What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 7

Global uranium enrichment capacity faces structural deficits post-2034 as demand grows 5.6-7.8% annually. Western fuel cycle independence drives premium pricing.

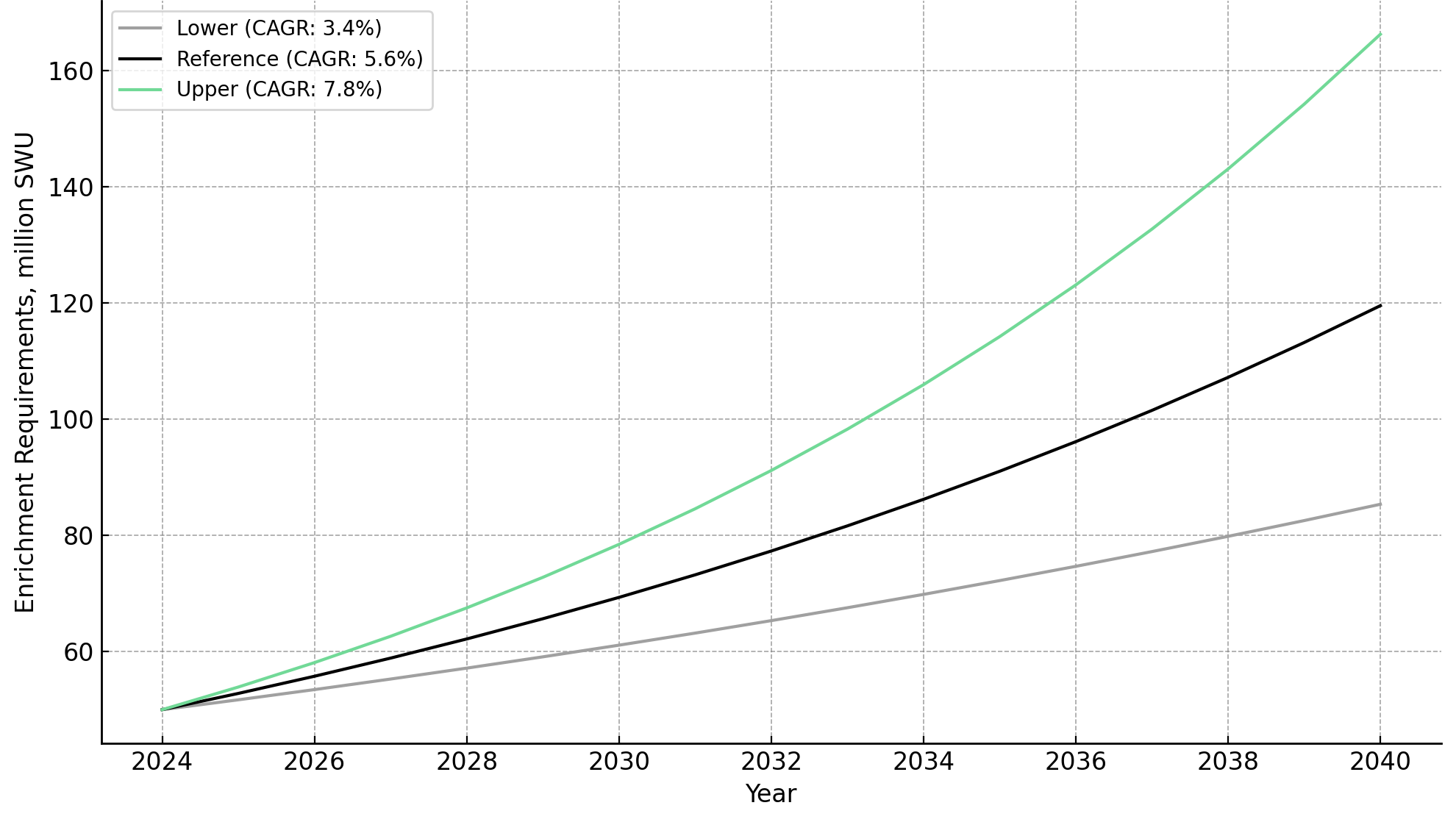

- Global enrichment demand is growing at a 5.6–7.8% compound annual growth rate through 2040, outpacing installed capacity and signaling a post-2034 supply deficit under the Upper Scenario.

- Russia's 27 million Separative Work Unit capacity dominance poses a critical energy security risk, driving Western initiatives to diversify enrichment sources and secure front-end uranium feedstock.

- The emergence of Small Modular Reactors and High-Assay Low-Enriched Uranium fuel requirements amplifies long-term demand for enriched uranium and upstream feed material.

- United States and Canadian uranium producers including Energy Fuels, enCore Energy, IsoEnergy, and ATHA Energy are strategically positioned to underpin Western fuel cycle independence.

- Institutional investors should focus on front-end bottleneck beneficiaries, low-cost producers, high-grade explorers, and developers tied to conversion and enrichment resilience.

The Midstream Constraint Reshaping Uranium Markets

The uranium sector is experiencing a renaissance driven by net-zero carbon targets and renewed energy security priorities across Western economies. Yet while industry attention has concentrated on mine restarts and reactor buildouts, a structural constraint is forming midstream, in the conversion and enrichment stages of the nuclear fuel cycle. This bottleneck, largely invisible to equity markets until recently, now represents the most significant supply risk facing the sector through 2040.

Global dependence on Russian enrichment capacity mirrors the energy vulnerabilities exposed by Europe's reliance on Russian natural gas. Russia controls approximately 27 million Separative Work Units of annual enrichment capacity, a dominance that Western governments and utilities now view as strategically untenable. The resulting pivot toward secure, domestic fuel supply chains is reshaping uranium demand fundamentals and creating a multi-year investment opportunity for producers capable of feeding Western enrichment infrastructure.

The next re-rating in uranium equities will hinge not only on mine supply, but on which producers can reliably deliver feedstock into the constrained enrichment system. As conversion and enrichment capacity struggle to keep pace with reactor demand, uranium producers aligned with Western fuel cycle independence are positioned to capture premium pricing and institutional capital flows.

The Global Enrichment Landscape

Uranium enrichment is the process that transforms natural uranium into reactor-grade fuel by increasing the concentration of the fissile isotope Uranium-235 from 0.711% to the 3–5% required for over 90% of operating nuclear reactors. The technical measure of enrichment effort is the Separative Work Unit, a metric that quantifies the energy and infrastructure required to separate isotopes. For institutional investors evaluating uranium equities, understanding Separative Work Unit dynamics is as essential as tracking reserve grades or all-in sustaining costs. Enrichment capacity determines how much mined uranium can be converted into usable fuel, making it a direct constraint on reactor operations and a critical driver of upstream demand.

Higher enrichment levels require proportionally more Separative Work Units per kilogram of Low-Enriched Uranium produced. For instance, producing 10 tonnes of Low-Enriched Uranium enriched to 4.5% Uranium-235 requires 62,306 Separative Work Units when operating at a tails assay of 0.30%, compared to 68,014 Separative Work Units at a 0.15% tails assay. This trade-off between enrichment effort and feed material efficiency becomes increasingly material as utilities balance Separative Work Unit availability against uranium feedstock costs.

Accelerating Demand and Supply Deficit Projections

Global enrichment requirements are accelerating at rates unseen in previous nuclear cycles. Under the Reference Scenario, enrichment demand is projected to grow at a 5.6% compound annual growth rate through 2040, reaching approximately 120 million Separative Work Units annually. The Upper Scenario, which incorporates accelerated Small Modular Reactor deployment and extended reactor lifespans, projects a 7.8% compound annual growth rate, pushing demand toward 95 million Separative Work Units per year by the end of the next decade.

These projections represent a structural shift from the subdued demand environment that characterized the post-Fukushima period. Current installed global enrichment capacity stands at approximately 90 million Separative Work Units, with incremental expansions planned by Urenco, China National Nuclear Corporation, and Orano. However, even under optimistic capacity expansion assumptions, the Reference Scenario points to a potential global enrichment shortfall beginning after 2034. Under the Upper Scenario, this deficit arrives earlier and deepens significantly, creating a supply-demand imbalance that could persist for years.

Russian Dominance and Western Diversification Imperatives

Global enrichment capacity is dominated by four producers: Rosatom of Russia, Urenco (a consortium of the United Kingdom, Netherlands, and Germany), Orano of France, and China National Nuclear Corporation. Russia's Rosatom controls approximately 27 million Separative Work Units of annual capacity, representing nearly one-third of the global total and a position of unparalleled influence over the nuclear fuel supply chain.

This concentration creates systemic risk. Western utilities have historically relied on Russian enrichment services due to their cost competitiveness and reliability. However, geopolitical tensions and sanctions imposed following Russia's invasion of Ukraine have exposed the strategic vulnerability of this dependency. The United States, which sources roughly 25% of its enrichment services from Russia, has moved to ban imports of Russian enriched uranium, while European utilities are accelerating their diversification efforts.

Western Fuel Cycle Independence and Uranium Feedstock Security

The Western pivot away from Russian enrichment services is driving a fundamental reassessment of uranium feedstock security. Enrichment facilities require a steady supply of uranium concentrate, commonly known as yellowcake, to produce Low-Enriched Uranium. As Western utilities diversify enrichment contracts toward Urenco, Orano, and prospective domestic capacity, the demand for secure, non-Russian uranium feedstock is intensifying.

The United States faces a particularly acute supply challenge. American utilities consume approximately 50 million pounds of uranium annually, yet domestic production capacity, even when fully ramped, reaches only 4 to 5 million pounds per year. Stephen Roman, President and Chief Executive Officer of Global Atomic, quantifies the supply deficit:

"Our mine will produce as much as every uranium mine combined in the US. They're burning 50 million pounds a year and they're making everything ramped up, maybe four or five million pounds a year in the United States. So there's a big delta there."

This mismatch underscores the strategic importance of American producers capable of delivering feedstock into the conversion and enrichment chain. Energy Fuels operates the White Mesa Mill in Utah, the only conventional uranium mill in the United States, processing uranium ore into yellowcake that supplies domestic conversion infrastructure. enCore Energy, through its in-situ recovery operations at the Rosita and Alta Mesa projects in Texas, is delivering new domestic feedstock aligned with the Department of Energy's capacity goals.

Conversion Capacity Constraints and Sequential Dependencies

Conversion capacity represents the second midstream bottleneck in the nuclear fuel cycle, and its constraints are as material as those in enrichment. Conversion facilities transform uranium concentrate into uranium hexafluoride, the chemical form required for enrichment. Under the Reference Scenario, conversion requirements are projected to rise at a 5.5% compound annual growth rate, reaching over 100,000 tonnes of uranium per year by 2040. Yet global conversion capacity remains concentrated in a handful of facilities in France, Canada, the United States, Russia, and China, with limited expansion planned in the near term.

Western conversion capacity operates near full utilization, and several facilities face aging infrastructure and regulatory constraints. The closure or prolonged maintenance outages at key plants could trigger supply disruptions, forcing utilities to draw down inventories or compete for limited spot capacity. This vulnerability has not gone unnoticed by policymakers. The United States government has initiated funding programs to support domestic conversion capacity, recognizing that enrichment independence is meaningless without a secure conversion supply chain.

The interdependence between conversion and enrichment creates a multiplier effect on uranium demand. As enrichment capacity expands to meet Western diversification goals, conversion facilities must scale in parallel. IsoEnergy has established toll milling agreements in Utah, allowing the company to process ore from its high-grade Canadian deposits through American infrastructure. American Uranium's in-situ recovery project in Wyoming aligns with America's front-end expansion, benefiting from the state's regulatory framework and proximity to existing infrastructure.

Global Atomic's Dasa Project in Niger offers a complementary source of non-Russian, near-term supply. Niger is a Tier-1 uranium jurisdiction with established mining infrastructure and stable production history. The Dasa deposit's high grade and proximity to existing processing facilities enable low capital intensity development, positioning Global Atomic to deliver feedstock into global conversion chains independent of Russian or Kazakhstani supply. Niger represents a strategic counterweight to Russian and Central Asian exposure.

ATHA Energy, with its large landholding in Canada's Athabasca Basin, represents long-term feedstock potential. The Athabasca Basin hosts some of the highest-grade uranium deposits globally, and Canada's stable regulatory environment and historical role as a major uranium exporter provide jurisdictional security. As Western utilities prioritize secure, high-grade feedstock, explorers with significant Athabasca exposure are positioned to capture strategic value through exploration success and eventual resource development.

Troy Boisjoli, Chief Executive Officer of ATHA Energy frames the supply-side risk:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career… The real demand that's being built up coupled with some of the supply side risk, is a setup like we have not seen in the uranium space."

Small Modular Reactors and High-Assay Low-Enriched Uranium Demand

Small Modular Reactors represent a paradigm shift in nuclear technology, offering scalable, factory-fabricated designs that reduce construction timelines and capital intensity compared to traditional large-scale reactors. Many advanced reactor designs, including Small Modular Reactors, require High-Assay Low-Enriched Uranium fuel, which is enriched to between 5% and 19.75% Uranium-235, significantly higher than the 3–5% enrichment used in conventional reactors.

High-Assay Low-Enriched Uranium enables longer fuel cycles, smaller reactor cores, and improved thermal efficiency, making it essential for next-generation reactor economics. However, commercial-scale High-Assay Low-Enriched Uranium production in the West remains limited. The Department of Energy has established the High-Assay Low-Enriched Uranium Availability Program, contracting with Urenco, Centrus Energy, and Orano to develop domestic High-Assay Low-Enriched Uranium supply.

Quantifying SMR Contribution to Enrichment Demand

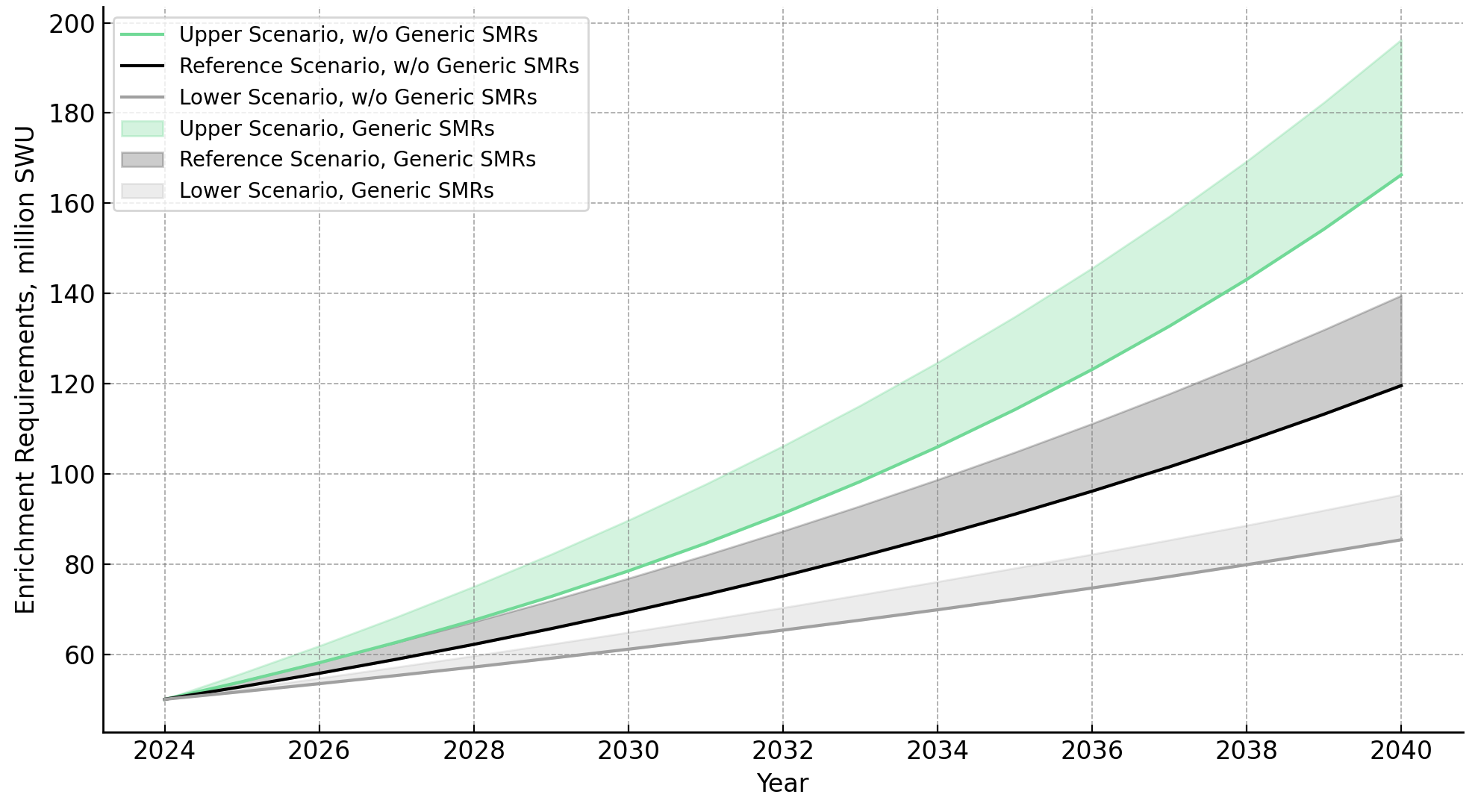

Under the Reference Scenario, generic Small Modular Reactor deployment is expected to require approximately 3.7 million Separative Work Units per year by 2035–2040. This represents a notable deployment pace, with Small Modular Reactor demand commencing by the end of the current decade and increasing annually at a moderate pace. By the end of the next decade, Small Modular Reactors could account for over 10% of global enrichment requirements.

The Upper Scenario envisions accelerated Small Modular Reactor adoption beginning in the late 2020s, with Separative Work Unit deliveries required as early as 2026. Under this trajectory, Small Modular Reactor demand is projected to increase by an average of 1.8 million Separative Work Units per year, exceeding 29 million Separative Work Units of annual requirements from 2040 onward. Dev Randhawa, Chairman and Chief Executive Officer of F3 Uranium, frames the demand urgency:

"Whoever wins the race to have more scalable green energy has a better chance of winning the AI wars… They want energy that's base load and scalable… There's only one energy in the world that's clean and scalable, base load nuclear."

High-Grade Feedstock and Advanced Reactor Supply Chains

Small Modular Reactors alter enrichment economics by requiring higher Separative Work Units per fuel unit, even without proportional reactor growth. This structural shift creates incremental demand for uranium feedstock, as each kilogram of High-Assay Low-Enriched Uranium requires more natural uranium input than conventional Low-Enriched Uranium. High-grade deposits offer economic advantages in High-Assay Low-Enriched Uranium supply chains due to lower conversion costs and reduced environmental footprint per unit of output.

F3 Uranium, with its high-grade Tetra Zone discovery in Saskatchewan's Patterson Lake corridor, is positioned for long-term Small Modular Reactor-linked demand. As Small Modular Reactor demand scales, high-grade Canadian projects represent strategic feedstock sources for Western High-Assay Low-Enriched Uranium programs.

Myriad Uranium’s Wyoming project hosts the largest-known uranium reserves in the United States, offering potential High-Assay Low-Enriched Uranium feedstock scale. The project's conventional mining profile aligns with renewed interest in non-in-situ recovery supply, a shift driven by technical challenges in some in-situ recovery districts and utility preferences for diversified feedstock sources.

Laramide Resources is working with the Department of Energy's Los Alamos National Laboratory on in-situ recovery and groundwater restoration technology, aligning with High-Assay Low-Enriched Uranium infrastructure goals. This collaboration positions Laramide at the intersection of technical innovation and policy support, an advantage as the Department of Energy scales domestic High-Assay Low-Enriched Uranium capacity.

Geopolitical Bifurcation and Supply Chain Localization

Enrichment and conversion now represent critical fronts in energy independence, with Western alliances coordinating industrial policy to de-risk the nuclear fuel cycle. The United States, Canada, the European Union, and Australia are establishing bilateral uranium agreements and funding programs to expand domestic enrichment capacity and secure feedstock supply. These initiatives reflect a broader strategic shift: nuclear energy is no longer viewed solely as a climate solution but as a pillar of national security and economic competitiveness.

China and Russia are simultaneously building parallel fuel cycles, increasing bifurcation risk for global utilities. Chinese investment in enrichment capacity, coupled with Russia's continued dominance, creates a bifurcated market where Western utilities must compete for limited non-Russian supply. This bifurcation is driving premium pricing for Western-sourced uranium and enrichment services, a dynamic that institutional investors are beginning to recognize in equity valuations.

Mark Chalmers, President and Chief Executive Officer of Energy Fuels, observes the urgency among new market entrants:

"It's not just utilities, It's the tech companies that realize they need the power, they need the base of energy. It bodes well for the interest and the realization that you're going to need material quantities and a lot of companies are trying to go upstream to get their position now because they're afraid there will be no position later if they don't move."

Pricing Dynamics and Capital Market Response

Enrichment capacity constraints are translating into higher conversion and uranium prices, incentivizing mine restarts and new exploration. Western uranium equities are now trading at enterprise value per pound premiums compared to historical troughs, supported by institutional rotation into nuclear as a core decarbonization and energy security investment. Companies with low all-in sustaining costs and scalable infrastructure are best positioned for margin expansion as enrichment tightens.

Development capital is flowing into the sector at unprecedented levels. Energy Fuels raised $600 million through a convertible note offering, while ATHA Energy have completed equity placements to advance their projects. Philip Williams, Director and Chief Executive Officer of IsoEnergy, highlights the cost reality:

"The actual real price of getting that marginal pound of production out of the ground is much higher than anyone thinks. When you're producing less than your nameplate capacity, your fixed costs are going over a much smaller amount of pounds, so your per pound cost is higher. Those numbers will ultimately get into the market and it will be a surprise to everybody in the space."

This cost dynamic suggests that long-term uranium pricing must rise significantly above current levels to incentivize the supply necessary to meet enrichment demand. For investors, this creates a favorable setup: structural demand growth, constrained supply, and rising marginal costs, a combination that has historically driven sustained commodity price appreciation.

The Investment Thesis for Uranium

- Structural demand growth drives enrichment requirements beyond installed capacity, with a global deficit likely after 2034 and earlier under accelerated Small Modular Reactor deployment scenarios.

- Policy-driven repricing creates durable tailwinds for domestic producers as Western governments localize the fuel cycle, encompassing conversion, enrichment, and feedstock supply.

- Front-end leverage positions companies supplying uranium concentrate into Western circuits, Energy Fuels and enCore Energy to capture premium pricing as utilities prioritize supply chain security.

- High-grade optionality offers asymmetric upside through explorers and developers such as ATHA Energy, F3 Uranium, Global Atomic, IsoEnergy, American Uranium, Laramide resources and Myriad Uranium as Small Modular Reactor demand scales and High-Assay Low-Enriched Uranium programs mature.

- Environmental, social, and governance considerations converge with security priorities, directing superior capital flows toward projects aligning with government policy, environmental standards, and geopolitical diversification objectives.

Fuel Cycle Integration as the New Investment Framework

The enrichment and conversion deficit is not a temporary imbalance but a structural constraint reshaping uranium markets through 2040. As governments anchor nuclear policy around energy security, uranium producers capable of feeding the front end of the cycle become critical infrastructure rather than commodity suppliers. For institutional investors, the opportunity lies in identifying producers with secure access to Western conversion and enrichment infrastructure, favorable cost structures, and jurisdictional alignment with policy priorities. The uranium investment thesis has evolved beyond mine supply, it now centers on fuel cycle integration and energy independence.

Read more:

Part 6 - Conversion Supply and Demand

Part 5 - Uranium Supply and Demand

Part 2 - Nuclear Energy Security Imperatives

TL;DR

Global uranium enrichment capacity is heading toward a structural deficit after 2034 as demand accelerates at 5.6-7.8% annually through 2040, driven by reactor restarts and Small Modular Reactor deployment. Russia controls 27 million Separative Work Units of capacity, creating strategic vulnerabilities that are forcing Western utilities to diversify away from Russian supply. The resulting bottleneck extends beyond enrichment to conversion facilities, which must transform uranium concentrate into the hexafluoride feedstock required for enrichment. This midstream constraint is reshaping investment opportunities, favoring producers with access to Western processing infrastructure, particularly in the United States and Canada. As governments prioritize fuel cycle independence, uranium producers capable of feeding Western enrichment capacity are positioned to capture premium pricing and institutional capital flows.

FAQs (AI-Generated)

A Separative Work Unit measures the effort required to enrich uranium by separating Uranium-235 from Uranium-238. It's the core metric for tracking enrichment capacity and demand, similar to how barrels measure oil production. Investors should monitor SWU dynamics because enrichment capacity constraints directly affect how much mined uranium can be converted into reactor fuel, creating bottlenecks that drive uranium pricing.

Current global enrichment capacity stands at approximately 90 million SWUs annually, but demand is projected to grow 5.6-7.8% per year through 2040, reaching 120-165 million SWUs depending on the scenario. Even with planned expansions by Urenco, Orano, and China National Nuclear Corporation, the gap between demand and supply widens significantly after 2034, particularly under accelerated Small Modular Reactor deployment scenarios.

Russia's Rosatom controls approximately 27 million SWUs of annual enrichment capacity—nearly one-third of the global total. The United States sources roughly 25% of its enrichment services from Russia, creating strategic vulnerability similar to Europe's dependence on Russian natural gas. This has prompted Western governments to ban Russian enriched uranium imports and invest in domestic enrichment capacity, driving demand for secure, non-Russian uranium feedstock.

Small Modular Reactors require High-Assay Low-Enriched Uranium (HALEU) fuel enriched to 5-19.75% U-235, significantly higher than conventional reactors' 3-5%. By 2035-2040, SMRs are expected to require 13.7 million SWUs annually under the Reference Scenario, potentially exceeding 29 million SWUs under accelerated deployment. This creates incremental uranium demand because each kilogram of HALEU requires more natural uranium feedstock than conventional Low-Enriched Uranium.

Producers with access to Western conversion and enrichment infrastructure hold strategic advantages. United States domestic producers like Energy Fuels (operating the only conventional uranium mill in the U.S.) and enCore Energy (in-situ recovery operations) benefit from government prioritization of domestic supply. Canadian producers with high-grade deposits—including IsoEnergy, F3 Uranium, and ATHA Energy—offer jurisdictional stability and toll milling access to U.S. processing infrastructure. Companies aligned with Western fuel cycle localization are positioned to capture premium pricing as utilities prioritize supply chain security.

Analyst's Notes

Subscribe to Our Channel

Stay Informed