What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 8

Fuel fabrication demand accelerates from 2027 as Asia's reactor boom, geopolitical shifts, and advanced fuel tech drive structural uranium supply tightening through 2040.

- Fuel fabrication is the least understood yet most strategic stage of the nuclear fuel cycle, connecting reactor performance directly to uranium demand and price sustainability.

- Global fabrication demand is set to accelerate from 2027 onward, driven by new reactor builds, first-core requirements, and Asia's projected doubling to quadrupling of fuel consumption by 2040.

- Geopolitical reconfiguration post-Ukraine war is reshaping supply security. European VVER operators are rapidly qualifying non-Russian suppliers, while the U.S. and allies invest in HALEU and advanced fuel infrastructure.

- Technological upgrades, Enhanced ATF, SMRs, and HALEU, will structurally raise uranium enrichment intensity, linking fabrication advances back to higher front-end demand.

- Uranium producers with low-cost, near-term supply such as Energy Fuels, Global Atomic, and Denison Mines are strategically positioned to capitalize on the tightening link between fabrication innovation and feedstock security.

The Overlooked Engine of the Nuclear Fuel Cycle

Fuel fabrication represents the final engineered conversion of enriched uranium into assemblies designed for specific reactor geometries. Unlike uranium, conversion, or enrichment, which trade globally, fuel assemblies are bespoke, reactor-specific components requiring precision manufacturing and long-term contracts. A PWR17 assembly cannot substitute for a VVER-1000 design, creating technical barriers that span multiple years of qualification and regulatory validation.

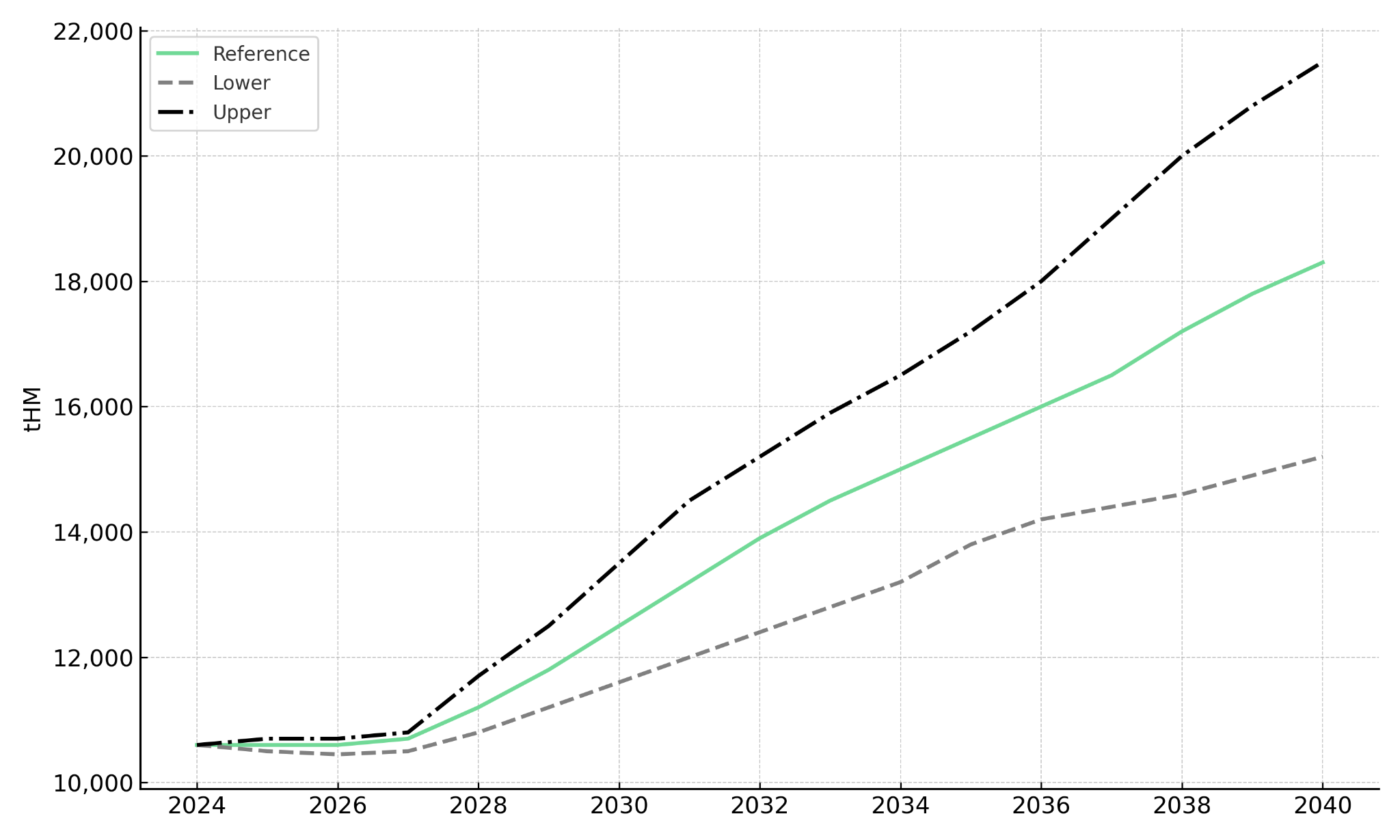

The demand profile consists of first cores, three times larger than reload batches, and steady reload demand, creating temporary surges tied to reactor commissioning timelines. The IAEA Reference Scenario projects nearly 3,000 tonnes of heavy metal per year for first cores by the end of the projection period. Asia accounts for the majority of growth, underscoring how front-end uranium supply and downstream fabrication capacity must remain aligned.

The macro environment for uranium has reached an inflection point driven by supply-side constraints. Troy Boisjoli, Chief Executive Officer of ATHA Energy, frames the investment opportunity:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career. The real demand that's being built up coupled with some of the supply side risk is a structural setup, like we have not seen in the uranium space."

Asia's Reactor Boom & The Next Wave of Fabrication Demand

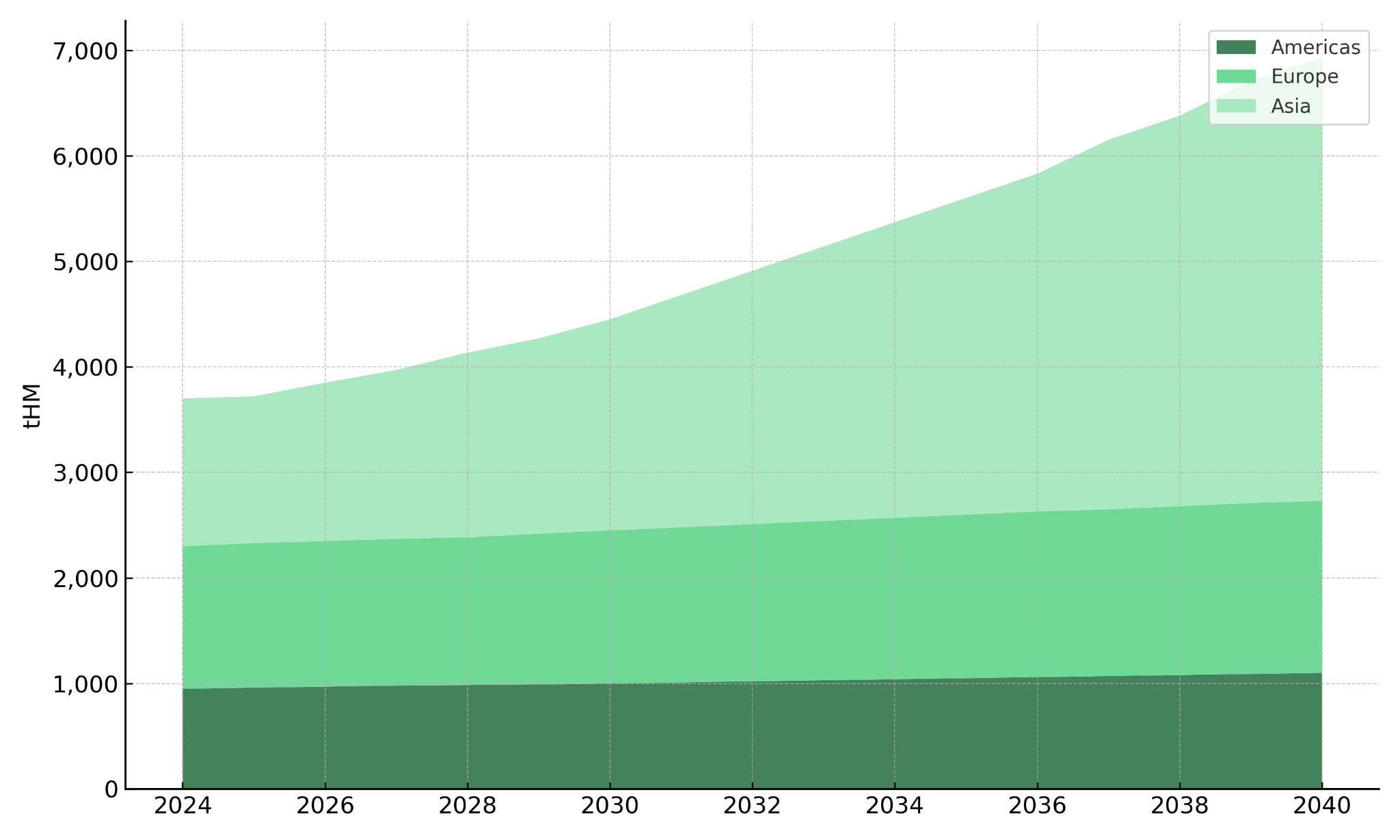

Asia leads the nuclear expansion, with demand projected to double to quadruple by 2040, depending on scenario. Countries including China, India, South Korea, Bangladesh, and Turkey are commissioning reactors that require both PWR17 and VVER fuels. Emerging markets in Africa, the Middle East, and Central Asia could add 600–1,200 tonnes per year of fabrication demand, aligning with uranium resource development in Africa.

This geographic concentration highlights the importance of supply-chain localization and regional fabrication infrastructure. Global Atomic's Dasa Project highlights this positioning as the highest-grade uranium project in Africa at 4,113 ppm, Dasa's 73 million pounds of reserves in a 23-year mine plan provide scale for regional demand. The project has maintained operational continuity through Niger's political transitions, with community relationships since 2008.

The United States faces a particularly acute uranium supply challenge. Stephen Roman, President and Chief Executive Officer of Global Atomic, quantifies the deficit:

"They're burning 50 million pounds a year, they're making everything ramped up, maybe four or five million pounds a year in the United States."

This supply-demand imbalance has driven strategic US government support for domestic production, including the Prohibiting Russian Uranium Imports Act and infrastructure funding for enrichment capacity.

Bannerman Energy's Etango Project in Namibia sits at the intersection of African fuel export potential. With 225 million pounds of resources, Etango is one of the world’s largest advanced uranium assets. Namibia's 45-plus year uranium history and geopolitically neutral positioning provide jurisdictional stability. The project is fully permitted with its Mining Licence received in December 2023, and early development works have been completed.

ATHA Energy's exploration portfolio across Canada's Athabasca, Angikuni, and Thelon Basins ensures future uranium availability. The flagship Angilak Project contains a historical resource estimate of 43.3 million pounds at 0.69 percent grade. The company successfully completed its 2024 exploration program, achieving a 100 percent drill hit rate for uranium mineralization.

The Geopolitical Reordering of the Nuclear Fuel Market

Russia's invasion of Ukraine triggered immediate reconfiguration of nuclear fuel supply chains. The non-fungibility of fuel assemblies amplified disruption severity, VVER reactors could not simply switch suppliers without multi-year qualification programs. European utilities rapidly initiated qualification of Western fabricators to replace TVEL-supplied fuel. This qualification process requires years of engineering validation and regulatory licensing, creating sustained capital demand and long-term contract certainty.

The non-fungibility barrier means supply chain diversification carries structural inertia, once alternative supply is qualified, it rarely reverts. Investors should view this as a durable de-risking of non-Russian fuel supply, supporting multi-decade stability in Western uranium demand.

Energy Fuels operates the Pinyon Plain mine, which achieved record monthly output of 258,745 pounds in May 2025 at 2.14 percent uranium oxide grades. The White Mesa Mill is the only fully licensed and operating conventional uranium processing facility in the U.S. With zero debt and working capital of $253 million as of mid-2025, Energy Fuels maintains financial strength to serve as a cornerstone domestic supplier.

The realization that critical mineral dependencies create strategic vulnerabilities has reshaped policy frameworks. Mark Chalmers, President and Chief Executive Officer of Energy Fuels, describes notes:

"The realization is that this critical mineral focus, the requirement on these critical minerals, the dependency on China and other countries... they're necessary for these modern technologies moving forward."

enCore Energy's ISR operations at Rosita and Alta Mesa target 3 million pounds per year by 2026, scaling toward 5 million pounds by 2028. The company's fully licensed processing infrastructure significantly reduces permitting risk. Ur-Energy's Lost Creek facility resumed commercial production in 2023 and is reliably producing uranium, with 1.2 million pounds per year designed capacity. The Shirley Basin project is advancing toward commissioning targeted for 2025, which will enhance annual production by an additional 1.0 million pounds.

Technology Upgrades Driving a New Uranium Demand Curve

Enhanced Accident Tolerant Fuels represent evolutionary improvements offering significant safety and performance benefits. E-ATF implementation, particularly to support longer fuel cycles, often requires LEU+ enriched uranium. E-ATF development, driven partly by the EU's requirement to use ATF from 2025, focuses on new cladding and fuel compositions. The need for higher enrichment to compensate for new materials directly impacts the front-end fuel cycle, highly relevant to investors tracking commodity inputs.

Small Modular Reactors are a key growth area. Many advanced reactors require enrichments up to 19.75% U-235, known as HALEU. Producing fuel for SMRs and Generation IV reactors requires adapting existing facilities or building new ones. The US DOE's efforts to support HALEU availability through contracts and corporate initiatives such as the Natrium Fuel Facility demonstrate clear public-private investment in necessary infrastructure.

The adoption of E-ATF and SMR-specific fuels could lift uranium enrichment requirements by 10–20% globally. This links directly to upstream growth opportunities for explorers and developers positioned for scalability. Denison Mines' Phoenix ISR Project's low-cost structure at $16.04 per pound offers competitive economics as higher enrichment intensity drives uranium price floors. With first production targeted for 2027/2028, Phoenix's development timeline aligns with accelerating demand growth.

As uranium markets confront constrained supply response, industry leaders emphasize structural advantages of production positioning. David Cates, President and Chief Executive Officer of Denison Mines, articulates the disconnect:

"The demand side is outperforming, which is excellent... its recognition of the importance of nuclear energy is not in debate anymore at all... The supply side has really been a struggle. The idea that we will have a perfect supply response to evolving and increasing demand is probably unrealistic."

Following its December 2023 acquisition of Consolidated Uranium, IsoEnergy's portfolio spans the high-grade Hurricane development project and conventional mining assets including the Tony M mine in Utah. Hurricane contains one of the world's highest-grade published indicated uranium resources at 34.5 percent uranium oxide, with 55.2 million pounds of measured and indicated resources. The company maintains $84.7 million in cash and equivalents as of mid-2025, with NexGen Energy maintaining a 30.9 percent shareholding.

Capital Reallocation & Modernization of Fabrication Infrastructure

Modernization efforts are drawing investment from governments and private firms, signaling new capital inflows into the downstream segment. The DOE's HALEU Availability Program, TerraPower's Natrium initiative, and the GNF-Framatome collaboration illustrate active public-private reindustrialization in Western fuel supply chains. Modernization often focuses on uprating existing plants or adding shifts, lowering capital intensity versus greenfield builds.

Despite apparent global overcapacity, the shift to specialized fuels, HALEU, TRISO, ATF, creates a bifurcation: overcapacity in legacy designs, undercapacity in advanced fuel fabrication. This asymmetric investment pattern will eventually translate to pricing power in enriched feedstock, favoring uranium producers with optionality and liquidity.

Premier American Uranium's flagship Cebolleta Project in New Mexico contains 18.6 million pounds in the indicated category, while the Cyclone Project in Wyoming has an exploration target range of 7.9 to 12.6 million pounds. ISR technology offers cost advantages and reduced environmental footprints, particularly valuable for securing community support and regulatory approvals.

The Investment Thesis for Uranium

- Fuel fabrication demand growth reinforces multi-decade uranium consumption visibility, driven by first cores and reloads as global nuclear capacity expands.

- Technological shifts including Enhanced Accident Tolerant Fuels, Small Modular Reactors, and HALEU-dependent advanced reactor designs structurally increase uranium intensity per megawatt-hour generated.

- Geopolitical diversification secures non-Russian supply chains, driving long-term contract repricing and sustained demand for uranium from allied nation jurisdictions.

- Capital reindustrialization across Western markets revalues low-cost, development-ready uranium assets positioned to serve emerging HALEU and LEU-plus fuel segments.

- High-grade, low-cost projects including Denison's Wheeler River, Global Atomic's Dasa, and IsoEnergy's Hurricane stand to outperform as input costs reset and contracting cycles reflect structural tightening.

- Companies with strong balance sheets, proven management teams, and jurisdictional advantages in premier mining regions capture disproportionate value as utilities prioritize supply chain resilience.

- Production visibility through operational assets or near-term development projects provides cash flow certainty supporting continued exploration investment and resource expansion.

- Geographic diversification across multiple projects or basins reduces single-asset execution risk while providing production flexibility.

Fuel Fabrication Is Re-Shaping Uranium’s Pricing Cycle

The fuel fabrication segment has transitioned from a downstream technical process to a determinant of nuclear sector supply chain security and cost trajectory. As first-core and reload demands surge through 2040, and as advanced fuel designs proliferate across both existing reactor fleets and new SMR deployments, upstream uranium markets are entering a structurally tighter phase characterized by sustained demand growth and supply chain reconfiguration. For investors, understanding fabrication dynamics is no longer optional, the segment defines where future uranium pricing power originates, how quickly new nuclear capacity can be deployed, and which jurisdictions and supply chain participants capture value as the global nuclear fleet expands. The geopolitical reordering accelerated by Russia's invasion of Ukraine has permanently altered utility procurement strategies, with supply security now commanding premium valuations relative to marginal cost advantages. Technological innovation within fabrication, particularly the transition toward LEU-plus and HALEU enrichments, creates a structural increase in uranium demand per unit of electricity generated, establishing higher uranium price floors while creating specialized market segments where technical capability and regulatory licensing command differentiated pricing.

The uranium producers best positioned to capitalize on these fabrication-driven trends combine several attributes: low-cost resource bases ensuring competitiveness across price cycles; development timelines aligned with demand acceleration in the late 2020s; jurisdictional positioning in allied nation frameworks prioritized by Western utilities; financial strength supporting multi-year development programs without excessive dilution; and management teams with demonstrated execution capability through permitting, construction, and operational ramp-up phases. Those positioned in low-cost, strategically located uranium assets, particularly projects in advanced development stages with clear pathways to production and established utility interest, will likely benefit most from this downstream-driven supply realignment as fabrication becomes the binding constraint on nuclear sector growth through the next two decades.

Read more:

Part 7 - Fuel Fabrication Supply and Demand

Part 6 - Conversion Supply and Demand

Part 5 - Uranium Supply and Demand

Part 2 - Nuclear Energy Security Imperatives

TL;DR

Fuel fabrication represents the critical link between reactor performance and uranium demand, yet remains the least understood stage of the nuclear fuel cycle. As Asia's nuclear capacity doubles to quadruples by 2040, first-core requirements three times larger than standard reloads will drive unprecedented fabrication demand acceleration from 2027 onward. Russia's Ukraine invasion triggered permanent supply chain realignment, with European utilities rapidly qualifying Western fuel suppliers while the U.S. restores domestic production capacity. Enhanced Accident Tolerant Fuels and HALEU-dependent SMRs increase uranium enrichment intensity 10-20 percent, structurally raising price floors. Low-cost producers in stable jurisdictions, particularly Canada, the U.S., and Namibia, with near-term production timelines and strong balance sheets are positioned to capture premium valuations as fabrication constraints bind nuclear sector growth through the next two decades.

FAQs (AI-Generated)

Fuel fabrication is the process of converting enriched uranium into precision-engineered fuel assemblies designed for specific reactor types. Unlike upstream uranium mining or enrichment, fabricated fuel assemblies are non-fungible, a PWR17 assembly cannot substitute for VVER or BWR fuel. This creates multi-year qualification barriers when utilities switch suppliers, making fabrication capacity a binding constraint on how quickly new nuclear plants can be deployed. For uranium investors, understanding fabrication bottlenecks is critical because downstream capacity constraints directly translate to upstream feedstock demand visibility and pricing power.

E-ATF designs use LEU+ enrichments (less than 5% but greater than 20% U-235) to extend fuel cycles from 18 to 24 months, requiring proportionally more natural uranium feedstock per assembly. SMRs, particularly advanced designs, require HALEU enrichments up to 19.75% U-235. Combined, these technologies could increase global uranium enrichment requirements by 10-20%, operating independently of reactor capacity additions. This enrichment intensity uplift establishes higher uranium price floors by raising the cost structure at which marginal supply becomes economic, benefiting low-cost producers with development optionality.

Asia accounts for the overwhelming majority of fabrication demand growth, with requirements expected to double, triple, or quadruple depending on deployment scenarios. China and India lead expansion, but growth extends across South Korea, Bangladesh, Turkey, and Japan's reactor restarts. Africa, the Middle East, and Central Asia could add 600-1,200 tonnes of heavy metal per year by 2040. This geographic concentration creates opportunities for uranium producers in stable jurisdictions, Canada, the U.S., Namibia, to secure long-term offtake agreements with fabricators serving these growth markets.

The Ukraine invasion triggered immediate reconfiguration of fuel supply chains, particularly for VVER reactors in Central and Eastern Europe. Utilities rapidly initiated multi-year qualification programs for Western fabricators (Westinghouse, Framatome) to replace Russian TVEL supplies. The structural inertia in these qualification barriers creates durable realignment, once Western suppliers achieve licensing, utilities rarely revert given the investment required. This establishes multi-decade revenue visibility for non-Russian supply chains and permanently revalues supply chain attributes: geographic diversity, jurisdictional stability, and long-term contracts now command premium valuations over marginal cost differences.

The best-positioned producers combine: (1) low-cost resource bases ensuring competitiveness across price cycles; (2) development timelines aligned with late-2020s demand acceleration; (3) jurisdictional positioning in allied nation frameworks (Canada, U.S., Australia, Namibia) prioritized by Western utilities; (4) strong balance sheets supporting multi-year development without excessive dilution; and (5) management teams with demonstrated execution through permitting, construction, and ramp-up. Projects in advanced development stages with clear production pathways and established utility interest capture the most value as fabrication becomes the binding constraint on nuclear growth through the next two decades.

Analyst's Notes

Subscribe to Our Channel

Stay Informed