Kazakh Supply Surge Tests Uranium's Momentum: Price Dip Masks Structural Bull Market Fundamentals

Uranium dips below $80/lb on Kazakh supply surge, but structural bull market intact. AI demand, nuclear buildouts, and supply deficits support long-term thesis.

- Uranium prices retreated below $80/lb in early November following a one-month high of $82.50, driven by rising Kazakh exports and renewed supply availability.

- A 33% surge in Kazatomprom exports and a 10% increase in output eased supply concerns, temporarily weighing on sentiment despite unchanged long-term demand fundamentals.

- United States deregulation of enrichment and reactor development, artificial intelligence-driven electricity demand, and renewed nuclear buildouts in Kazakhstan, China, and India reinforce uranium's long-term investment case.

- Physical uranium funds such as Sprott Physical Uranium Trust (SPUT) trade at discounts to net asset value (NAV), signaling near-term risk aversion, but producers and developers continue advancing toward growth.

- Examples include Energy Fuels' United States rare earth element (REE) expansion, IsoEnergy's diversified merger and acquisition (M&A) strategy, enCore's in-situ recovery (ISR) production ramp-up, Global Atomic's Dasa development, and ATHA Energy's exploration scale in Canada's basins.

Price Consolidation After Record Gains

The recent 1.84% monthly decline in uranium prices marks the first sustained pullback since Q1 2025. Futures retreated below $80/lb, erasing gains from the October rally when prices reached $82.5/lb, the highest level in a month.

While some traders interpret this as a correction, the macro backdrop remains decisively bullish. Uranium is still 1.18% higher than a year ago, with long-term contracts trading at premiums to spot, a reflection of persistent supply deficits and the structural inflexibility of new mine development.

Short-term softness is largely driven by producer behavior rather than demand erosion. Kazatomprom, the world's largest supplier, reported a 33% increase in exports and a 10% rise in total output in Q3 2025. These figures temporarily alleviated concerns about 2026 supply deficits but may not be sustainable given upcoming tax regime changes and resource-grade declines.

Supply Dynamics: Kazakhstan's Output Growth & Tax Reform

Kazakhstan continues to anchor the global uranium supply chain, producing 39% of global U₃O₈ in 2024. Its short-term production ramp reflects near-term optimization before tax policy changes take effect in 2026.

The government confirmed a new progressive Mineral Extraction Tax (MET) scheduled for implementation from January 1, 2026, that escalates based on uranium prices and production thresholds. The rate will rise by 2.5% if prices exceed $110/lb, increasing total costs for producers operating near the margin. This tax adjustment could cap future output and reinforce cost-curve support at current price levels.

Cost Curve & ISR Dominance

Kazakhstan's cost leadership is rooted in In-Situ Recovery (ISR) operations, representing nearly all production. Average production costs in the country are below $16–24/lb U₃O₈, well under the global incentive price of $70–$80/lb required to trigger new mine developments.

The United States ISR sector offers a strategic counterweight to Kazakh dominance. enCore Energy is ramping production at its Rosita and Alta Mesa Central Processing Plants in Texas, with the Rosita facility holding 800,000 pounds U₃O₈ annual nameplate capacity. The Gas Hills Project demonstrates projected pre-tax internal rates of return (IRR) of 54.8% at $87/lb uranium prices.

William Sheriff, Executive Chairman of enCore Energy, underscores the operational momentum:

"Our production rate on a daily basis has gone depending on what time frame you're measuring it against, from up 200% to up 300% and it's just a matter of urgency is the matter of the day and it's every day for us."

Demand Fundamentals: Decarbonization, Energy Security & AI Growth

The macro demand case remains underpinned by three converging forces: global decarbonization mandates, energy security realignment, and surging electricity intensity from digitalization.

The United States Department of Energy has accelerated support for nuclear power, cutting red tape for uranium conversion and enrichment permits, and supporting small modular reactor (SMR) deployment. Cameco's recent production guidance reduction at its flagship MacArthur asset highlights the supply-side inflexibility that continues to support prices despite short-term volatility.

Philip Williams, Chief Executive Officer of IsoEnergy, contextualized the supply challenge:

"The actual real price of getting that marginal pound of production out of the ground is much higher than anyone thinks."

Electricity demand from artificial intelligence, cloud, and data centers is accelerating nuclear's strategic importance. Microsoft's power purchase agreement with Constellation Energy for the Three Mile Island Unit 1 restart marks a structural inflection point, shifting uranium from a cyclical commodity to a technology-enabling input.

Stephen Roman, President and Chief Executive Officer of Global Atomic, emphasized the uranium landscape transformation:

"This year it seems that people have finally realized nuclear is where it's at. Microsoft is even here. That's big news and I think it's a sign of things to come that tech now is getting involved with nuclear because they know that's the only way to power data centers and their development."

Financial Market Sentiment: Physical Funds & Investor Behavior

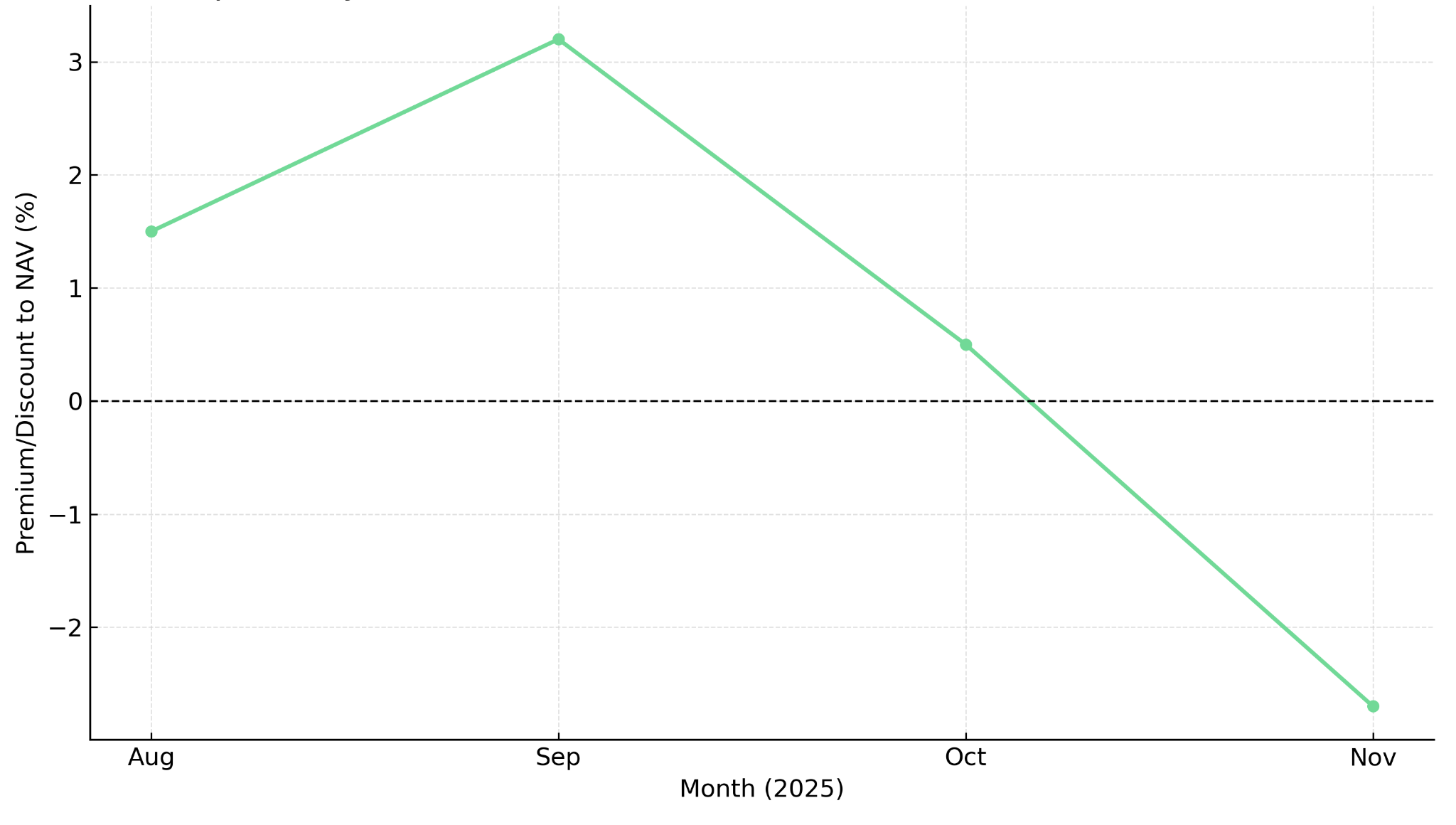

Despite macro optimism, investor sentiment has briefly cooled. The Sprott Physical Uranium Trust (SPUT), the world's largest uranium investment vehicle, held 73.9 million pounds of U₃O₈ as of November 7, 2025, valued at $5.76 billion.

However, SPUT traded at a 2.67% discount to net asset value (NAV), indicating short-term investor hesitation. Historically, SPUT premiums to NAV have coincided with aggressive price rallies. The current discount suggests investors are awaiting clarity on Kazakh production guidance and United States contract volumes before re-entering.

This divergence between physical market fundamentals and financial market behavior is often a key contrarian signal for institutional investors. The discount reflects a broader pattern: retail and momentum-driven capital exits during consolidation periods, while strategic buyers use these windows to accumulate physical exposure ahead of the next supply shock.

Strategic Positioning Across the Uranium Value Chain

The current market environment rewards companies with operational flexibility, jurisdictional safety, and diversified exposure across exploration, development, and production.

Exploration Leverage in Tier-1 Jurisdictions

ATHA Energy represents the high-torque exploration end of the uranium spectrum. With 3.8 million acres in the Athabasca Basin plus holdings in the Thelon Basin and Central Mineral Belt, ATHA controls Canada's largest uranium exploration land position. Its 10% carried interest on key parts of NexGen and IsoEnergy land in the Athabasca Basin allows exposure to high-grade discoveries without operational risk.

Troy Boisjoli, leadership at ATHA Energy, framed uranium’s structural opportunity:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career. The real demand that's being built up coupled with some of the supply side risk is a setup, a structural setup like we have not seen in the uranium space."

The company's 2024 exploration work at Angikuni Basin and success at the Mineralized RIB Corridor align with investor appetite for pre-development catalysts.

Development Momentum in High-Grade Assets

Global Atomic's Dasa Project exemplifies development-stage leverage. The Feasibility Study (2024) showed an after-tax net present value at 8% discount rate (NPV₈%) of $917 million and IRR of 57% at $75/lb, rising to $1.62 billion and 92.9% at $105/lb. The project operates in Niger, where elevated jurisdictional considerations following the 2023 military transition require careful monitoring. The company's 49% stake in Befesa Silvermet, Turkey provides financial diversification and near-term cash flow independent of mining operations.

Integrated Critical Minerals Strategy

Energy Fuels has diversified beyond uranium into rare earth elements (REE), leveraging the White Mesa Mill, currently the only United States facility with commercial capacity to process monazite sands for the full rare earth element suite, including heavy rare earths.

Mark Chalmers, Chief Executive Officer, articulated the company's differentiated positioning:

"Energy Fuels is a company that is unique from all others that you'd look at because we are focused on building a critical mineral hub that is built around our uranium business but also includes the rare earth suite of elements including the neodymium and the praseodymium and the dysprosium and the terbium and potentially samarium and also the heavy mineral sands."

The Phase 2 REE Expansion Feasibility Study for White Mesa Mill is expected in November 2025, and the Donald Project final investment decision (FID) is anticipated as early as Q1 2026. Energy Fuels' infrastructure advantage creates barriers to entry that few competitors can replicate.

Financial strength underpins the company's execution capacity. The recent convertible note offering was oversubscribed by more than 7x and raised $700 million, demonstrating robust institutional demand.

Diversified Growth Platform with Near-Term Optionality

IsoEnergy merges high-grade exploration, M&A growth, and near-term restart potential. Its Hurricane Deposit (48.6 million pounds at 34.5% U₃O₈ in the Indicated category) represents one of the world's highest-grade undeveloped uranium resources, while the acquisition of Toro Energy, expected to close in the first half of 2026, will add 78.1 million pounds of Measured and Indicated resources in Australia.

With $72.2 million in cash and equivalents as of September 30, 2025 ($76.4 million pro forma including Toro), and institutional backing from NexGen (30.1% pro forma ownership), Energy Fuels (3.9%), and Sprott ETFs (URNM/URNJ 9.2%, URA/URNU 3.9%), IsoEnergy's exposure spans the full uranium cycle. Its Utah mines are permitted past-producing properties positioned in trucking distance to Energy Fuels' White Mesa Mill with toll milling agreements established.

IsoEnergy's exposure to the Athabasca Basin offers particular strategic value. Cigar Lake is expected to produce ~18m lbs per annum by 2034 dropping to ~7m in 2035 and ~1m in 2036. The absence of obvious replacement projects amplifies the strategic importance of undeveloped high-grade resources.

"Time is our friend because the crunch in the basin is coming… Every day that goes by we think it increases in value both because the urgency for it to come online will only increase but also we're obviously bullish on the market and when the market increases inherently, the inherent value of it will also increase."

The Investment Thesis for Uranium

Investors should maintain exposure despite short-term volatility for the following strategic reasons:

- Structural supply deficit persists as decades of underinvestment in new mine capacity and enrichment infrastructure mean demand growth will continue to outpace supply through 2030, with no near-term relief from conventional project development timelines.

- Policy-driven demand growth accelerates across decarbonization mandates, with United States and allied governments reinforcing nuclear as the cornerstone of low-carbon baseload generation and energy security frameworks independent of geopolitical adversaries.

- Diversified corporate positioning offers differentiated risk-return profiles, with producers like enCore providing operational leverage, developers like Global Atomic delivering project-scale optionality with near-term production timelines, and explorers like ATHA capturing discovery torque in tier-1 jurisdictions.

- Financial market disconnect creates contrarian opportunity, as the Sprott Physical Uranium Trust discount to net asset value highlights short-term sentiment weakness that has historically preceded market re-entry by strategic buyers when utilities return to spot markets.

- Jurisdictional diversification favors North American and allied-nation producers positioned to capture capital flows shifting away from Russian and Kazakh-linked supply chains, particularly as geopolitical risk premiums become embedded in long-term contract pricing.

- Technology sector convergence transforms uranium's strategic importance beyond traditional baseload generation cycles, as artificial intelligence and data center electricity demand creates sustained load growth less sensitive to economic cycles than discretionary industrial consumption.

Volatility Masks Structural Strength

Uranium's brief retreat below $80/lb underscores the market's sensitivity to marginal supply data, yet the underlying fundamentals remain intact. From Kazakhstan's evolving tax regime scheduled for 2026 implementation to United States policy incentives, the macro environment is recalibrating to ensure future supply security.

Investors should view current weakness as an opportunity for portfolio positioning, not an exit signal. As governments double down on nuclear energy, and as power demand from artificial intelligence and data infrastructure accelerates, uranium's dual role as an energy and technology metal solidifies.

TL;DR

Uranium prices retreated below $80/lb in early November following increased Kazakh exports, but this short-term pullback masks robust long-term fundamentals. Kazakhstan's 33% export surge temporarily eased supply concerns, yet upcoming 2026 tax reforms and persistent supply deficits support the structural bull case. Demand drivers remain powerful: U.S. deregulation of nuclear development, AI-driven electricity needs, and global decarbonization mandates are accelerating nuclear adoption. Major tech companies like Microsoft are securing nuclear power for data centers, signaling uranium's evolution from cyclical commodity to technology-enabling resource. Companies across the value chain—from explorers like ATHA Energy to producers like enCore Energy and developers like Global Atomic—are advancing projects in tier-1 jurisdictions. The Sprott Physical Uranium Trust's discount to NAV suggests contrarian opportunity as strategic buyers position ahead of the next supply shock.

FAQs (AI-Generated)

The price decline was primarily driven by Kazakhstan's 33% increase in exports and 10% rise in output during Q3 2025, which temporarily alleviated near-term supply concerns. However, this production surge may not be sustainable given upcoming tax regime changes in 2026 and resource-grade declines.

AI and data center electricity demand is transforming uranium into a technology-enabling resource. Major tech companies like Microsoft are securing nuclear power agreements (such as the Three Mile Island restart) to power data centers, creating sustained electricity load growth less sensitive to economic cycles than traditional industrial demand.

The uranium sector offers diversified opportunities: explorers like ATHA Energy (largest Canadian land position), producers like enCore Energy (ramping U.S. ISR production), developers like Global Atomic (Dasa Project in Niger), and integrated players like Energy Fuels (uranium plus rare earth elements). IsoEnergy combines high-grade exploration with M&A growth strategy.

Kazakhstan will implement a progressive Mineral Extraction Tax starting January 1, 2026, that escalates by 2.5% when uranium prices exceed $110/lb. This could cap future output and reinforce cost-curve support, potentially limiting the supply surge that pressured prices in late 2025.

Many analysts view current weakness as a contrarian opportunity. The Sprott Physical Uranium Trust trading at a 2.67% discount to NAV historically signals periods when strategic buyers accumulate before the next rally. Structural supply deficits, policy-driven demand growth, and decades of underinvestment support the long-term bull thesis despite short-term volatility.

Analyst's Notes

Subscribe to Our Channel

Stay Informed