Antimony Has Become a Security Commodity & Western Governments Are Betting Billions to Catch Up

China's antimony export controls drove prices to $27.50/lb before demand destruction pulled them back to $14.50/lb. Western supply chains are rebuilding.

- Antimony has shifted from a niche industrial input to a security-classified commodity, with government stockpiling now driving prices alongside traditional supply and demand.

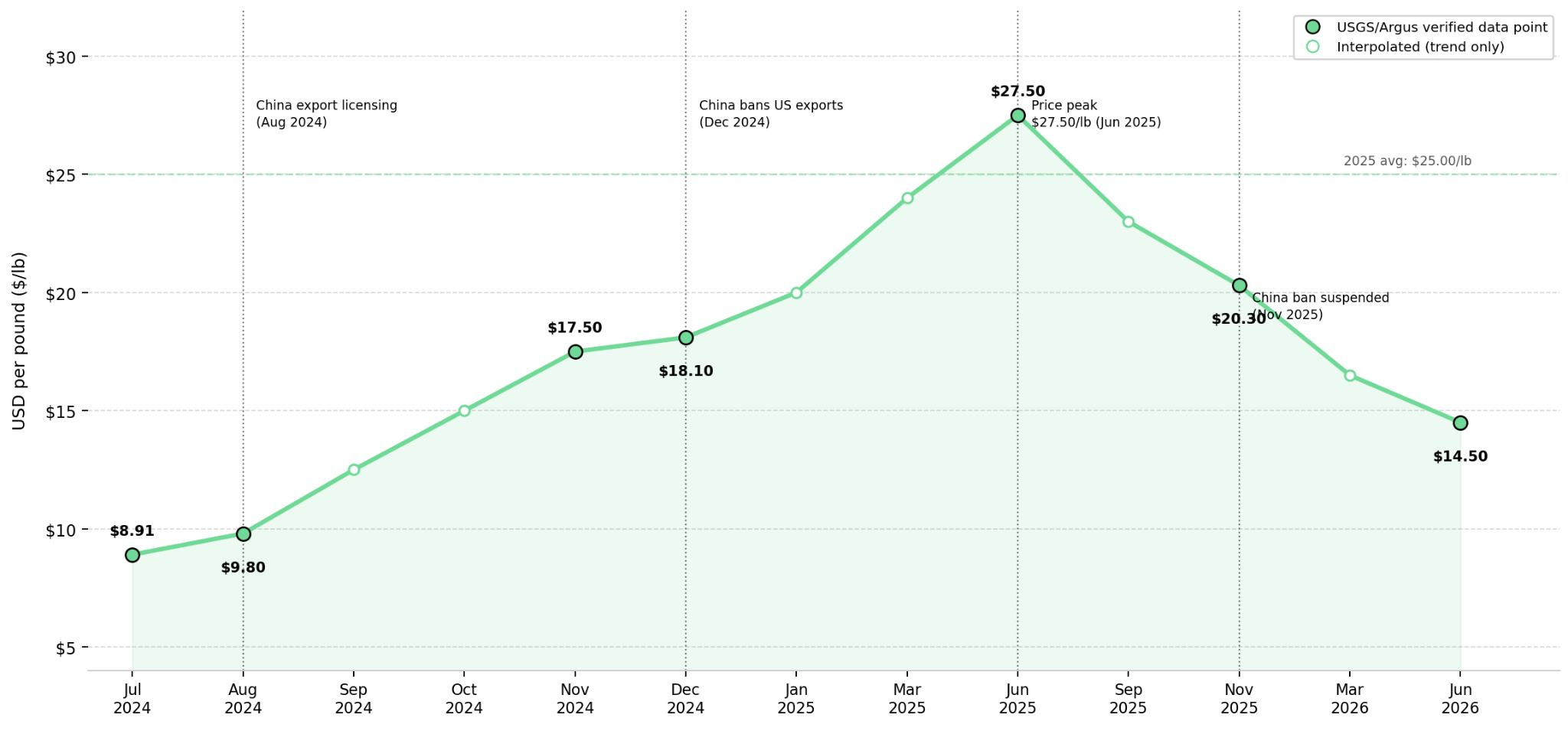

- China's antimony export controls escalated from licensing (August 2024) to an outright US ban (December 2024), then suspension (November 2025–November 2026). Licensing and the military-use ban persist, so renewed-cutoff risk, not normal trade, sustains the price premium.

- Western antimony rose from $9.80/lb (August 2024) to a $27.50 peak (June 2025), fell to $20.30 (November 2025), then $14.50 by June 18, 2026, per USGS/SMM, driven mainly by demand destruction and new supply, not China's export policy.

- The US and Australia have moved from monitoring antimony supply chains to funding them directly, including a conditional Department of War award to an Idaho antimony developer and Australia's A$1.2 billion Critical Minerals Strategic Reserve, announced in January 2026.

- Producers with existing mining and processing infrastructure, including byproduct antimony already embedded in operating silver mines, may capture near-term value faster than early-stage exploration projects.

China's Production Dominance Creates a Binary Supply Risk for Antimony Buyers

For most of the past century, antimony was a commodity nobody outside metallurgy and chemical manufacturing paid attention to. It hardens lead in batteries, acts as a flame-retardant synergist, and features in ammunition primers, semiconductors, and fiber optics. What changed is not the classification itself, which has been applied since 2018, but the policy attached to it: the 2025 Federal Register revision of the US critical minerals list reaffirmed antimony's inclusion, and Australia has separately named it a priority mineral under its new federal reserve, triggering funding eligibility and stockpile authority that did not exist a decade ago.

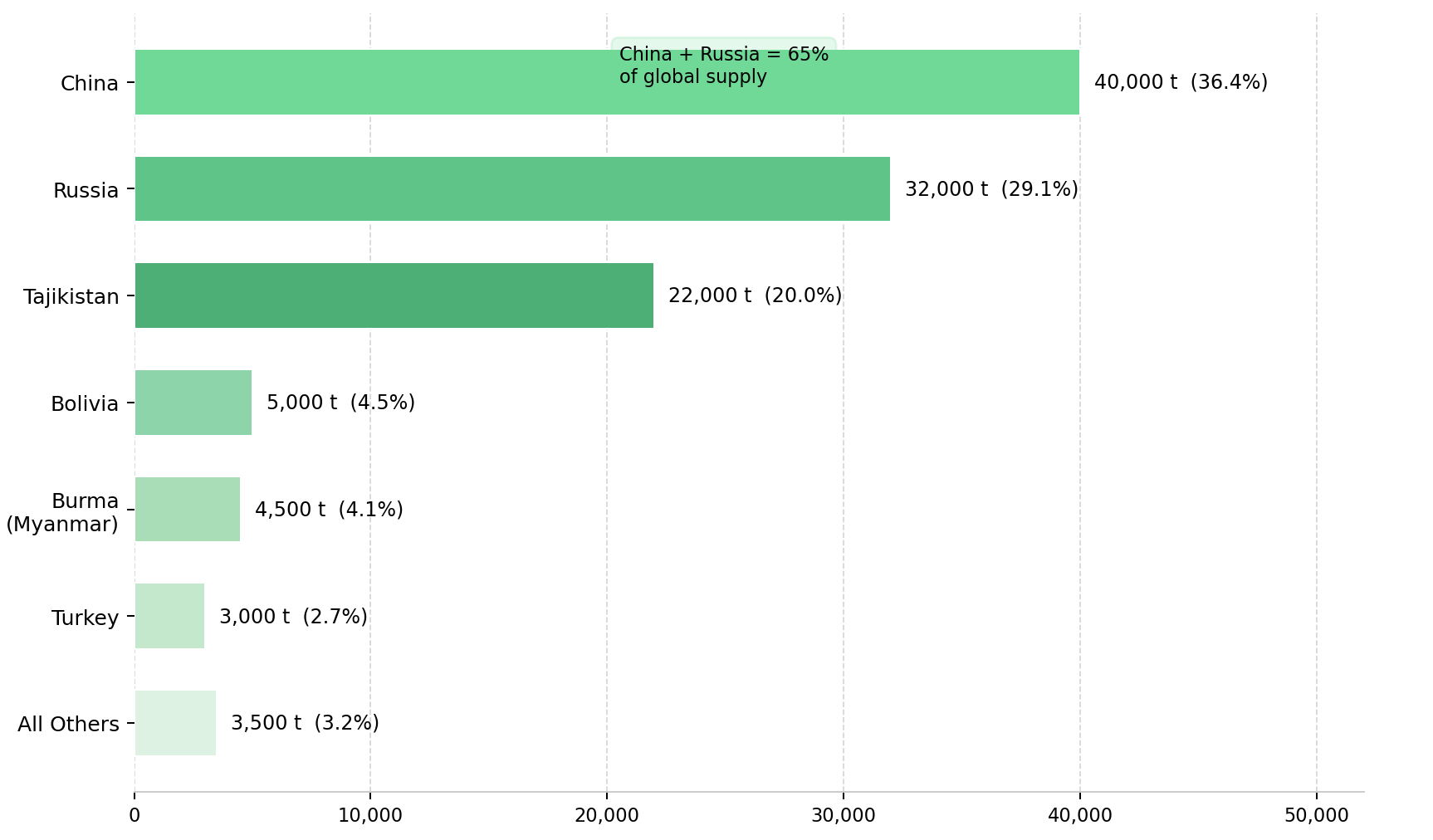

World reserves exceed 2 million tons, and China's 2025 mine production of roughly 40,000 tons accounted for approximately 36 percent of the estimated 110,000-ton global total, per USGS data, with the remainder split among Russia, Bolivia, Tajikistan, Australia, and Myanmar. For a Western buyer, that concentration is a binary risk: supply is available until a single government decides otherwise, and the past two years have shown this is no longer theoretical.

China's Export Policy Created Antimony's Risk Premium

China announced export controls on antimony in August 2024, requiring licenses for ore, metal, oxide, and related technology. By December 3, 2024, Beijing escalated to an outright prohibition on antimony, gallium, germanium, and superhard materials destined for the US, alongside a separate, still-active ban on dual-use mineral exports to US military end users.

China suspended the broader prohibition on November 9, 2025, running until November 27, 2026, though the military-use restriction remains permanently in force and no further extension or reversal has been confirmed. The market reaction was immediate and disproportionate to any actual change in physical supply, as defense contractors and flame-retardant manufacturers without inventory buffers competed for non-Chinese material at almost any price, establishing supply-chain risk as a standalone pricing factor.

Price Signals Are Driving Capital Back Into the Sector

Sustained pricing, not a single spike, is what underwrites mine development decisions, because financiers discount future cash flows using base-case price assumptions that span years, not weeks. The metal price climbed from $9.8 per pound in August to $18.10 per pound in December, continued higher into a mid-2025 peak, then eased and averaged $25 per pound across all of 2025, more than double the 2024 average, but the price decreased to $20.30 per pound in November.

That easing has continued into 2026: as of June 18, 2026, US antimony metal averaged $14.50 per pound against $11.80 per pound in Europe and roughly $7.66 per pound for China's domestic benchmark, according to Shanghai Metals Market.

Most of that decline predates China's export ban suspension and instead reflects the 2025 spike correcting itself: CRU Group and Fastmarkets both attribute it primarily to demand destruction and to new supply, expanded Southeast Asian processing capacity and higher-cost marginal production drawn in by the price highs. The China-Western gap has narrowed but not closed, which is the more durable signal: a sustained, multi-year premium over the Chinese price, not the absolute price level, is what clears a feasibility study hurdle rate.

The Economics of Antimony Development

Antimony rarely justifies a standalone mine. Most producible antimony arrives as a byproduct of silver, gold, or base-metal ore bodies, so cut-off grades and recoveries are set by the host metal, not antimony content. Net present value and internal rate of return calculations for byproduct antimony streams carry far less downside sensitivity to price assumptions than a standalone deposit would, since the primary metal already covers most costs. A standalone project must clear its full cost structure on antimony pricing alone, a materially higher bar, which is why government-backed offtake agreements and stockpile commitments are increasingly substituting for conventional financing tests.

Government Policy Is Becoming a Market Participant

Antimony pricing is no longer set purely by industrial buyers and producers. Over the past eighteen months, the US and Australia have moved from monitoring critical mineral supply chains to actively funding them.

The US' Push to Rebuild Domestic Capacity

The DOE announced intent to issue nearly $1 billion in funding opportunities on August 13, 2025, targeting mining, processing, and manufacturing technologies across critical mineral supply chains, citing national security and energy dominance as primary objectives.

The Department of War has already made a conditional funding award of $80 million to an Idaho-based antimony mining project, per USGS Mineral Commodity Summaries, showing federal capital now flowing directly into project-level antimony development.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold & Silver, described the government's push to replenish critical metal reserves:

"We are now seeing critical reserves in these metals being built: stockpiles of silver, that's stockpiles of antimony, uranium, all of these other critical metals that the US government wants to have available to them... We've talked about the US Antimony Joint Venture submitting a white paper to the US government and getting them involved in what we're doing."

Australia's Strategic Reserve Model & the Rise of Commodity Insurance

Australia announced a A$1.2 billion Critical Minerals Strategic Reserve on January 12, 2026, naming antimony a priority mineral alongside gallium and rare earth elements. The reserve, administered by Export Finance Australia, supports stockpiling, offtake agreements, and contracts for difference, the last of which functions as commodity insurance: government guarantees a floor price in exchange for assured future supply, directly improving project financeability.

Building Domestic Supply Chains Requires More Than Mining

Mining concentrate is the easier half of the antimony supply chain to reshore. Converting concentrate into flake metal, oxide, or trisulfide requires smelting infrastructure that is scarce, capital-intensive, and slow to permit, meaning processing capacity, not mine output, is the binding constraint on substitution for Chinese material.

Why Vertical Integration Is Becoming a Competitive Advantage

United States Antimony, operator of the only active antimony smelter in the country at Thompson Falls, Montana, began mining its own feedstock nearby in November 2025, per the USGS, putting mining and smelting under one roof and reducing the transportation and counterparty risk standalone operators carry.

Emerging US Antimony Supply Chain

That same logic now applies at Americas Gold & Silver's Galena Complex in Idaho's Silver Valley. In February 2026, Americas Gold & Silver and United States Antimony formed a joint venture, Americas holding the majority interest and United States Antimony serving as managing member, to build a dedicated processing facility at Galena.

Why Existing Producers May Hold an Advantage Over Greenfield Projects

Not every company exposed to antimony carries the same risk profile. Producers with operating mills, permitted infrastructure, and existing offtake relationships face a different path than explorers still working toward a maiden resource estimate, a distinction that matters more in antimony than most commodities because so much supply arrives as a byproduct of an already-operating mine. Galena has produced silver, copper, and antimony together for years; United States Antimony's own Montana mine only began production in November 2025.

The Value of Existing Infrastructure

Turner has described Galena as holding over 200 million ounces of silver resource at roughly 500 grams per tonne, among the higher-grade silver deposits globally, with antimony and copper arriving alongside that silver without a dedicated mine plan or capital budget. Turner frames the byproduct economics as incremental revenue layered onto production the company would undertake regardless:

"For every additional ton that we mine for the high-grade silver, we get with it for free additional high-grade copper and antimony… What we're doing with these initiatives, the new tech agreement and the US Antimony Joint Venture, is maximizing the revenue from what we're already mining… these byproducts are extremely helpful in bringing down costs over time."

What Would Cause Prices to Fall & What to Monitor

Antimony's recent rerating has already partly reversed, and the reasons are mostly structural rather than political. The price peaked at $27.50 per pound in June 2025, then fell to $20.30 per pound by November 2025, before China's export ban suspension took effect, and continued sliding to $14.50 per pound by June 18, 2026, per USGS and Shanghai Metals Market. Industry trackers including CRU Group and Fastmarkets attribute the bulk of that decline to demand destruction, the price spike itself suppressed downstream consumption from photovoltaic glass and flame-retardant manufacturers, and to new supply responding to high prices, including expanded Southeast Asian processing capacity and higher-cost marginal mines drawn into production. China's November 2025 suspension is a secondary factor narrowing the China-international gap further into 2026, not the cause of the initial fall.

The more direct forward risk to the thesis is a different one: a durable, unrestricted resumption of Chinese exports, rather than the partial, reversible suspension already in effect, would remove the supply-chain risk premium rather than merely compress it.

The forward signals are now demand and supply-side as much as political: whether photovoltaic glass and flame-retardant demand stabilizes or keeps softening, whether Southeast Asian and Tajik supply growth continues to outpace Western reshoring, and whether China's suspended export ban lapses or is extended again ahead of its November 27, 2026 expiration.

The Investment Thesis for Antimony

- Antimony has become a strategic commodity driven by national security priorities layered on top of, not replacing, industrial demand, making supply-chain resilience a durable, multi-year theme rather than a short-lived reaction to one policy announcement.

- Government funding programs, strategic reserves, and contracts for difference are measurably reducing commercialization risk for qualifying projects.

- Producers with existing mining and processing infrastructure, including byproduct antimony streams embedded in operating silver mines, carry lower execution risk than greenfield developers, and vertically integrated supply chains spanning mining through finished metal are positioned to capture more value than standalone concentrate producers.

- Standard mining metrics, including all-in sustaining cost, net present value, internal rate of return, reserve quality, and permitting status, remain the relevant lens for this exposure, not the critical-minerals narrative alone.

Antimony's investment case is being shaped as much by export licensing decisions in Beijing and stockpile budgets in Washington and Canberra as by geology. The next phase may depend on whether Western governments can convert policy ambition into operating mines, commissioned smelters, and drawn-down reserves before the next disruption arrives.

TL;DR

China's antimony export controls, escalating from licensing in August 2024 to a full US ban by December 2024, triggered a price surge from $9.80/lb to a $27.50 peak before falling back to $14.50 by mid-2026. The disruption exposed how dependent Western industries are on a single supplier for a mineral critical to flame retardants, ammunition, and semiconductors. Governments are now direct market participants: the US conditionally awarded $80 million to an Idaho antimony project, while Australia launched a A$1.2 billion Critical Minerals Strategic Reserve. Producers with existing infrastructure and byproduct antimony streams carry the lowest execution risk in this environment.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed