Atalaya Mining (ATYM) - 7.3% Dividend Paying Copper Producer

Interview with Alberto Lavandeira, CEO of Atalaya Mining

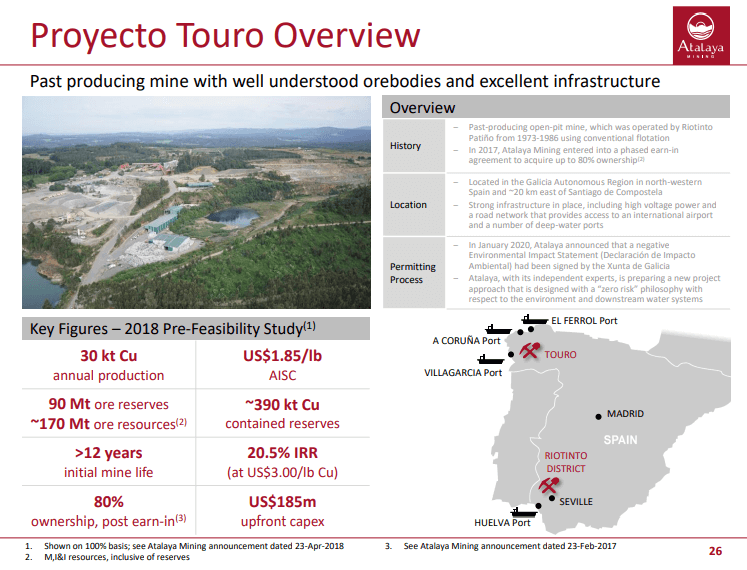

Atalaya Mining is a fast-growing AIM and TSX-listed mining and development company that produces copper concentrates and silver by-products at its wholly-owned Proyecto Riotinto site in southwest Spain and is currently under expansion. The company has a phased, earn-in agreement to acquire up to 80% ownership of Proyecto Touro, a brownfield copper project in northwest Spain that is currently in the permitting stage.

Matt Gordon caught up with Alberto Lavandeira, CEO and Director, Atalaya Mining. Alberto has over 38 years of experience operating and developing mining projects. As CEO, President, and COO of Rio Narcea Gold Mines, he built 3 mines between 1995-2008. He was also involved in the development of the Mutanda Copper-Cobalt Mine (DRC) during this tenure with Samref Overseas S.A. as a Director.

Company Overview

Atalaya Mining strives to become a leading multi-asset copper producer in Europe, maximizing the potential value of its low-cost, low-risk assets and exploring new opportunities. The company was founded in 2004 and is headquartered in Cyprus. EMED Tartessus S.L., Eastern Mediterranean Resources, Atalaya Minas de Rio Tinto Project UK Limited, Winchcombe Ventures Ltd, Tamari, LLC, Emed Mining Spain S.L.U., Atalaya Financing, Limited and EMED Marketing Ltd are the company's subsidiaries. The company is listed on the Toronto Stock Exchange (TSX-V: AYM), and the London Stock Exchange's Alternative Investment Market (AIM: ATYM).

Atalaya Mining is a copper-focused company. The company has been consistently delivering growth through expansion and is generating a healthy cash flow. The company started paying dividends last month and plans to deliver them shortly. The company has a business model that features minimum overheads. It currently has a staff of 500 employees.

ESG Initiatives

The company has forged strong relationships with the neighboring local communities. It recently had a meeting with 6 mayors of the local villages for its social initiatives, employment generation, and contributions. The company's ESG (Environmental Social and Governance) initiatives are a model for the mining community.

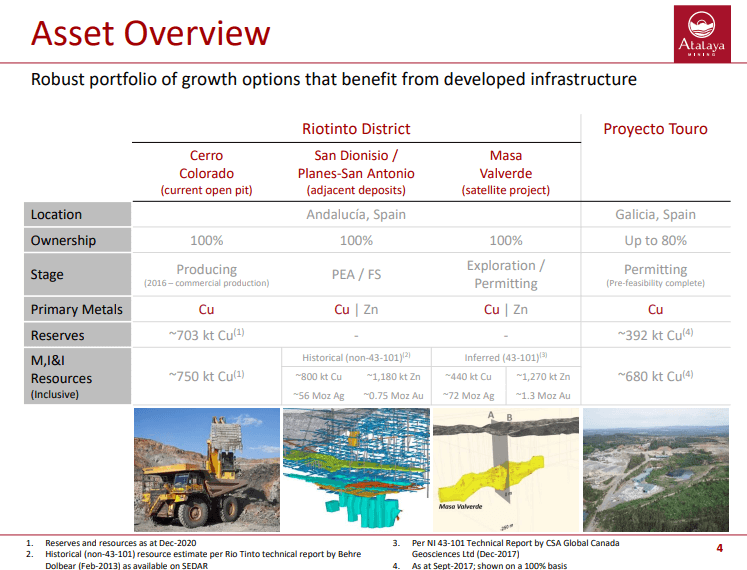

The Riotinto Project

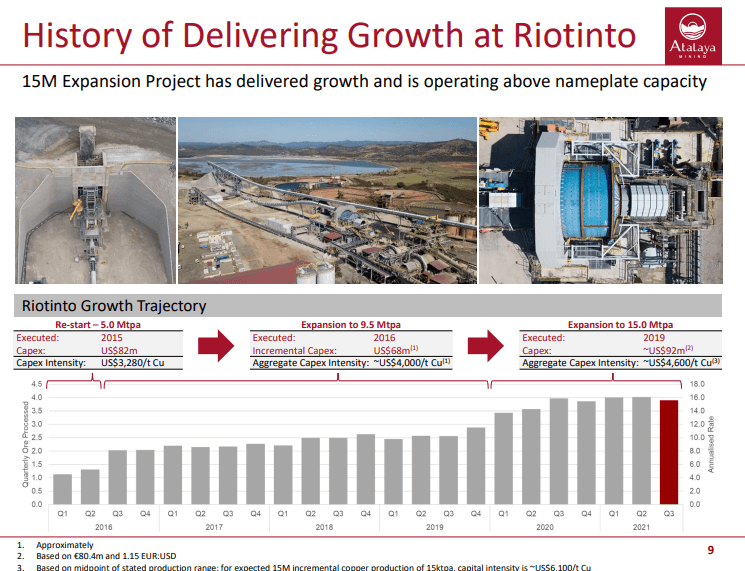

When Atalaya Mining started operations at the Riotinto Project, the mine had a 12-year life with a production rate of 9Mt/year. The Feasibility Study was carried out back in 2013. The company started refurbishing the old installation and initiated drill operations while simultaneously restructuring the plant. During this time period, the company was a 5Mt/year producer. The refurbishment process spanned a duration of 12 months.

During the second year of operations, the company expanded its production capacity beyond 9Mt/year. Over the course of 2 years, the company effectively doubled its copper reserves.

Atalaya Mining was successful in further expanding its operations to 15Mt/year. It is currently processing up to 16Mt on a yearly basis. The current mine life is expected at 12 years running at a higher capacity. Following this, the company plans to carry out an open-pit operation.

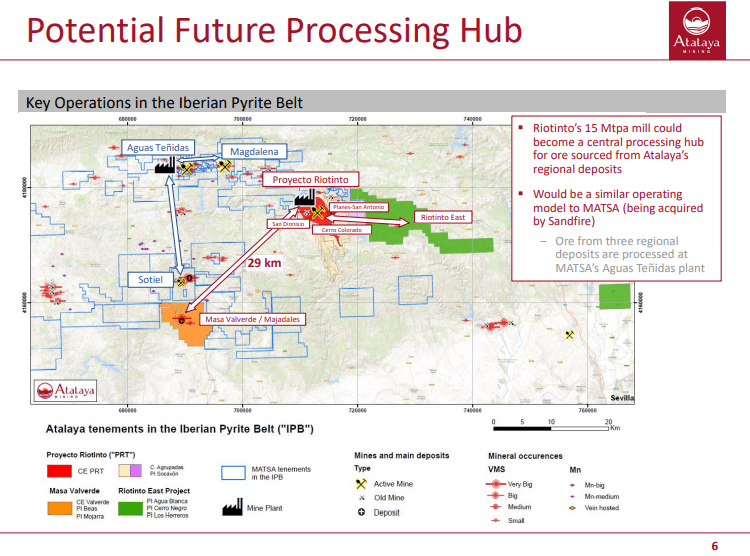

The company's Atalaya pit was historically mined and had a lot of reserves left behind. The company also has the San Antonio metallic deposit, located 1 km from the pit.

The company recently acquired a large deposit 29km away featuring 70Mt-80Mt material. The company has effectively doubled its reserves excluding this new deposit. It aims to increase the production profile of its operations while extending the mine life. This will enable the company to increase the volatility and optionality of its assets.

The company is looking to grow production through the existing plant by processing higher-grade material. The company has significant capacity to process underground and high-grade material. It anticipates that the mine life will extend up to 20 years. The company recently posted strong Q2 and Q3 production numbers.

Atalaya Mining is stockpiling the marginal material, anticipating a jump in the market pricing of copper. Meanwhile, it is using the generated cash flow to reward the shareholders. Once the copper prices rise, the company plans to keep stockpiling reserves at a constant grade. The company has maintained a constant production rate at the Riotinto deposit for the past 4 quarters.

Mining Efficiency Metrics

Atalaya Mining's current operations feature a flotation plant that is running at $50,000/day or $16M/year. This plant has the capability to treat the mineralized material, though it requires periodic removal of waste. The ore-to-waste ratio is 2:1 or lower. Each ton of material passed through the plant requires the removal of 2t of waste. This waste is stockpiled by the company as it contains copper which is currently serving as an ore reserve.

In the past year, the company has focused on plant efficiency, leading to a steady production of 16Mt/year, exceeding the nameplate capacity.

This is a low-grade bulk mining operation. The company's main recoveries come from dumps rather than tailings. This is also called waste rock which contains lower amounts of copper than the reserves. The company stockpiles this waste rock as the cost of extraction has already been incurred. This waste rock can generate revenue once the copper market prices rise.

Cash Position

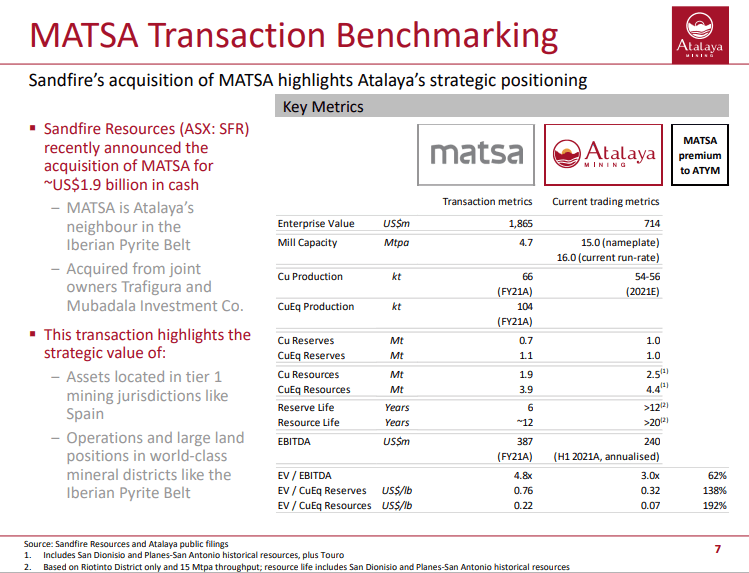

Atalaya Mining posted strong Q3 results in 2021. The company generated €50M in quarterly revenue. The company has a market cap of $650M with a 20% cash flow deal. The company's stocks are low-priced and despite being evaluated 3x lower than comparable enterprises, it has a strong cash flow.

The company's generated cash flow in the past 3 quarters has been $120M. The company has also posted very high EBIDTA (Earnings Before Interest, Taxes, Depreciation, and Amortization) numbers. This has enabled the company to grow its balance sheet and offer dividends.

Atalaya Mining raised capital through equity in the past. Backed by a strong team, it was able to build the mine for $200M instead of the original $300M budget. This demonstrates the company's inclination towards being efficient with capital.

The company plans to offer $50M in dividends to its shareholder base, which accounts for 30%-50% of its free cash flow. At the same time, the company is looking to advance a new project called Tourro, located in northern Spain. This would allow the company to sustain its growth prospects.

The company is aiming at covering all expenditures post-investment pre-taxes through the generated cash flow. This includes the budget for exploration, overheads, and a very low-interest debt.

The company had a negative working capital in 2020. In the past 9 months, it has been successful in generating a cash flow surplus of $80M-$90M. The company's share price jumped by £1 within the past 9 months.

Atalaya Mining was able to grow from €18M in negative working capital in December 2020 to €127M in working capital surplus in a span of 9 months. The company is currently awaiting approvals for the Touro project to generate additional cash flow.

The Masa Valverde Deposit

Atalaya Mining is currently working towards de-risking the Masa Valverde deposit by drilling 2 high-prospect areas. This deposit features mixed reserves of copper, lead, and zinc, a typical feature for the region. This deposit features certain areas with high copper and high zinc reserves. The company is currently infill drilling the areas and seeking areas with anomalies to develop the deposit into a prospective future operation.

Targets 2021 and Beyond

Atalaya Mining is looking to stabilize its operation in 2022. The upcoming challenge would be inflation, leading to a rise in energy and steel prices along with higher operating costs. The company anticipates that this inflation would coincide with a growth in copper prices, enabling the company to maintain its existing margins. The company expects the production numbers and financials to be similar to 2021. It is currently awaiting approvals for its Tourro project, a new and upcoming project with strong growth potential.

M&A Considerations

Atalaya Mining is not looking for a potential M&A (Merger and Acquisitions). The company has 2 major shareholders that collectively own a 44% stake in the company. The remainder of the company's shareholders is institutional in nature. Paired with a strong and experienced local team, there is no M&A activity expected from the company in the future.

To find out more, go to the Atalaya Mining Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed