Analyst's Notes: Which Popular Mining Investment Criteria is Actually Meaningless?

This week, the Analysts have chosen to focus on All-In Sustaining Costs and the dangers that come with relying too heavily on the data provided by companies.

We are committed to helping investors come to grips with the resources sector and learn how to interpret news releases made by companies. In these Analyst’s Notes we illustrate how news from companies affects the investment case for the stock, and how it can affect peers as well. The topics are selected based on what the analysts think is both relevant and informative to you, the investor.

Before making comments, please ensure you have read the whole article and the FAQs at the bottom.

This week, we have chosen to focus on All-In Sustaining Costs.

Several investment analysts and commentators, writing about investment in gold and silver companies, attach much importance to numbers for Cash Cost per ounce and All-In Sustaining Cost (AISC) per ounce produced. This note, and others, will show you why it is actually meaningless to use AISC as an investment criterion.

We believe that there is a conceptual problem with attempting to use operating and all-in sustaining costs per ounce. In this note we give a background to how the metrics came about, review the serious limitations to AISC, and conclude that investors should rely on the Statement of Cash Flow of audited financial statements to find a realistic sustainable cash cost of production.

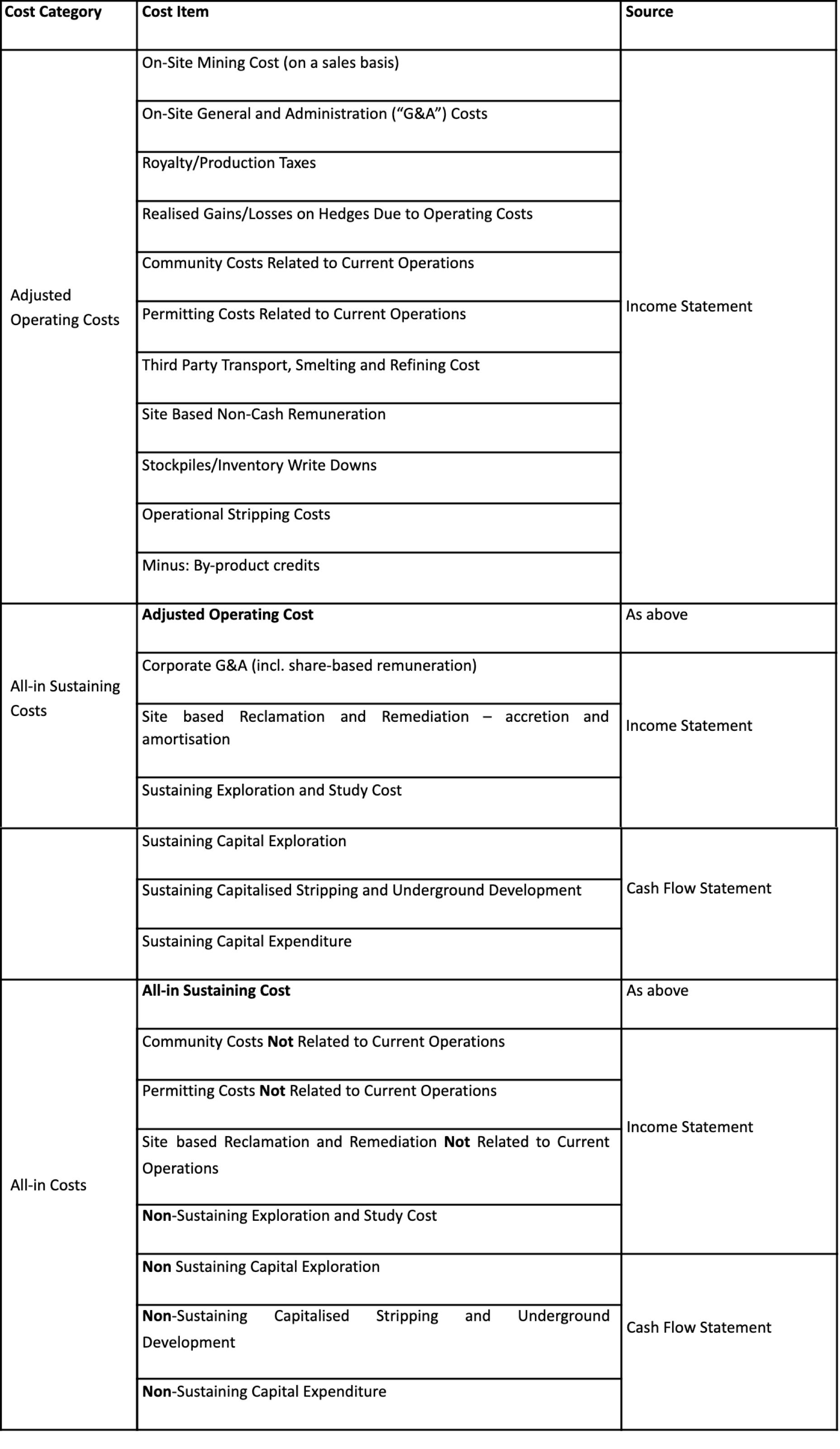

Background

Cash Cost per Ounce

The standard for Cash Operating Cost was proposed in 1996 by the Gold Institute and widely adopted throughout the gold industry, partially because regulatory bodies such as the Toronto Stock Exchange and others recommended its use by listed companies.

Cash Operating Cost per ounce of gold was widely adopted by the industry because it purported to provide transparency to the economics of gold mining operations.

Cash Costs include:

- Mining

- Processing

- Site general and administrative (G&A) costs but ignores corporate G&A expenses

- Interest expenses

- Development cost and taxation.

However, with the definition of Cash cost just being a guideline companies are free to include or exclude what they believe is relevant, such as:

- Royalties

- Smelting/refining charges

- Realised gains on forex and hedging

- Environmental duties

- Inventory adjustments.

Why the Gold Institute found it necessary to create such a flawed measure when the audited financial statements provide all the required information for true cash operating cost is unclear.

Perhaps the idea of having a simple ‘catch-all’ figure was tempting? Whatever the motivation, the move spawned a monster, a shape-shifter that can be configured to tell whatever story a Company wishes to tell. Which is a pity, as the cash flow statement reconciles how the cash balance changes from period to period and never lies. You cannot create or hide cash by re-allocations and book entries.

A cash flow statement has three major components:

- Cash from Operations

- Cash from Investing Activities

- Cash from Financing Activities.

For the purposes of cost analysis the two first components are most relevant. These two sections are clearly defined in terms of accounting standards and practices and cannot be manipulated by the company and signed off by the auditors.

Cash from Operations is the true cash generated by operations during the period after accounting for all expenses incurred during a quarter or a year, including all office costs, interest and taxes. The financial statements give Cash from Operations excluding and including changes in net current assets. As the changes in general are in the long run absorbing cash, because of inflation and losses to consumables and spares through obsolesce and pilferage, we prefer to refer to the inclusive number. The cash cost of operation is simply the difference of revenue minus cash from operations.

Let’s compare in Table 1 the difference between the cash cost established in this manner with some cash cost numbers quoted by four companies for the 2019 financial year.

# after by-product credit equivalent to US$108/oz Au sold for OceanaGold, US$12/oz for Centamin and US$13/oz for Barrick

@ on a co-product basis quoted US$689/oz

The table shows that the actual cash cost of production is generally much higher than the quoted number. Look at the differences between the quoted numbers and the calculated numbers! The average difference is US$343/oz, ranging from Centamin’s US$171/oz discrepancy to Barrick’s US$588/oz difference.

The quoted number is reduced when the company has by-products (definition: accounting for less than 20% of total revenue) or co-products (more than 20%) and their revenue credited against expenses (when by-product), or the expenses are ascribed in relation to the proportional contribution to revenue.

We can learn from this that quoted cash costs often flatter actual cash costs. However, even the auditors cannot prevent manipulation of the cash flow from operations number. It's important to remember that numbers can paint any picture the author chooses, it is incumbent on us to hold companies accountable to paint a more realistic image.

The true cost of sustainable mining is not just the expenses incurred in a year, but also those expenses incurred from which the operation benefits over more than one year. By accounting standards this expense needs to be costed over the years the company is supposed to derive benefit from such an expense, the so-called matching principle. For example, when there is an outlay on waste stripping in excess of the life of mine (“LOM”) strip ratio, companies will capitalise the excess, reducing the cash cost per ounce. The more the company can capitalise, the lower the cash cost per ounce they can quote.

All-inclusive Sustaining Cash Cost per Ounce

In recognition of the shortcomings of Cash Cost per Ounce, the World Gold Council issued a "guidance note" on 27 June 2013 on All-in Sustaining Cost (“AISC”) to incorporate costs relating to sustaining production, such as underground development and stripping costs and replacement of mining and other equipment to maintain production. The guidance note includes a table, reproduced below as Table 2, that went into great detail what to include in the various measures and where in the financial statements these could be found.

The mining industry generally adopted All-in Sustaining Cost, with many starting to include All-in Cost in their statements as from 1 January 2014, as suggested by the World Gold Council. One of the reasons given for adopting AISC is to show governments that mining companies are not as profitable as indicated by cash costs alone, which could ease pressure for higher royalties and taxes and resource nationalisation in general.

So, what is the problem with AISC metrics? Well, it is a superficial measure that does not provide any information an investor cannot get from the financial statements. Worse, it lacks rigour. The definition is so loose that it can be easily manipulated by the companies to present a distorted picture about their true cash generative capacity.

Principally, the adoption of unit cost reporting is totally optional to the companies and also what definition they use. Each company is free to report their costs in the manner they wish. All they need to do is put some sort of vague statement in their reports and caution that their definition may differ from what others use. Therefore, the metric cannot be a proper measure for comparison of the cost performance between companies.

Furthermore, the guidelines still exclude important cash flow items such as:

- Income tax

- Investments in working capital (except for adjustments to inventory on a sales basis)

- All financing charges (including capitalised interest)

- Costs related to business combinations, asset acquisitions and asset disposals

- Re-allocation of Capital Expenditure to reduce Operating Expenditure

In particular income taxes and finance charges are relevant to the shareholder, as they can have consequences for the amount of cash the company generates and will have available to reward shareholders through dividends, or share buy-backs.

Why AISC is Meaningless and Abused by the Mining Industry

To demonstrate that AISC is meaningless as a gauge on how much a company really generates in cash, the performance of five diverse precious metal companies have been reviewed, some with important co-product revenue (e.g. SSR Mining), some purely open pit, others with both open pit and underground operations.

Table 3 summarises the performance over 5 years from 1 January 2015 until 31 December 2019. The starting period is just after 2014 when most companies started to report AISC figures as per World Gold Council suggestion.

The approach to the comparison is to reproduce the cash flow statements of each company, sum the 5-year results and arrive at the amount of cash generated or consumed before financing activities: Cash from Operations after changes in working capital minus Investments over 5 years. This is then compared to the notional amount of cash that should have been generated based on the difference between total revenue and all-inclusive sustaining cost quoted by the companies.

As a bit of a digression, the table also shows that, of the five companies, only one company paid dividends (Centamin = CEE). Investors will be hard pressed to find a precious metal company that pays substantial dividends without returning to the market at regular intervals for equity investments that exceed the total amount of dividends paid. Kudos to Centamin - exceptional work.

# 50% profit share

% reduced by US$132 million in “investments” for marketable and plant disposal

$ includes US$103 million in restricted cash that will be released upon transaction approval

The rows that are highlighted yellow give respectively the net cash generated by the company based on the cash flow statement and based on the balance of revenue minus ASIC cost.

As always when reviewing financial reports, it is never straightforward. Whereas we prefer audited statements to draw conclusions on the true financial performance, the following shortcomings were noted for some of the examples:

- In the case of Centamin (CEE) an adjustment was necessary. The reason is that the company is exempt from income taxes in return as part of its production sharing agreement with the Egyptian government. The government shares 50% of the cash flow after the company had recouped its investments. It is therefore a kind of “income tax” and should therefore be accounted to make comparison with their peers that are subject to income tax, possible. The green highlighted cell shows the total cash disbursed to the government.

- In the case of SSR Mining (SSR) the sale of marketable securities for US$132 million is includes as a credit to “investment” instead of being treated as a financial transaction, thereby understating the true level of investments in mineral assets net of sustaining capital expenditure shown in the blue highlighted cell.

- In the case of Teranga Gold (TGZ) a temporary feature such as an increase of US$103 million in restricted cash as “investments”, which will be released when the transaction gets official approval (see the grey highlighted cell).

The above indicates that any cost analysis will have to review the details of the cash flow statement to determine whether certain items should be added or excluded. It is exactly this kind of level of detail that prompted the World Gold Council to try to come up with a AISC formula. Sorry guys, when it comes to making money through investing in the resources sector, it is never easy. The work needs to be done - either by you, or by trusted neutral analysts with no axe to grind. That’s us, by the way.

What the table does illustrate is the degree by which AISC costs understate the true cash outlays of the company). The difference is partially due to items excluded such as taxes, investments in working capital and financial expenses, but most importantly because of a proportion of capital expenditure classified as for “growth” in production.

Companies love to re-allocate capital expenditure to reduce AISC costs. For example, Argonaut Gold considers “capitalized stripping and leach pad construction as expansionary in nature”. When completing project economic analysis to motivate project go-ahead the cash flow model includes these items as part of the outlays required to achieve a certain life of mine (LOM) production. The waste stripping and leach pad construction over the LOM is there to achieve this planned production and does not contribute to “growth”. Similarly, the capital development in underground mines are part and parcel of achieving LOM production and usually do not give “growth”. Conceptually the definition of AISC cost is incongruous with the original project feasibility assessment.

The observant reader will have noticed that all companies in Table 3 have achieved growth in gold production since 2015. So, the reallocation was therefore at least partially valid? Again, not all is what appears.

For example:

- Centamin’s growth is due to the company at the final stages of ramp up reaching peak production in 2016. The company has seen a decline since 2016.

- Argonaut has brought the San Agustin mine in production to replace El Castillo which is due to close by the end of 2021. The growth in production is therefore temporary.

- SSR achieved its growth mainly through the acquisition of Claude Resources in 2016 which was paid for in shares, therefore not reflected as a cash investment.

- Similarly, but to a lesser extent, Teranga achieved substantial growth from the Wahgnion project through the acquisition in 2016 of Gryphon Minerals Limited by issuing shares for approximately US$50 million.

- Semafo achieved all its production growth in 2019 when it brought its Boungou mine in production just as Mana’s output was dropping down fast. The production increase is due to the Siou underground mine section starting up. It has however a short LOM at this stage planned to be depleted in 2024. However, of all the companies in Table 3, this company can claim growth (which will only be sustained when they bring in something new by 2025).

Mining companies have to run hard to stand still. Their main asset is a depleting one and replacing this takes a bucketful of money. Companies like to classify these outlays as for “growth” whereas it is essentially to extend the life of the holding company. There are very few mining companies that can claim to have truly grown their production, and those who did usually benefited from an exceptional project (i.e. B2Gold when commencing the Fekola mine in 2017) and are thereafter condemned to keep up with depletion. B2Gold’s December 2020 Corporate Presentation forecast no growth until 2024, not long before the current Otjikoto reserves are depleted.

The discussion above was to show why AISC cost reports are pretty meaningless.

However, the companies also abuse AISC as it allows management to hide its incompetence. As is observed in an article in kitco.com “The Real Cost of Mining”:

“Companies capitalize significant expenditures year after year as Investments in Mining Property. Then every few years they take major write-offs to clear out the balance sheet. That effectively hides underperformance in bad years and then allows future years to ignore those costs.

We submit that gold mining write-downs are more a result of marginal operations than expensive acquisitions. The earnings that get written-off would not have been earnings if costs were originally classified as expenses instead of capital items.”

In other words, companies do not account properly for bad investment decisions on an annual basis and “adjust” at larger intervals, expecting shareholders to shrug their shoulders on these book entries as being historical and not important to the immediate and future cash flow of the company.

So what should you do?

We recommend that you do not put too much faith into All-In-Sustaining-Cost figures as reported by mining companies. All too often the figures are not ‘all-in’ and are not ‘sustaining’ over more than a single reporting period.

We recommend you see that analysis of cash flow statements in financial statements give a vastly superior picture of the true cost of sustained mining than AISC.

The formulas is relatively simple:

(Cash from Ops after Changes in Working Capital – Cash Used for Investing Activities) / Au ounces Sold

Yes, there are flaws as the cash flow statements can give an incomplete picture as they hide tax-like outflows under “financial activities”, do not show the consideration paid in company shares and include temporary items such as restricted cash, but they give you a much better understanding of the Company.

The fact that AISC figures produced by mining companies is highly selective explains why even “low AISC” companies somehow never make enough net free cash to pay dividends. Not only that but many of these ‘highly profitable’ companies find themselves having to come back to the equity markets over and over again, to refinance.

We recommend that you, dear reader, do yourself a favour and in future do the analysis. Again, it is the cash from operations after changes in Working Capital, minus the cash used for investing activities, and all of that divided by the ounces of gold sold.

Make sure to check that there are no exceptional items included and see whether the company can genuinely claim a proportion of the capital expenditure was spent on a project that will truly increase production in the medium to long term. The amount of cash spent on this particular project can be found in the financial statements under a table in the notes called Property, Plant and Equipment and deducted from Cash Used for Investing Activities in the formula.

Good Luck! And if you cannot face doing that work, we are certainly glad to do it for you (as long as you do not bite our heads off should we point out that your favourite company is destroying value).

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed