerate reactor builds, lifting long-term uranium demand curves despite recent spot price softness.

- Tier-one jurisdiction projects with near-term production capacity, like those operated by Energy Fuels and IsoEnergy, are positioned to capture early capital inflows.

- Exploration-stage assets with scale and grade advantages - such as ATHA Energy’s Angilak and Global Atomic’s Dasa - offer asymmetrical upside as utilities lock in long-term contracts.

Understanding the World Bank's Shift

For decades, multilateral development banks maintained a prohibition on nuclear financing, effectively constraining capital access for uranium-linked infrastructure projects. This policy stance created artificial barriers to nuclear development, particularly in emerging markets where energy security and decarbonization objectives intersect with capital constraints.

The trigger for this historic reversal stems from rising urgency around decarbonization, energy security imperatives, and the strategic need for geopolitical diversification away from Russian nuclear fuel supply chains. The policy scope now encompasses eligibility criteria for reactor projects, enrichment facilities, and broader fuel cycle infrastructure, fundamentally altering the risk-return profile for uranium sector investments.

The magnitude of this shift becomes clear when analyzing capital costs per gigawatt of nuclear capacity, which typically range from $6 billion to $10 billion. Multilateral Development Bank participation serves as a cornerstone for blended finance structures, combining project debt with sovereign guarantees to de-risk private investment. This financing architecture has historically proven transformative in hydro and renewable energy sectors, suggesting similar potential for nuclear infrastructure development.

Strategic Implications for the Uranium Market

The correlation between nuclear buildout timelines and uranium demand curves creates a direct transmission mechanism from policy changes to commodity fundamentals. Sovereign and institutional financing fundamentally alters the cost of capital for developers, enabling projects that previously faced prohibitive financing costs to achieve commercial viability.

Historical precedent from hydro and renewable sectors demonstrates how Multilateral Development Bank financing entry catalyzes broader private capital participation. In nuclear energy, this dynamic is particularly pronounced given the sector's high capital intensity and long development timelines, where access to patient, low-cost capital proves decisive for project economics.

The transformation of financing structures creates distinct competitive advantages for Western-aligned producers. Energy Fuels Chief Executive Officer Mark Chalmers notes:

"Sovereign and institutional backing fundamentally alters the competitive landscape for United States and allied uranium producers."

Structural Underinvestment Meets Policy Acceleration

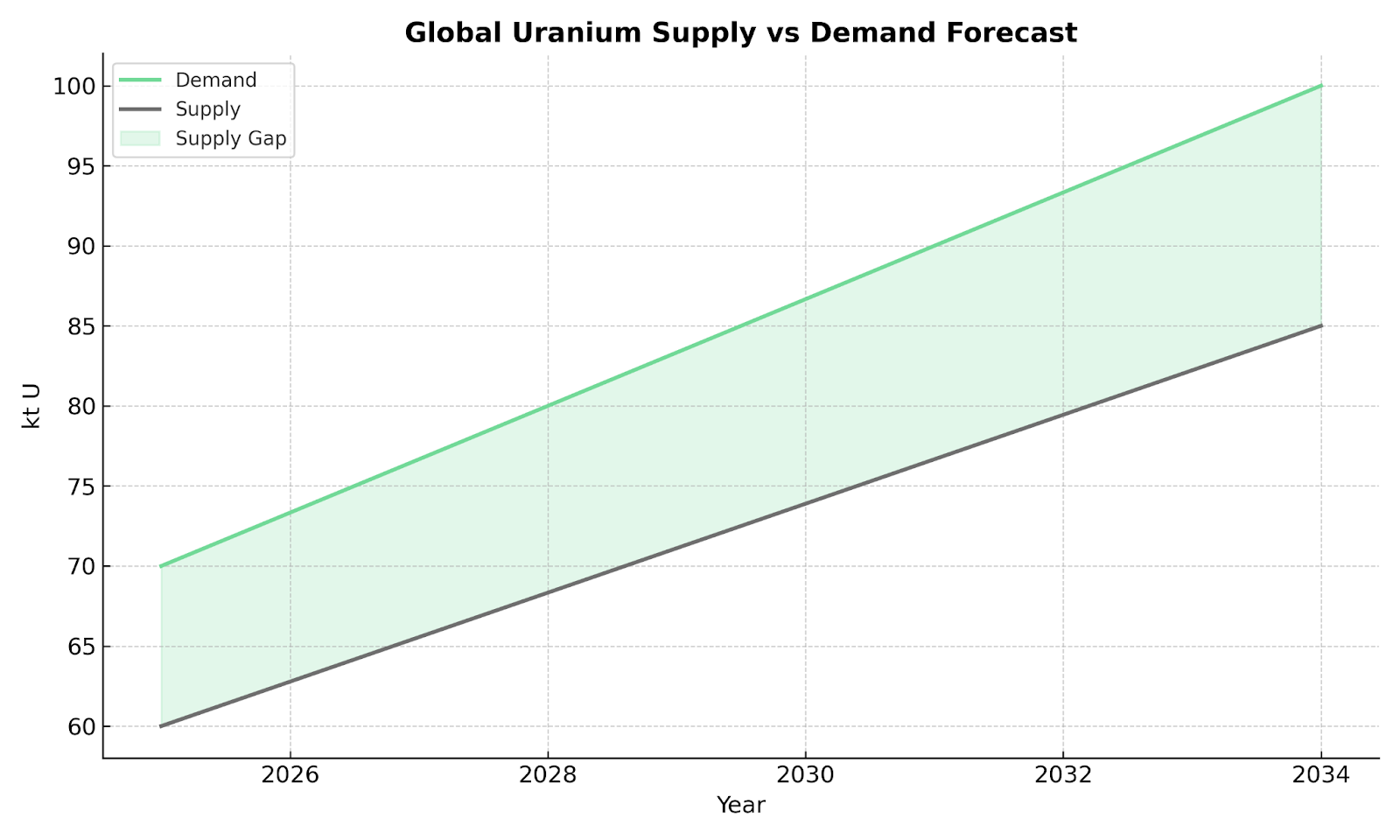

The current uranium market exhibits a significant supply deficit, with mine output failing to meet utility demand according to World Nuclear Association projections. This supply gap reflects years of underinvestment in new capacity, exacerbated by the complex challenge of bringing new supply online amid permitting lead times, capital expenditure inflation, and Environmental, Social, and Governance compliance requirements.

Despite recent softness in spot uranium prices, long-term contract prices have increased by over 23% year-on-year, signaling strong utility interest in securing future supply. This divergence between spot and term markets indicates a widening supply gap expected to persist for years rather than quarters, creating sustained upward pressure on contract pricing.

The structural nature of this underinvestment becomes evident when examining project development timelines. Uranium mining projects typically require 7-10 years from discovery to production, with permitting processes alone consuming 2-4 years in most jurisdictions. Current pipeline constraints ensure that even aggressive policy support cannot immediately address supply deficits.

Currency Volatility, Interest Rates & Capital Allocation

The strong United States dollar and elevated interest rates create a complex operating environment for uranium developers, affecting project financing structures differently across jurisdictions. Companies with Canadian dollar-denominated costs, such as ATHA Energy and IsoEnergy, face favorable exchange rate dynamics for United States dollar-denominated uranium sales.

Conversely, projects in jurisdictions like Niger face foreign exchange exposure challenges, where Global Atomic's Dasa project must navigate currency risk alongside operational execution. This dynamic creates additional layers of risk assessment for institutional capital allocation, favoring projects with natural currency hedges or established risk management frameworks. ATHA Energy Chief Executive Officer Troy Boisjoli reinforces this theme:

"The current macroeconomic environment provides the best conditions we have ever seen for uranium exploration and development."

Supply Chain Realignment & Geopolitical Risk Premiums

The United States ban on Russian uranium imports fundamentally reshapes global uranium supply chains, creating immediate demand for enrichment and conversion capacity outside Russian influence. This policy shift removes approximately 20% of United States uranium supply from Russian sources, requiring utilities to secure alternative supplies at potentially higher costs.

Niger's political instability compounds supply chain vulnerabilities, affecting approximately 5% of global uranium supply and amplifying premiums for secure jurisdictions. Recent political developments in the region highlight the concentration risk inherent in uranium supply chains, where a small number of countries control significant production capacity.

Beneficiaries of the Jurisdictional Premium

The transformation of uranium from a commodity to a strategic asset has created distinct valuation tiers based on jurisdictional risk. Tier-one North American assets command 30-50% higher valuation multiples compared to traditional regions like Niger or Kazakhstan, reflecting geological prospectivity and political stability premiums.

The company's White Mesa Mill represents the only permitted, operational conventional uranium mill in the United States, creating unique strategic value for Western-aligned supply chains. IsoEnergy Chief Executive Officer Philip Williams emphasizes this jurisdictional advantage:

"Being a dual-jurisdiction producer with near-term United States output provides strategic value that utilities increasingly recognize and are willing to pay premiums for."

Capital Formation & Deployment in the New Uranium Cycle

Multilateral Development Bank funding serves as a cornerstone for blended finance structures, combining project debt with sovereign guarantees to achieve investment-grade risk profiles. Access to low-cost institutional capital can shift Net Present Value and Internal Rate of Return thresholds for uranium projects, enabling development of assets previously considered sub-economic.

This financing transformation has potential to accelerate Final Investment Decision timelines for advanced projects like Global Atomic's Dasa development and Energy Fuels' capacity expansions. The availability of patient, low-cost capital particularly benefits capital-intensive projects with long payback periods, characteristics common in uranium mining.

The financing advantage becomes pronounced for companies with proven technical teams and de-risked assets. Projects with measured and indicated resources in established mining jurisdictions can more readily access institutional capital compared to early-stage exploration ventures or assets in frontier regions.

Exploration to Production - Positioning Across the Curve

ATHA Energy's exploration scale in Canada positions the company for multi-decade optionality as uranium demand grows. The company's 3.4 million acre land position across Canada's key uranium jurisdictions provides exposure to discovery potential in tier-one geological settings.

The flagship Angilak project demonstrates this positioning, with the Lac 50 deposit containing 43.3 million pounds of U3O8 at 0.69% grade, representing one of the highest-grade deposits globally outside the Athabasca Basin. Recent exploration unveiled an exploration target range of 60.8 million pounds to 98.2 million pounds U3O8, materially expanding the mineralized footprint.

IsoEnergy's Tony M Mine exemplifies low-capital expenditure restart opportunities delivering near-term pounds into tight markets. The fully permitted, past-producing mine requires minimal reactivation capital while providing immediate production capability, addressing supply shortages with reduced execution risk. Global Atomic Chief Executive Officer Stephen Roman highlights the competitive advantage of advanced development status:

"Being the only greenfield uranium mine currently under development positions us advantageously for favorable financing terms as institutional capital enters the sector."

Timelines, Permitting & Infrastructure Readiness

Permitting timelines vary significantly across jurisdictions, with United States and Canadian regulatory frameworks offering greater predictability compared to frontier regions. The Canadian Nuclear Safety Commission serves as the lifecycle regulator for uranium projects, providing regulatory consistency that facilitates long-term planning and investment.

Infrastructure advantage proves decisive in project economics, with Energy Fuels' White Mesa Mill demonstrating unique processing capabilities through toll milling arrangements. The facility's ability to process uranium, rare earth elements, and vanadium creates operational flexibility while generating additional revenue streams.

Resource categorization plays a crucial role in financing approval, with measured and indicated resources providing greater certainty for project finance structures compared to inferred resources. Companies with advanced resource definitions can more readily access institutional capital and secure offtake agreements with utilities.

Risk Management in a Volatile Market

Hedging strategies for uranium producers and developers have evolved to address price volatility and operational risk. Long-term offtake agreement structures provide price stability while securing project finance requirements, with utilities increasingly willing to sign multi-year contracts to ensure supply security.

Global Atomic has already secured four uranium offtake agreements, three with United States utilities, demonstrating utility commitment to securing future supply from reliable sources. These agreements provide revenue visibility while supporting project financing initiatives.

The risk management framework extends beyond price hedging to encompass jurisdictional, operational, and financing risk. Companies with diversified asset portfolios, strong balance sheets, and experienced management teams demonstrate superior risk-adjusted returns in volatile commodity cycles.

The Investment Thesis for Uranium

The uranium sector presents a compelling investment proposition driven by multiple converging factors. Macro tailwinds emerge from the historic policy shift by the World Bank, aligning with G7 and national energy security agendas while driving institutional capital into nuclear infrastructure. This policy support creates a foundational demand driver that extends beyond traditional commodity cycles.

Structural supply deficits ensure multi-year upward bias for uranium contract pricing, with underinvestment and delayed project pipelines constraining near-term supply response. The magnitude of required new supply necessitates sustained higher pricing to incentivize development of marginally economic projects.

Jurisdictional advantages command supply premiums as utilities diversify away from geopolitically exposed sources. Tier-one jurisdictions like Canada, Australia, and the United States offer regulatory stability and political predictability that justify valuation premiums in an increasingly security-conscious market.

Capital efficiency becomes decisive in volatile markets, with low-capital expenditure restarts like IsoEnergy's Tony M Mine and existing infrastructure like Energy Fuels' White Mesa Mill offering rapid response to demand surges. These assets provide immediate production capability without extended development timelines.

Exploration upside potential remains significant in tier-one jurisdictions, with large-scale, high-grade exploration portfolios like ATHA Energy's Canadian assets and first-mover development projects like Global Atomic's Dasa providing asymmetrical upside potential as uranium demand accelerates.

Uranium's Repricing as a Strategic Asset Class

The World Bank's policy shift signals institutional acceptance of nuclear energy as a critical technology for achieving decarbonization goals while maintaining energy security. This represents the early stages of a capital cycle inflection point—comparable to renewable energy development in the early 2000s—where project readiness and jurisdictional safety will determine market winners.

For institutional investors, the uranium sector presents a unique opportunity to gain exposure to a strategic commodity transitioning from cyclical oversupply to structural deficit. The convergence of policy support, supply constraints, and capital market access creates conditions for sustainable repricing of uranium assets.

Long-term demand fundamentals, coupled with constrained supply and expanded financing options, establish the foundation for strategic repricing of uranium as an asset class. Companies positioned in tier-one jurisdictions with advanced projects, experienced teams, and strong balance sheets are best positioned to capitalize on this transformation.

Analyst's Notes

Subscribe to Our Channel

Stay Informed