Analyst's Notes: Sabina Gold & Silver

Get industry analysts' take on the latest mining company press releases, and its effect on you - the investor.

Executive Summary

Sabina Gold & Silver Corporation ("Sabina") (TSX:SBB)(OTC:SGSVF) owns the well advanced, high-grade Back River gold project in Nunavut, Canada. The market capitalisation of the Company is C$548 million. Back River is fully funded and it is scheduled to start production in early 2025. Given that the operation will start with a large and high grade open pit, that production is actually quite close, and that there are plenty of opportunities to extend mine-life, The Analysts felt compelled to dig a little deeper on Sabina. Here’s what we found...

While the wider gold market peaked in mid-2020, Sabina held on a bit longer to peak at C$3.29 / share on 27 December 2020. Since then, however, it has all been downhill. Like other gold companies, Sabina is trading at, or close to, 52 week lows, at C$1.00 / share as of 28 September 2022.

Returning to fundamentals, the Back River project comprises two main areas called Goose and George. Mining will start with a high-grade open pit at Goose grading 6.33 g/t Au. Total Proven and Probable Open Pit Reserves contain 1.67 million ounces (“Moz”) at a grade of 5.27 g/t Au. The Goose open pit reserves are supplemented by underground reserves of 1.91 Moz at a grade of 6.76 g/t Au. Looking even further ahead, Goose also boasts Inferred Resources of 2.86 Moz and there are another 1.2 Moz in Indicated Resources in the George mineral tenement block. Back River has a track record of delivering reserves from resources so The Analysts are confident that a high proportion of these resources will eventually be mined.

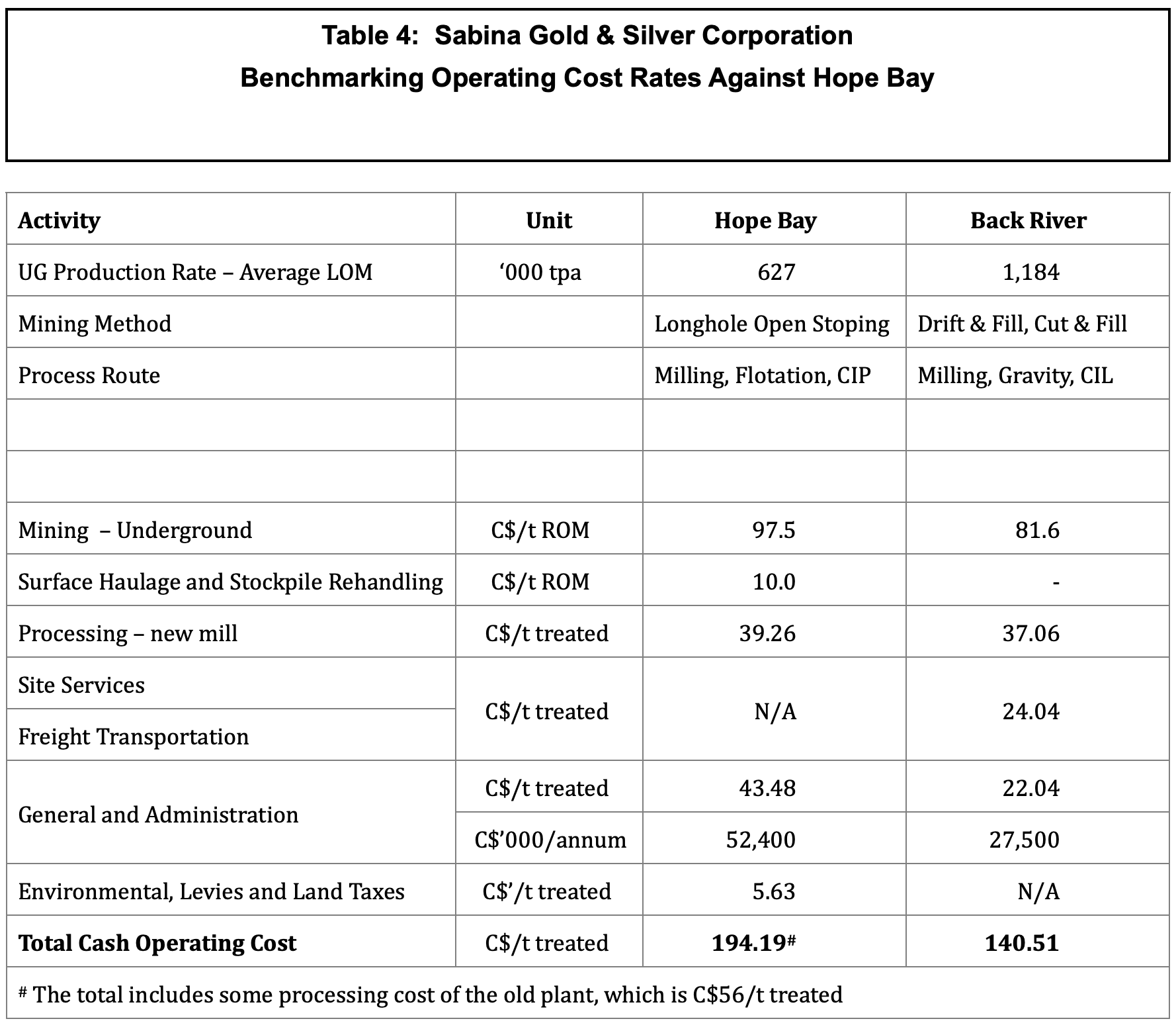

During the analysis of Sabina, The Analysts noted a few minor concerns but no fatal flaws. The main bone of contention was around projected operating costs, particularly underground mining costs. Operating in the Arctic is difficult and expensive. There is no reason why underground mining costs will be lower at Back River than at other mines in the area. The Back River feasibility study assumed an underground mining cost rate of C$82/t. Nearby operation Hope Bay has higher underground mining costs at C$98/t. The Hope Bay mine is also in the arctic and yet it uses a lower cost mining method and, being a larger operation, it has economies of scale. The Analysts have run the numbers using both costs.

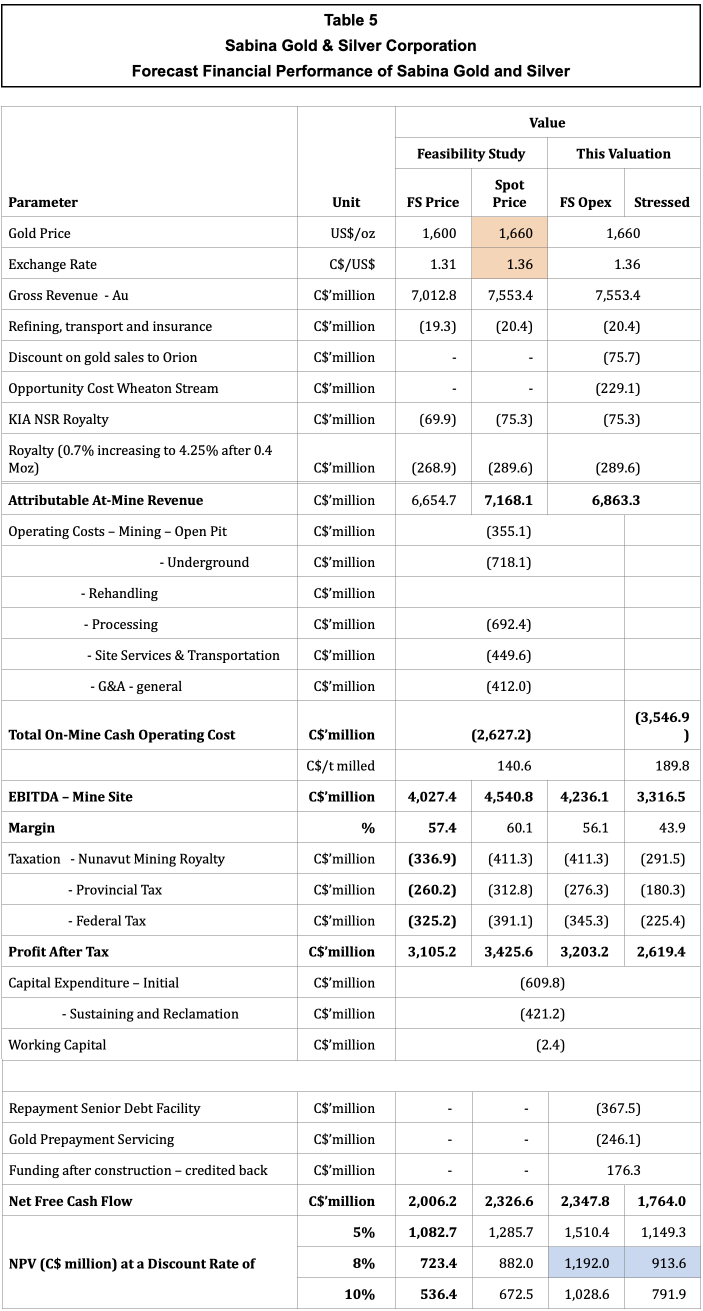

The Analysts have also modelled the project with and without the construction financing package included. Assuming a long-term gold price equal to the spot price of US$1660/oz on 28 September 2022, this valuation comes to a NPV8 of C$882 million for full equity financing. Using the financing package lined up with Wheaton Precious Metals and Orion Mine Finance, The Analysts arrive at valuations of NPV8 C$1,192 million, dropping to C$914 million using 35% higher operating costs.

At the share price of C$1.00 on 28 September 2022 the market capitalisation of Sabina is C$548 million, which is 60% of the calculated NPV8 for the cost-stressed case.

Despite the current mood of the gold market The Analysts feel that Sabina represents asymmetric risk with limited downside and plenty of upside. Sabina is in a similar position to Lundin Gold when it had a share price of C$4.65 in late 2018 with debt finance in place, construction started, and an NPV of US$786 M. Fifteen months later the mine was in production and a share price of C$12.60. The Analysts feel that Sabina Gold could embark on a similar price run as Back River comes into production in early 2025.

Introduction

Sabina Gold & Silver Corporation ("Sabina") (TSX:SBB)(OTC:SGSVF) is a Canadian company that owns the well advanced, high-grade Back River gold project in Nunavut, Canada. Back River is fully financed and currently under construction.

The Back River Gold District is the Company’s main asset with estimated cumulative exploration and evaluation expenditures of C$404 million and property and equipment of C$175 million spent on the Back River Gold District since 2009, including acquisition costs. Sabina also has a residual royalty on the Hackett River deposit but this note will exclusively deal with Back River.

Back River project was acquired in June 2009 and it has been the focus of exploration and studies since then. It is a case study of how long it takes to advance from discovery to production. In March 2011 mineral resources of 1.9 million ounces (“Moz”) had been established, but it took eleven years for mine construction finance to be in place in February 2022.

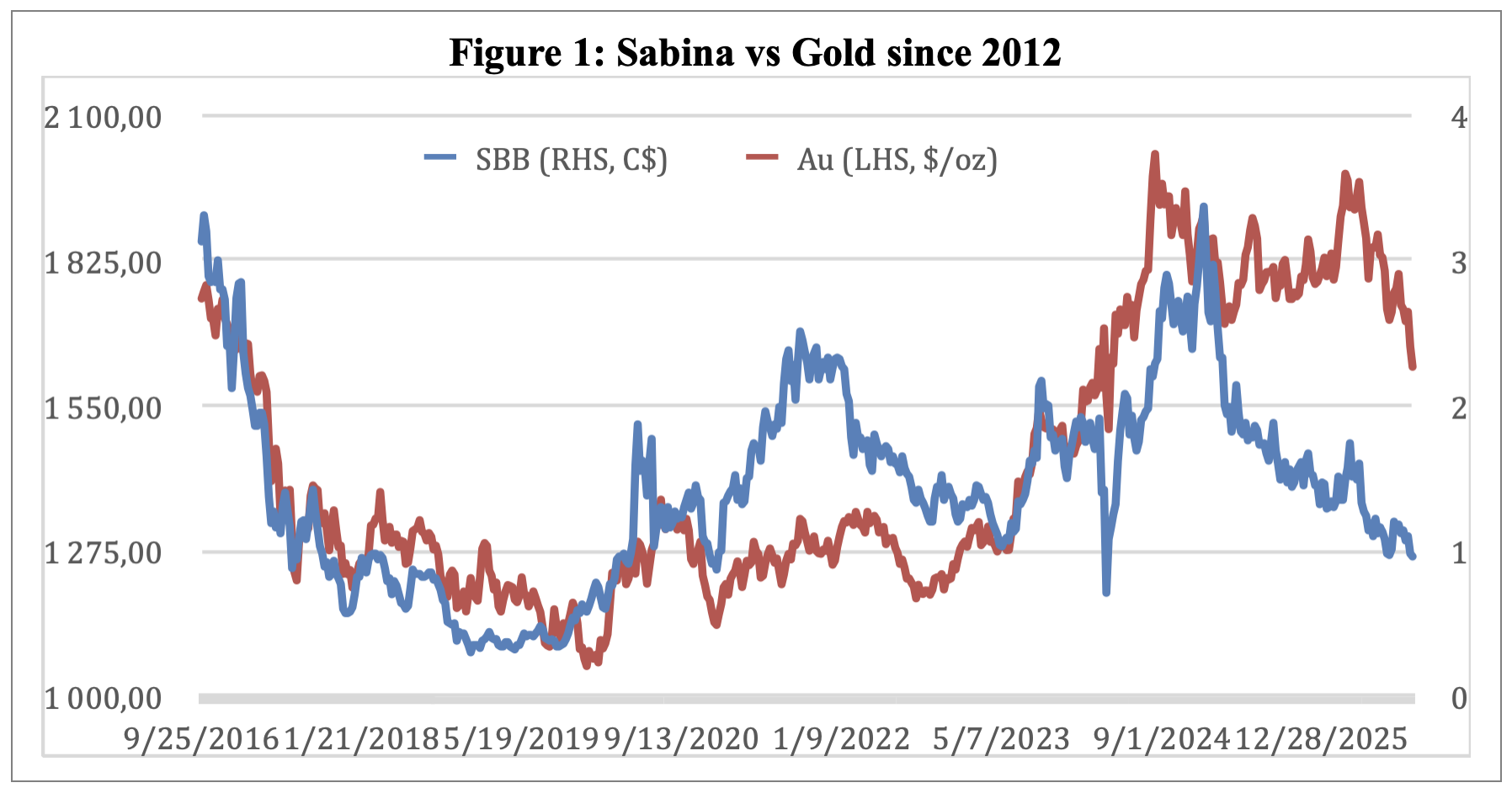

Figure 1 shows the share price performance of Sabina over the last 10 years on the Toronto stock exchange compared to the US dollar gold price performance over the same period.

The chart shows that share price performance was initially closely correlated to the gold price and news flow. From mid-2016 onwards, the shares are still broadly influenced by gold price, but a scan through historic news releases reveals a linkage. The share price typically falls on any news linked to delays in the process, and performs well when new studies and improved resources are announced. From its peak at C$3.29 per share in 2020, Sabina has lost 72% in value as development news has been slow and the wider gold market has been in retreat. It was only announced on 7 September 2022 that a final construction decision had been made.

Since 2009 the company has raised cumulatively almost C$786 million over the years to develop the Back River project, almost all equity financing. This does not reflect the non-equity components of the US$520 million construction finance package agreed to in February 2022.

Technical Background

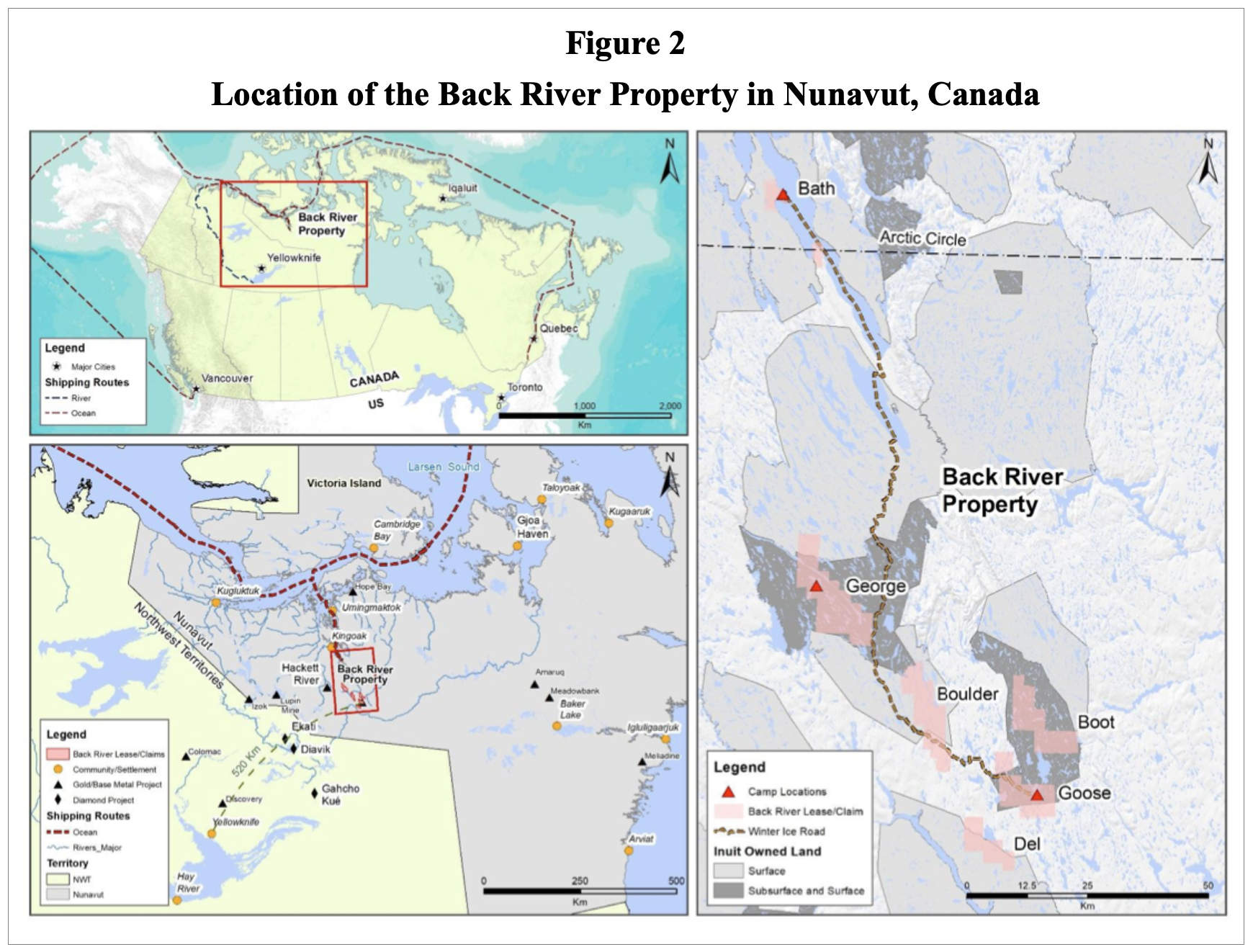

The Back River Gold Project is located in a challenging location in terms of access and climate, the south-western part of Nunavut Territory, 520 km northeast of Yellowknife, see Figure 2).

Goods can only be shipped in during the summer season and construction and mining activities need to work around the short shipping season. Ice roads and short windows for sea access add considerable risk to the project.

Sabina has secured a considerable area of mineral rights covering almost 584 km squared. The project area is divided in three main sites: Goose and George sites with advanced stage prospects and Bath, which is the port location at the Marine Laydown Area (“MLA”). Production of the areas is covered by effectively 4.25% royalties to various parties plus 1% royalty to the Kitikmeot Inuit Association.

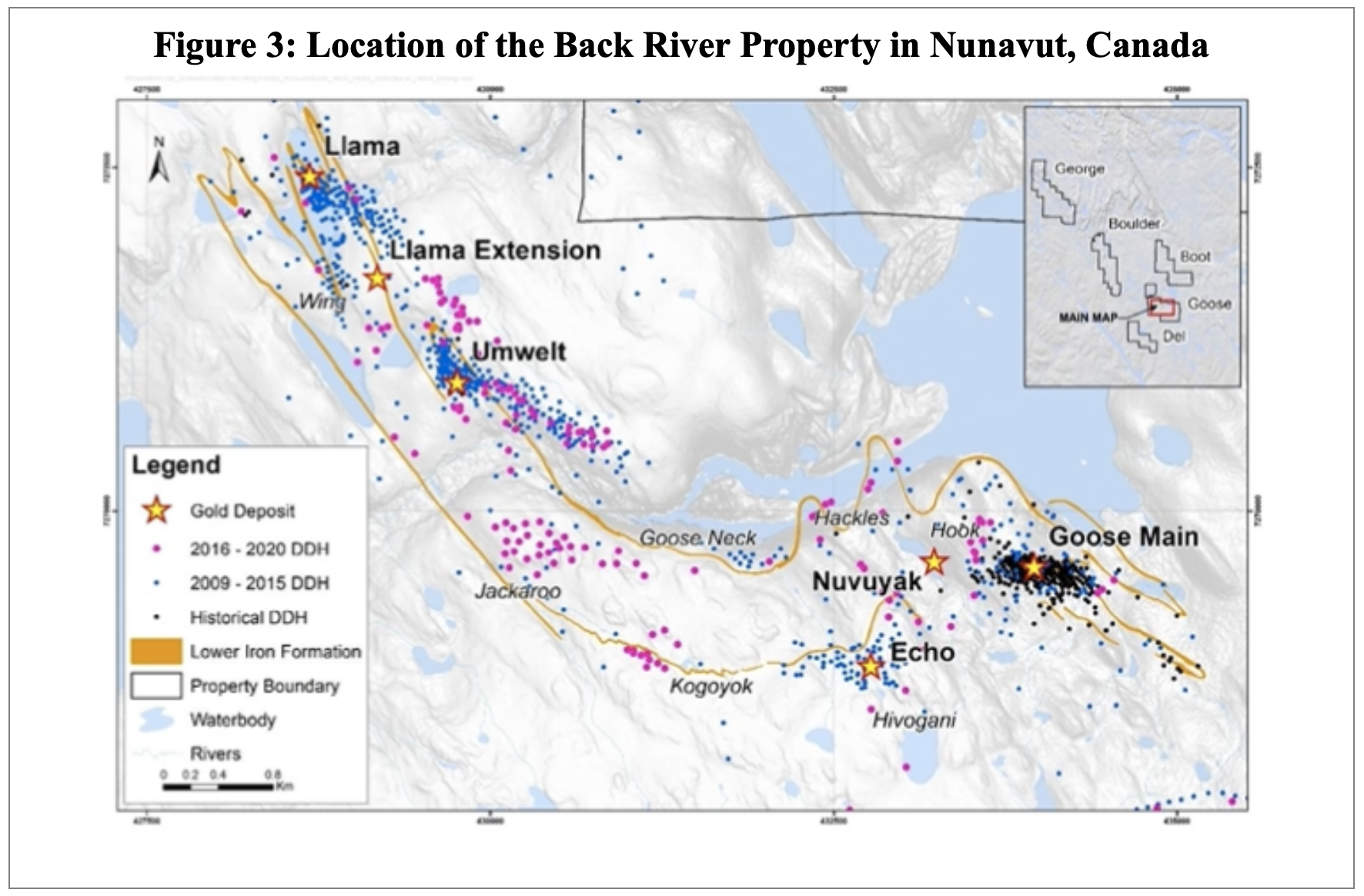

The gold mineralisation is banded iron formations that have been highly folded. In the Goose area the iron formation is thickened 3 to 5 times by folding, with thicknesses in fold hinges greater than 50 m. In the George area the mineralisation is not folded and has a width on average of approximately 4 m. It is probably for this reason that the focus has been on the Goose area deposits and where the mine will be built. The deposits that are part of the production plan are: Goose Main, Llama, Llama Extension, Umwelt and Echo.

Figure 3 shows the drill collar sites and the relative locations of the various prospects in the Goose area.

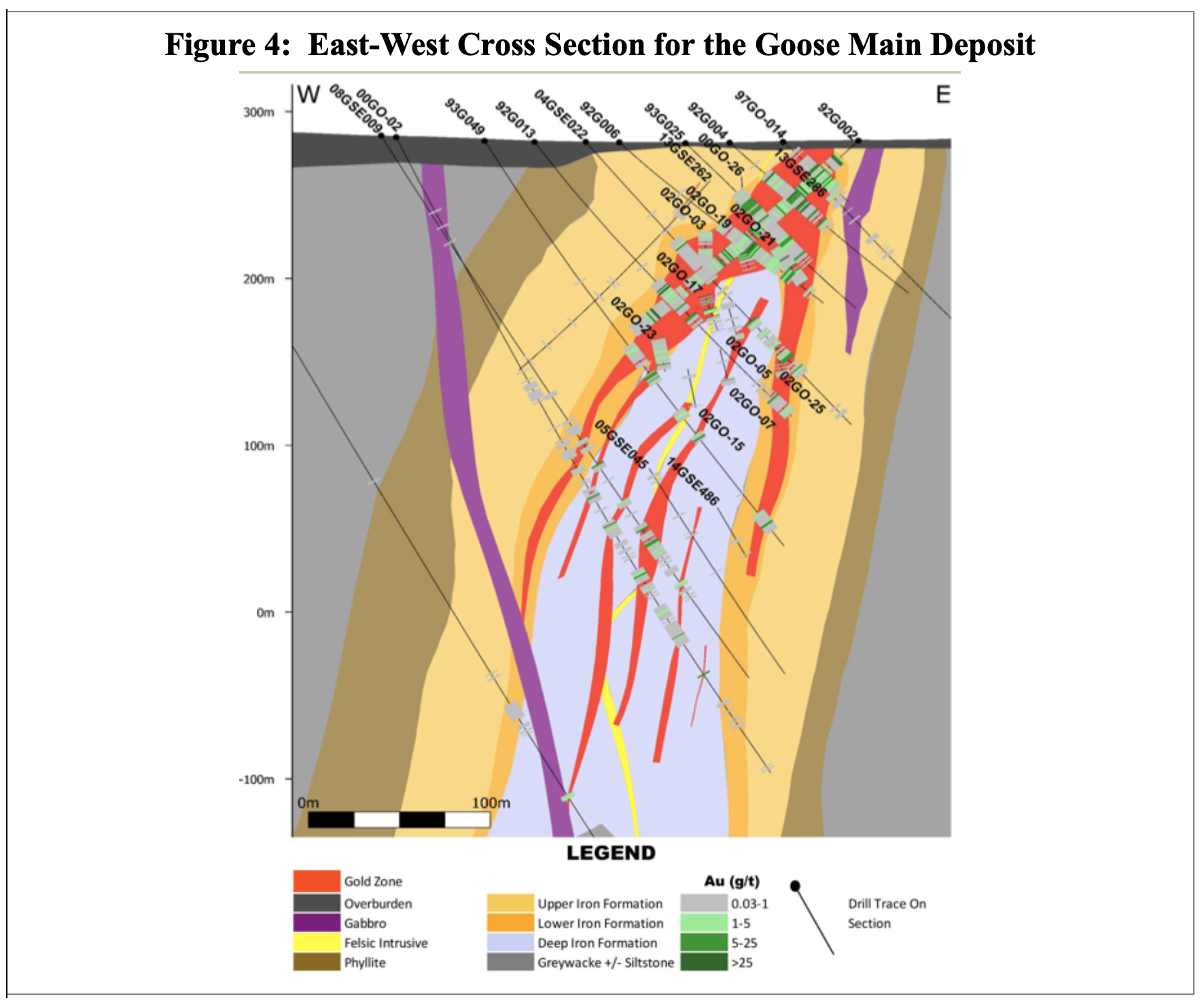

Figure 4 shows a cross section through the Goose Main deposit to illustrate the folded nature of the deposits.

Approximately 60% of the gold mineralisation occurs within the Lower Iron Formation (“LIF”), indicated in brown in the section, and the remaining 40% occurs in the core of the underlying central greywacke. Very minor gold and sulphide mineralisation is developed in the Upper Iron Formation (indicated in light brown). Gold mineralisation is more pronounced and of higher grade in areas of brittle deformation, and of lower grade, or absent, in areas of ductile deformation. Brittle deformation created pathways for mineralising fluids, which introduced quartz, sulphides and gold.

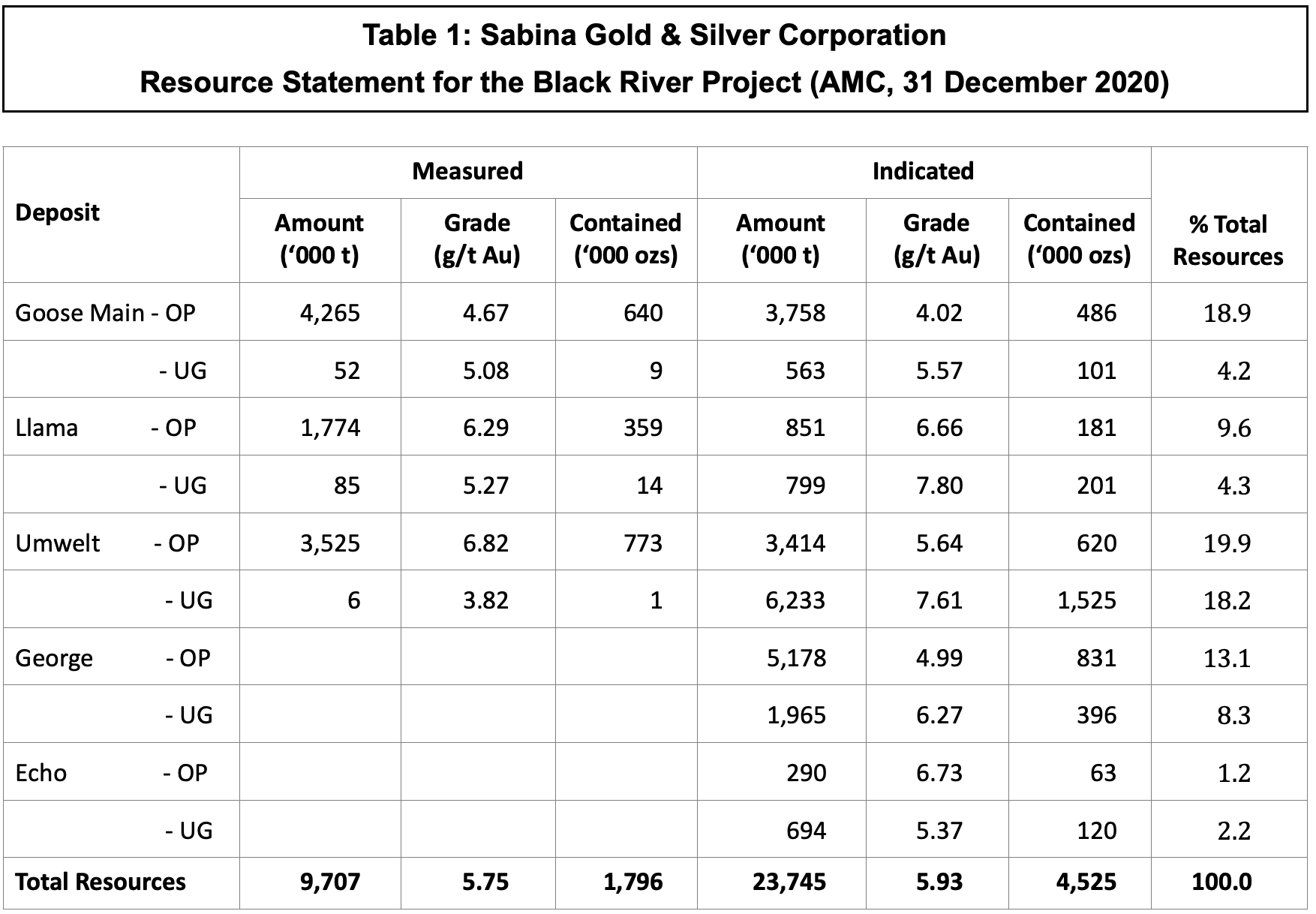

Mineral resources were defined effective 31 December 2020 using a gold price of US$1,500 oz, resulting in a cut-off grade of 0.3 g/t Au for open pit resources and 1.0 g/t Au for underground. Table 1 reproduces the Resource Statement.

From the table it is evident that almost 63% (4.0 Moz) of the 6.3 million ounces gold in Measured and Indicated resources is present as open pittable material. However not shown in the table are another 2.86 million ounces in Inferred resources, which are almost fully accounted for by underground material at Umwelt (0.57 Moz), At Llama Extension (0.42 Moz), George (0.89 Moz) and Nuvuyak (0.58 Moz).

For the mineral reserves the same gold price and roughly the same cost assumptions were used, but now including dilution (between 4.1% and 15%), resulting in cut-off grades varying from approximately 1.5 g/t Au for open pit mining and between 3.5 g/t and 5.0 g/t for underground mining. The Analysts consider the use for a range of cut off grades as unnecessary refinement given that the limits of resources are generally very sharply defined with changes in cut-off grade resulting in only small changes in tonnage, typically changing less than 6% for a 50% change in cut-off grade.

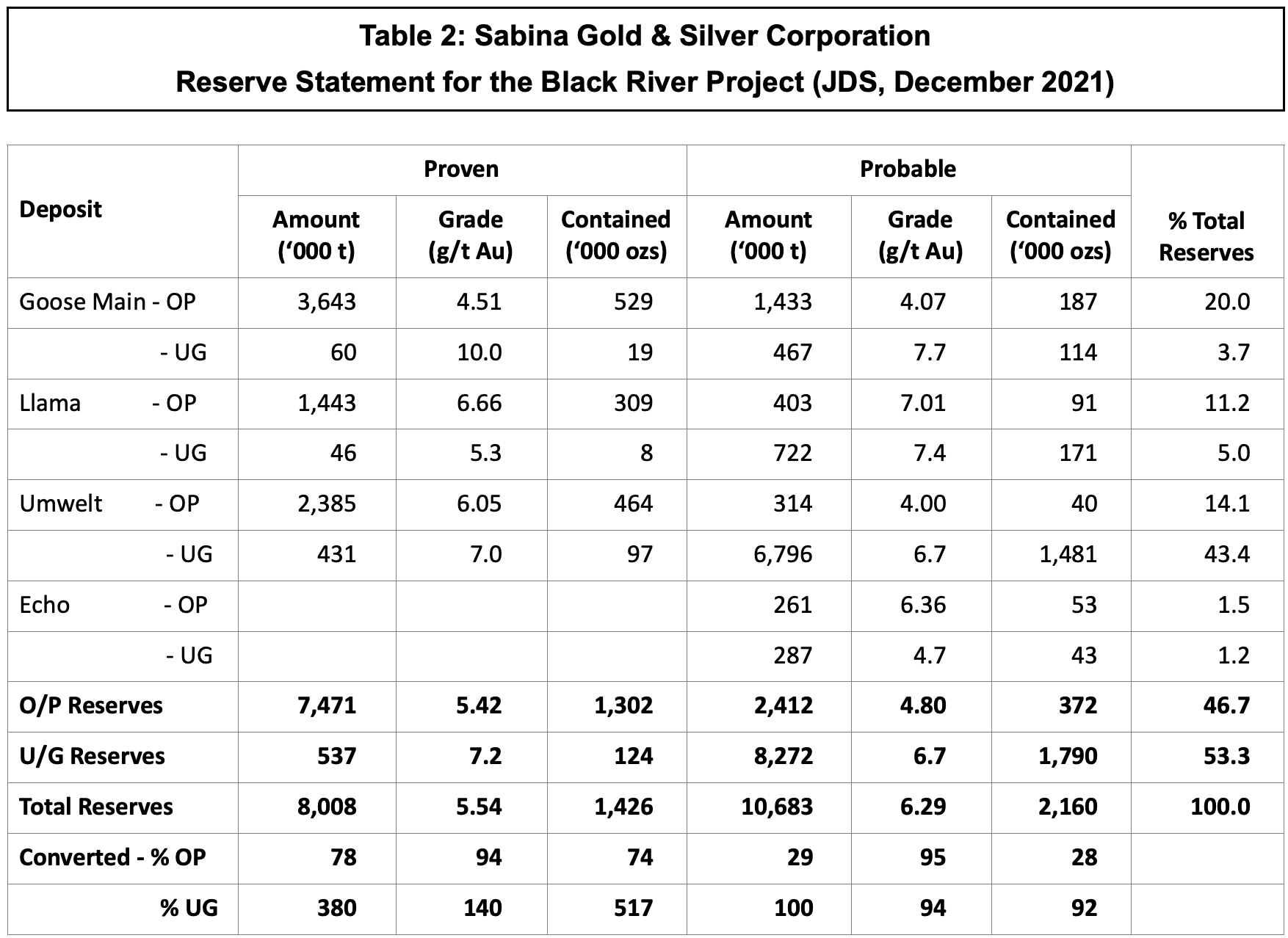

Table 2 gives the December 2021 reserves for the Back River deposits.

The table shows that gold in reserves is almost equally split between open pit and underground material.

The chosen underground mining methods are Drift and Fill (“DF”), Cut and Fill (“CF”) and to a very minor extent longhole open stoping. These are relatively costly methods, but required to cope with the variability of the deposits, rock mechanical conditions and to control dilution.

The mineralisation is very amenable to processing with high recoveries (92%-95%), after gravity concentration and leaching of the gravity tailings once milled to 80% passing 50 μm.

Economic Assessment

The valuation has considered several cases: i) using the input parameters of the feasibility study to check the accuracy of the tax model of the valuation, ii) determining the value of the feasibility study case at the spot price on 28 September 2022, and iii) valuing the company by modelling the secured funding and iv) a cost-stressed case using 35% higher total operating cost.

The details of the funding are:

From Orion Mine Finance (“Orion”):

- A Senior Secured Debt Facility of US$225 million. The interest rate is LIBOR + 5%-8% based on when the drawdown was. As 3-month LIBOR is currently 3% this valuation has assumed an average rate of 10% per annum. The interest is accrued and capitalised until 30 September 2025 after which it is repaid in 20 quarterly instalments until 30 June 2030.

- A US$75 million gold pre-payment facility with delivery commencing on 30 September 2025 for a total of 15 quarters at 7,250 oz per quarter.

- A gold metal offtake agreement which covers all of the refined gold production until 5 million ounces has been delivered, reducing to 20% thereafter. Orion will pay Sabina at the prevailing market prices minus 1%.

- A US$75 million private placement at C$1.30 per share.

Wheaton Precious Metals Corporation (“Wheaton”), which applies to the Goose project area only:

- A US$125 million Stream Agreement in return for 4.15% of gold production until 130,000 ozs have been delivered, dropping to 2.15% thereafter and dropping to 1.5% after delivery of 200,000 ozs. Payment of the gold is at 18% of the prevailing gold price until the US$125 million has been repaid, increasing to 22% thereafter.

- A US$20 million private placement at C$1.30 per share.

As a condition for the Orion facilities Sabina had to arrange additional equity financing of US$105 million, which it satisfied on 30 March 2022.

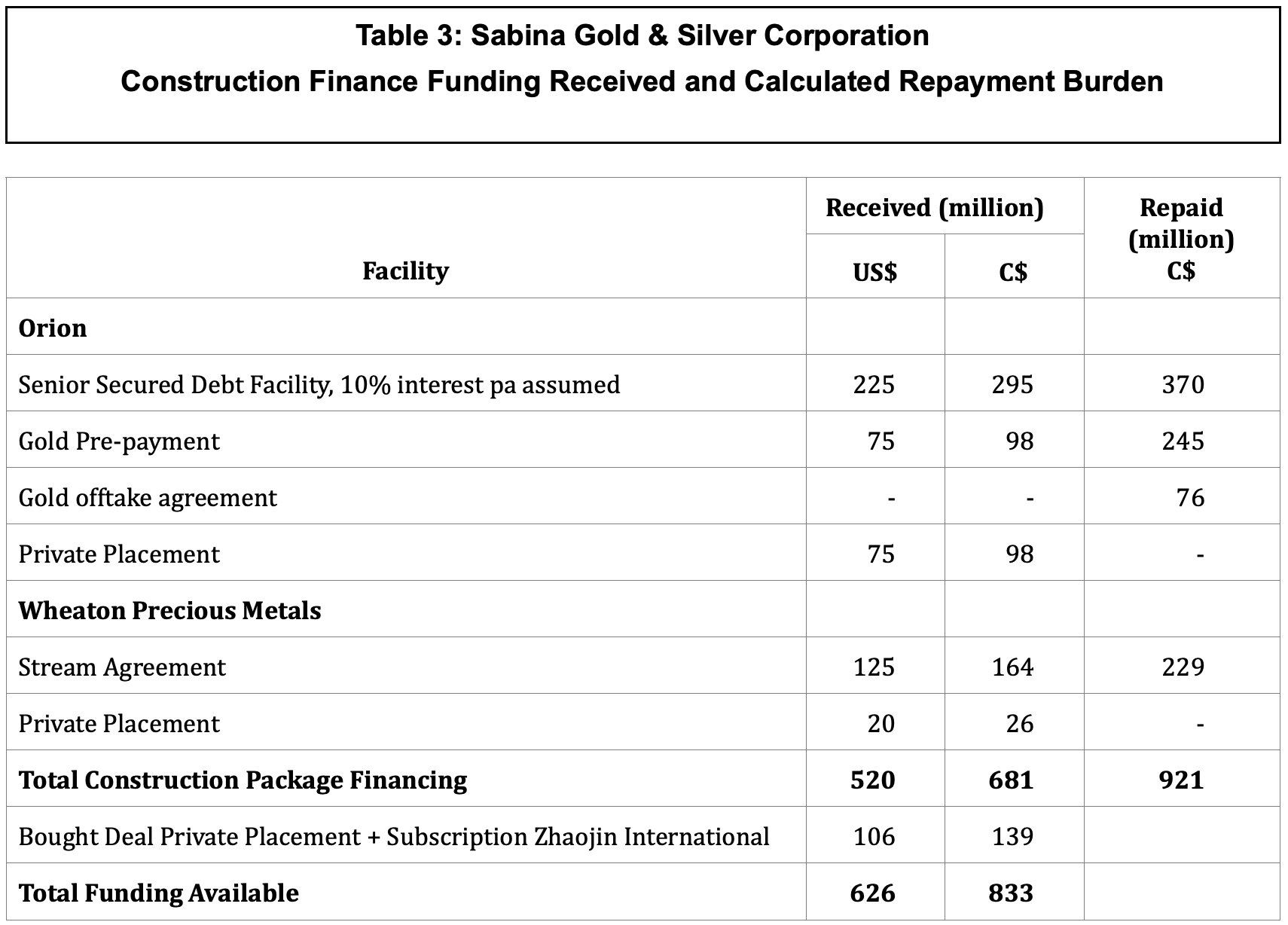

Table 3 shows the total financing arranged in 2022 to fully fund the construction of the mine.

The table shows that the total amount raised is well above the estimated initial construction capital cost of C$610 million, including the contingency provision of C$56 million. It should however be noted that Sabina expects to have to invest in working capital amounting to C$68 million in the year before production start and an additional C$35 million in the first year of production.

The Annual Information Form dated 23 March 2022 suggests first production in the first quarter of 2025. To simplify modelling, this valuation has assumed start of production as per 1 January 2025.

The feasibility study provides for a 2-year pre-production period. Open pit mining activities during this period are scheduled to provide sufficient ore exposure for plant start-up and commissioning. Mining also focuses on providing sufficient waste rock for constructing, for example, site roads and laydown areas. Ore mined during the pre-production period is planned to be stockpiled and re-handled to the mill during operations. Mining in the pre-production period would create substantial high-grade stockpiles to maximise mill head grades in the early part of the production schedule.

The pre-production mining activities are at the Echo open pit to create a void into which the first tailings will be deposited. The Echo pit, and thereafter Umwelt and Llama pits will accommodate all tailings produced. This has major advantages for environmental control and capital expenditure savings on construction of a dedicated tailings facility.

The amount of material processed is projected in the feasibility study to ramp up over two years with 0.94 Mt in year 1, 1.18 Mt in year 2, reaching steady state throughput of 1.46 Mt in year 3. The reason for the ramp-up was that the Echo pit would not have sufficient capacity until the next pit becomes available. However recent detailed geotechnical test work on tailings samples and the inclusion of a high-capacity tailings thickener make such a ramp up unnecessary. This valuation has ignored this improvement, which gives a slight conservative bias to the results.

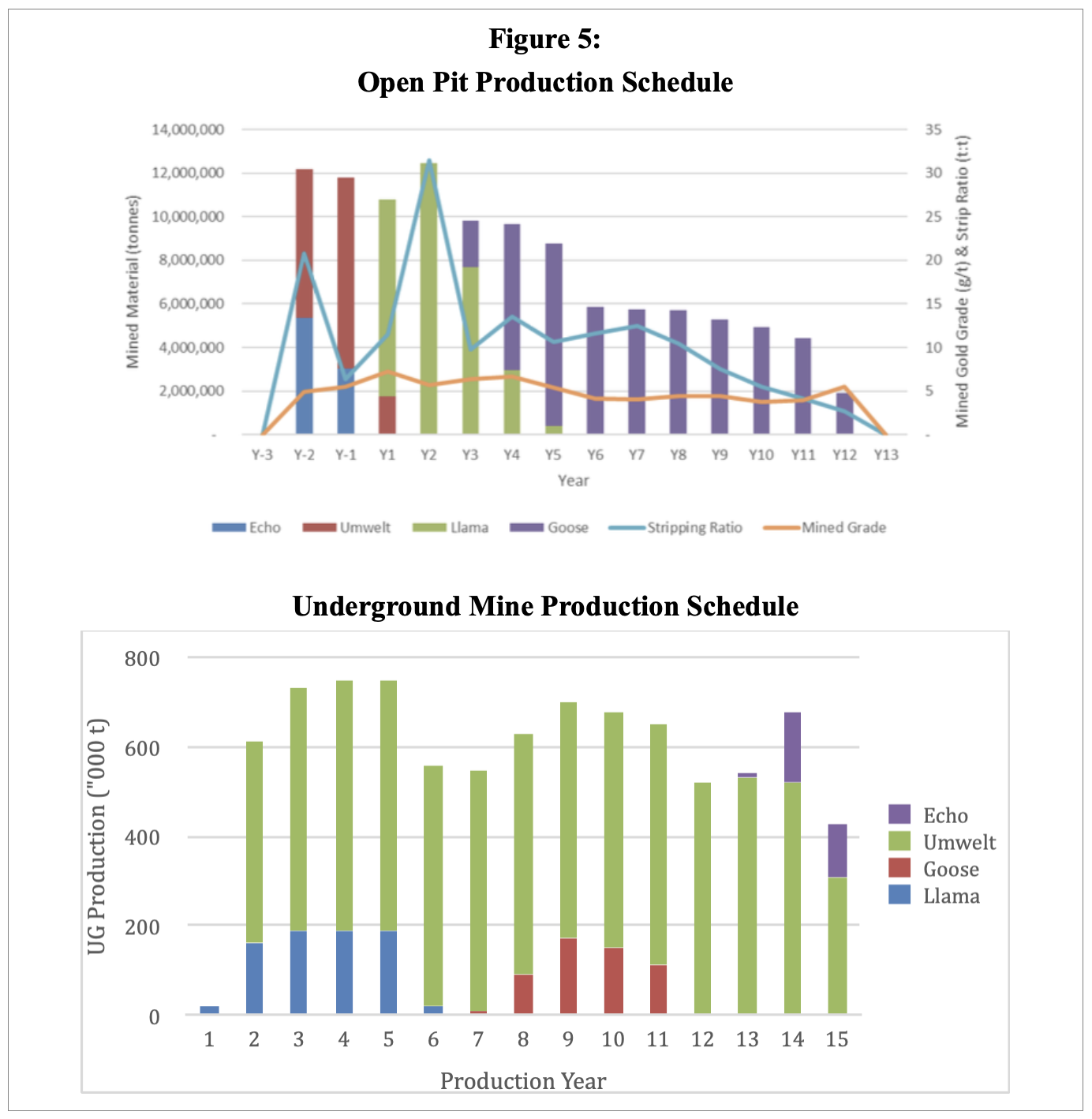

Figure 5 shows the production schedule over time for open pit (top) and underground (bottom) mining by source.

Figure 6 gives the stockpile movement and processing schedule.

The diagram shows that stockpile movement is considerable, amounting to more than 40% of total ore mined. The price to be paid for high grade in the early periods is a considerably investment in working capital and much more complex production requiring strict grade control and good stockpile management.

The capital expenditure to get the mine in production amounts to almost C$610 million with another C$138 million in the two-year ramp-up period. The Analysts are of the opinion that the provisions are realistic, for example C$1,700/t monthly production for the process plant (excluding indirect costs) is a conservative number.

The suggested operating cost rates, however, are low when compared to similar operations in similar climatic conditions, such as the Hope Bay mine. Table 4 benchmarks the feasibility study cost rates with those suggested for Hope Bay.

As Hope Bay has much better economies of scale and will employ mining methods that are cheaper, the overall operating cost of C$81/t for Back River looks unrealistic.

Table 5 summarises the LOM results for four cases: using the input parameters of the feasibility study assuming a gold price of US$1,600/oz, the same but assuming the gold price of US$1,660/oz on 28 September 2022 and the exchange rate of C$/US$1.36 on that date, the case including the funding arranged for construction and this case, but with 35% higher operating cost (“the Stressed Case”).

The total taxes calculated by The Analysts for the case using feasibility study inputs exceeds the amount of the feasibility study by only 2.5%. Arriving at an almost identical tax figure, gives The Analysts comfort that the model is accurate.

Unless cost stressed the project has an indicated margin of more than 56%, which compares very favourably to other mining projects. When using 35% higher operating cost the cash margin drops to 44%, which is still good. This valuation arrives at a Net Present Value at a discount rate of 8% of C$1,192 million, or C$914 million when cost stressed.

This valuation excludes substantial Indicated resources at George (1.2 million ounces) and Inferred resources and Inferred resources of 2.86 million at Goose. This means that in reality the LOM of the Back River project will be substantially longer than the modelled 15 years with treatment of higher grade continuing after year five.

If the average cash flow of year 5 to year 8, when the company is taxed fully and before low grade stockpile processing, is taken as representative, this would add approximately C$110 million per annum to the financial performance for the Stressed Case. Such cash flow in year 10 discounted at 8% would add C$45 million to the overall value.

The main risk is cost underestimation of operating in an Arctic environment, despite having cost-stressed the valuation. Sensitivity analysis, however, shows that the project is very robust with the NPV8 dropping to half the initial capital expenditure, often seen as a minimum go-ahead criterion, should operating cost be another 65% higher at C$313/t milled.

At the share price of C$1.00 on 28 September 2022 and with 548.4 million shares issued the market capitalisation of Sabina is C$548.4 million. This is approximately 60% the calculated NPV8 for the Stressed Case.

Despite the current mood of the gold market The Analysts feels that Sabina represents asymmetric risk with limited downside and plenty of upside. Sabina is in a similar position to Lundin Gold when it had a share price of C$4.65 in late 2018 with debt finance in place, construction started, and an NPV of US$786 M. Fifteen months later the mine was in production and a share price of C$12.60. The Analysts feel that Sabina Gold could embark on a similar price run as Back River comes into production in early 2025.

The Analysts consider Sabina to be a good investment opportunity.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed