Bannerman Energy (BMN) - Top 10 Uranium Producer is Realistic Target

Interview with Brandon Munro, CEO & MD of Uranium Developer, Bannerman Energy

We recently spoke to Brandon Munro, CEO of Bannerman Energy, who updated us about the developments at their Etango Project in Namibia. Etango is a large project, with a world-class uranium reserve. They’ve recently “reimagined” their business model at Etango with their “Etango 8 Development”, which has resulted in a fast-tracked, streamlined production schedule.

Company Overview

Founded in 2005, Bannerman Energy (formerly Bannerman Resources) is an Australian, multi-listed uranium development company. Headquartered in Subiaco, Perth, Western Australia, the company’s flagship asset is the Etango Project in Namibia.

Directors and Management

In addition to CEO Brandon Munro, eight other people have leadership roles within the company. They are Ronnie Beevor (Non-Executive Chairman); Mike Leech (Namibia Chairman); Clive Jones (Non-Executive Director); Ian Burvill (Non-Executive Director); Twapewa Kadhikwa (Non-Executive Director, Namibia); Werner Ewald (Managing Director, Namibia); Robert Orr (CFO) and John Turney (Project Advisor-Etango).

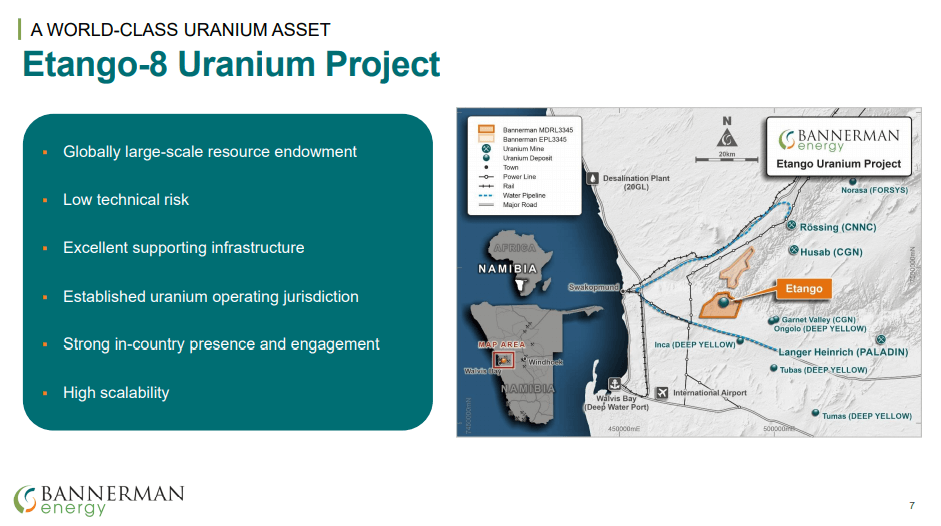

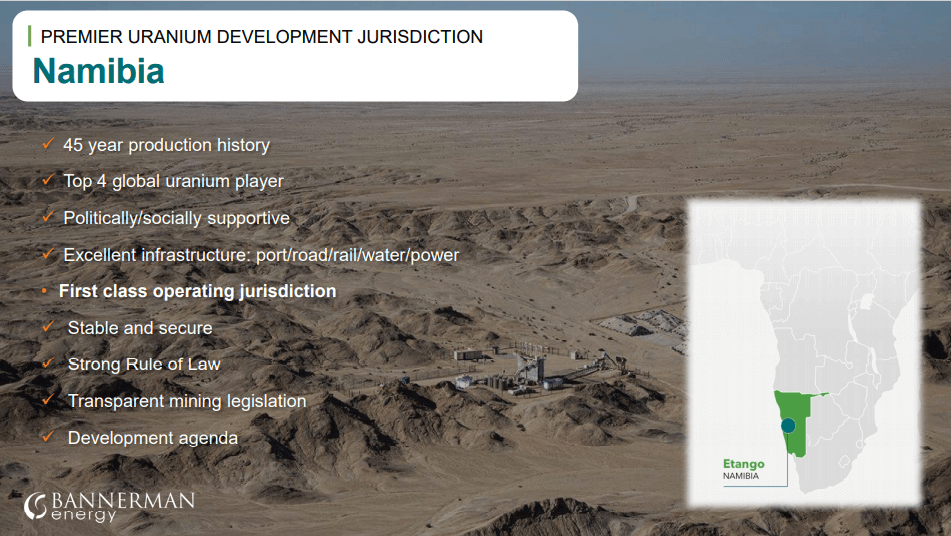

The Etango Project

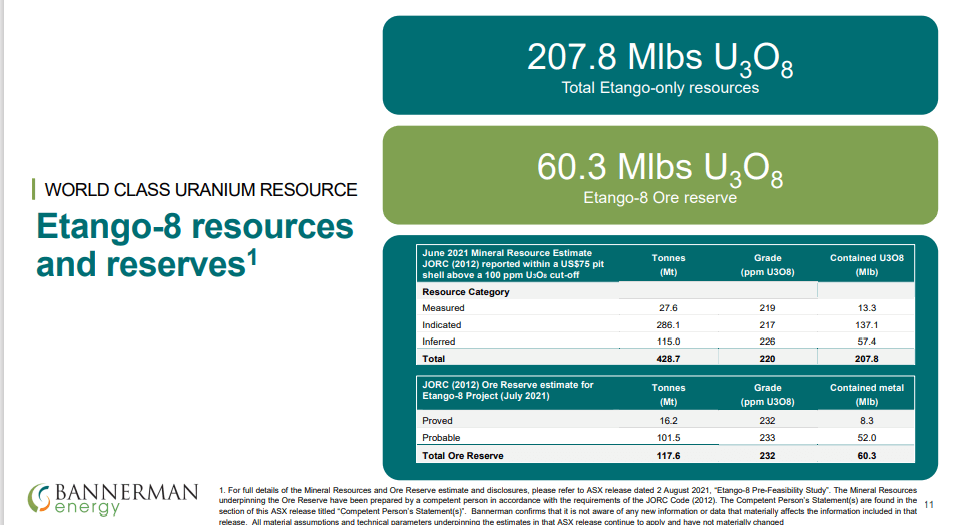

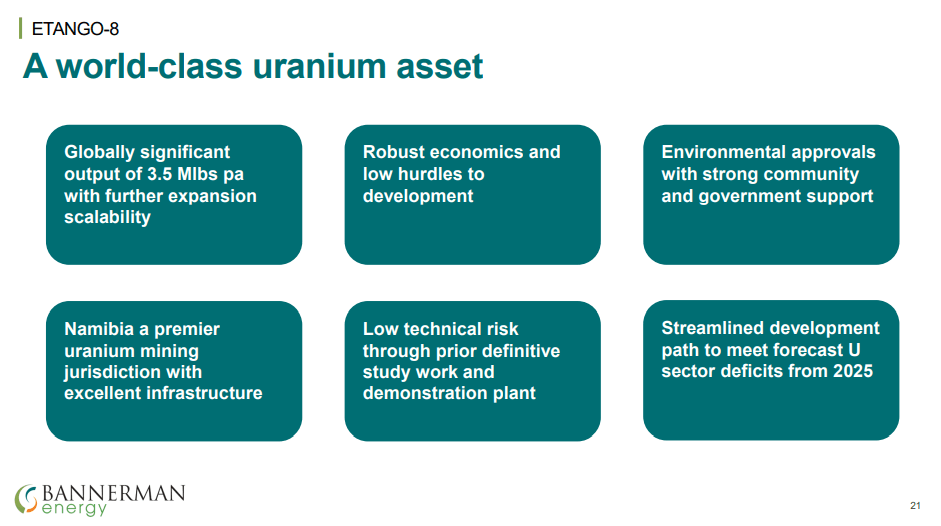

The Etango Uranium Project is located in the Erongo Region of east-central Namibia, 30 kilometres southeast of Swakopmund. This large deposit has a uranium mineral resource estimated at 227 M lbs. of U308. The company has just finished a Pre-Feasibility Study (PFS) on Etango. The results of the PFS, as well as previous studies, indicate that Etango is strongly amenable to development, both from a technical and economic perspective.

Pre-Feasibility Study at Etango

Munro was quite excited about the recent release of their PFS to the investor community.

“We’re really happy with how it’s come out and we’re just excited to get it out into the marketplace and just start talking about it.”

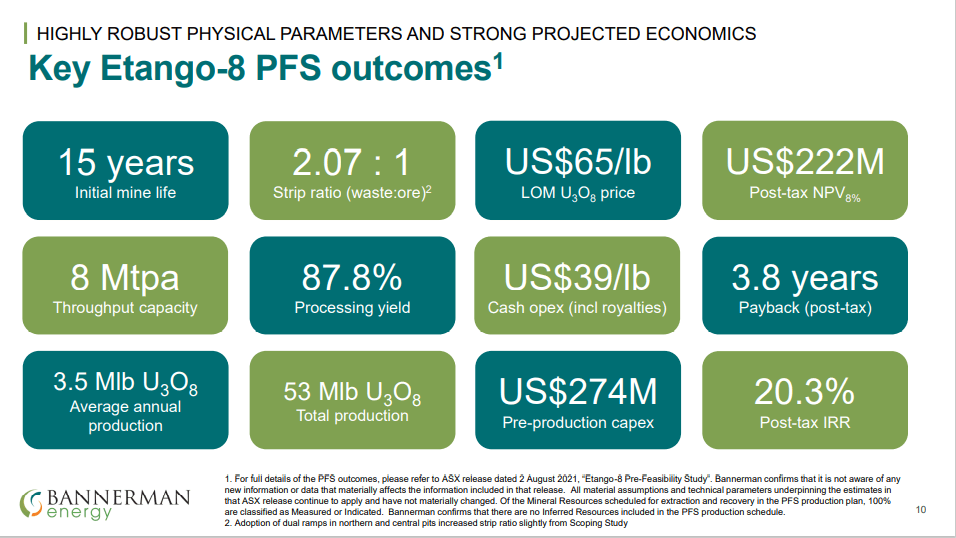

The company had previously indicated that it would be ready by early August 2021, and they provided it right on time (meeting promised targets, a good sign for investors). The numbers contained in the PFS came in as previously predicted by the company. Munro reminded us that it’s very unusual for a PFS to hit the same numbers, and slightly improve what’s in a Scoping Study. Normally, what you would have with a fresh project is a degree of optimism and uncertainty in a Scoping Study that struggles to bear out in a PFS. The fact that the numbers aren’t very different, is a testament to the high-quality technical work that’s been done on this project since 2005.

A number of assumptions have been built into the PFS. Bannerman has assumed an average $65 contracted price, about double of today’s uranium spot price. This gives the project a post-tax IRR of 20%, which is quite comfortable according to Munro given the relatively easy nature of the open-pit mining operations that they envision. The project models out at a post-tax NPV (using a discount rate of 8%) of USD $212M.

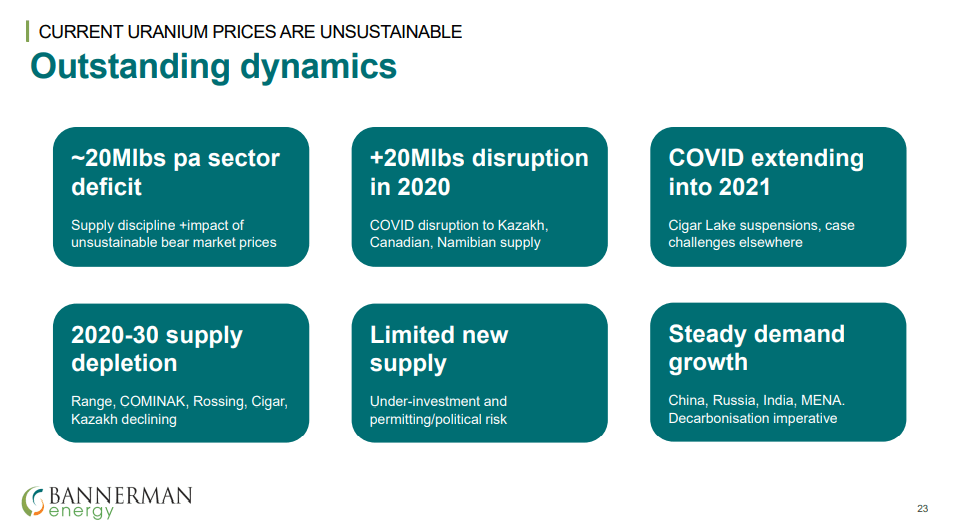

Munro is very comfortable with their assumed uranium price of $65. The company has modelled the entire uranium sector using a very detailed macro-economic analysis, a process in which Brandon has been intimately involved. For example, they are aware that a large proportion of current uranium production around the world is not economic at the current spot price. They’ve already seen significant production go into care and maintenance, both in Canada, Namibia, and elsewhere. There are many hundreds of billions of dollars of sunk capital in nuclear power plants that will continue to operate and continue to deliver clean electricity into a decarbonized world that needs them more than ever.

The uranium to fuel these nuclear power plants simply has to be bought over a period of time. Munro believes that the current price of uranium is unsustainably low. If the current price stays where it is, the amount of production of Uranium in the world will go down even further, which is already running at a 15% - 20% deficit in the sector. He believes that the uranium price needs to settle in the order of $75 to $80 over the medium term to incentivize enough new production to come on stream.

In this decade, four of the top ten producing uranium mines have either already shut or are scheduled to close. In addition, the huge production centre in Kazatomprom, Kazakhstan, will be depleted significantly over the next few years. The new uranium production has to come from somewhere. Based on these reasons, Munro is very comfortable using $65, and certainly believes that there’s upside above that as well.

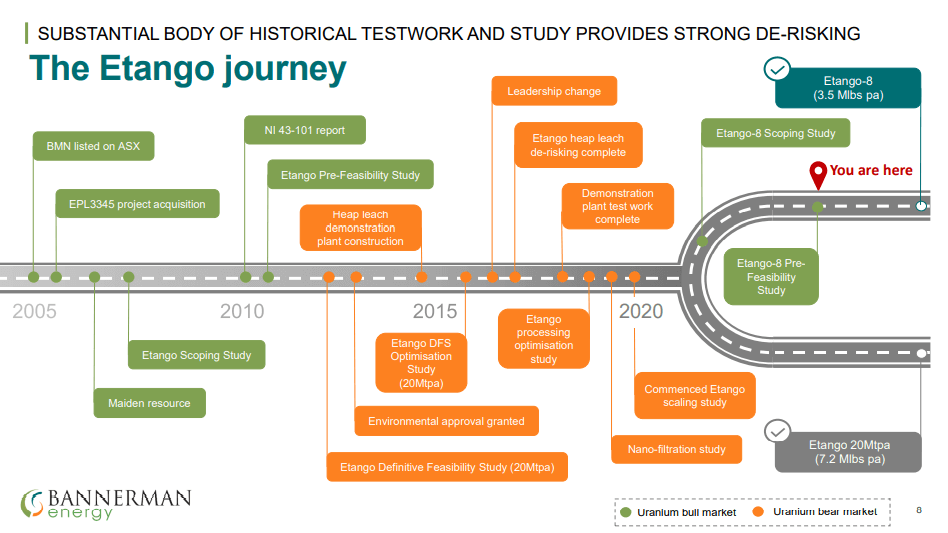

Etango “Reimagined”

Back in 2012, Bannerman released a Definitive Feasibility Study on the giant-sized Etango project. It was subsequently refreshed in 2015. The project that was envisioned at that time had a throughput of 20Mt for the enormous annual average production of 7.2Mlbs of uranium per annum, ranking up there at that stage among the top ten Uranium mines in the world once it was in production. That work was started in a much different market setting and before the Fukushima incident in Japan.

That project size would require an enormous capital cost, about USD $793 M. For a project of that scale it is quite common and not unreasonable, but in a bear market, it wasn’t very proportionate to Bannerman’s market capitalisation. Questions arose about the ability to finance the project and this resulted in a number of development hurdles coming into play.

About two years ago, Bannerman began rethinking the whole project. In particular, they imagined a scenario in which the total production was scaled back. Was there a way they could do that without hurting the economics?

The current project was envisioned as a bulk-tonnage operation, which is often the bigger the better. However, a curious thing happened. The team found that if they stayed within a pit shell design of about 50Mlbs - 60Mlbs, the stripping ratio came right down. That’s because the uranium ore body at Etango is exposed at the surface. Disposal costs of waste rock were drastically reduced in the new scenario.

By reducing the scale of the project, they dramatically reduced the Cap-Ex and did so in such a way where it actually reduced the Op-Ex rather than increasing it. For that reason, Bannerman has just published a PFS that has a pre-production capital cost of USD $274M, which compares very well with the USD $793M that was released in 2015. And, in the new scenario they have only halved the production to 3.5Mlbs per year.

Also of importance to potential investors, it will be relatively easy with minimal incremental cost to scale the project back up to the original 7.2Mlbs that they previously earmarked as the production target with the larger project. That larger resource gives Bannerman Energy some interesting leverage opportunities going forward.

“It enables us to get into production sooner, with lower development hurdles. Once we’re in production and profitable, we can look at expanding up to the original contemplated production levels in our 2015 DFS.”

African Uranium

In general, one of the knocks against African uranium, especially when compared to Athabasca Basin uranium, is the overall low grade of the metal ore. However, the cost of mining it is also low. In Namibia in particular, there is an extremely supportive government and a very supportive community. First-world uranium jurisdictions can come with a series of potential roadblocks. These are not as big a deal in Namibia; it's a very stable jurisdiction.

“That’s where we do have a distinct advantage in Africa generally, but particularly in Namibia, really stable jurisdiction, politically stable.”

In addition, at Etango, it's a very simple deposit to mine. Bannerman can produce uranium using a truck-and-shovel operation and a heap leach. Etango requires no underground activity and no robotics, just conventional open-pit mining. This is going to be a ‘sleep-well-at-night’ project.

Definitive Feasibility Study

Munro has a target date of third quarter 2022 to deliver a Definitive Feasibility Study (DFS) at Etango. He envisions needing $4M, which is money that they already have ($12.5M as of the 30th of June). The company is in a fortunate position because all of the required work for the DFS is complete. That work has been done to such a high standard that Bannerman can do a DFS on this project for $4M in about a year. The resource drilling is all done. Metallurgical work including operating a pilot plant is in place. The environmental work is completed.

Does Bannerman Have the Expertise to Build Etango Mine?

Munro is confident that he has the expertise in-house at the senior staff levels to get the project into production. Mike Leech, The Namibian chairman, was the managing director of the Rossing Uranium Mine in Namibia at a time when it was the largest uranium mine in the world. In addition, he was the CFO for 15-years before that. Werner Ewald, the managing director in Namibia, was mining manager at Rossing, and has been in the industry for a very long time. He’s very involved in the Namibian Chamber of Mines and is regarded as a real ESG leader in Namibia.

Munro himself has lived in Namibia for 6 years and knows the players, government people, and how the uranium industry works in the country. He is the co-chair of the World Nuclear Association’s Nuclear Fuel Demand subgroup, the body that WNA entrusts to forecast nuclear fuel and uranium demand out to 2040.

Marketing Efforts

As the project moves forward, long-term contracts will be negotiated and signed. Yellowcake will be delivered to utilities. This will require quite a bit of marketing.

Munro, Leech and Ewald have very deep experience, both of Namibia and the global uranium market, such that they will be able to conduct the required marketing or attract that specific expertise as needed.

Munro believes that right now is not the right time to begin marketing efforts. The current conversations that Bannerman is having with financiers and the industry, in general, is regarding what this company is all about and the scope of what they are trying to do. Right now, they want to communicate what they stand for and what their values are, and, when the time is right, they’ll engage in more detailed conversations.

In fact, Munro is hearing that some companies are putting in big marketing efforts to try to obtain contracts right now, but he hasn’t seen an announcement from any of those companies that they’ve succeeded. Apparently, these types of contracts are not being signed at the moment because of market doldrums.

It’s very quiet out there, so the uranium that is being bought or committed via long-term contracts is through old customer relationships with the likes of companies such as Cameco. Bannerman needs to wait for that process to wash out. When more demand comes to market, the new players will get their opportunity. In the meantime, they’ve got a strong collegiate relationship with those utilities and fuel buyers, and the other global market participants that Munro engages with through his work at the WNA and through the reputation and individual relationships that he and his company are continuing to cultivate.

Opinion On the Sprott Physical Uranium Trust

Sprott is in the process of listing its Physical Uranium Trust (SPUT) on the NYSE. Munro believes that this will definitely affect the whole uranium market. It’s coming on the scene during a timeframe when nuclear utilities are having their contract coverage running out at a time when a large proportion of the world’s current uranium production will be depleting.

SPUT will have the capacity to do frequent at-the-market raisings in Canada and within a period of time will access some much bigger markets in the US. That’s a positive for Bannerman Energy and every other uranium company because they will be competing for scarce spot pounds at a time when utilities will also start to re-enter the market. The spot market is thinly traded, so any level of serious competition is going to have a relatively immediate price impact.

Summary of the Opportunity

Bannerman’s opportunity will come when competition for term contracts becomes more active. The company intends to set themselves up for that time, when they will deploy all the advantages that they have over their competition.

To find out more, go to the Bannerman Energy Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed