Industrial Demand Growth & a 297koz Platinum Deficit Strengthen the Case for Future Mine Supply

Platinum demand is expanding beyond autocatalysts into industrial, hydrogen, and AI infrastructure markets as a 297koz deficit supports future mine supply.

- catalytic converters, historically platinum's largest end market, but growth in industrial, hydrogen, and emerging technology applications is offsetting part of that decline.

- The World Platinum Investment Council (WPIC) forecasts industrial platinum demand rising 9% to 2,238 koz in 2026, driven by renewed glass-capacity expansion, while automotive demand is projected to fall 2% and jewellery demand 12%.

- Hydrogen technologies and platinum-containing applications tied to data-center infrastructure are creating new sources of demand beyond the automotive market, reducing reliance on catalytic converters as the metal's dominant end use.

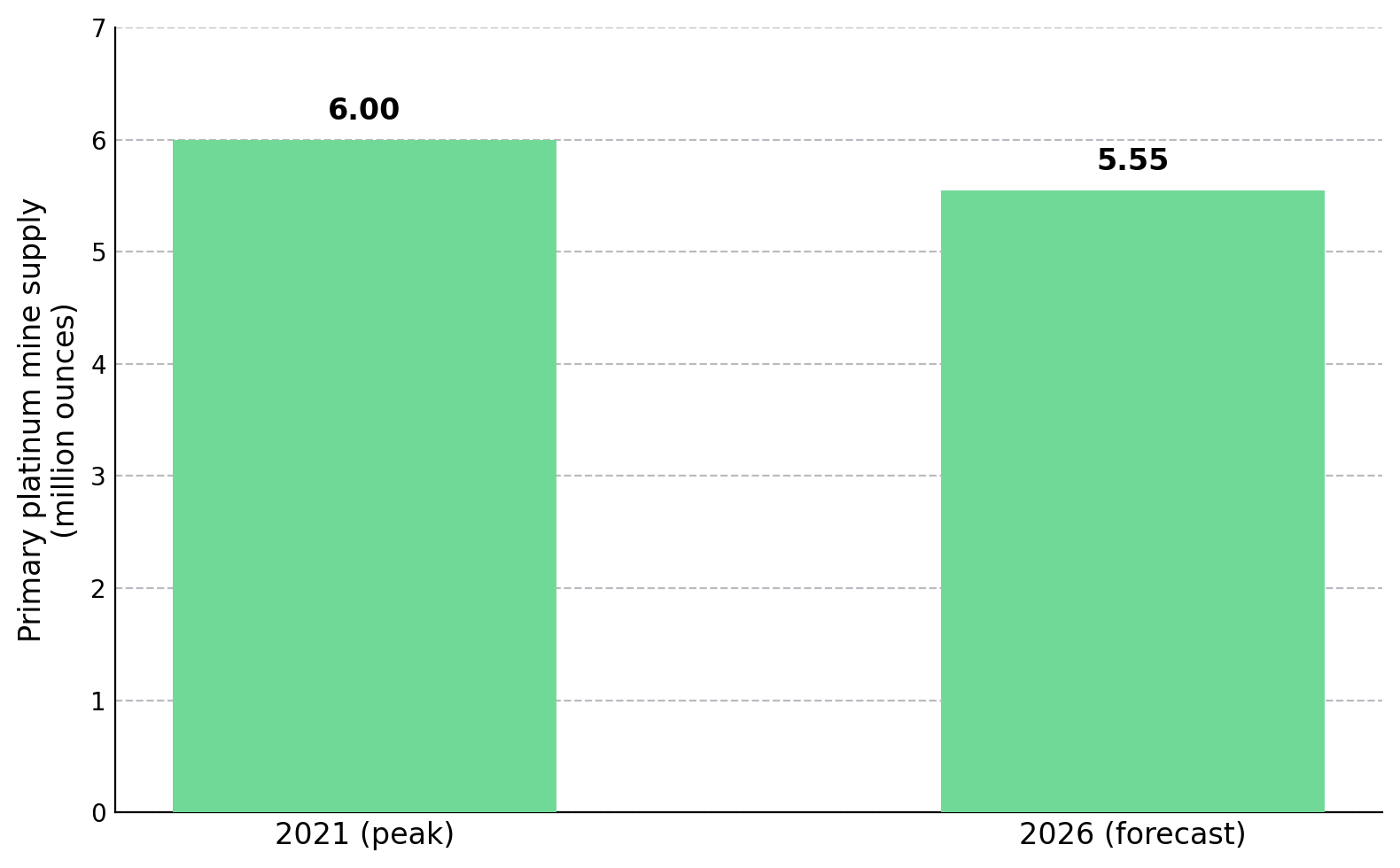

- A broader demand base, combined with mine supply that is forecast to remain near 5.5 million ounces in 2026 versus more than 6 million ounces in 2021, reduces reliance on any single end market and strengthens the case for sustained platinum deficits.

- A broader platinum demand base can increase the strategic value of early-stage resources by reducing uncertainty around future end-market demand, although exploration-stage companies remain exposed to permitting, financing, technical, and execution risks.

BEV Growth Reduces Autocatalyst Demand as Platinum Supply Stays Tight

For most of the past two decades, the automobile sector has been the dominant source of platinum demand. Roughly 40% of annual platinum demand has historically come from autocatalysts, which use platinum to reduce vehicle exhaust emissions in internal combustion engine vehicles. As a result, platinum demand became closely tied to global vehicle production and emissions standards that influence autocatalyst loadings. It also left platinum exposed to rising battery electric vehicle adoption because BEVs do not require exhaust systems or catalytic converters.

As BEV adoption increases, WPIC forecasts automotive platinum demand declining 2% in 2026, while jewellery demand falls 12%, reflecting weaker demand from platinum's traditional end markets. Hybrid vehicle growth, higher platinum loadings required to meet stricter emissions standards, and continued substitution of platinum for palladium offset part of the decline, but not enough to return automotive demand to growth.

Nick Smart, Chief Executive Officer of ValOre Metals, explains why platinum supply has remained constrained even as prices have risen sharply:

"The primary mine production of platinum has been in decline in the last 5 years. That is in the context of a metal price which has doubled over the course of the last year, so that tells you something about the inelasticity around supply and the difficulty of bringing new metals into the market."

Hydrogen, Industrial Growth & AI Infrastructure Diversify Platinum Demand

If the automotive pillar is shrinking, the more important question for a long-horizon investor is what replaces it. The answer is not a single substitute but a broadening of the demand base across several unrelated end-markets. This diversification sits at the heart of the platinum demand 2026 narrative, and it changes the metal's risk profile in a way that headline auto figures obscure.

Industrial Demand Growth Offsets Automotive Weakness

Industrial demand is currently the largest source of growth offsetting weaker automotive demand. WPIC forecasts platinum industrial demand rising 9% to 2,238 koz in 2026, driven primarily by renewed investment in glass-production capacity. Platinum is used in glass-manufacturing equipment such as bushings and crucibles, which wear out over time and must be replaced, linking platinum demand to industrial capital spending and manufacturing investment.

Industrial platinum demand is driven by manufacturing and capital-investment cycles rather than vehicle production. Demand comes from chemical, petroleum, electrical, and glass applications, making it more dependent on industrial capital spending than vehicle sales. For investors, industrial demand should be assessed separately from automotive demand because the two markets respond to different economic drivers and investment cycles.

Energy Security Policies Create a New Platinum Demand Driver

Hydrogen technologies represent another potential source of platinum demand growth. Platinum is a key catalyst in proton-exchange membrane (PEM) electrolysers, which use electricity to produce hydrogen, and in fuel cells, which convert hydrogen back into electricity. As governments invest in domestic hydrogen production to strengthen energy security, platinum demand becomes increasingly linked to public policy and infrastructure spending rather than consumer vehicle purchases. Hydrogen-related platinum demand is unlikely to be a major contributor in 2026, but it could become more significant if hydrogen deployment expands over the next decade.

AI Infrastructure Creates a New Platinum Demand Channel

WPIC identifies artificial intelligence infrastructure as a potential new source of platinum demand, including applications in optical communications and data-storage technologies. Demand from these applications remains small relative to automotive and industrial consumption, but continued investment in data-center infrastructure creates an additional source of platinum demand that is independent of vehicle production.

Growing Platinum Demand Raises the Value of Future Mine Supply

Platinum demand spread across automotive, industrial, hydrogen, and data-center applications is less dependent on any single end market than demand dominated by autocatalysts. The diversification reduces uncertainty about whether sufficient platinum demand will exist when a new project reaches production. Expectations for future demand directly influence key valuation metrics such as NPV and IRR because they affect assumptions about future prices, revenues, and project economics. A broader and more reliable demand base can support stronger project valuations by increasing confidence in future revenue assumptions.

Primary mine supply is forecast at about 5.5 million ounces in 2026, down from more than 6 million ounces in 2021, while WPIC projects a fourth consecutive annual market deficit of roughly 297 koz. When demand growth outpaces supply growth, new sources of platinum production become more valuable to the market. ValOre Metals provides an example of how investors may evaluate undeveloped platinum resources in this environment. Its Pedra Branca project in Brazil hosts an estimated 2.2 million ounces of platinum, palladium, and gold combined at a grade of 1.08 g/t across seven near-surface zones, according to a National Instrument 43-101 technical report.

The resource remains in the inferred category and is not a reserve, while the project has yet to publish an NPV, capital-cost estimate, or AISC ahead of its first PEA, targeted for late 2026. ValOre's market value of roughly C$26 million remains well below that of comparable development-stage platinum group metals companies valued between approximately C$126 million and C$236 million, reflecting its earlier stage of advancement. Much of that valuation gap reflects the absence of economic studies and operating data rather than a definitive assessment of the project's resource potential.

Growing demand from multiple end markets increases the strategic value of new platinum supply, particularly from jurisdictions outside southern Africa, where most primary platinum production is concentrated.

Stronger Demand Does Not Eliminate Project Risk

Stronger platinum demand fundamentals improve the outlook for future supply, but project success still depends on company-specific factors such as metallurgy, financing, permitting, and execution. The long-term demand outlook and the risks that could prevent a project from reaching production should both be evaluated.

Metallurgical Recovery Remains a Critical Valuation Variable

Stronger platinum demand does not eliminate project-level processing risk. Most South African platinum deposits occur in sulphide ore that can be processed using flotation, while oxidised near-surface ore often requires more complex hydrometallurgical techniques. Pedra Branca's near-surface mineralisation is oxidised, making metallurgical performance a key factor in the project's economic viability. ValOre has reported positive early-stage recovery results from a leach-based route, but those results remain subject to further testing and scale-up.

Those recovery rates, approximately 74% for platinum and 73% for palladium, come from shake-flask testing, an early-stage laboratory method, and must be confirmed at larger scales before they can support a PEA. Metallurgical performance therefore remains a critical project variable, because recovery rates directly influence operating costs, payable metal production, and ultimately project valuation.

Platinum Demand Drivers Should Be Modelled Separately

Investors should not assign the same importance to every source of platinum demand when building long-term forecasts. Demand linked to emissions regulations and government-backed hydrogen programmes is generally more durable because it depends on policy commitments rather than short-term consumer spending. Jewellery demand and the timing of industrial capital projects can fluctuate with consumer sentiment, financing conditions, and capital spending cycles. DInvestors should model declining automotive demand should be modelled separately from growth in industrial and hydrogen demand because each responds to different drivers and can develop at different rates.

The Investment Thesis for Platinum

- Platinum demand is expanding across industrial, hydrogen, and data-center applications, reducing reliance on autocatalysts and increasing confidence that future demand can support new mine supply and project development.

- Mine supply remains near 5.5 million ounces, below 2021 levels, while WPIC forecasts a fourth consecutive annual market deficit. With little supply growth available, additional demand from industrial, hydrogen, and technology applications is more likely to translate into tighter market balances and stronger platinum pricing.

- Demand growth across multiple platinum end markets increases the importance of future mine supply, particularly from projects outside southern Africa, where most primary platinum production is concentrated.

- Pre-economic-study explorers typically trade at substantial enterprise value per ounce discounts to development-stage peers because they have not yet published economic studies that establish NPV, operating costs, or project returns.

- Projects located in jurisdictions with established permitting frameworks and existing infrastructure can face lower development costs, shorter timelines, and fewer execution risks when advancing from resource definition to production.

- Valuation gains for exploration-stage companies typically depend on milestones such as a maiden economic study and larger-scale metallurgical test results that reduce project uncertainty. The broader platinum demand outlook would weaken if declining autocatalyst demand outpaces growth from industrial, hydrogen, and technology applications.

Viewing platinum solely through the lens of electric vehicle adoption overlooks the growing contribution of other demand sources. While autocatalyst demand is declining, industrial, hydrogen, and data-center applications are becoming increasingly important consumers of platinum, while mine supply remains constrained. For investors, the key implication is that platinum demand is becoming less dependent on a single end market and increasingly influenced by industrial investment and government-supported hydrogen deployment. A broader demand base can improve confidence in long-term project valuations and increase the importance of future mine supply. However, exploration-stage projects still require economic studies and larger-scale metallurgical testing before investors can determine whether a resource is likely to become a profitable mine.

TL;DR

Platinum's long-standing dependence on automotive catalytic converters is weakening as battery electric vehicle adoption reduces autocatalyst demand, but industrial demand is forecast to rise 9% in 2026 while hydrogen and AI-related infrastructure create additional sources of consumption. At the same time, mine supply remains constrained near 5.5 million ounces and WPIC forecasts a fourth consecutive market deficit of 297koz. For investors, the key implication is that broader demand support and limited supply growth increase the importance of future mine supply, although project valuation still depends on economic studies, metallurgical performance, financing, permitting, and execution risks.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

Stay Informed