Undervalued? Silvercorp Targets 5x Revenue Increase in 6 years as It Expands Beyond China

Silvercorp's profits surge on higher metals prices; new Ecuador and Kyrgyzstan projects and a Hong Kong listing aim to close its valuation gap with peers.

- Silvercorp Metals reported a sharp rise in net income and free cash flow in its fiscal Q3 and Q4 (quarters ended December and March), driven primarily by higher silver, gold, and zinc prices

- President Lon Shaver attributes the company's valuation discount versus peers to its history as a single-asset (Ying Mining District), single-jurisdiction (China) producer, which has limited interest from some investors.

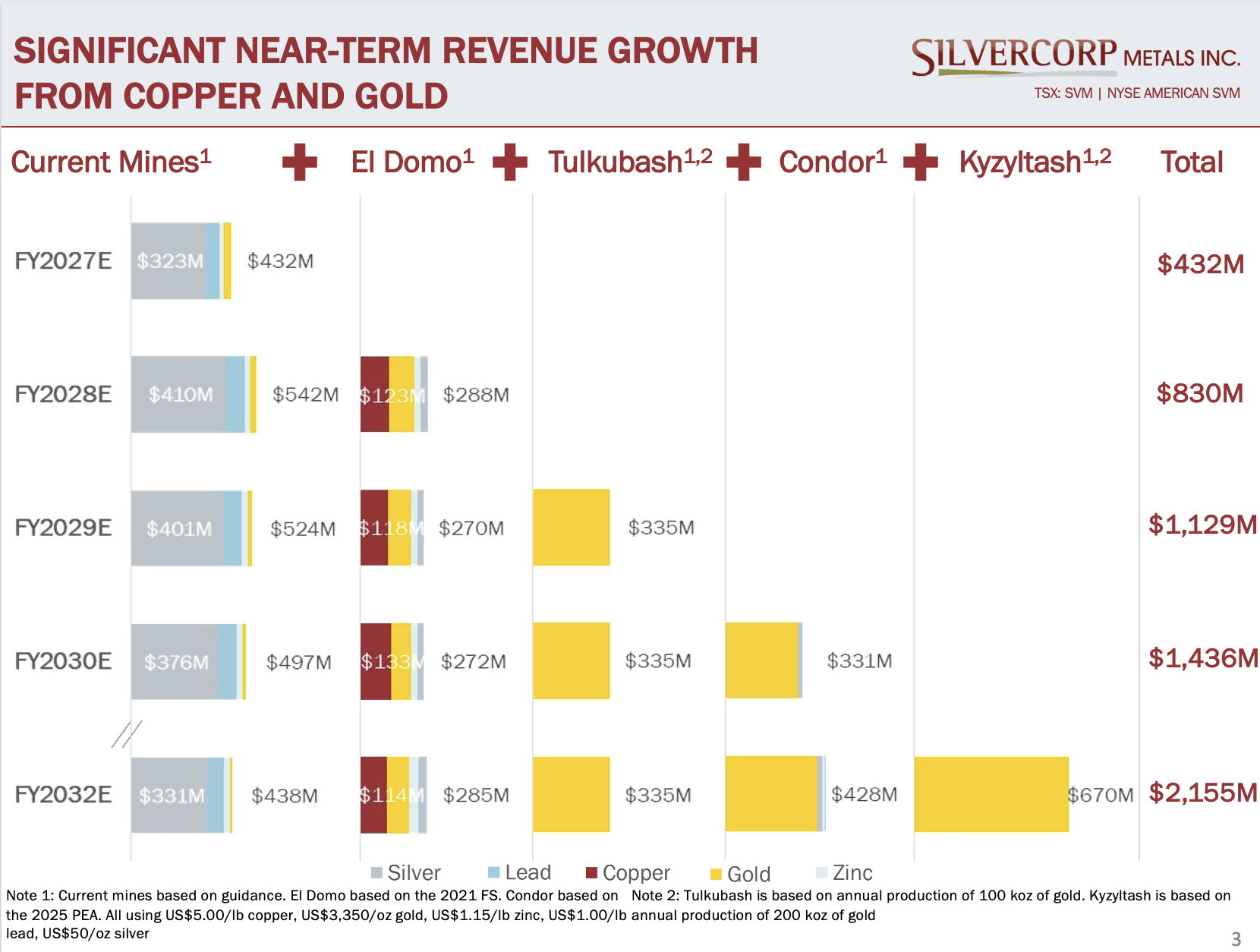

- The company is diversifying through the El Domo project in Ecuador (now in construction, targeted for production in mid-2027), the Condor gold project in Ecuador, and two newly acquired gold projects in Kyrgyzstan representing exposure to more than 6 million ounces.

- Silvercorp has filed a registration statement for a tertiary listing on the Hong Kong Stock Exchange, in addition to its existing TSX and NYSE American listings, to reach a broader pool of investors.

- Management outlined a path from approximately $400 million in current revenue to over $2 billion within five to six years, to be funded through internal cash flow and an untapped roughly $220 million RMB-denominated credit facility.

Silvercorp Metals, a silver, lead, and zinc producer with its primary operating base in China, has spent the past two fiscal quarters posting some of its strongest financial results in years. In a discussion with company President Lon Shaver, the conversation centered on a question many investors have asked: why does a profitable, cash-generative silver producer continue to trade at a discount to its peer group? Shaver laid out the company's recent operating performance, the cost and pricing dynamics behind it, and the steps Silvercorp is taking - including new projects in Ecuador and Kyrgyzstan and a planned Hong Kong listing - to address that valuation gap. The discussion is relevant to investors evaluating silver equities in a higher metals price environment, where the distinction between price-driven and operationally-driven earnings growth matters for assessing the durability of returns.

Recent Financial Performance: Margins Expand on Higher Metals Prices

Silvercorp's two most recent quarters, ended December and March, showed a marked increase in net income and free cash flow. Shaver was direct in attributing the bulk of this improvement to metals prices rather than operational change:

"from the operational improvements, I'd say our production has shown some modest growth, but really it's come down to metals prices that we've been experiencing."

He noted that the fiscal fourth quarter, which falls during Chinese New Year, has historically been seasonally weaker due to mine shutdowns and catch-up payments. This year, expanded production capacity at the Ying mine offset that typical seasonal dip, allowing the company to capture more fully the benefit of higher prices. Operationally, the company tracks performance using a margin-per-ton framework: revenue per ton of ore mined (the net smelter return) minus the all-in sustaining cost per ton, with the resulting margin having "upticked dramatically here these last couple quarters because of higher metals prices," partly aided by treatment and refining terms that have moved in the company's favour, amid tight concentrate markets for silver and zinc.

Cost Discipline Amid Industry-Wide Inflation

While metals prices have been the primary driver of recent results, Shaver pointed to specific operational measures aimed at controlling costs in an inflationary mining environment. These include converting ore haulage trucks from diesel to rechargeable electric vehicles, and scheduling electricity-intensive activities such as crushing and dewatering during off-peak overnight hours to take advantage of lower power rates.

The company is also evaluating greater mechanization and automation in both milling and mining to reduce labor requirements per ton of rock moved. All-in sustaining costs for the twelve months ended March were just over $14 per ounce of silver, net of byproduct credits.

The Valuation Discount: A Single-Asset, Single-Jurisdiction Legacy

Despite the improved financial profile, Silvercorp continues to trade at lower valuation multiples than its North American silver peers and Chinese-listed mining companies, on both trailing and forward-looking bases. Shaver framed this gap as a function of perception rather than performance:

"up to now we've been a largely single asset, single jurisdiction company... it's located in China and not all investors are familiar with what it's like to operate in China."

He added that peer companies with higher multiples tend to be those with multiple assets across multiple jurisdictions, suggesting that diversification, rather than operational improvement alone, may be necessary to close the gap.

Interview with Lon Shaver, President, Silvercorp Metals

Diversification: Ecuador and Kyrgyzstan

Silvercorp's response to this discount has been a series of corporate transactions intended to diversify its asset base. The company acquired a project in Ecuador, El Domo, which is now under construction with production targeted for mid-2027. A second Ecuadorian asset, Condor, is being advanced as what the company believes could be a low-cost underground gold project.

Earlier this year, Silvercorp acquired two gold projects in Kyrgyzstan, which Shaver said provide exposure to, and control over, more than 6 million ounces of gold that could be brought into production in stages. Together, these projects are intended to diversify revenue by both geography and commodity, with management projecting revenue growth from roughly $400 million currently to over $2 billion within five to six years.

Funding Strategy and the Hong Kong Listing

Shaver emphasized that Silvercorp's growth plans are largely self-funded through internal cash flow, supplemented by an untapped RMB-denominated term credit facility with Chinese banks worth roughly $220 million at what he described as attractive rates. He noted the importance of internal funding capacity given that capital market access can be cyclical:

"these windows come and go... so being able to generate your own returns out of your own assets is key."

The company also indicated it would consider equity markets opportunistically if valuation and timing were favourable. Separately, Silvercorp has filed a registration statement to pursue a listing on the Hong Kong Stock Exchange, in addition to its existing listings on the TSX and NYSE American. Shaver said this move is intended to access funds and individual investors in Asian markets who have shown growing interest in precious metals companies, not just the underlying commodities, and who may be more familiar with the jurisdictions in which Silvercorp operates.

TL;DR

Silvercorp Metals has seen net income and free cash flow rise sharply over the past two quarters, driven mainly by higher silver, gold, and zinc prices rather than production growth. The company attributes its valuation discount to North American and Chinese peers to its historical concentration in a single asset and jurisdiction, and is addressing this through new projects in Ecuador and Kyrgyzstan, a planned Hong Kong listing, and continued cost discipline. Management projects revenue could grow from roughly $400 million to over $2 billion within five to six years, funded largely through internal cash flow and an available credit facility.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed