Arizona Metals (AMC) - Focus on Copper-Gold VMS is the Plan

Pais, ex broker, and mining research analyst tells us that Arizona Metals is hunting Copper-Gold. Their main asset is the Kay Mine.

Pais, ex broker, and mining research analyst tells us that Arizona Metals is hunting Copper-Gold. Their main asset is the Kay Mine. The second is the Sugarloaf project but is not for now. Money is tight. Both founders have worked together before and cut their teeth on the Telegraph Gold project, which eventually became Castle Mountain and Newcastle Mine sold to Equinox by another group. Arizona Metals is looking to explore and develop this far enough to become interesting for someone else to come in and develop and get it into production.

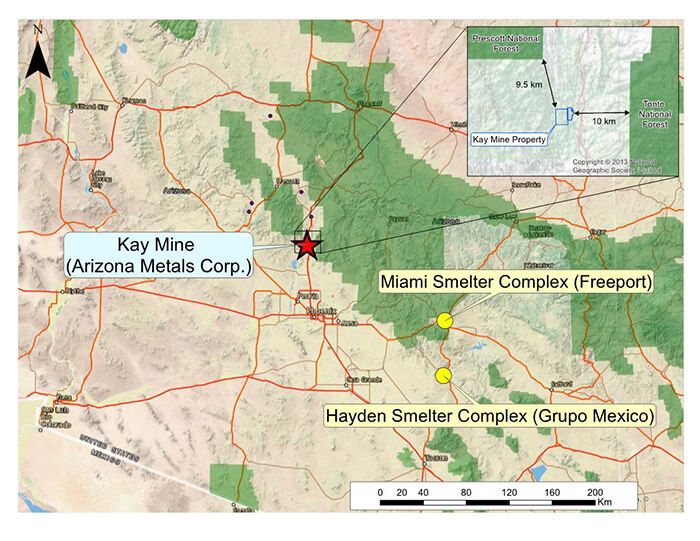

Arizona Metals owns 100% of the Kay Mine Property with a historic estimate by Exxon Minerals in 1982 as a “proven and probable reserve of 6.4 million short tons at a grade of 2.2% copper, 2.8g/t gold, 3.03% zinc, and 55g/t silver”. The mineral reserve categories per the Exxon historical estimate are not consistent with current CIM definitions for proven and probable mineral reserves. The Kay Mine is open for expansion on strike and at depth.

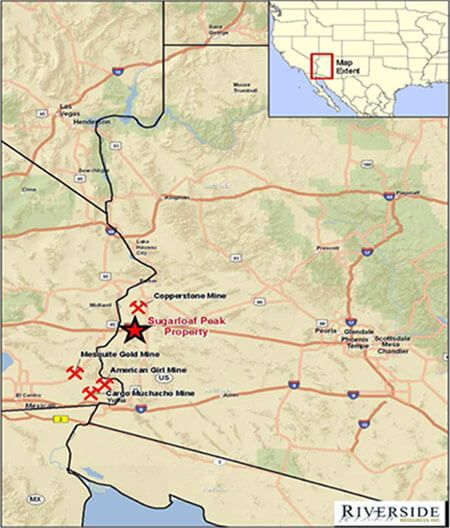

The Company also owns 100% of the Sugarloaf Peak Property, which is a heap-leach, open-pit target and has a historic estimate of “100 million tons containing 1.5 million ounces gold” at a grade of 0.5g/t (Dausinger, 1983, Westworld Resources). The historic estimates at the Kay Mine and the Sugarloaf Peak Property have not been verified as current mineral resources.

We Discuss:

- 1:37 - Company Overview

- 3:01 - Team Experience & History of the Company

- 4:54 - Advice to Self: Lessons Learned & Applied

- 10:32 - Business Plan & Goals to Meet

- 15:45 - Delays and Boundaries

- 17:41 - Polymetallic Potential & Metal Equivalent Alteration

- 22:18 - Delivering Value & Growth: Timing & Money

- 28:47 - Sugarloaf Peak: Opportunity or Distraction?

- 30:44 - Management Remuneration

- 31:26 - Under the Radar: Exciting the Market

Company Overview:

Arizona Metals is a recently listed company and owns 100% of two exploration projects in Arizona and the flagship asset is the Kay Mine, an hour north of Phoenix. The Kay Mine is a high-grade VMS Copper Gold deposit with a historic resource defined in 1982 by Exxon Minerals. It is about 6Mt at 6.4% Copper equivalent, primarily made up of Copper and Gold but hasn’t been explored in the last 40 years until Arizona started their phase one drill programme this January.

The Kay Mine property - Arizona Metals Corporate Presentation Nov. '20

The second project is the Sugarloaf Peak project which is also 100% owned by Arizona, is two hours West of Phoenix and is an open pit target. It also has a historic resource from 1983, a 1.5Moz of Gold at 0.5, so it’s lower grade but Arizona thinks it has good potential. They have just completed a small drill programme there, primarily for metallurgy as they want to show that the deposit can leach before they start spending money on making it bigger.

The Sugar Loaf Peak property - Arizona Metals Corporate Presentation Nov. '20

Kay Mine is the priority at the moment and Arizona is focused on permitting a phase two 11,000m programme out of Kay Mine and expect to start drilling again later this year.

Team Experience and History

The company was founded by Pais and Paul Reid, the Chairman in 2014. Prior to that they had worked together for a number of years in the brokerage business primarily financing junior mining and exploration companies. In 2011, they started a company called Telegraph Gold and raised money to acquire assets primarily in California, the main asset being the Castle Mountain mine, which was a past producing heap-leach open pit mine that had been shut down due to low Gold price and some legal issues. They listed it in 2013 as Castle Mountain Mining and stepped away from the management on the listing, but still remain shareholders. It then became Newcastle Gold and then last year Newcastle Gold merged with two others to form Equinox Mining and the Castle Mountain mine went back into production this year.

They acquired the Sugarloaf Peak Project in 2016 and then in 2019 acquired the Kay Mine which is also Arizona, but high grade. They listed the company last year and started drilling in January.

Business Plan

Pais tells us that plan with the previous company was to find assets with a historic resource that had a significant amount of work done but hadn’t been advanced due to metal prices at the time or another issue that could be overcome now. Sugarloaf Peak has the historic resource from 1983 and hadn’t been worked in 30-years as it was too low grade with the Gold prices at the time.

Kay Mine is very similar as it has a historic resource. When Exxon had the Kay Mine project in 1982 it was considered marginal due to the metal price. Now, 40-years later the deposits remain untouched, the metal price is much better and they are starting off with a decent size resource that they hope to expand, upgrade, de-risk, do the metallurgy, do the background testing and eventually sell. Their goal would be to make it big enough to sell to a mid-tier company or a major company that could put it into production.

Pais explains that the shareholders in their Castle Mountain project did very well out of that project and many of them are the same shareholders that are in this company now. A lot of the value that they captured was related to the Gold price as they acquired the project when the Gold price was very low. They also think that they acquired the Sugarloaf Project and the Kay project at a relatively low part of this cycle with low Gold price and low Copper price. So, there may be value left to capture now by putting the work in through drilling.

The Kay Mine

The key is to show the scale of the project explains Pais. They have to show that the Kay Mine can be much bigger than the 6Mt that was proven by Exxon in 1982, but they had a very narrow focus of where their exploration was. At the Kay Mine the 6Mt is a stark estimate by Exxon as defined over a strike length of 320m. Arizona has completed a phase one programme which was 6,700m and 20 holes, and they have hit Sulphides on 19 of the 20 holes. The 12th was a bit off target. Arizona Metals is confident in the historic data based on that phase one drilling programme that has really confirmed what Exxon reported.

They have 2 options now. Either drill another 20,000m to prove that 6Mt from historic into 43-101, or to start expanding it. The project is underexplored so there is potential to make it much bigger and they are planning to drill about 500m on strike to the north, and another 300m on strike to the south.

Expansion potential

These areas have never been drilled but the geophysics, soil sampling and rock sampling, is all showing good indication that it does expand in those directions. There are also 2 large targets to the west that have never been tested. In the last 40-years most of the exploration that was focused on the Kay Mine was done from underground and there was very little surface drilling done. The surface drilling was focused below the workings of the Kay Mine. Arizona thinks the real potential to show the scale is to start testing this and to the west of those untested as they think there are potentially multiple Kay type deposits on their claims This is typical in the region and typical for these VMS type deposits and if they can show that it will show the market that this could be a significant land package.

The goal is to make the Kay deposit bigger, prove potential other projects and start the de-risking process. They have started some baseline studies showing water studies and started a desktop metallurgy study too. They are planning the long-term metallurgical testing for the project with SRK, which will increase as they continue to get drill holes.

The ultimate goal is to sell the project to somebody that can build a mine and there are a number of mid tiers or majors that might be interested. Pais thinks that they will need 10Mt at this kind of grade to support a standalone operation and to attract a mid-tier company and this this is an achievable goal but in reality, they hope to make the project significantly bigger.

Drilling programme

Arizona is planning to start an 11,000m programme next month and hope to get a 3rd of the way through it by the end of this year. They finished the phase one programme in August which was delayed by about 2-months because of COVID. They put everything on hold in March for a month to put in the required safety protocols for COVID. They started the permitting process as soon as they completed phase one and expect to receive the drill permit in the next few weeks, which will allow drilling to start in November. Drill results from the lab have also been delayed due to COVID and it taken almost 2-months to get assays compared to the usual two weeks.

The Kay Mine is a Copper-Gold VMS deposit and the metal value in Kay is primarily Copper-Gold but Arizona has done some of the assays in Gold equivalents because on the southern edge of the Kay Mine the deposit switches from being primarily Copper-Gold to being what looks like a Gold-Zinc lens. Here, the Copper value has dropped from 3% to 5% on average, down to 0.1%, so very low Copper but the Zinc rate has increased from 2% up to 10%, and with that very good Gold rates of 4g/t to 6g/t. Arizona sees the southern area as a very important exploration target with potentially a Gold rich Zinc lens there that’s much lower in Copper. Therefore, in some holes, they have reported in Gold equivalents or Zinc equivalents because there’s very little Copper. But the bulk of the 6Mt is Copper-Gold so that’s Copper equivalents.

Delivering value & growth

Arizona has CAD$5M now after completing the phase one programme at both projects. Plus, some of the CAD$3M warrants money is coming in. The 11,000m drilling programme should cost about CAD$2.5M to CAD$3M says Pais. He explains that the geophysics is showing good potential to expand the clay mine by two times on strike to the north and then also double it again to the south. The deposit is defined over 300m of strike and there is 500m untested to the north. There is also a single drill hole from 1993 in the north, a very shallow hole, it was 120m deep and is believed to be the starting depth of the deposit. So, the Kay Mine starts at 120m.

Pais explains that the best wins in the Kay Mine are at about 300m deep where they have a nice zone, 40-metre-wide zone of good grades and that’s what they will be targeting on the strike to the north. Then to the south they have 300m untested, but that’s where it looks like it’s switching into a Zinc-Gold zone. The strike potential is significant and there is expansion potential on the strike too. They also have 2 targets to the west that have never been drilled which starts right at the surface with the same soil, the same rock anomalies, it’s on the same context, the same geological context as the Kay Mine adds Pais.

Then 1,000m west they’ve got the Western convector which is a 70m wide convector, right at the surface, 1,000m of strike, never drilled, with also the same signatures as Kay, the same soil samples, the same rock samples. Arizona plan to start drilling both those convectors and think that either one of those could be another Kay type deposit which would require its own drill programme and that would drive the need for additional capital.

Exciting the market

Arizona has drilled in the phase one programme, had two drills turning, drilled 6,700m, 20 holes, including the break for COVID and it took about four months. Pais suggests that if they were just to focus on the Kay Mine to prove up a 43-101 resource on that 6Mt, they would need another 30,000m of drilling, which would cost about CAD$10M and they could drill that within 12-months. And if they start showing similar grades at the central and western targets, Pais thinks the value will be driven up due to continuity in the Kay Mine drilling as it is typical in these VMS deposits to have multiple lenses in a small radius. He thinks that the market can quickly work out that they are making it much bigger without having to put a resource on it.

Pais admits that Arizona has been under the radar as it’s a fairly new company. He thinks that they will drive the value of the company just with additional drilling and in the phase one drilling programme, they were hitting good results on every hole. These are very good indications that they can drive more value with the phase two programme starting in November and there will be a steady news flow of results from now.

To find out more go to the Arizona Metals website

Analyst's Notes

Subscribe to Our Channel

Stay Informed