Bannerman Energy Primed to Deliver on Looming Uranium Supply Deficit with World-Class Etango Project

Bannerman Energy CEO provides update on Etango uranium project in Namibia, funding and offtake discussions, detailed engineering, and expansion/extension optionality.

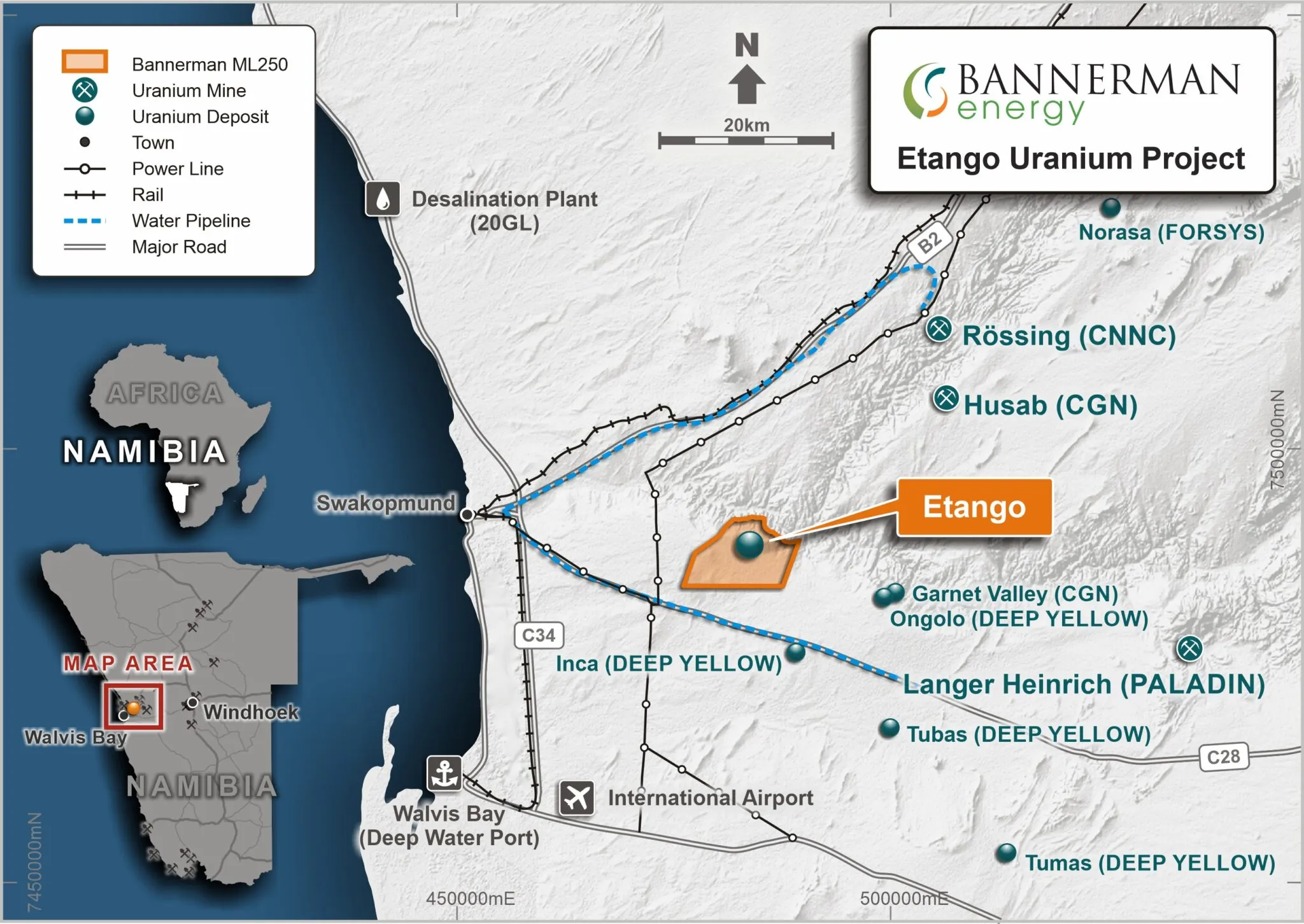

- Bannerman Energy is focused on developing its 8 million ton per annum Etango Uranium Project in Namibia

- The company has evaluated expansion (XP) and extension (XT) options to potentially increase production to 16 Mtpa or extend the mine life from 16 to 27 years

- Strategic funding discussions are ongoing following receipt of the mining license in December; Bannerman has cash to continue detailed design work through year-end

- The company aims to contract 75-80% of production, leaving some uncontracted to benefit if uranium prices rise; discussions are underway with utilities

- Detailed engineering by Wood Group is nearing completion; tendering suggests capital costs in line with the DFS estimate

Primed to Deliver Uranium Into a Rising Market

Bannerman Energy (ASX:BMN) provided updates on the company's Etango Uranium Project in Namibia and its funding and development plans. With a mining license in hand and strengthening uranium market fundamentals, Bannerman is focused on advancing the 8 Mtpa development while evaluating options to expand or extend the project to capture further upside.

Interview with CEO Gavin Chamberlain

Expansion and Extension Studies Provide Optionality

Chamberlain explained that Bannerman recently completed conceptual studies examining two potential options to build upon the 8 Mtpa base case development:

"We decided we needed to really put some numbers to it that we can talk to. So we spent the last 3 months evaluating 2 options. One option, which we call XP, is the expansion option, which would take us from 8 million tons to 16 million tons throughput. The other option was XT, which is an extension option where effectively we leave the plant as it is, but we run the life of mine from 16 to 27 years."

The expansion case would require significant capital but could allow Bannerman to scale up production to capture rising uranium demand and prices. The extension case provides greater flexibility by doubling the operating life with minimal additional capital.

Chamberlain reiterated that Bannerman's immediate focus remains on the 8 Mtpa base case, with the XP and XT options representing potential future growth opportunities. Having the studies completed provides strategic optionality:

"These 2 options are just potential future extensions to the life of mine and all the production... The idea of being able to use the flexibility of having additional tons available to Bannerman as a whole is extremely attractive to us. Potentially we will contract in a large portion of our initial tonnage, and if the market continues to move, it will mean that we have additional tonnage available to us that is uncontracted and that's financially extremely attractive."

Funding Discussions Advancing

Following the granting of Etango's mining license in December, Bannerman has seen an uptick in interest from potential financiers and partners. The company is pursuing a dual-track funding process evaluating both a strategic approach and traditional debt/equity financing.

While the details remain confidential, Chamberlain indicated discussions are progressing well. Importantly, with A$35 million in cash, Bannerman has the financial strength to complete detailed engineering through year-end while the optimal funding package is assembled.

On the strategic front, the company is in discussions with utilities on long-term contracting to underpin the project financing. Chamberlain said Bannerman is targeting 75-80% of production under long-term contracts, but aims to keep a portion uncommitted. This would allow the company to reserve some production to sell into the spot market if uranium prices continue to rise.

Detailed Engineering On Track

Detailed engineering work on Etango by lead engineer Wood Group is well advanced, keeping the project on track for a development decision upon completion of financing. Chamberlain said the company went to market to tender packages representing 80% of the total capital cost, providing a high degree of confidence in the DFS estimate.

While not all tenders are complete, Chamberlain said the company has been pleasantly surprised by the competitiveness of construction contractor pricing. This provides a buffer against potential capital cost escalation impacting other projects.

-With the mining license in hand, Bannerman Energy is firmly focused on advancing its world-class Etango uranium project against the backdrop of a strengthening uranium market. The completion of detailed expansion and extension studies provides strategic optionality to build on the solid 8 Mtpa base case development.

The company is making steady progress with funding discussions and detailed engineering. Management is taking a prudent approach, aiming to lock in long-term sales contracts to support financing while preserving exposure to rising uranium prices. With a strong cash buffer and encouraging initial construction tender results, Bannerman is well positioned to be among the next wave of global uranium development projects.

The Investment Thesis for Bannerman Energy

- Etango is one of the few uranium projects globally with a mining license and completed DFS, substantially de-risking the asset

- The 8 Mtpa base case development has robust economics at current uranium prices, with expansion/extension options providing additional upside

- With A$35 million in cash, Bannerman is well funded to complete detailed engineering and advance offtake/financing discussions

- Management is taking a conservative approach to contracting, aiming to lock in long-term contracts to underpin financing while preserving exposure to further uranium price upside

- Competitive construction contract tenders and advanced detailed engineering provide confidence the project can be developed in line with DFS capex estimates

Macro Thematic Analysis

The global energy transition is increasingly recognizing the role nuclear power must play in providing reliable, zero-carbon baseload electricity. This is driving a fundamental shift in the outlook for nuclear fuel demand, with the sector moving from a decade of oversupply to a growing structural deficit.

The uranium market is entering a period of sustained demand growth against the backdrop of constrained supply. Mines shuttered during the prolonged bear market will take time and significant capital to restart. Crucially, a lack of investment in new projects has left the pipeline of new supply exceptionally thin.

This supply crunch is being exacerbated by an increase in long-term contracting by utilities looking to lock in future requirements amid rising concerns about fuel security. The situation has been thrown into even sharper relief by recent geopolitical events, which highlight the concentration risk of today's primary uranium supply.

These factors are underpinning a strong pricing outlook, with the incentive price for new developments estimated at US$70-80/lb U3O8 – well above current spot prices. Assets like Bannerman's Etango, with completed feasibility studies and mining approvals in place, are exceptionally well-placed to fill the looming supply gap.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed