Yamana Gold (YRI, AUY) - $500m Unsecured Notes Strengthens Cash Position

Interview with Peter Marrone, Exec. Chairman of Yamana Gold

We recently had a chance to get an update about Yamana Gold from Peter Marrone, the Executive Chairman and founder of the company. He discussed a number of details regarding their steady investment plan focused on organic growth.

Company Overview

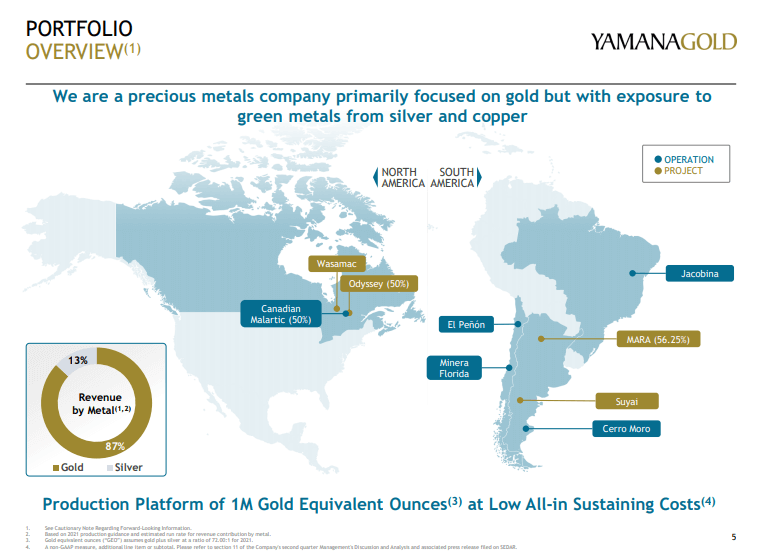

Yamana Gold Inc. is a Canadian company headquartered in Toronto, Ontario. The company owns and operates gold, silver and copper mines in Canada, Chile, Brazil and Argentina. It is listed on three major exchanges: TSE, NYSE, and LSE. Yamana has a market capitalization of $4.06 Bn.

Yamana’s producing mines include Canadian Malartic (Canada), Cerro Moro (Argentina), El Peñón (Chile), Jacobina (Brazil), and Minera Florida (Chile). They are also involved with several advancing projects including the 100%-owned Wasamac Project, Canada.

Management at Yamana

The CEO of Yamana Gold is Daniel Racine. As mentioned, Peter Marrone is the Executive Chairman. The remainder of the management team consists of Jason LeBlanc, Senior Vice President, Finance and CFO; Yohann Bouchard, Senior Vice President and COO; Richard Campbell, Senior Vice President, Human Resources; Gerardo Fernandez, Senior Vice President, Corporate Development; Craig Ford, Senior Vice President, Health, Safety and Sustainable Development; Henry Marsden, Senior Vice President, Exploration; and Sofia Tsakos, Senior Vice President, General Counsel and Corporate Secretary.

Marrone’s Pitch

Over the last 18 years, the company has progressed to a major gold producer from its humble beginnings in Brazil in 2003. Yamana prefers to work in those countries where gold mining is supported by stable jurisdictions. The criteria for county selection are

1. Is the country a good place to be mining?

2. Can the opportunities be de-risked by operating in a rules-based jurisdiction?

Yamana is dedicated to organic growth. Everything that they do, from health, safety, environment, community relations, through exploration, development and operations, is focused on that goal.

Recent Unsecured Note Sale

In a recent bit of news, Yamana announced a 10-year unsecured senior note worth USD $500 M. The company intends to use this money as available cash as well as to purchase back some outstanding bond debt. The company had over USD $700 M of cash of which $480 M is allocated to the general treasury. They looked at the interest rate that they were paying on their debt, which is 4.9%, and realized that this is nowhere near where interest rates are today. They also have a debt payment of $190 M due in 2022, and several more in subsequent years. It simply made sense to do the note deal and essentially halve their interest payments.

Marrone assured investors that this is nothing unusual. Their net debt is at an enviable 0.5 x. They will efficiently lower their gross debt burden even further, so it is a prudent course of action. At the end of these actions, they will still have a cash balance of $250 M in the company treasury. And the interest carried on the restructured debt will be reduced to about USD $20 M per year. The interest savings go directly to the bottom line as an increase in free cash flow. The company now has more flexibility in pursuing their goal of organic growth.

Is the Balance Sheet Clean Enough?

At the moment, Marrone believes that the balance sheet is as clean as possible. As an investment-grade-rated company, it is logical and normal to maintain some debt on the balance sheet. Some may prefer to have a debt-free balance sheet, particularly in the precious metals arena. Marrone thinks differently. They have a completely-unborrowed USD $750M revolving credit facility. They expect to keep it on board in case of a rainy day.

In addition, they have a net debt position in the range of USD $480M-$500M. That net debt will continue to decline because the cash balance will continue to increase as a result of the free cash flow that they generate. What one should be looking at is the risk in maintaining debt, and the risk of maintaining debt when it's too high. The risks occur when the debt is immediately due and when there is an interest component that is a heavy load on the financial strength of the company. For Yamana, the debt is at least 10 years out; their carried interest rate is close to 2.6%. In fact, the interest that they're paying on bonds is amongst the lowest of all of the companies in the gold industry.

The result is that Yamana can now focus on growth and cash returns to investors. Indeed, the company's dividend has just increased. Dividends have now seen a full 500% increase since the beginning of 2019. Additionally, they have introduced a stock-buyback program as well, which provides additional financial flexibility.

Are Investors Buying Into The Yamana Story?

Marrone’s take on the investment climate today is that it is filled with a number of crosscurrents, not all of which are presently in alignment for a rapid move up in the Yamana stock price. Not much new money is coming into specialist funds. Generalist investors are dipping their toe a little into this pool, but are not ready to fully plunge in. There's some ambivalence with what's happening with gold price, but there's also increasingly a resonance that gold price is sustainable at these levels.

When looking historically at the precious metals space, there are times when the physical price led the stock price, and other times when stocks shot ahead of the gold itself. Marrone’s view is that the sector is at an inflection point. There's an increasing recognition that companies in the sector are generating significant cash flows, and can afford to pay and increase dividends.

Now, looking directly at Yamana, the company said that their production would grow from the first half to the second half of 2021. Marrone believes that there is an element in all markets where it's not about what happens in two to three years, but what happens in a month or quarter or so. He believes that many investors are waiting to see that they get through that first half, where there was weaker production by comparison to the upcoming second half.

Yamana’s recently delivered financial results show an increase in cash balances, free cash flow, and dividend, as well as the introduction of a stock buyback program. Yamana’s share price has outperformed that of their peers. Now the company is moving into the second half of the year, with its significantly better production. That will result in a better cash flow. Marrone anticipates a strengthening of their share price in the 3rd and 4th quarters.

Marrone takes a longer-term view as an investor. He’s not disrespectful of people's short-term views. Yamana was a great performing stock last year. The stock has languished for the first couple of quarters this year, but it still is an excellent investment proposition. And if one looks over the longer term, he thinks that Yamana represents a huge value proposition. He believes that the share price will go up.

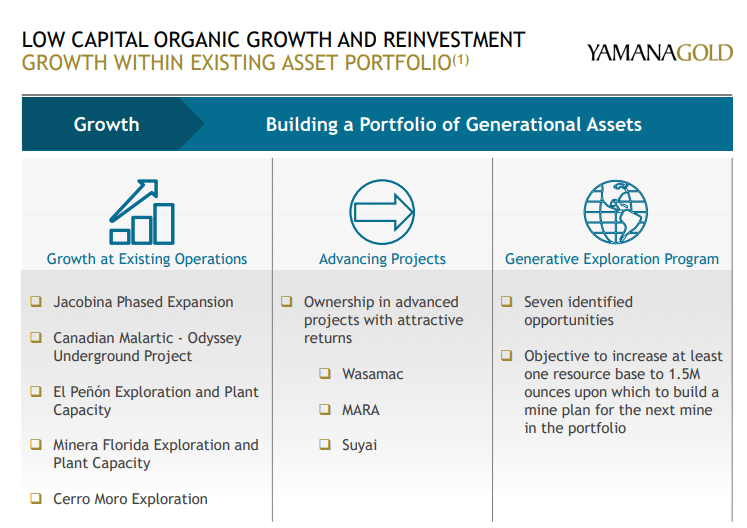

Focus On Organic Growth

With a financial situation that is not overleveraged, the company is now in an enviable position to pursue its organic growth goal. Two projects in particular, Wasamac and Jacobina, were discussed by Marrone.

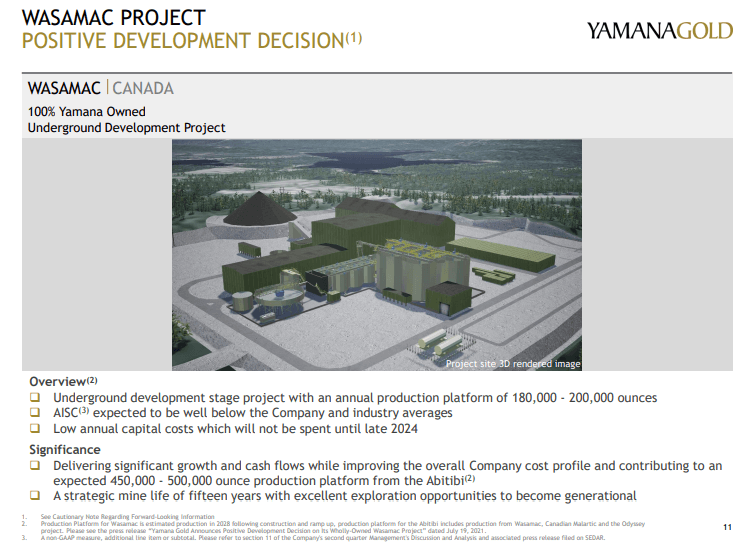

Wasamac: A Value Purchase in Quebec, Canada

Wasamac is an underground gold project located 15 km. west of Rouyn-Noranda in Quebec’s prolific Abitibi region and 100 km. west of Yamana's 50%-owned Canadian Malartic mine. It was purchased by Yamana for USD $114 M earlier in 2021. A good-quality feasibility study had already been completed in 2018. The project has 1.9 M oz. of proven and probable gold. That number will grow as Yamana continues to develop the asset.

Yamana sees Wasamac’s value at about USD $400 to 500 M, based on a 10-year life on proven and probable reserves alone. By increasing the mine life by a mere 5-years, the asset value doubles to closer to $900 M of net asset value. The property will probably produce some 160,000 to 200,000 oz. per year. In the first four years of mine life, the production will be at the high end of that range. Wasamac was bought at an excellent price and has great returns for just about any gold price.

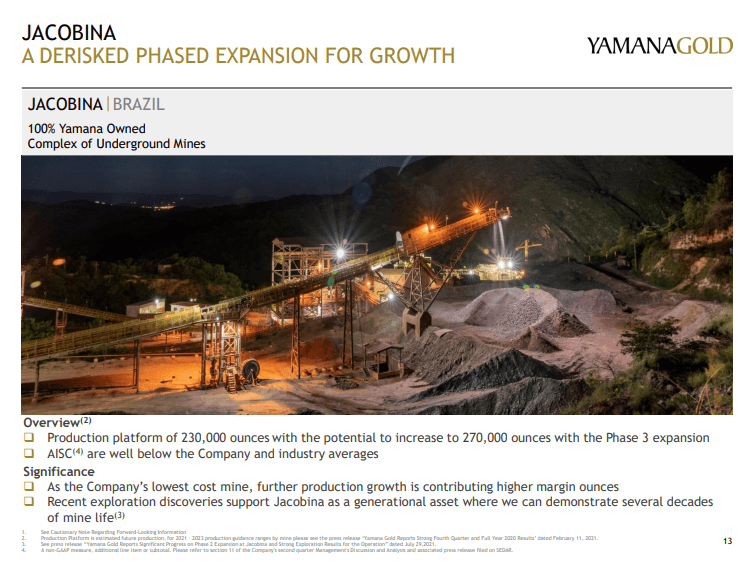

Jacobina: A Suite Of Brazilian Gold Mines

The Jacobina mining complex is located in Bahia state in northeastern Brazil. It consists of five underground gold mines: Canavieiras, João Belo, Morro do Cuscuz, Morro do Vento, and Serra do Córrego. Yamana acquired its 100% interest in Jacobina when it completed the purchase of Desert Sun Mining in 2006.

Yamana has a three-phase expansion underway. At one point Jacobina was producing just shy of 80,000/year. In 2014-2015 the company embarked on a program that had the following components. The first was to understand the geology properly. Jacobina is a reef structure and very different from a lot of the other gold mines in North America. The end game was to get a better and larger inventory of minable gold.

They were actually mining more gold than they could process at Jacobina. So, they created a three-phase optimization plan. The company completed phase 1 early in 2021; now the plant processes 6,500t/ day. This translates to a production increase from 80,000 oz. per year up to year to 170,000 to 180,000 oz. per year.

The second phase is beginning and the announcement will come soon. The cost of this phase is between $15M-$20M for modest modifications to the plant to get production up to 8,500 oz. per day. Plans for the third phase have already been optimized and will deliver even better output numbers. Overall, the company is looking at an operating life of up to 20 years at the higher production levels.

What Type of Investor Should Be Attracted to Yamana

Yamana’s message to existing and potential investors is this: They are a major Gold producer operating in stable, high-quality countries. They have a growth portfolio that has seen an 11 to 12% increase over the last year, and over the next several years increases by another 20-25%. CAPEX is low. Capital obligations are low on a year-to-year basis.

Marrone believes that Yamana should appeal to almost all types of investors, retail or institutional, who are interested in the company’s value proposition and the significant de-risking that they have done with their assets.

To find out more, go to the Yamana Gold Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed